Markets traded flat on Friday as they absorbed the latest in the Elon Musk saga, and as pundits began to ponder the possibility of a protracted trade war with China. Tesla (TSLA) has vowed to stand behind its embattled CEO as the SEC is leveling charges of fraud surrounding his tweet about taking the company private. In its initial thrust, the SEC is demanding that Mr. Musk be removed from the board of Tesla. The stock traded down around 14% to lows not seen since April. As the first full week of tariffs went into effect between the U.S. and China, there appeared to be little movement to resolve the differences between the two countries. The fear now is that unlike Mexico, China may take a firm stand resulting in a lengthy and costly trade war between the two global giants. Tariffs may now dominate headlines well into the fourth quarter.

Cal-Maine Foods (CALM) and Stitch Fix (SFIX) kick off October earnings on Monday. Cal-Maine is up slightly on the year. Last quarter Cal-Maine’s CEO warned that proposed tariffs were impacting feed stock for the egg producer. Analysts will be looking for the concrete impact of those tariffs on Monday. Stitch Fix has done nothing but reward investors after going public late last year. But, some worry that a new service being rolled out by Amazon (AMZN) may cut into the data driven clothing provider’s market share. Investors will want to listen closely to any clues on how competition is impacting the company.

Monday’s economic calendar includes, the PMI Manufacturing Index, ISM Manufacturing Index and construction spending. Construction spending is expected to rise .1% for August. The number is being closely watched as it is a key component in GDP, and economists fear rising prices may be impacting growth. While the FOMC was the focus this week, there are several economic numbers being released next week as the fourth quarter of 2018 gets into gear. Tuesday we’ll see Redbook retail numbers. New mortgage applications, ADP employment, the PMI Services Index and ISM non-manufacturing data will all be released on Wednesday. Jobs will be the focus on Thursday with both the job cuts report and jobless claims being released. We’ll close the first week of October on Friday with employment situation numbers and international trade data.

Tuesday, Pepsico (PEP) and Paychex (PAYX) report earnings. Pepsico should give an update on its recently announced acquisition of SodaStream. Lennar (LEN) and Pier 1 Imports (PIR) report on Wednesday. Analysts will be watching Lennar closely for an update on costs and the lack of construction workers plaguing the industry. Closing out the earnings calendar on Thursday (no earnings are currently scheduled for Friday) are Constellation Brands (STZ) and Costco (COST). Analysts are expecting both strong earnings and an increase in membership levels from the bulk retailer.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

Something strange is happening in the investment-bank and hedge-fund world: a growing sense that the next recession (which, by the way, Wall Street has long been wrongly predicting for years) finally has a due date: 2020.

The number of Wall Street firms predicting this date is staggering.

Bloomberg’s Joe Wisenthal has collected a few predictions, such as one from Moody’s Analytics chief economist Mark Zandi, who said 2020 will be the economic “inflection point,” and Société Générale’s economic team, who said the likelihood of a 2020 recession has risen due to, among other things, a tight labor market and higher borrowing costs.

Even former Federal Reserve Chairman Ben Bernanke is getting in on the act, saying a boom “is going to hit the economy in a big way this year and next year. Then in 2020, Wile E. Coyote is going to go off the cliff.”

Doom and Gloom = Cheap 7%+ Dividends for You

This all sounds scary, but the stock market doesn’t care—it’s been too busy surging to new highs:

What, Me Worry?

Stocks’ 10% year-to-date gain means that, if this trend continues, we’ll see a 13% total return for the S&P 500 for all of 2018. That’s far from the kind of market Wall Street seems to be panicking about.

So let’s dig into the fears behind this gloom and doom, and why there’s nothing to fear at all. Then I’ll show you 2 funds you can buy now that will get you all that is best about this still-strong US economy.

And when I say “best,” I’m talking huge dividends up to 10%, and long-term performance that tops the market’s return, too.

But first, let’s dive into 3 fears that are driving the market today, so we can see what’s setting up the 2-fund opportunity I’ll show you toward the end of this article.

Hysterical Fear No. 1: An Inverted Yield Curve

By far, the biggest panic of 2018 has been over the yield curve.

When the difference between the yield on the 2-year US Treasury and the 10-year US Treasury goes negative for longer than a few days, America falls into recession. This is pretty much clockwork: it’s happened every time for decades, making this the most reliable recession indicator.

And the yield curve—that is, the difference between these two yields—has been narrowing since February 2018, when the market’s last major sell off hit:

A Worrying Indicator?

Note, however, that the fast decline from February to July has abated, and we are now about where we were in July.

This doesn’t mean an inverted yield curve isn’t coming (it still looks likely), but it isn’t coming yet. And since a recession typically happens about 12 to 18 months after the inverted yield curve appears, we still have plenty of time to tap the market’s rising gains (and dividends), starting with the 2 funds below.

Hysterical Fear No. 2: Declining Profits

The second fear is so silly it almost isn’t worth taking seriously—until you realize a close look at this fear shows just how wise it is to buy stocks now.

And that worry is that corporate profits are perfectly positioned to start falling.

That sounds bad—until you look into why they are so well positioned to fall: because they’re so absurdly strong right now.

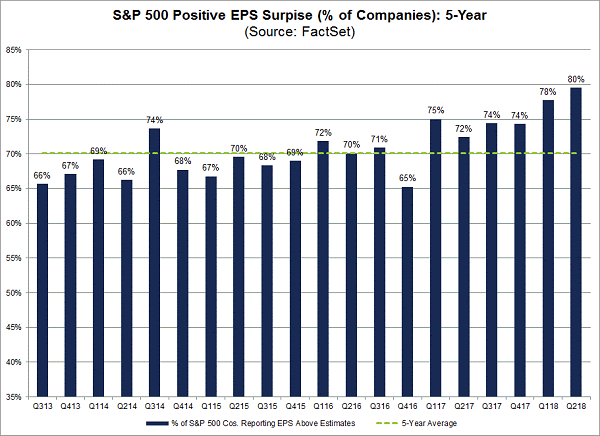

Let me quote FactSet: a “record-high percentage of S&P 500 companies beat EPS estimates for Q2.” That sounds good—and then when you realize just how high expectations were, you realize this isn’t just good, it’s amazing.

Despite expectations of 23% earnings growth (itself higher than the first quarter’s 20% rise), the market reported 25% growth. A staggering 80% of companies beat expectations—far beyond the former record holder, the first quarter of 2018.

Earnings Crush (High) Expectations

Here’s the Chicken Little logic: with earnings growth this high, how can it possibly get any higher?

Of course, this is an old fear we saw in the third quarter of 2014, when oil prices were crashing and pundits warned that a 2008-style disaster was about to unfold. Here’s what the market has done since then:

62% Gains in Just 4 Years

The bottom line? If you sell into today’s fears, expect to miss out on gains like these.

Hysterical Fear No. 3: Tariffs, Tax Cuts and Trump

The 3 “Ts” that are driving many financial fears are largely political, with a lot of attention honing in on two moves by Donald Trump.

The first move was the 2017 tax cuts that many economists have said could overheat the economy. The second, and more alarmist, fear is that Trump’s tariffs, specifically those aimed at China, will result in a trade war that kills US exports.

The trade-war fears largely drove the market correction in February, but there’s just one problem: the tariffs are too small to matter. Even at their recent expansion to $250 billion in imports, tariffs on Chinese goods represent about 1% of America’s economy. And those tariffs are effectively a tax of about 13% of those $250 billion—meaning the actual impact on the US economy is about 0.17% of GDP.

These are microscopic numbers. Yes, they could increase—but until they do, the drag on the economy from tariffs is too small to matter, meaning it’s too early to respond from an investment point of view, no matter what your politics may be.

The Right Response

Still, these fears feel like they warrant some type of response, so what should it be?

Simple! As canny contrarians, we’re going to pounce on these overdone worries and buy stocks now.

But what’s the best way to do it?

