Looking for viable stocks to buy at this juncture seems like a herculean task. The markets never looked convincing in October and it dubiously proved that point midweek. The Dow Jones shed 608 points exactly a week before Halloween, sending shivers down Wall Street. More problematic, at least for the nearer-term, is that the situation is likely to worsen.

Inarguably, the biggest concern is our ongoing trade war with China. Neither side obviously wants to concede, which means we’ll play hardball. Eventually, we’ll win out, but the victory will not come cheap. The other headwind impacting those seeking stocks to invest in is our political landscape. Politics is never conciliatory. However, I’ve never seen the country so divided. Anybody who has any amount of public clout has voiced their opinions to sway the electorate.

Based on everything that we’re seeing, the House will go to the Democrats. President Trump will, therefore,e face a contested government, which means nothing will get done. That might appease one side of the political spectrum, but it clouds deciphering which stocks to buy. Still, while the markets are swimming in red ink, a few viable publicly-traded companies exist. Primarily, the best “greenlight” stocks to invest in are levered toward consumer staples. That’s not surprising, considering that their underlying industry enjoys relatively consistent demand.

But other sectors have also outperformed in October, providing surprisingly healthy options for investors. Here are eight greenlight stocks to buy in a sea of red.

Hormel Foods (HRL)

Hormel Foods (NYSE:HRL) is simply one of the most monstrous stocks to buy this October. Since the start of the month, HRL stock was up nearly 7% (well, 6.66% to be exact … spooky!). While those numbers wouldn’t ordinarily raise eyebrows, consider that the Dow Jones has dropped almost 8% over the same timeframe. The venerable index is down for the year, while HRL stock has gained 17%.

Strangely, Hormel is getting a lifeline while so many other previous stocks to buy are heading towards the butcher. Revenues sharply declined last year, and HRL stock took serious damage. However, shares are on the upswing as management is back to robust growth.

Plus, Hormel has an opportunity to advantage the multi-billion dollar alternative-meat market. Hormel’s subsidiaries are exploring this sector, which should lift HRL stock long-term.

Source: Shutterstock

Tyson Foods (TSN)

Tyson Foods (NYSE:TSN) doesn’t quite match Hormel Foods’ performance. Year-to-date, TSN stock is down nearly 23%, which hardly inspires confidence for those looking for stocks to invest in. That said, Tyson Foods has enjoyed a surprisingly robust October. For the month, TSN stock is up over 3%. Again, this wouldn’t generate headlines except for the fact that the broader markets are in full meltdown mode. As such, TSN is a great place to park your money in this storm, especially considering its 1.94% dividend yield.

Fundamentally, the company is also coming around. Like other food companies, Tyson experienced a disjointed sales performance in recent years. However, this year, revenue is on pace to exceed 2016 and 2017 results.

Not only that, investors will likely appreciate TSN stock for the underlying company’s consistent demand. Irrespective of where the economy heads, people need to eat. When you look at the volatility in most investment sectors, Tyson Foods simply makes sense.

Hershey (HSY)

With Halloween coming up, Hershey (NYSE:HSY) seems like an appropriate choice among greenlight stocks to buy. After all, both kids and adults love Hershey’s iconic chocolates. Plus, the company levers several popular and delectable brands. Certainly, the markets are buying into the story. While the first half of this year was more than forgettable, the story changed dramatically in the second. Since the beginning of July, HSY stock has gained over 17%.

Even more impressive, the chocolatier and candy-maker increased momentum in October. Since the beginning of this month, HSY stock is up nearly 6%.

Fundamentally, I like Hershey heading into its third-quarter earnings report. The company has enjoyed three years of consecutive revenue growth, and it’s on pace for a fourth. In addition, stable free cash flow bolsters the case for HSY stock.

Oh yeah, let’s not forget about its 2.8% dividend yield. At a time when the broader markets are tanking, passive income is at a premium.

Philip Morris International (PM)

Based on the bigger picture, you’d think that Philip Morris International (NYSE:PM) has no business belonging on a list of stocks to invest in. Traditional cigarette sales are down sharply as more Americans are butting out. More importantly, the under-18 crowd isn’t picking up on the habit.

Indeed, PM stock started falling in the second half of 2017. Unfortunately for shareholders, the decline hasn’t ended. On a YTD basis, Philip Morris shares are down almost 15%.

