Year-to-date my Hidden Yields subscribers have booked total returns (including dividends) of 155%, 30% and 27%. These profits inspired a common question:

“How’d Brett know when to sell?”

Most investors focus on buying. But selling is an ignored art. And leave it to savvy readers like you to recognize this.

I believe in letting winners run, of course, especially with respect to dividend growers. Sometimes there’s never any reason to actually sell a stock if the dividend’s sponsor is consistently growing its profits and dishing them with shareholders.

Other times, however, we’re better off booking gains and re-deploying our money to more promising pastures. Which brings us back to my readers’ prescient question – how’d I know, because they want to be able to identify sell signals, too.

Remember, there are three ways a stock can pay us:

- With a dividend today,

- By repurchasing its own shares (to make each remaining one intrinsically more valuable), and/or

- By boosting its payout tomorrow so that its stock price follows its dividend higher.

Our Hidden Yields formula focuses on the third – and most lucrative – strategy. It’s led us to 24.3% annualized returns to date. But it takes a few months worth of patience to achieve these gains, because we give up the most obvious strategy – dividends today – in exchange for this price upside tomorrow.

Sell Signal #1: Slowing Dividend Growth

Which means if a dividend grower isn’t growing that payout fast enough, we should move on.

Earlier this year, warehouse landlord and Hidden Yields alumni First Industrial (FR) raised it quarterly payout by 3.6%. That may be enough to excite more “basic” dividend investors, but it doesn’t cut it for us.

FR had been fine for us. In nearly two years, my readers and I saw its payout climb by 14%. We enjoyed 21% price gains too. Add up our dividends and our share appreciation, and we banked 27% total returns.

FR Gains: 21% Price + 6%+ Dividends = 27% Total Returns

“Fine” dividend growth isn’t enough for us, however. So we parted ways as friends and put FR back on our watch list.

Sell Signal #2: Low “Relative” Yield

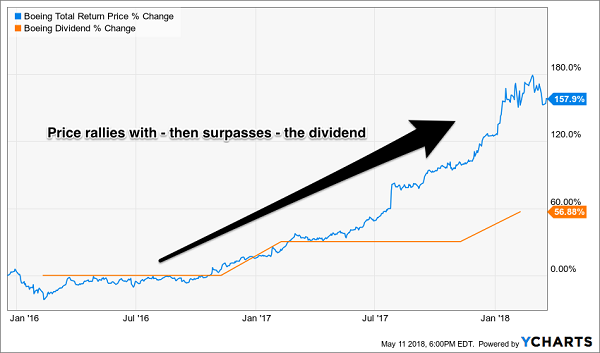

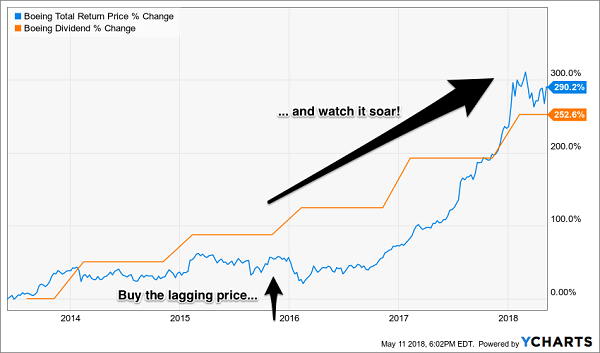

If you want to make real money with stocks, you should always put your money with the faster dividend grower. Boeing was a great example – we added it to the Hidden Yields portfolio in December 2015. Two massive dividend raises since have sent the stock soaring to the tune of 157% total returns for us:

Boeing Soars With Its Payout

Our catalyst was the 57% cumulative “raise” from Boeing, which in turn rocketed its stock price higher. It certainly helped that we bought shares when they were a coiled spring, due to “catch up” with the firm’s ever-growing payout.

Blue Line (Price) Was Due to Catch Up – and It Did

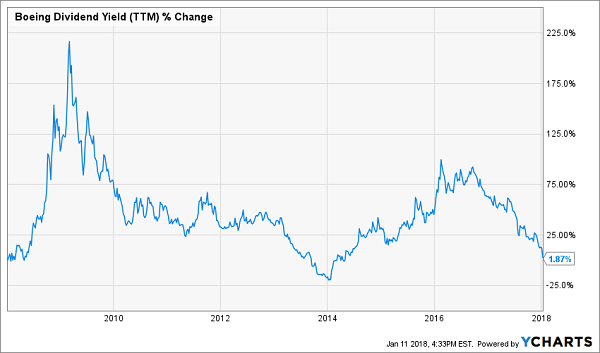

But the curse of high prices is low yields. And Boeing’s price moonshot cratered its current yield:

The Curse of a High Price: A Low Yield

Could shares keep moving higher? Sure. But we’re not in the “buy and hope” business. We banked our 157% gains and put our cash into the next 100%+ mover.