If you choose to buy stocks individually, you’ll need to invest a lot of time and/or money in research. Pick a low-cost index fund like the SPDR S&P 500 ETF (SPY) and you’ll likely enjoy a strong return. But that return will, by definition, be mediocre, because SPY doesn’t try to pick winners or losers. Plus, SPY’s dividend yield is a joke at 1.7%.

Then there’s the path less traveled: high-yield closed-end funds (CEFs) that invest in many S&P 500 stocks and offer a shot at better price gains, along with a higher income stream (and not just a little higher: payouts of 7% and more are common in CEF land).

2 Funds Set for Big Gains (and Dividends) as Wall Street Frets

Our first pick is the Nuveen S&P 500 Dynamic Overwrite Fund (SPXX), which provides a mix of equity exposure and insurance on a big market slide to provide returns, because this fund uses call options (a kind of insurance against stock exposure) to limit downside risk.

It also boasts an outsized 6.7% income stream that’s nearly 4 times the S&P 500’s average yield. Plus, SPXX has closely tracked the market in terms of overall performance while providing that bigger income stream:

SPXX Hands You Your Win in Cash

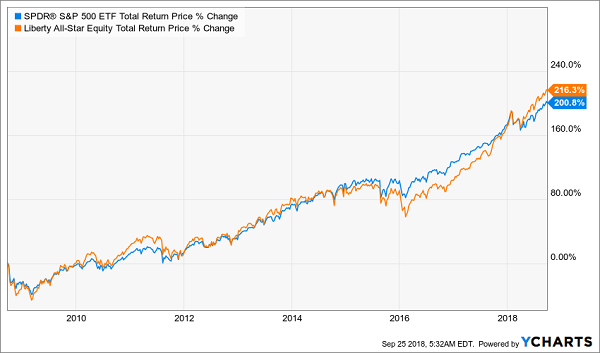

Or you could snap up the Liberty All-Star Equity Fund (USA) and its incredible 10% dividend yield, as well as its portfolio of mid-cap and large-cap US stocks. This one has actually beaten the “dumb” index fund over the last decade, too:

A Massive Return Over the Long Haul

Whatever path you take, it’s pretty clear that now is not the time to panic—even as we keep our eyes peeled for whatever 2020 may bring!

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

With Halloween a little over a month away, both kids and adults are prepping for the fright-filled holiday. But since October also represents the start of the fourth quarter, it’s an ideal time to consider which stocks to sell.

I say this because several names, whether they’re standout performers or backmarkers, gained on the back of a generally improving economy. But with our politics hitting a very sour note ahead of the midterm elections, the markets have lost their sheen. More importantly, the China tariffs casts a dark cloud on most sectors.

Therefore, getting rid of stocks to sell helps to protect our portfolio from unforeseen events. That’s the easy and obvious part. The more difficult component is separating the winners from the duds.

For this list of companies to avoid, I’m staying away from stocks that have already suffered severe declines. Typically, these names can temporarily skyrocket due to a short squeeze or simply a reactionary move. Instead, I’m going bearish on organizations that have done well this year, but whose premiums have gotten too rich.

So with that intro out of the way, here are my choices for stocks to sell in October:

Stocks to Sell in October: Dillards (DDS)

Source: Shutterstock

Department stores and the broader retail sector have experienced a surprising comeback in 2018. Left for dead due to declining foot traffic and competition from e-commerce companies, the retail rally proved brick-and-mortars are still relevant.

Unfortunately, Dillards (NYSE:DDS) didn’t receive the memo.

Sure, DDS shares are up big, gaining 29% since the start of the year. Therefore, it seems strange that I would include it in my stocks to sell list. Here’s the deal: I doubt that DDS will continue positively surprising Wall Street. In its most recent quarter, Dillards managed an uninspiring revenue growth rate of 2.5% to $1.5 billion. In comparison, Nordstrom’s (NYSE:JWN) sales growth jumped over 7% to $4 billion.

My biggest concern is that brick-and-mortars lack a compelling growth story. Some competitors will makes it, but not all. That leaves DDS in a tight spot, which might explain traders’ hesitation over the last several weeks.

TripAdvisor (TRIP)

Source: Shutterstock

TripAdvisor (NASDAQ:TRIP) has enjoyed a stunning performance in 2018. Since the January opener, TRIP stock has skyrocketed 51%. This is despite the fact that since the end of July, TRIP shares evaporated close to double digits.

So why am I including TripAdvisor on a list of stocks to sell in October? I’m just not sure that the company’s equity is worth its rich premium. Currently, TRIP is trading at 30-times forward earnings. The average for the global leisure industry is 18 times forward earnings.

The other concern I have is declining revenue growth. In its most recent second quarter earnings report, TripAdvisor registered $433 million in sales. This was an improvement of only 2% year-over-year. To put this into greater context, TRIP achieved over 8% YOY growth in Q2 2017.

People may be traveling more often now, but TRIP stock isn’t enjoying the benefits.

Under Armour (UAA)

Source: Shutterstock

Having covered Nike (NYSE:NKE) for its earnings report, I can better appreciate the difficulty involved in the sports-apparel market. Nike, for all its successes and brand popularity, didn’t impress many analysts for their fiscal Q1. To succeed here requires that you fire on all cylinders.

That brings me to Under Armour (NYSE:UA, NYSE:UAA). UAA achieved a remarkable turnaround this year. Since the start of 2018, shares have gained around 46%. But after peaking in early June, UAA hasn’t really looked the same.

Much of the bearishness is fundamental. Under Armour is losing traction with teenagers, which is a critical demographic. They’re the ones not only buying the products, but using them in athletic competitions. Plus, if you can’t win with American teens, you’re going to have difficulty internationally against dominant force Adidas (OTCMKTS:ADDYY).

Finally, UAA simply doesn’t have the financial resources to go toe-to-toe with the big boys. If you’ve made a profit, this is one of the stocks to sell in October.

Qualcomm (QCOM)

Source: Shutterstock

This is an incredibly controversial idea, so allow me to caveat this upfront: we’re talking about stocks to sell in October, and not indefinitely. And with that specific framework in mind, I’m temporarily going bearish on Qualcomm (NASDAQ:QCOM).

Immediately, QCOM bulls will respond that the 5G rollout is upon us. With next-generation high-speed internet, Qualcomm’s revenues should blow through the roof. Plus, the company’s legal battle with Apple (NASDAQ:AAPL) should either blow over or perhaps move towards Qualcomm’s favor. Either way, we’re looking at an optimistic environment for QCOM stock.

From a longer-term perspective, I agree. But technically, QCOM has shown weakness in recent trades. If I know anything, it’s that the market is always right. Furthermore, I’m reminded of the fact that the first 4G phone rolled out in 2010, yet QCOM experienced significant turbulence that year before ultimately rising higher.

Yes, 2010 wasn’t a great year for the broader economy. However, I can also say the same this year specifically regarding the ongoing China tariffs. Bottom line: QCOM is a long-term buy, but for right now, it’s a risky trade.

National-Oilwell Varco (NOV)

Source: Shutterstock

If you’re in the broader oil business, life is good. Crude oil prices have steadily increased throughout this year. The international benchmark Brent Crude is $82 per barrel, and technically, it looks set to break back into triple-digit territory.

So it sticks out like a sore thumb when a sector player like National-Oilwell Varco (NYSE:NOV) signals weakness. I get the point that NOV stock is up over 19% year-to-date. However, shares have been riding a losing streak since the first of August, which is worrisome.

The other reason I don’t care for NOV is that you can easily find better deals in the oil market. National-Oilwell Varco trades at 43 times forward earnings, whereas the industry average is a little over 21x. Moreover, NOV pays out a pittance in dividend yield, less than 0.5%.

Again, for the inherent risk you’re taking in the oil sector, you have far better options.

Tesla (TSLA)

Source: Shutterstock

For quite some time, I’ve supported Tesla’s (NASDAQ:TSLA) Elon Musk. Whatever troubles TSLA was facing in the markets, at the end of the day, I trusted Musk and his potential. We’ve all witnessed what this modern-day Einstein has accomplished.

Meeting sales targets for an automobile company? This should be child’s play compared to launching a convertible to Mars.