But that statistic is deceptive because PM stock found new life since the end of August, with shares up 17%. And in October, the tobacco firm is on the verge of double-digit territory.

One of the things I like about PM stock is the underlying company’s IQOS product. IQOS, which is a type of vaporizer, plays directly into the e-cigarette craze. The advantage that Philip Morris levers is product knowledge. Not all vaporizers accurately replicate traditional smoking, which should benefit the top and bottom lines.

Finally, PM stock pays out a 5.1% dividend yield, which you definitely can’t ignore.

Verizon Communications (VZ)

With Verizon Communications (NYSE:VZ) recently putting up a convincing Q3 earnings beat, this is an easy one to put on your list of stocks to invest in. After wildly choppy trading over the past few years, VZ stock is finally on the right track. Moreover, the telco giant has completely moved against the grain in October. VZ stock is up over 8% for the month, while for the second half, shares have registered nearly 17%.

Naturally, many investors are gun shy about jumping onboard a company that is near all-time highs. However, VZ stock is the real deal. The telco firm enjoyed impressive wireless-subscription growth, while its potential for 5G is a gamechanger. The new wireless network offers multiple synergies, and Verizon was the first to deliver commercial 5G services.

Among the companies mentioned here, VZ stock provides a very generous dividend yield at 4.2%. Considering the broader selloff, Verizon provides much-needed stability and protection.

Source: Shutterstock

Superior Drilling Products (SDPI)

One of the biggest victims of the market selloff is the oil and energy sector. With global indices freefalling, Wall Street fears that demand for oil products will deflate. However, we shouldn’t ignore the fact that the U.S. has placed sanctions on Iranian oil exports, which comes into effect Nov. 4. That potentially boosts the contrarian case, not only for oil stocks, but for equipment companies, like Superior Drilling Products (NYSEAMERICAN:SDPI).

While energy firms have felt the heat, October has been (mostly) kind to SDPI stock. Despite today’s 15% decline, SDPI shares are up more than 10%. Of course, with that kind of performance, you want to be careful about going in too deeply. Still, SDPI stock has sound fundamentals. Primarily, the company has generated strong revenue growth. SDPI is on pace for an annual profit which hasn’t happened since at least 2014.

Should the supply-demand situation improve for the energy market, SDPI stock is primed for additional growth.

Source: Shutterstock

Iamgold (IAG)

When equities are deflating, the rule of thumb is to look at gold. So far, the precious metals sector has lived up to its reputation. Gold prices are up about 3% for October, driving up several mining companies.

However, one miner that hasn’t enjoyed much of a sentiment lift is Iamgold (NYSE:IAG). This month, IAG stock is up nearly 2%. That’s not bad in and of itself, considering the panic-selling on the Street. That said, Iamgold’s competitors have seen robust double-digit growth.

Due to the fact that the broader markets continue to flash all kinds of ugly, I believe Iamgold will eventually rise along with its peers. Fundamentally, IAG stock levers impressive stats. It’s one of the few gold companies that have registered consecutive years of growth. Moreover, Iamgold’s cash flow has stabilized relative to earlier years’ dysfunctionality.

Rosetta Stone (RST)

Back in July, I pegged Rosetta Stone (NYSE:RST) as one of the long-term stocks to buy. I felt that the company offered a compelling service, which is to get people up-to-speed on learning a foreign language. While we’re incredibly blessed to live in the world’s top superpower, and that English is the international language, that status isn’t likely to hold indefinitely.

For one thing, changing demographics have pushed Chinese as the world’s most spoken language. In theory, this and other factors should boost RST stock.

What I didn’t expect was for Rosetta Stone to hold its own during the October selloff. Yes, RST stock did experience volatility when the major indices tanked. However, RST is back to level ground, which gives me confidence in the company’s “bigger picture” potential.

As of this writing, Josh Enomoto is long gold bullion.

