Last week a Federal Energy Regulatory Commission (FERC) ruling sent the MLP and energy infrastructure stocks into a tailspin. The news release caused an immediate 10% drop in the MLP indexes. Prices recovered to close at a 5% decline. A closer read of the facts shows the fears were overblown and this steep drop may end up in hindsight as the MLP sector’s equivalent of the March 2009 bottom of the last stock bear market.

Here is the scary headline from Bloomberg:

Pipeline Stocks Plunge After FERC Kills Key Income-Tax Allowance

The reality is that the ruling only applies to interstate (not intrastate, which is most pipeline miles) pipelines and to just one of the methods a pipeline company can use to set interstate transport rates. Here is how large cap MLP Magellan Midstream Partners, L.P. (NYSE: MMP) explains the effect of the FERC ruling on its business:

“Although Magellan is organized as an MLP, it does not have cost-of-service rates that would be directly impacted by this policy change. Rather, the rates on approximately 40% of the shipments on Magellan’s refined products pipeline system are regulated by the FERC primarily through an index methodology. As an alternative to cost-of-service or index-based rates, interstate pipeline companies may establish rates by obtaining authority to charge market-based rates in competitive markets or by negotiation with unaffiliated shippers. Approximately 60% of Magellan’s refined products pipeline system’s markets are either subject to regulations by the related state or approved for market-based rates by the FERC. In addition, most of the tariffs on Magellan’s crude oil pipelines are established by negotiated rates that generally provide for annual adjustments in line with changes in the FERC index, subject to certain modifications.”

Numerous other large cap MLPs and corporate pipeline companies have issued press releases to state that their business results will not be affected by the FERC ruling. It appears that few pipelines have rates set using the “cost of service” rules.

Related: A High-Yield Stock That’s Better at 15% Than One at 20%

In the bigger picture, MLP values have been falling since late January. Over the same period companies in the sector reported 2017 fourth quarter results that were very positive. MLP fundamentals have been improving for several quarters, and the trend will continue as North American oil and gas production continues to grow.

15 MLPs in the Alerian MLP Infrastructure Index raised distributions and the other 10 kept them level. There were no reductions. This combination of falling market values against strong fundamentals reminds me very much of the bottom of the last bear market which occurred in March 2009. At that time, it seemed that nothing would stop the market decline. In hindsight that point in time was when stocks reached what I politely call “stupidly cheap” prices. Currently quality MLPs look “stupidly cheap.”

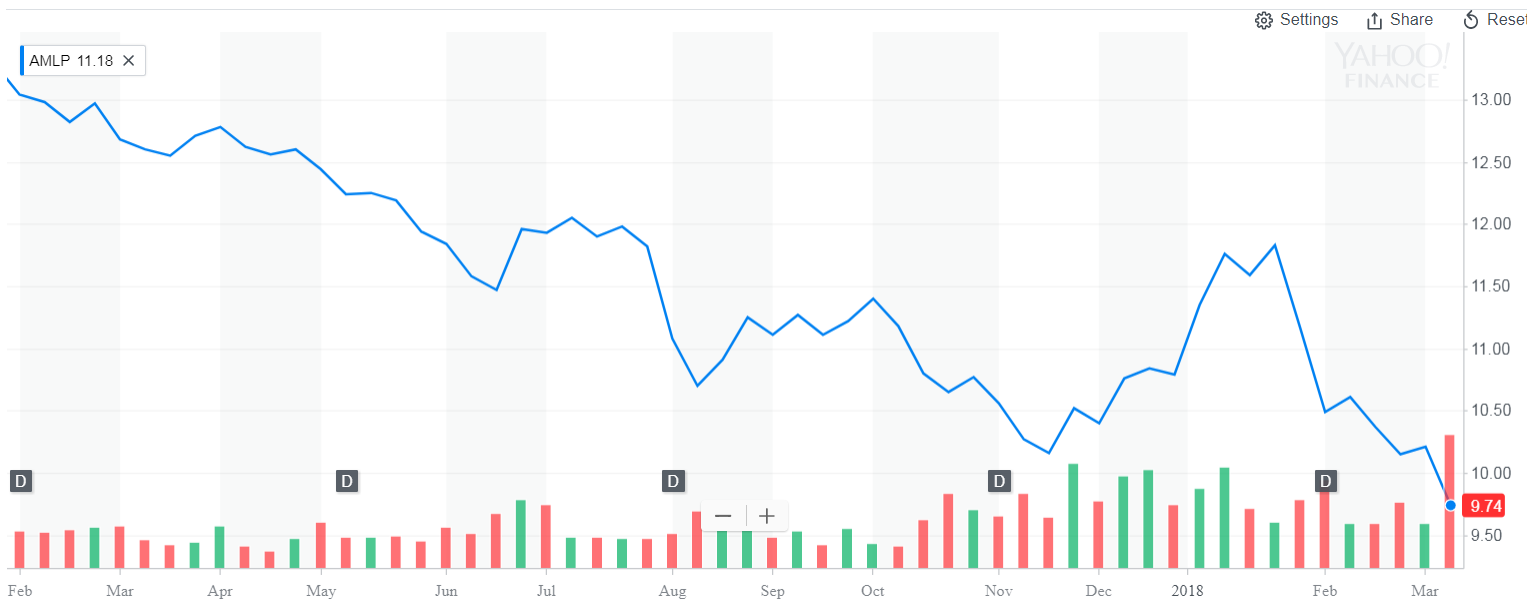

Here are the bear market charts of the SPDR S&P 500 ETF (NYSE: SPY) for the 2007 to 2009 bear market compared to the Alerian MLP ETF (NYSE: AMLP) bear market which started in February 2017. If MLPs form a bottom here, the pattern points to significant gains over the next few years.

If you own quality MLPs that have fallen in value, it is a good time to add more to your positions. In my Dividend Hunter newsletter, my primary MLP recommendation is the InfraCap MLP ETF (NYSE: AMZA). This ETF pays monthly dividends which benefit from option selling by the fund managers. After the big FERC fueled drop, AMZA yields over 17%.