Unfortunately, we have one little problem: Musk at times has proven to be more a child than an adult. Whether it was his cryptic tweet that drew an SEC investigation, or his outbursts against analysts asking questions that are “not cool,” Musk has gone off the deep end.

TSLA has always suffered significant challenges, primarily with its car-production goals. But now, the company can’t even rely upon run-of-the-mill leadership, let alone a disciplined, focused CEO. Musk’s volatile behavior magnifies whatever ails TSLA. Bottom line, I’m out, and not just for October.

Wells Fargo (WFC)

Source: Shutterstock

I have reservations towards big banks. As bellwethers of the underlying economy, we should see a correlation between consumer confidence and rising bank stocks. And actually, we’ve seen exactly that since President Donald Trump assumed office. But recently, things look shaky.

Among the “Big Four,” no one is having a worse month in September than Wells Fargo(NYSE:WFC). WFC stock is down almost double-digits at points since the close of Sept. 4. Wednesday’s session didn’t do the financial institution any favors, dropping 2%.

What’s going on? For one thing, WFC suffers the same issues as other major banks. Their earnings and sales growth originate from sources other than income from normal business activities (ie. lending, services, etc.).

But as my friend Will Ashworth pointed out, WFC underperforms its peers in other segments as well. For example, while jobless claims are declining, the company is “laying off as many as 26,500 employees, not a great a piece of news if you own Wells Fargo stock.”

Exactly. I don’t have any issue if you decide to take a shot on the big banks. But I’d put WFC on the list of stocks to sell.

To start this week, Comcast (NASDAQ:CMCSA) absorbed a 6% loss in the markets. The rationale for the volatility isn’t at all surprising. News stations everywhere announced that CMCSA emerged victorious in their bidding war for Sky (OTCMKTS:SKYAY).

But what did Comcast really win? The heavily indebted organization is now scheduled to assume even more debt. As so many people have argued months before this announcement, CMCSA would become unnecessarily unwieldy. Moreover, at a time when the cord-cutting phenomenon is accelerating, doubling down on traditional media seems counterproductive.

Adding insult to injury, noted analyst Craig Moffett downgraded CMCSA, questioning management’s longer-term vision. Not only that, Moffett points out that Comcast is paying a rich premium for Sky, a premium that the markets didn’t believe it was worth.

Subsequently, Disney (NYSE:DIS) is up nearly 4% for September. I’m siding with the markets and steering clear of CMCSA.

China-based investments always attract the bulls’ interest, even if they aren’t ready to pull the trigger yet. But with the benchmark iShares China Large-Cap ETF (NYSEARCA:FXI) near the upper range of its recent consolidation channel, I think this is a great time to sell.

Like millions of Americans, I’m anxiously watching news media as we engage in a heated economic conflict with China. I’m trying to see if anybody is going to back down or offer to go to the negotiating table. But listening to President Trump speak, he relishes his “bad cop” role against the Chinese.

I don’t mind tough talk. But when you’re talking tough for its own sake, I get worried, especially if you’re the leader of the free world.

Right now, I’ve got to put FXI and most Chinese companies in my bag of stocks to sell in October. This trade war is going to last longer than most people anticipate. Plus, we should expect to see a few nasty surprises along the way.

Papa John’s (PZZA)

Source: Shutterstock

Just recently, embattled Papa John’s (NASDAQ:PZZA) shot up 8.5% on the news that ousted founder John Schnatter is seeking private-equity firms to help take over the company. This is a perfect time to consider dumping PZZA stock.

First of all, I don’t know too many companies that want to associate themselves with Schnatter. The reward is limited, and the risk abundant. Just keep in mind that Americans today are especially sensitive to racial issues.

Second, the PZZA fiasco is one of those rare cases where the controversy becomes more pernicious as time passes. Most news media focused on Schnatter saying the N-word during a conference call. But that’s only half the story. Schnatter also accused KFC icon Colonel Harland Sanders of also using the word.

It’s an insane accusation because it’s not something that can be proven. Plus, the optics of slandering a dead man doesn’t go over well. For what it’s worth, the evidence that Sanders was racist is flimsy.

This ongoing drama will likely negatively impact PZZA stock for the simple reason that its rivals aren’t stupid. You’re not going to see Domino’s Pizza (NYSE:DPZ) make this egregious error. So while Papa John’s works hard to restore its reputation, the competition will jump to a perhaps unassailable lead.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

Throughout U.S. corporate history, there have been some very memorable company founders such as JP Morgan and Henry Ford. Fast forward a few decades and we have Bill Gates and Steve Jobs.

I suspect though that history will less kindly remember the current batch of founders including the likes of Travis Kalarick of Uber, John Schnatter of Papa John’s and Elon Musk of Tesla. These entrepreneurs succeeded initially, but failed to come up with a succession plan to transition to a professional management. And worse, they’ve stayed on too long, becoming both an embarrassment and a hindrance to their respective companies.

In the case of Musk and Tesla, he may have let his strong dislike of people pointing out the flaws in his company’s finances go so far that he may have committed a crime with his “funding secured” tweet. The U.S. government has launched a criminal investigation into Tesla.

All of the above examples are companies that failed at the very important task of planning for the replacement of an executive who serves not only as the company’s manager but also as its pitchman and inspiration. These companies should all have planned for a staged withdrawal with the elevation of several key executives to key positions. But Tesla for example, cannot seem to keep an executive for more than a few months.

However, there are companies that have done things right. Here are two examples, with one company’s success very plain to see and another that I believe will continue its success after its founder leaves.

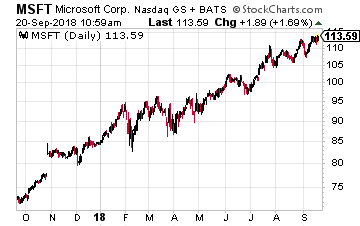

Microsoft’s Teddy Roosevelt

Former President Teddy Roosevelt is perhaps best known for his approach to foreign policy that was summed up in one phrase, “Speak softly and carry a big stick.”

That seems to be the approach of Microsoft(Nasdaq: MSFT)CEO Satya Nadella. His default posture, even with rivals, is to discuss mutual advantage first, competition second. This is in stark contrast to his predecessor – the boisterous Steve Ballmer and Microsoft founder Bill Gates, who both took business as an us-versus-them competitive fight to the death.

That attitude had Microsoft’s stock and business going nowhere for more than a decade. In contrast, Nadella’s ‘soft’ approach has worked marvelously. The company’s strong revenue growth have pushed its shares to an all-time high. Microsoft’s revenue expansion is being powered by cloud computing services for businesses, where revenues have climbed from a single-digit percentage to a third of sales in just five years. Its emphasis on cloud computing is evidence that Mr Nadella was tough enough and carried a big enough ‘stick’ to win the internal company battle with the guardians of Microsoft’s legacy personal computing businesses.

It is giving Amazon a real run for its money in the sector. That because unlike the other big cloud players, Microsoft’s business extends from all the way from giant corporations to individual consumers using its Office software online. It has become a leader in edge computing — this is where more data-crunching is carried out on the network “edge” — the name given to the many computing devices that intersect with the real world, from internet-connected cameras and smartwatches to autonomous cars.

And Nadella has turned Microsoft into a highly diverse company, offering products that range from applications to services to consumer hardware like the Xbox. It is also one of a handful of tech companies leading in the next age of computing – quantum computers. These machines tap into the weirdness of quantum mechanics — a branch of physics that deals with the behavior of sub-atomic particles. And it holds the promise of exponential gains in computing power, making supercomputers and even blockchain technology obsolete.

These moves make Microsoft the likely next entrant to the very exclusive “four comma club” – that is, having a stock with a valuation of $1 trillion or more.

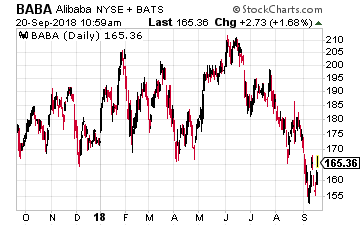

Jack Ma and Alibaba

Another company that is doing things right is Alibaba (NYSE: BABA) and its founder Jack Ma, who recently revealed plans to step away from the company.