Buffett just went all-in on THIS new asset. Will you?Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

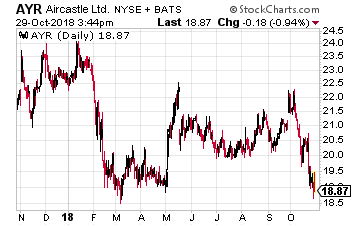

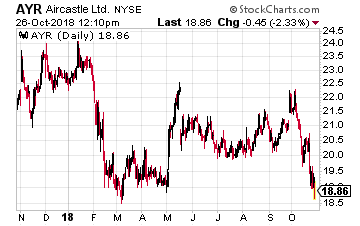

Aircastle Limited (NYSE: AYR) owns approximately 240 commercial aircraft that are leased to 84 airlines around the world. Aircastle must be nimble to adjust for changing needs for aircraft type and client airlines financial conditions. For example, in 2017, Aircastle purchased 68 aircraft and sold 37.

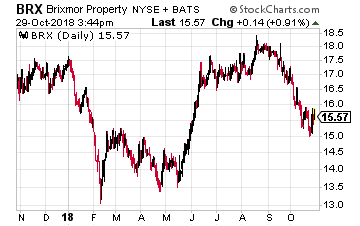

Aircastle Limited (NYSE: AYR) owns approximately 240 commercial aircraft that are leased to 84 airlines around the world. Aircastle must be nimble to adjust for changing needs for aircraft type and client airlines financial conditions. For example, in 2017, Aircastle purchased 68 aircraft and sold 37. Brixmor Property Group Inc (NYSE: BRX) is a real estate investment trust (REIT) that owns community and neighborhood strip malls. These malls are typically anchored by a grocery store and the tenants are often in businesses that are largely immune from ecommerce sales competition.

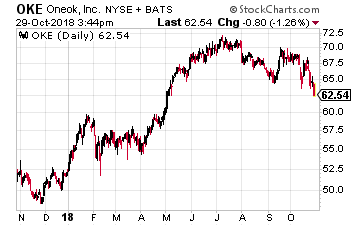

Brixmor Property Group Inc (NYSE: BRX) is a real estate investment trust (REIT) that owns community and neighborhood strip malls. These malls are typically anchored by a grocery store and the tenants are often in businesses that are largely immune from ecommerce sales competition. ONEOK, Inc. (NYSE: OKE) is an energy sector infrastructure services company. ONEOK focuses on natural gas and natural gas liquids (NGLs). The company provides gas gathering services in the energy plays, facilities to process NGLs into the different components like ethane and propane, and interstate pipelines to transport natural gas and NGLs to their demand centers.

ONEOK, Inc. (NYSE: OKE) is an energy sector infrastructure services company. ONEOK focuses on natural gas and natural gas liquids (NGLs). The company provides gas gathering services in the energy plays, facilities to process NGLs into the different components like ethane and propane, and interstate pipelines to transport natural gas and NGLs to their demand centers.

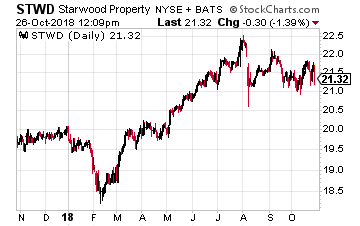

Starwood Property Trust (NYSE: STWD) is a commercial property finance REIT. The book of loans is very conservative with a 62% LTV.

Starwood Property Trust (NYSE: STWD) is a commercial property finance REIT. The book of loans is very conservative with a 62% LTV. Aircastle Limited (NYSE: AYR) may be my personal favorite stock to buy in a bear market. Aircastle is an aircraft leasing company with client airlines around the world.

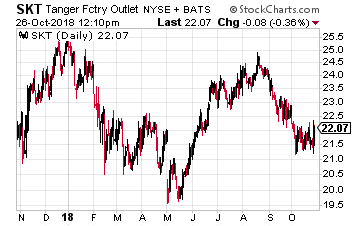

Aircastle Limited (NYSE: AYR) may be my personal favorite stock to buy in a bear market. Aircastle is an aircraft leasing company with client airlines around the world. Tanger Factory Outlet Centers (NYSE: SKT) is the only pure play owner of outlet type shopping centers. In tougher economic times people still like to shop but are more likely to go to an outlet mall to score some deals.

Tanger Factory Outlet Centers (NYSE: SKT) is the only pure play owner of outlet type shopping centers. In tougher economic times people still like to shop but are more likely to go to an outlet mall to score some deals.

PETER KRAUTH

PETER KRAUTH