Such as? I’ll share seven stocks with similar setups in a minute. First, let’s wrap up this lesson with our third potential warning flag.

Sell Signal #3: Business is Fine Today, But Looks Dicey Tomorrow

“First-level” dividend growth investors look in the rearview mirror, fawn over past payout increases, and declare a stock an “aristocrat” simply because its past performance is good.

Warren Buffett, the guy who made a fortune on Coca Cola (KO) and inspired countless copycats who saw their late money grind sideways, said it well:

“If past history is all there was to the game, the richest people would be librarians.”

When you and I buy next year’s payout today, we need to picture the future. Are we looking at a retail REIT that is having its rent checks intercepted by Amazon (AMZN)? Or are we looking at an Amazon-proof retailer that is actually a bargain due to overblown worries?

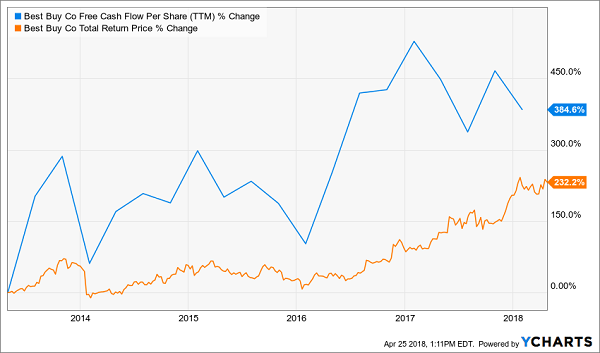

Let’s consider the case of Best Buy (BBY), which boldly decided to take Amazon head-on in 2012 when turnaround CEO Hubert Joly took the helm. And not only did the electronics giant live to tell about it, but it’s now leveraging Jeff Bezos’ website as a shopping channel of its own!

In recent years, Joly has been smartly “doubling down” on the quality of its retail stores (which Amazon doesn’t have). This has powered impressive free cash flow (FCF) growth, which has in turn driven serious stock returns:

Expert Service. Unbeatable Stock Price.

What else doesn’t Amazon have? A dividend, of course. Meanwhile Best Buy pays one, and its growth has been spectacular. Joly & Co. just raised their dividend by 32%. This “high velocity payout” is now up 165% in the last five years! It’s a big reason investors have enjoyed 232% returns in the face of regular Amazon fears.

We dividend hounds don’t get the benefit of hindsight. We must determine up front whether the light at the end of a tunnel represents brightening prospects – or a train rolling in to smash our firm’s entire business model.

This Friday: 7 Fast Dividend Growers with Bright Futures and 100%+ Upside

Life is too short to waste our time with middling dividends! Since share prices move higher with their payouts, there’s a simple way to maximize our stock market returns: Buy the dividends that are growing the fastest.

Don’t be fooled by modest current yields. They often don’t capture the growth potential (and it’s the dividend’s velocitythat really makes us big money – not its starting point).

How to we buy high velocity dividends, the aristocrats of tomorrow? It’s a simple three-step process:

Step 1. You invest a set amount of money into one of these “hidden yield” stocks and immediately start getting regular returns on the order of 3%, 4%, or maybe more.

That alone is better than you can get from just about any other conservative investment right now.

Step 2. Over time, your dividend payments go up so you’re eventually earning 8%, 9%, or 10% a year on your original investment.

That should not only keep pace with inflation or rising interest rates, it should stay ahead of them.

Step 3. As your income is rising, other investors are also bidding up the price of your shares to keep pace with the increasing yields.

This combination of rising dividends and capital appreciation is what gives you the potential to earn 12% or more on average with almost no effort or active investing at all.

Please don't make this huge dividend mistake... If you are currently investing in dividend stocks – or even if you think you MIGHT invest in any dividend stocks over the next several months – then please take a few minutes to read this urgent new report. Not only could it prevent you from making a huge mistake related to income investing, it could also help you earn 12% a year from here on out! Click here to get the full story right away.

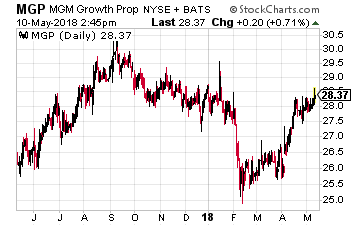

In April 2016, hotel and gaming company MGM Resorts International (NYSE: MGM) spun off about two-thirds of its hotel properties into a new real estate investment trust (REIT) IPO. MGM structured the new company, called MGM Growth Properties LLC (NYSE: MGP), to have a high level of cash flow safety to pay the planned dividend and with the potential for future growth.