This transition has been in the works for almost a decade. Ma actually handed over the reins as chief executive in 2013, first to Jonathan Lu. Daniel Zhang, who replaced Mr Lu two years later, shoulders the bulk of the day-to-day running of the company along with a number of individual business heads.

That is in sharp contrast to how traditional Chinese firms are run, where control is passed on to members of the immediate family, not employees. And in a way, it reminds me of the transition at Apple from Steve Jobs to a professional manager like Tim Cook.

And while Ma remains the face of the company and contributes to the big picture plans for Alibaba, professional managers are running the day-to-day operations. For instance, Ma has never hosted an earnings call, which instead are handled by M.r Zhang, executive vice-chairman Joe Tsai and chief financial officer Maggie Wu. Contrast that to Musk’s disastrous handing of the earnings call several months ago.

So while many of Alibaba’s initiatives carry his fingerprints, they are increasingly led by the next generation. Zhang makes sure Singles Day – the largest shopping day in the world – runs smoothly. Last year, sales hit a record of $25.3 billion, dwarfing Amazon’s Prime Day.

Zhang is also the driving force behind Alibaba’s ‘new retail’ strategy — the blending of online and offline shopping — through operations such as the Hema supermarket chain where consumers can shop, order deliveries or eat in the store. Zhang is likewise championing Alibaba’s grand plan for global trade without frontiers.

Like Taobao, where more than 630 million consumers shop every month, these were all Jack Ma ideas that are being implemented by highly qualified people, such as Zhang and Jian Wang who is running Alibaba’s cloud business, which is growing by leaps and bounds. Alibaba is also moving other areas, ala Microsoft, including quantum computing and artificial intelligence (AI) chips.

Alibaba is doing things right and trade war fears are merely giving long-term investors a chance to buy the stock at a reasonable valuation level.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

The U.S. economy is growing nicely, with any recession at least a few years out in the future. Average wages for working folks are also starting to increase after years of stagnation. Confidence in the economy and more money in their pockets will have people more willing to spend on recreation activities. Now is a good time to consider income stocks backed by consumer discretionary spending, especially for recreation activities.

Real estate investment trusts (REITs) own a wide range of property types lease the many kinds of businesses. It is often financially more efficient for a retail or services business to lease property or buildings rather than own them. REITs typically specialize in a specific property type. This gives them expertise to generate superior returns and often help their tenants be more successful in their own businesses. As noted above, this is a good time to look at REITs with properties used in the recreation and leisure industries.

Here are three specialty REITs focused on gaming and other recreation activities.

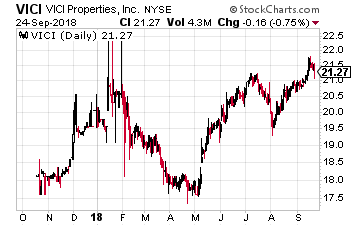

VICI Properties, Inc. (NYSE: VICI) was spun-off by Caesars Entertainment (Nasdaq: CZR) with an October 2017 IPO. The company’s portfolio includes 20 market-leading gaming properties in nine states, including the world-renowned Caesars Palace, and four championship golf courses. The properties are leased to Caesars Entertainment Corporation and operate under leading brands such as Caesars, Horseshoe, Harrah’s and Bally’s.

Caesars doesn’t not have an ownership position in VICI and there are no Board members common to both companies. With the spin-off, VICI is completely independent. Caesars does provide very strong 3.6 times rent coverage on the properties and contracted capex spending commitments to keep the properties at the forefront of the gaming industry. The REIT is internally managed. For growth VICI has rights of first offer (ROFO) on properties Caesar would want to capitalize through a sale lease back. The REIT can also pursue third party acquisitions.

Two dividends have been paid, with a 9.5% increase between the first and second.

The shares currently yield 4.9%.

MGM Growth Properties LLC (NYSE: MGP) was spun-off in April 2016 by MGM Resorts International (NYSE: MGM) in April 2016. The REIT currently owns 11 properties leased to and managed by MGM. All the properties are on a single master-lease, which gives the rental payments to MGM Growth Properties the highest level of safety. The lease has built in annual escalators and a profit-sharing component.

In contrast to VICI, MGM retains a majority ownership in MGP and pays all the operating expenses of the REIT. MGP also has ROFO on properties owned by MGM. The REIT has already made third party acquisitions.

In its history, MGP has produced steady 10% per year dividend growth.

The shares yield 5.9%.

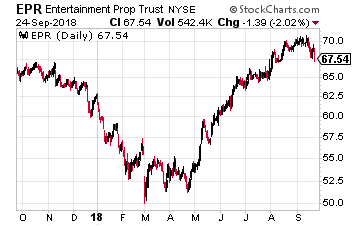

EPR Properties (NYSE: EPR) was founded in 1997 as a pure play owner of movie theater properties. Today the company 169 multiplex theater and family entertainment centers generating $280 million of annual net operating income, 80 golf entertainment complexes, ski areas, and other entertainment attractions producing $182 million of NOI, and 146 charter and private schools generating NOI of $115 million.

The EPR management team has great expertise in its focused property areas and helps tenants be as profitable as possible. All properties are leased to tenants on triple-net contracts. The EPR dividend has grown every year since 2010 with a 7% compound annual growth rate.

Dividends are paid monthly, and the yield is 6.1%.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

As expected, the Federal Reserve raised interest rates by a quarter of a percentage point from 2.00% to 2.25%. The Fed had done an excellent job of telegraphing the move, as the CME reported that 95% of traders expected the quarter point increase. With no surprises, the markets took the raise in stride, and finished flat. The only notable change to the Fed’s policy statement language was the removal of the word “accommodative” to describe Fed policy. With the rate increase out of the way, the market will likely turn back to trade tariffs as the main headline for the rest of the week. James Hackett, CEO of Ford (F), rekindled the tariff discussion Wednesday afternoon when he stated the tariffs on aluminum and steel have now cost the automobile manufacturer $1 billion in profit. It’s likely we’ll hear from several more companies in the days ahead as to the negative impact of the tariffs on their bottom lines.

Thursday morning Accenture (ACN) and Carnival (CCL) will report earnings. The consulting and outsourcing company has put in a good showing this year with continued growth in both its business lines. Accenture has expanded its offerings in recent years by acquiring cloud and internet of things (IOT) companies that can augment its core business. Analysts are watching margins closely at the $110 billion company, as competition has been steadily increasing in both consulting and outsourcing. This is the biggest quarter of the year for Carnival. The company generates a disproportionate amount of its revenue and operating income in Q3. The stock has basically traded flat thus far in 2018. The main focus for investors as the company reports is whether Carnival can contain expenses as revenue rises. This quarter will definitely set the tone for the remainder of the year for the cruise company.

While the market was focused on the Fed and its Wednesday afternoon announcement, the remainder of the week is full of economic numbers to chew on. Thursday we’ll get reports on durable goods, GDP, international trade, jobless claims, pending home sales, wholesale inventories, retail inventories and corporate profits. Corporate profits are expected to jump to a healthy 6.7% year-over-year for Q2 ‘18. That’s a major uptick from .1% reported in Q1. On Friday we’ll see personal income and outlays, Chicago PMI, and consumer sentiment. The consumer sentiment number is expected to come in at 100.8, an important reversal of the downward trend in place since March of ‘18. The survey of 600 households measures both current conditions and expectations for future economic opportunity.

Friday earnings will include Vail Resorts (MTN) and BlackBerry (BB). While the summer earnings report from ski operator Vail Resorts may not be the most important of the year, it does give the company a chance to report on infrastructure improvements headed into the busy winter season. The company can also preview early season pass sales numbers for investors. BlackBerry isn’t your old BlackBerry anymore. But, the transformation has been long and arduous, and the accounting for old businesses along the way has clouded earnings. This may be the quarter the company’s connected car business comes into focus. Analysts are looking for a strong showing from the BlackBerry Technology Solutions (BTS) unit which houses the connected car operating system.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

Even in America’s reddest states, favorable conditions for medical marijuana stocks could emerge soon. A permissive medical marijuana law received voter approval in Oklahoma earlier this year. Also, Republicans in Texas recently approved medical marijuana in their party platform. Cannabis’ days as a Schedule I drug are likely numbered. When this status changes, investing in medically-related marijuana stocks could reach a fever pitch in the fourth quarter and beyond.

