The big rebound is on! But don’t worry, your opportunity to grab big gains (and dividends) hasn’t evaporated.

There’s still time!

And you can start with 3 of the 4 funds I pounded the table on back on February 19. At the time, all 4 of these cheap selloff buys were paying a combined 13.4% income stream.

So why are just 3 of these funds still worthy of your attention, only a few weeks later?

I’ll unpack that—and name these 3 top-flight funds—in a moment. First, let’s step back and take a look at what happened in a very wild February, and where it all leaves us now.

A Market Disaster Gets Undone

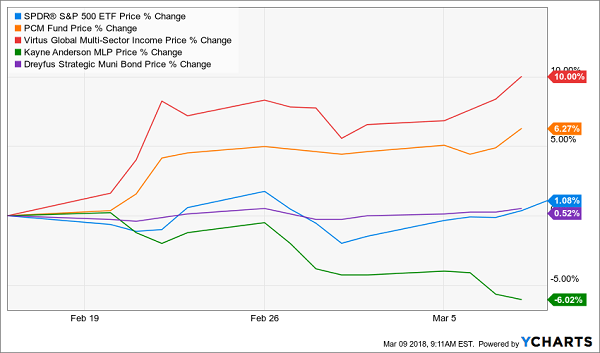

So much has happened. First, the S&P 500 (SPY) did this:

Was It All a Dream?

The good news is, the stock market losses we saw at the start of the month are now history.

The even better news is that the S&P 500 is up just over 3% from the start of 2018, meaning this market isn’t overheated. That “goldilocks” position should be giving investors more confidence that now is the right time to get back into the game.

It also means time is running out if you haven’t gotten back in already.

And if you’re sitting on cash?

No problem. I’ll show you where to put that cash to work without overpaying too much for the wrong investments.

But before I get to that, let’s take a look at those 4 funds I earmarked in February. They were the PCM Fund (PCM), the Virtus Global Multi-Sector Income Fund (VGI), the Kayne Anderson MLP Investment Company (KYN) and the Dreyfus Strategic Municipal Bond Fund (DSM).

How do these funds look now?

A Quick Improvement

While the warm weather—and a corresponding drop in natural gas and heating oil demand—has weighed on the master limited partnership–focused Kayne Anderson fund, the average return for these picks since I pointed them out, about two weeks ago, is 2.7%, while the S&P 500 is down slightly since then.

In other words, if you’ve heard that buying a low-fee index fund is the right thing to do, just take a look at that chart.

So What Now?

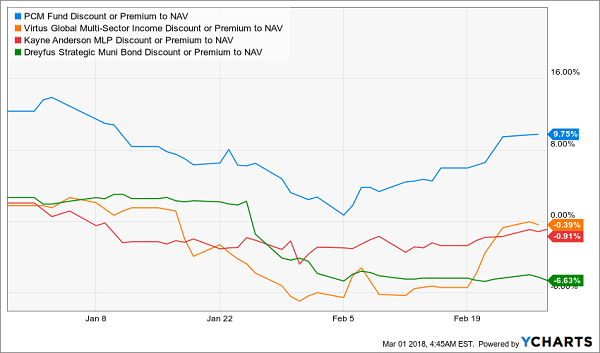

To determine which of these funds remain compelling options, we need to look at their discount to net asset value.

This is where we compare the market price for these funds, which trade daily like normal stocks, and their NAV, which is based on the market price of every item in their portfolios.

Now you’d think an efficient market would make these two figures the same, right? Wrong!

That’s because these are closed-end funds, a little-known corner of the market that’s worth around $300 billion, compared to the multi-trillion-dollar mutual fund and ETF universes. (If you’re unfamiliar with CEFs, click here for an easy-to-follow primer I recently wrote on these cash machines.)

The small size of the CEF market means a lot of big investors who could profit from these inefficiencies don’t bother—and it also means a lot of mom-and-pop investors don’t know these funds even exist.

That’s our opportunity.

The 4 funds I’ve shown you are all CEFs, and, of course, none of them are trading at their NAV (although two do come close):

3 Bargains—and 1 Ship That’s Sailed

First, let’s tackle the PCM Fund, which trades at a 9.8% premium to its NAV, meaning it’s priced above the actual market value of its portfolio. That’s because PIMCO, the fund manager, is great at beating the market, so the market rewards them with a premium.

But a near double-digit premium is too rich for my blood, so this isn’t the best fund to buy right now. And if you nabbed PCM at its unusually low premium earlier in February, you might want to consider getting out or, at the very least, holding on and allocating cash to other investments.