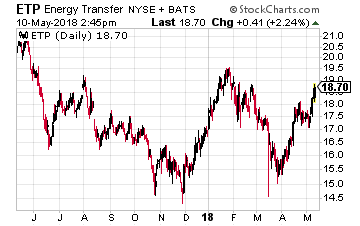

In April 2016, hotel and gaming company MGM Resorts International (NYSE: MGM) spun off about two-thirds of its hotel properties into a new real estate investment trust (REIT) IPO. MGM structured the new company, called MGM Growth Properties LLC (NYSE: MGP), to have a high level of cash flow safety to pay the planned dividend and with the potential for future growth. At the end of 2017 I forecast that the energy midstream/infrastructure sector would return to valuation growth in 2018 providing lots of upside potential in the group. Through 2017 MLP sector market values declined sharply even as business fundamentals continued to improve. 2018 should be the year when investors realize very attractive returns from the quality companies in the sector.

At the end of 2017 I forecast that the energy midstream/infrastructure sector would return to valuation growth in 2018 providing lots of upside potential in the group. Through 2017 MLP sector market values declined sharply even as business fundamentals continued to improve. 2018 should be the year when investors realize very attractive returns from the quality companies in the sector.

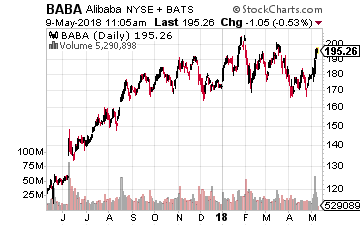

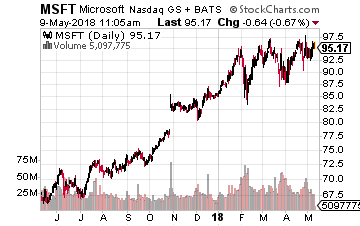

In the first category – algorithms – the U.S. has a lead, but it is narrowing fast. China’s growing capabilities were evident in the good showing by Chinese researchers in the annual ImageNet competition for image recognition or when relative newcomer Alibaba (NYSE: BABA) tied perennial powerhouse Microsoft (Nasdaq: MSFT) in a reading comprehension test for AI.

In the first category – algorithms – the U.S. has a lead, but it is narrowing fast. China’s growing capabilities were evident in the good showing by Chinese researchers in the annual ImageNet competition for image recognition or when relative newcomer Alibaba (NYSE: BABA) tied perennial powerhouse Microsoft (Nasdaq: MSFT) in a reading comprehension test for AI.

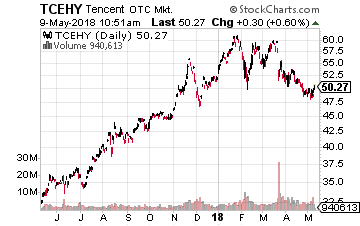

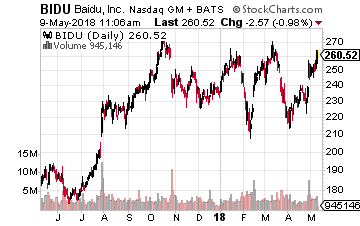

However, some of the very best Chinese AI companies are either still in the start-up stage or their stocks trade only in China. That leaves the three national champions, the so-called BAT stocks – Baidu (Nasdaq: BIDU), Alibaba and Tencent Holdings (OTC: TCEHY).

However, some of the very best Chinese AI companies are either still in the start-up stage or their stocks trade only in China. That leaves the three national champions, the so-called BAT stocks – Baidu (Nasdaq: BIDU), Alibaba and Tencent Holdings (OTC: TCEHY).

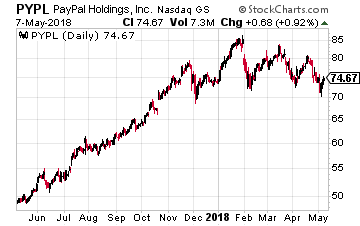

It has had a history of being a successful disruptor. And it will enter the payments space with several distinct advantages. These include a network of more than two million merchants, 100 million Amazon Prime users and those 30 million users already of Amazon Pay.

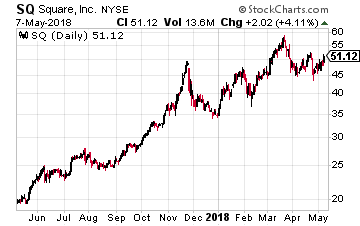

It has had a history of being a successful disruptor. And it will enter the payments space with several distinct advantages. These include a network of more than two million merchants, 100 million Amazon Prime users and those 30 million users already of Amazon Pay. Square is still up solidly for the year, but that is largely due to Bitcoin hype. Famed short-seller Andrew Left said recently that the stock was rising solely due to Bitcoin mania from investors and that Square was a “collection of yawn businesses.”

Square is still up solidly for the year, but that is largely due to Bitcoin hype. Famed short-seller Andrew Left said recently that the stock was rising solely due to Bitcoin mania from investors and that Square was a “collection of yawn businesses.”