Right now, most pot stocks trade on the OTC market and base themselves in Canada. The thirst for American investment has led more marijuana stocks to list on the NYSE and Nasdaq already, but more will likely join them when cannabis’ Schedule I designation ceases to exist. Both the designation swith and increased U.S. listing should flood more investment capital into the marijuana industry, driving stock prices higher. While many of these marijuana stocks have already achieved high valuations, investors could still more gains.

These four medical marijuana stocks are perfect to get into now before the interest in pot stocks becomes even bigger:

CannTrust Holdings, Inc. (CNTTF)

Source: Shutterstock

Vaughan, Ontario-based CannTrust (OTCMKTS:CNTTF) exists as a federally-regulated medical marijuana producer within Canada. It produces a 100% pesticide-free medical-grade cannabis and cannabis oils. The company also conducts medical research on marijuana-related drug products. CannTrust partnered with McMaster University and Hamilton Health Sciences on medical research trials.

CannTrust just completed their first overseas shipment of cannabis oil to Denmark-based StenoCare. CannTrust’s cannabis oil is the first and only to gain acceptance on the Danish Medicine List thus far. Incidentally, StenoCare will launch Europe’s first IPO by a medical marijuana company next month. Such a move will likely expand CannTrust’s reach within Europe.

From a financial perspective, CannTrust outshines most other marijuana stocks in one area — making a profit. Analysts forecast it will earn 11 cents CAD (8.5 cents U.S.) per share in 2018. They expect that to grow to 38 cents CAD (29 cents) per share in 2019. While that brings the forward price-to-earnings (P/E) ratio to 115, CNTTF still compares well to other profitable peers. Moreover, if the stock price were to stay the same over the next year, that P/E would fall to just over 33.

This marijuana stock’s profit should rise as its recreational brands also gain traction. With supply agreements in place in the Atlantic provinces, CannTrust now can sell across Canada. And with a schedule change in the U.S., its medical products could move south of the border. With the high growth potential and the financial stability, CNTTF one of the few cannabis stocks that will prosper under any conditions.

Hexo Corp. (HYYDF)

Source: Shutterstock

Hexo Corp. (OTCMKTS:HYYDF) develops and produces medical marijuana products for the Canadian market. Formerly known as Hydropothecary, this company offers a wide variety of cannabis-based products to treat various conditions.

Hexo has taken a slower approach than most of its peers. Unlike others, it has kept its focus to its core region, in this case, Quebec. However, that creates advantages. Through supply agreements, this should give the company a market share of about 34% within Quebec. Quebec also happens to border four pot-friendly U.S. states. If the U.S. market were to become available, Hexo could expand to New York and New England while keeping to its regional market.

Despite its smaller footprint, investors still need to look at HYYDF stock. It makes 24 different products ranging from tried products like cannabis flowers and cannabis powder to a fine cannabis mist. The company also works in conjunction with Molson Coors (NYSE:TAP) on cannabis-infused drinks.

Since the company has not spent heavily on expansion, analysts expect the company will break even next quarter. This should make the company profitable by the fourth quarter of this year. Consensus estimates for 2019 place profits at five cents CAD (3.9 cents) per share.

That gives the company a 2019 forward P/E ratio of about 129. This ratio should come down in future years, and it still compares favorably to most marijuana stocks. With its forecasted profits and its go-it-slow approach, I think HYYDF will not only survive, but thrive.

MariMed Inc. (MRMD)

MariMed (OTCMKTS:MRMD) specializes in medical-marijuana consulting. As a company, it helps others optimize production and sales for both the medical and legal cannabis firms. It helps to design production facilities to grow safe medical cannabis. It also offers business planning services to cannabis companies. Additionally, MariMed produces its own proprietary products that it sells under the MariMed brand name.

Such a business could help medical marijuana companies in Canada bring product into the U.S. once marijuana ceases to be a Schedule I drug. Moreover, it should help cannabis enterprises produce more medical marijuana as legal roadblocks gradually disappear. According to their last quarterly report, the company has initiated plans to operate in Florida, Michigan, New Jersey, Pennsylvania and Ohio.

Also, when non-cash charges are excluded, MRMD could call itself one of the profitable marijuana stocks. The company earned $530,000 in the first six months of the year. Due to stock option issuance and payment of debt via stock sales, the company reported an $8.1 million loss.

However, this shows MariMed can earn money. Profits should move much higher once more markets open up as well. With its own product line and its consulting business positioned in multiple states, MRMD should grow along with the U.S.’s weed industry.

OrganiGram Holdings, Inc. (OGRMF)

Source: Shutterstock

Unlike its peers, OrganiGram (OTCMKTS:OGRMF) takes a unique approach to medical pot. It focuses on treatments for conditions such as PTSD and chronic pain.

The firm also emphasizes partnerships. The company will invest in Eviana Health Corporation, a European, cannabinoid-focused hemp company. With Europe more ready than ever to embrace legalization, this gives OrganiGram an early advantage.

OrganiGram also signed a deal with Canopy Growth (NYSE:CGC). Under terms of the agreement, OrganiGram will provide Canopy’s Tweed retail locations in Newfoundland and Labrador with branded cannabis products. Since Canopy also made a deal with Constellation Brands (NYSE:STZ), this creates that much-needed U.S. connection. This agreement could lead to a medical marijuana agreement in the U.S. whenever the government permits Canadian medical cannabis products.

Analysts also expect OrganiGram to begin reporting profitability beginning in the fourth quarter. For 2019, consensus earnings stand at 14 cents CAD (11 cents) per share.

At current prices, this takes the 2019 forward P/E ratio to about 48.6. Given where other marijuana stocks trade, this makes OGRMF a safer bet than most. Also, with its connections to Europe and now, an indirect contact in the U.S., OrganiGram should place itself in a strong market position once sales in the U.S. and Europe take off.

As of this writing, Will Healy is long CNTTF stock.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

One of the best tech stocks to buy in October 2018 isn’t a flashy FANG stock or legacy Silicon Valley giant, but it could make you a killing.

Consider any innovative technology such as cloud computing, smart homes, self-driving vehicles, immunotherapy, and the Internet of Things (IoT), and it’s a certainty that the company we’re highlighting played a role.

The clients for this company run the spectrum from start-ups to some of the biggest companies on the planet, including Nike Inc. (NYSE: NKE) and Alphabet Inc. (NASDAQ: GOOGL).

While flying under the radar, this company has grown into the third-largest electronics manufacturing company in the world.

This is a mighty feat for a tech firm that most investors have never heard of.

And the innovations it fuels is why it’s one of the best tech stocks to own…

How Innovation Is Driving Tech’s Growth

While this is a backdoor play in the tech sector, it isn’t a small one by any measure.

The technology sector is primed for growth thanks to continued innovation. Just consider some of the recent breakthroughs…

Research firm MarketsandMarkets reports that the IoT market is projected to grow at a rate of 26.9% annually, from revenue of $170.57 billion in 2017 to $561.04 billion by 2022.

Allied Market Research says the market for self-driving vehicles is going to reach $54.23 billion by next year and then grow at an annual rate of 40% over the next seven years.

According to Statista, the smart home industry in the United States alone will close to double from $27.5 billion last year to $53.5 billion in 2022.

And one of the best tech stocks to buy now has become the top supplier for each one of these innovative trends. This company is a one-stop shop capable of taking any technology-based concept all the way through to production.