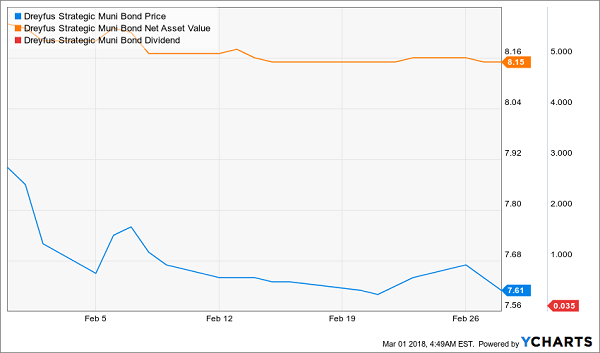

Meanwhile, the Dreyfus Strategic Municipal Bond Fund sports a discount to NAV that has widened since my February 19 article—but investors haven’t really lost any money since I recommended it. How is that possible?

Simple: the fund’s price has slid, but the NAV is staying straight.

Stable NAV, Lower Price

And since investors are still getting the fund’s 5.5% dividend yield, they’re pocketing a strong income stream while they hold on. And since it’s gotten even cheaper, despite the fact that the fund’s real, intrinsic value hasn’t changed, it’s something worth considering if you have cash to spare.

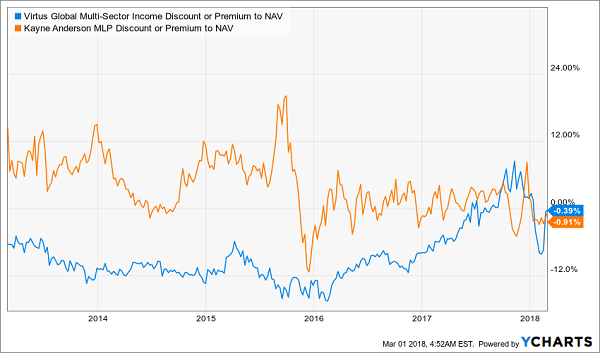

Now let’s hit the Virtus Global Multi-Sector Income Fund and the Kayne Anderson MLP Investment Company. Both funds are trading close to their NAV, and both are paying massive dividends—12% and 10.6%, respectively. So should income investors hold on or buy more?

To answer that question, we’ll take a look at this chart showing where their discounts to NAV stand relative to history:

The Big Picture

This chart makes one thing clear: KYN is now cheaper than it’s been through most of its history, where it tends to trade at a premium to NAV. On the other hand, VGI’s discount, while off a bit from the last few months, is narrower than it usually is.

That makes one thing clear: buying more KYN and waiting for it to revert to its historical mean looks like a smart move, while cautiously adding VGI is also practical, since it’s a strong fund with a very good portfolio.

So if you’re sitting on cash, 3 of these funds still deserve your attention. And thanks to the 500-strong CEF market, there are a lot more out there, too—starting with the 14 I want to tell you about now.

One Click for the 14 Best Funds of 2018

That’s right—you can skim right through all the 500 or so CEFs in the world with just one click and go straight to the 15 funds with the highest yields and biggest gains ahead in 2018 (I’m talking SAFE dividends up to 9.6% and double-digit upside).

All you need is a no-risk 60-day trial to my CEF Insider service. And your timing is perfect, because I’m making a limited number of these trial memberships available now!

Simply CLICK HERE to start your no-obligation trial. When you do, you’ll get instant access to the names, tickers and my complete research on each and every one of the 15 cash machines in the CEF Insider portfolio.

These 15 bargain CEFs all trade at absurd discounts to NAV that are slowly narrowing. That puts unrelenting upward pressure on their share prices and sets us up for a market-crushing gain in 2018!

But the best part—by far—is the dividends.

Right now, the portfolio boasts an average yield of 7.4%. But remember, that’s just the average! Cherry-pick my 3 highest-yielding funds and you’ll be pocketing life-changing payouts like 9.6%, 9.55% and 9.0%!

I hope you’ll take this opportunity to join the small group of investors across the country who are pocketing regular monthly dividend checks from these 15 terrific funds.

Please don't make this huge dividend mistake... If you are currently investing in dividend stocks – or even if you think you MIGHT invest in any dividend stocks over the next several months – then please take a few minutes to read this urgent new report. Not only could it prevent you from making a huge mistake related to income investing, it could also help you earn 12% a year from here on out! Click here to get the full story right away.

Source: Contrarian Outlook