Critical: A breakthrough technology could disrupt every major industry, and one tiny company is at the center of it all. Its stock is trading for less than $10 now, but it could deliver a 471.9% gain for early investors. Learn more…

The company can create prototypes, protect a company’s intellectual property, establish a supply chain, and handle global distribution. Tech giants and entrepreneurs alike rest easy knowing that this firm has their back when they are developing or launching a new product or line.

This is just one of the reasons why this company was named among the world’s most admired by Forbes.

But the best reason to buy stock in this company is its sterling growth potential.

In fact, that’s exactly why it’s on our radar.

This company has a perfect Money Morning Stock VQScore™, meaning it’s a major growth target trading at the best buy-in price you’ll see.

That’s exactly why analysts are projecting this stock could soar 50% over the next year…

The Best Tech Stock to Buy in October

Flex Ltd. (NASDAQ: FLEX) is a Singapore-based company that designs, engineers, manufactures, and distributes a variety of consumer products.

It was originally a Silicon Valley company founded in 1969 as Flectronics Inc., but it moved overseas and shortened its name in 2016. It has 200,000 employees that work across 100 locations in 40 countries.

Over the years, Flex’s list of projects has covered the spectrum of high-tech innovation, and it’s an impressive resume.

Google enlisted the help of Flex several years back, when it wanted to break into the market for video streaming. Flex already had experience with smart home technology and devices and was able to hand Google a prototype for Chromecast in just one month.

The product launched within 24 hours in 2013, and Google had to cancel its sales promotion because it couldn’t keep up with the overwhelming sales volume.

Several years prior, Flex worked with NASA to deliver the mobility functions for its Curiosity rover, which was dispatched to Mars in 2011. The company outfitted the rover with technology that included sensors for delivering feedback and movable joints. With this tech, operators on Earth can monitor the changing conditions on Mars to make adjustments to the rover’s performance.

NASA moved to extend the mission of Curiosity indefinitely in 2012. To date, it has been collecting valuable data on Mars for over 2,200 earth days.

Nike turned to Flex when the company decided that it had to speed up its turnaround time for custom-made sneakers. The company put together a team that was able to swiftly identify and solve Nike’s largest inefficiency.

Before this partnership, Nike’s practice of laser cutting was deemed inefficient because the oxygen mixing with the laser beam burnt edges on the fabric.

Flex’s team of chemists and engineers were able to redesign a laser-cutting system that eliminated those burnt edges, which allowed Nike to significantly reduce the wait time for a custom sneaker from weeks to just a few days.

Flex is able to tackle just about any electronic issue brought to it by a client, but it is also known for helping innovators. Through its Lab IX incubator program, the company assists new tech companies in bringing disruptive ideas and products to market.

One example is Grabit, which is an automation arm that is used in warehouses and factories. Instead of gripping or simple suction, the arm uses electro-adhesion to handle fragile items like flat-screen TVs and solar panels.

The Lab IX program gave Grabit’s designers the tools they need to perfect their products and processes and bring it to market.

These are impressive feats for a tech company, but it is still a tech stock that is flying under the radar, making it an even better profit play.

FactSet reports that eight analysts out of 11 rate FLEX a “Buy” and give it a price target nearly double its current price.

And this is still selling the stock short.

In the past year, FLEX’s price/earnings ratio is only 63% of the industry average, which means it’s trading at a significant discount before Wall Street catches on.

Wall Street gives FLEX a high price target of $20 a share, a 54% increase from today’s share price of $13.03.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

One of the more popular strategies among investors today is to seek out “home runs.” These are lesser-known companies that have tremendous upside potential, but carry the risk of collapsing should business prospects go awry. While a balanced portfolio allows for some speculation, now is also a great time to consider S&P 500 stocks.

Why? For starters, the oft-cited benchmark index has worked out its choppiness. Since the second half of this year, the S&P 500 has gained nearly 7%. In sharp contrast, the index was much more volatile in the first half, moving a mere 1% since the start of January. The improved sentiment is a chance for investors to benefit from a rising tide.

Another reason to consider S&P 500 stocks is that they’re more stable on the way down. Of course, nobody hopes for a decline once a position has been initiated. But in this unpredictable market environment, leading blue chips offer confidence that smaller names can’t provide.

With that said, let’s dive into the best S&P 500 stocks to buy:

S&P 500 Stocks to Buy: AbbVie (ABBV)

Source: Shutterstock

Biopharmaceutical firm AbbVie (NYSE:ABBV) has been a fixture of the S&P 500 index for almost six years. But after enjoying a stellar performance in 2017, sentiment has declined significantly this year. Since the January opener, ABBV is only slightly above parity.

That said, I think this is an ideal time to consider buying one of the most powerful names among S&P 500 stocks. ABBV levers excellent profitability and growth metrics, highlights being its operating margins and double-digit revenue growth rate. In the second quarter, AbbVie rang up nearly $8.3 billion, up over 19% year-over-year.

For Q3, investors expect earnings-per-share to hit $2.01. This is nearer the higher end of individual estimates, which range from $1.94 to $2.06. Although an ambitious goal compared to the year-ago level’s $1.41 EPS, ABBV has the goods to deliver a beat.

Primarily known for its Humira drug, AbbVie has several other popular drugs in its pipeline. Additionally, many of them are in the late stages of the clinical-approval process and therefore offer more potential.

S&P 500 Stocks to Buy: Electronic Arts (EA)

Source: Shutterstock

Electronics Arts (NASDAQ:EA) is one of the most popular video game companies in the world, so it’s no surprise that it’s included among the top S&P 500 stocks. However, with fame comes hubris apparently. Management badly blundered in its Battlefield franchise, sending EA stock crashing.

Late last month, EA announced that it will delay Battlefield V one month to Nov. 20. Fans didn’t appreciate the creative direction the game’s producers took the series, and the results showed. Poor pre-sale numbers forced the company’s hands, and management decided to move the title into a less-competitive month.

The delay also caused EA to adjust its full-year guidance lower to reflect the lost sales. Understandably, that freaked investors, causing the slide.

However, EA is much bigger than any one franchise. One of its strongest divisions is its pro sports lineup. Thanks to exclusive licensing, EA provides a gaming experience unlike any other. Moreover, the Battlefield V issue isn’t unsolvable. Once designers give what the customers want, they’ll come running back.

As it stands, I view EA stock and its recent volatility as an opportunity to buy on discount.

Analysts once feared that the e-commerce revolution would negatively impact consumer-electronics retailers, and for the most part, they were right. Even mighty Best Buy (NYSE:BBY) had to adjust to the new realities of their industry. But BBY emerged as a success story.

Management focused on longer-term changes, such as incorporating lucrative businesses and getting rid of units that don’t work. Currently, their computing and mobile phones division represents the greatest share of total revenue. Coming in second place is consumer electronics, a very encouraging sign considering that Amazon (NASDAQ:AMZN) has changed the game here.

Another factor that should buoy investor sentiment is the company’s earnings performances. Since their fiscal Q1 2016, BBY has not once failed to at least meet consensus earnings targets. In fact, during this time, BBY exceeded expectations except for just one time in Q3 2018.

I don’t expect much to change for its fiscal Q3 2019 report. With a consensus EPS forecast of 85 cents, this is a very realistic target. In the prior year Q3, BBY delivered 78 cents EPS.

S&P 500 Stocks to Buy: Visa (V)

Source: Shutterstock

With unemployment near multi-year lows, and consumer sentiment generally moving higher, now is a great time to consider Visa (NYSE:V). For one thing, Visa dominates the credit-card market, levering 323 million cardholders. Its closest rival is Mastercard (NYSE:MA), which is some distance away at 191 million cardholders.

Another reason to look into V stock is its technical performance. Since the beginning of this year, V shares have gained over 28%. But I wouldn’t consider this to be a fluke. Thanks to the improved sentiment toward the consumer economy, Visa is likely to make steady gains.

Of course, I don’t expect massive upside. But as long as consumers keep buying, which appears likely at this point, V stock is in good shape. Visa started to come alive in late 2011 (around when we started to recover from the Great Recession), and it hasn’t looked back since.

For the longest time, S&P 500 stocks related to the restaurant industry had a giant question mark over them. Facing a difficult road following the recession, and with brick-and-mortars experiencing declining foot traffic, eateries were in a bad position.

But fast forward to this year, and suddenly, the tune has changed. For 2018, Darden Restaurants (NYSE:DRI) has gained over 24%. And while DRI shares appear overextended at this level, I wouldn’t be surprised if it eventually moves significantly higher.

As Bloomberg reported last month, consumers have splurged at restaurants across the country. In fact, we’ve witnessed a record spike in revenues at food establishments. Part of the reason is related to tax cuts as people are choosing to spend their extra funds on restaurants.

But I think a bigger component is the labor market. While not a perfect situation, those who have college education and in-demand skills are finding ample work. That’s a boon for DRI, as it appears Americans are getting hungry again.

Wall Street is currently scrutinizing oil prices with a fine comb. Just recently, the White House announced plans to impose fresh tariffs worth $200 billion on Chinese goods. Of course, the implication is negative. Usually, when the number one and number two economies of the world clash, we all suffer.

But we also must consider a twist to this story: simultaneously, President Trump seeks to tighten Iran’s oil exports to zero to bring them to the nuclear negotiating table. Since Iran is one of the world’s biggest exporters, this factor should more than offset the China tariffs.

That’s why investors should look into buying Chevron (NYSE:CVX) during this market weakness. For one thing, I doubt the negative sentiment toward crude oil will continue. On another level, the vast majority of people drive fossil-fuel powered vehicles. Yes, electric vehicles are the future, but it will take some time for them to make a decisive impact.

For now, the Iran situation is the most pressing concern. Oil prices will likely trek higher throughout the rest of this year, meaning you’ll want exposure to CVX stock.

S&P 500 Stocks to Buy: Harley-Davidson (HOG)

Source: Shutterstock

Among S&P 500 stocks, absolutely none is more American than Harley-Davidson (NYSE:HOG). Indeed, Harley-Davidson is painfully American. They’re big, brash and unapologetic, much like our people. Own a hog from HOG, and you have a piece of Old Glory sitting in your garage, just waiting to terrorize the neighborhood.

So it’s a strange twist that Harley-Davidson, among all the S&P 500 companies, that has aroused President Trump’s vitriol. HOG and Trump have bickered back and forth over the administration’s hardline stance on tariffs and sanctions. In keeping with the times, Harley-Davidson’s management wants to shift some operations overseas. Anachronistic Trump isn’t having any of it.

Another problem impacting HOG stock are millennials. According to CNBC, young consumers that are steadily growing their income are avoiding motorcycles. And let’s face facts: HOG hasn’t performed well over the years.

Still, investors can salvage something here. Regarding millennials, analysts have previously made sweeping generalizations about this demographic, only to be proven wrong later. They could very well take up HOG riding when millennials eventually have — God forbid! — their mid-life crises.

Then there’s the international expansion. Once the sanctioning boils over, or if Trump gets voted out, HOG will enjoy a clean slate. That would also give them opportunities to boost their presence overseas. It will require some patience, but Harley-Davidson has the ability to surprise.

S&P 500 Stocks to Buy: Facebook (FB)

Source: Shutterstock

This year, Facebook (NASDAQ:FB) has turned from one of the most respected S&P 500 stocks to buy into one of the most demonized. Frankly, I don’t understand the vitriol. FB may have inadvertently assisted the Trump campaign, but come on! The American electorate voted for Donald Trump, not Facebook.

This is why I view antagonism toward Facebook as a political distraction and witch hunt. The difference here, though, is that politics are hurting FB stock, which is a shame. For instance, several analysts have noted with concern that the company generated the slowest growth in daily active users ever.

But isn’t this exactly what we should expect? FB has dominated the internet-connected world; they can’t reproduce humans. Not only that, the fact that any kind of growth occurred necessarily means that social outrage against the company failed. In late July, I wrote the following:

“The most recent FB earnings report actually proved my argument. North American DAU stats were flat year-over-year, and virtually in line with consensus expectations. That tells me that the aforementioned fiasco that led to the #DeleteFacebook campaign ultimately did nothing.

Facebook is simply too ingrained in our society, and I would argue, too useful for us to give up. Not even Hollywood’s self-righteousness and a trendy millennial’s exaggerated self-importance could dent Facebook engagement stats.”

The volatility makes no sense. I just look at it as an opportunity to buy FB stock on a discount.

HP (NYSE:HPQ) may appear as a strange choice for a stock to buy going into the Q3 earnings season. After all, as PC Magazine’s John C. Dvorak bluntly stated, “the traditional laptop is dead.” Dvorak asks a simple question: “When you look at PCMag’s roundup of the best laptops, do you ever think to yourself, ‘Wow, I want that now!’ Never happens.”

I’m actually a little bit surprised that Dvorak still has a job contributing articles for PC Magazine! And while I respect his opinion in that laptops lack compelling innovations, I disagree with his ultimate conclusion. The laptop and the PC platforms face new competition, but they’ve proven extremely resilient.

This is one of the reasons why HPQ has performed well since getting booted from the Dow Jones index. While pundits deride traditional computer products, they’re much more useful than gimmicky tablets. Plus, higher-end laptops provide the perfect balance between performance and portability.

Finally, to address Dvorak’s point, I don’t get excited about laptop innovations. That said, I don’t get excited about smartphone or tablet innovations, either. At a certain point, a smart device is a smart device.

But one thing that laptop and PC specialists like HPQ advantages is consistent demand. While traditional computers aren’t sexy, they get the job done quickly and efficiently. Thus, companies like HPQ aren’t going away anytime soon.

S&P 500 Stocks to Buy: FedEx (FDX)

FedEx (NYSE:FDX) is seemingly one of those S&P 500 stocks that faces an Amazon threat. Critical shipping partners at first, Amazon has made some noise about starting their own courier division. Understandably, the implications worry investors, but FDX is still a long-term buy.

We just need to consider that FedEx is an $81 billion enterprise. Rival UPS (NYSE:UPS) is a $120 billion enterprise. While it’s true that Amazon dwarfs both these stalwarts, even disruptive CEO Jeff Bezos must watch his expenditures. As he’s busy taking over disparate industries, he must ensure that his investments make economic sense.

While Amazon can toy around with their various internal courier solutions, it shouldn’t drastically impact FDX. The company, along with UPS, has a virtually impenetrable network. To duplicate that wouldn’t make financial sense.

Moreover, e-commerce sales represent a consistently increasing portion of total retail sales. Although Amazon dominates this sector, they’re not the only players. With several brick-and-mortars incorporating their own online channels, I like FDX for longer-term, reliable growth despite its recent quarterly miss.

Among the most-recognized S&P 500 stocks, Goodyear (NASDAQ:GT) is one of the more contrarian opportunities. You can tell this simply by looking at its price chart. Year-to-date, GT shares are down nearly 25%.

My frequent readers probably expect me to say something like GT has stabilized over the last several weeks. You’re right, and it has. Since the beginning of July, GT stock is up over 4%. Although that’s nothing to write home about, it provides some reassurance as the company approaches its Q3 report.

Admittedly, the day-to-day movements for GT stock are difficult to determine. But I’m encouraged that since the five years or so following the Great Recession, Americans have driven noticeably more miles. I expect this trend to continue, especially because our labor market has improved for the educated and upwardly mobile.

Undoubtedly, GT is a risky play due to its prior weak performances. But broader trends suggest that this volatility is a profitable opportunity.

S&P 500 Stocks to Buy: Home Depot (HD)

Source: Shutterstock

A significant and tragic reason why Home Depot (NYSE:HD) dominates the business news media is Hurricane Florence. The storm has already taken many lives, and intractably, several more families must undergo the rebuilding process. No matter how you cut it, HD revenues will experience a bump up.

Some might view that as an opportunity to profit off HD stock. But as I argued in a prior write-up for Home Depot, the trading benefits are inconclusive. In some cases, HD does rise immediately during major storms. But the data does suggest that particularly devastating storms tend to hurt HD in the nearer-term.

I don’t recommend trading HD based on Florence. If anything, these are one-off occurrences that are difficult to gauge. But more importantly, Home Depot has a business that’s largely immune to Amazon’s intrusions.

That’s especially the case for storms and other emergency events. Customers are not going to comparison shop online for necessary supplies. And even in non-emergency situations, Home Depot provides unparalleled conveniences.

S&P 500 Stocks to Buy: Lockheed Martin (LMT)

Source: Shutterstock

Lockheed Martin (NYSE:LMT) is one of the most renowned defense contractors among S&P 500 stocks. It’s also having a surprisingly weak year. Despite a burst in bullish sentiment recently, LMT has gained only 7.3% YTD. For the record, this is just a hair under the S&P 500 index.

In my opinion, LMT is not getting the respect that it deserves. I understand that President Trump boasts consistently about allegedly thawing relations with North Korea. Earlier this year, Trump met North Korean dictator Kim Jong-un in an unprecedented summit.

While I respect the President for taking some kind of action, I’m also firm that I don’t trust North Korea. Nor do I trust the maniacal “dear leader” Kim. Sorry, but not sorry.

How does this play into LMT stock? Simple: more than ever, we must demonstrate a show of force. This is physically best done through our advanced fighter jets. There’s nothing quite like buzzing around our enemies’ airspace, and letting them know we can physically do the business.

Admittedly, it’s an immature tactic, but it works. LMT allows us to flex our muscle but still maintain diplomatic channels. In this complicated geopolitical environment, LMT is easily a longer-term buy.

S&P 500 Stocks to Buy: Raytheon (RTN)

Source: Shutterstock

Should a conflict ever escalate into a hot one, I’d like to own Raytheon (NYSE:RTN) as a hedge. Known primarily for its smart missiles and guidance systems, RTN is one the most relevant defense contractors today.

Don’t get me wrong: physical warcraft, as I mentioned for Lockheed Martin, is still a critical component of our military diplomacy. However, the modern battlefield has become increasingly asymmetric. A terrorist with a homemade explosive can wreak untold damage. Or a lone hacker could bring a powerful economy to its knees.

This transition also means that powerful militaries with extensive physical assets are vulnerable to asymmetric attacks. To alleviate this problem, RTN produces next-generation weapons systems, such as combat drones. Such technologies allow military operators to conduct operations in hard-to-reach, inhospitable terrain.

The other invaluable benefit is that it keeps our men and women in uniform out of harm’s way. Especially in this ever-evolving world, having some exposure to RTN simply makes sense.

Altria Group (NYSE:MO) has simply not had a good year in 2018. Since the January opener, MO has shed 9.5% in the markets. The biggest concern for investors is that Americans are smoking far fewer cigarettes than ever.

The “good news,” though, is that American smokers are gravitating toward e-cigarettes or vaporizers. These products heat the tobacco flavoring near the point of combustion, but not beyond it. The resultant plumes are much cleaner and have noticeably fewer chemical byproducts, such as carbon monoxide.

Of course, vaporizer companies compete with big tobacco, but the comparison isn’t worth discussing. MO is a multibillion-dollar enterprise. As a whole, experts predict that the vaping market will hit $27 billion in value. Relative to Altria’s market capitalization of nearly $118 billion, that’s nothing.

Moreover, MO has invested significant resources into its heat-not-burn devices. Although similar in principle to vaporizers, Altria’s products are made by smokers, for smokers. The experience is much more attuned to what natural-cigarette aficionados prefer.

So don’t butt-out MO stock. This is an underappreciated contrarian opportunity.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

A combination of U.S. and Chinese tariffs going into effect, and an expected rate hike later this week, drove the DJIA lower Monday. The Nasdaq held onto a slight gain following the introduction of the new S&P Communications Services sector. Trade and interest rates will continue to be the focus of the markets midweek. Any positive news on the trade front could send the markets higher, as an interest rate hike is baked in at this point. Markets are not expecting any surprises from the Fed on Wednesday as the economic numbers continue to be strong. Any deviation from the script by Chairman Powell would likely have a major impact.

Tuesday the market will focus on Nike (NKE) as the company reports earnings for the first time following the airing of their latest advertising campaign, which includes Colin Kaepernick. In the current political climate many companies have chosen to distance themselves from controversial issues fearing a boycott of their products. Though Kaepernick is just one element of the ad campaign, analysts will be interested to hear how the company has performed since the campaign began, and what the company’s strategy was as they contemplated the pros and cons. Also reporting on Tuesday is Cintas (CTAS). The uniform rental company has been riding the surging economy and is up over 35% so far in 2018. Investors are looking for an earnings beat, and for some insight into what the company sees near term as the economy appears to be maintaining its positive trend.

Tuesday also kicks off the first day of a two day Fed meeting. Economic data released on Tuesday includes the Redbook retail sales numbers, the Case-Schiller home price index, the FHFA house price index, and consumer confidence. The confidence number is expected to fall slightly in September to 131.7 after a big increase in the August number. Wednesday will begin with mortgage applications and new home sales numbers, but everyone will be focused on the 2pm Fed announcement on interest rates. The Fed is widely expected to raise rates a quarter point. This announcement also includes a press conference by Fed Chair Powell. Markets will be listening closely for any clues of future rate increases.

Reporting earnings on Wednesday before the open is CarMax (KMX). The car retailer’s comparable store sales have been on a positive trend the past few quarters, but both numbers were on the negative side of the ledger. Analysts would like to see a return to positive comp sales, and ideally the company can show improvement on the bottom line as well. Joining CarMax is Bed, Bath & Beyond (BBBY). The home goods retailer has seen earnings drop for several years, and is facing stiff competition from Amazon and Walmart. Investors are looking to see if strong numbers from companies like Target (TGT) are translating to the discount retailer. If the company can produce an increase in margins we may see a bump in the stock, but analysts aren’t expecting much from the company as evidenced by the 13% decline so far this year.

Buffett just went all-in on THIS new asset. Will you? Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it... What is it? It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up. Click here to find out what it is.

That seems to be the approach of Microsoft (Nasdaq: MSFT)CEO Satya Nadella. His default posture, even with rivals, is to discuss mutual advantage first, competition second. This is in stark contrast to his predecessor – the boisterous Steve Ballmer and Microsoft founder Bill Gates, who both took business as an us-versus-them competitive fight to the death.

That seems to be the approach of Microsoft (Nasdaq: MSFT)CEO Satya Nadella. His default posture, even with rivals, is to discuss mutual advantage first, competition second. This is in stark contrast to his predecessor – the boisterous Steve Ballmer and Microsoft founder Bill Gates, who both took business as an us-versus-them competitive fight to the death. Another company that is doing things right is Alibaba (NYSE: BABA) and its founder Jack Ma, who recently revealed plans to step away from the company.

Another company that is doing things right is Alibaba (NYSE: BABA) and its founder Jack Ma, who recently revealed plans to step away from the company.

VICI Properties, Inc. (NYSE: VICI) was spun-off by Caesars Entertainment (Nasdaq: CZR) with an October 2017 IPO. The company’s portfolio includes 20 market-leading gaming properties in nine states, including the world-renowned Caesars Palace, and four championship golf courses. The properties are leased to Caesars Entertainment Corporation and operate under leading brands such as Caesars, Horseshoe, Harrah’s and Bally’s.

VICI Properties, Inc. (NYSE: VICI) was spun-off by Caesars Entertainment (Nasdaq: CZR) with an October 2017 IPO. The company’s portfolio includes 20 market-leading gaming properties in nine states, including the world-renowned Caesars Palace, and four championship golf courses. The properties are leased to Caesars Entertainment Corporation and operate under leading brands such as Caesars, Horseshoe, Harrah’s and Bally’s. MGM Growth Properties LLC (NYSE: MGP) was spun-off in April 2016 by MGM Resorts International (NYSE: MGM) in April 2016. The REIT currently owns 11 properties leased to and managed by MGM. All the properties are on a single master-lease, which gives the rental payments to MGM Growth Properties the highest level of safety. The lease has built in annual escalators and a profit-sharing component.