Source: Shutterstock

Volatility has hit hard again this October. The market has been up one second and down the next. And sadly at this point more down than up. But behind it all the economy remains strong and there are stocks to buy that look as compelling as ever.

“It is February all over again,” Mike Loewengart, CIO of E-Trade Capital Management told CNBC. “We have seen this before; we lived through this eight months ago and we know how that worked out — went to new highs. It was pretty violent and it wasn’t fun, but thing I point out to clients is that this type of volatility is normal.”

Even better, the stock market volatility means you can now snap up some of these stocks at bargain prices. You don’t need to take my word for it. These aren’t just my stock picks. Here I used TipRanks to find the favorite stocks of analysts with a proven track record of success. The idea is that these are analysts you can trust — because you can see their objective track record of success and average return. Why listen to any analyst when you can focus on analysts who time and time have again have proved they know what they’re talking about? It’s your money that’s at stake after all.

All the stocks to buy below share a ‘Strong Buy’ top analyst consensus. That’s with healthy upside potential. Here I dig into why these analysts are so bullish on these stocks right now. Let’s take a closer look:

This isn’t a stock to buy for the fainthearted. So if that’s you I recommend skipping to the next stock. Smartsheet Inc (NYSE:SMAR) is highly valued on any near-term metric. But for investors who have a strong stomach, Smartsheet could be a very lucrative software pick.

Richard Davis (Track Record & Ratings) is the number 1 analyst ranked by TipRanks. He is currently tracking a 36% average return per rating. Right now, he is betting on Smartsheet. That’s with a $35 price target, indicating shares could soar over 47%.

SMAR is basically a software as a service application for collaboration and work management. The company has just held two big events: an analyst day and a user conference. Davis has been at both. “Our offline conversations with customers at the firm’s user conference, bolstered by presentations at the firm’s analyst day leads us to conclude that a BUY rating is still the appropriate rating” he writes.

Net-net this is “a best-in-class company in terms of the key foundational metrics” which now has a $1 billion revenue target in 4-6 years. And what about the valuation? Davis has an answer ready: when growth software stocks are at the foothills of a large TAM opportunity the stocks almost always work. And in this case the probability that Smartsheet executes well for several more quarters, if not years, is high enough to warrant a bullish outlook.

Indeed, the stock has scored only Buy ratings from top analysts. This is with a $36 average price target (51% upside potential). Interested in SMAR stock? Get a free SMAR Stock Research Report.

Top Stocks To Buy: Merck (MRK)

When a stock has managed to climb in these choppy times, you know it must be doing something right. Pharma giant Merck & Co., Inc. (NYSE:MRK) is up over 10% in the last three months. And from top-performing analysts it scores 5 recent Buy ratings. So no Hold or Sell here.

The key product to keep your eye on is Keytruda. This is a prescription medicine that helps the immune system do what it was meant to do: detect and fight cancer cells. Its suitable for specific cancers including non–small cell lung cancer (NSCLC).

“We now see Keytruda as a $17Bn franchise” writes five-star BMO Capital analyst Alex Arfaei (Track Record & Ratings). This is up from his previous estimate of $13.5 billion. As a result, he boosts his MRK price target from $70 to $82 (16% upside potential). Bear in mind that’s the figure he’s expecting for 2030; in the near-term Keytruda should make sales of around $8 billion in 2018.

“Despite over-dependence on Keytruda, Merck is executing very well in the important IO [immunotherapy] market and should maintain leadership” concludes Arfaei. Plus the stock has a number of other growth drivers up its sleev,e including the Gardasil vaccine, animal health and Lynparza for ovarian cancer. Get the MRK Stock Research Report.

Top Stocks To Buy: Lowe’s (LOW)

I have spoken about Lowe’s (NYSE:LOW) before. And chances are high I will speak about LOW again. That’s because the stock has such significant support from top analysts.

In the last three months, 13 top analysts have published Buy ratings on the hardware store. This is 100% support for a stock in the challenging consumer goods sector. Indeed, investors are feeling pretty worried right now about higher rates and the potential for deterioration in the US housing recovery.

So what’s driving the bullish sentiment behind LOW? Top Oppenheimer analyst Brian Nagel (Track Record & Ratings) calls LOW one of his favorite stocks to buy right now. This is with a $140 price target (45% upside potential). “We have studied very carefully myriad housing data and revisited the tenets behind our long-standing, positive calls on LOW” he wrote on October 25.

Now he comes away from this deep dive “with further conviction in the underlying prowess of leading home improvement chains, given a now more diversified product and customer focus and still strong barriers to the threat of online disintermediation.”

As for LOW specifically, he believes new senior management has the potential to revitalize the chain and narrow the productivity gap between LOW and rival HD. So watch this space. Get the LOW Stock Research Report.

Top Stocks To Buy: Microsoft (MSFT)

Microsoft Corporation (NASDAQ:MSFT) is on a roll right now, crushing Street estimates with extremely robust 1Q19 results. This includes a $1.2B revenue beat and an equally impressive $0.18 EPS beat.

Think about this: 1Q19 revenue increased 18.5% y/y to $29.1B. We are now looking the fifth consecutive quarter of double-digit growth for the largest software franchise in the world.

“We would continue to Overweight MSFT shares on a multiyear model transformation driven by fast-growing cloud and internet segments that we estimate could top $70B in revenue by CY20 vs. $18.5B in CY16” says KeyBanc’s Brent Bracelin (Track Record & Ratings).

Bear in mind this analyst falls in the Top 25 out of over 4,800 analysts ranked by TipRanks. In other words, he knows what he’s doing. Bracelin sees prices surging 22% to $125. This is up from $123 previously.

Overall, 15 out of 16 top analysts have published Buy ratings on MSFT in the last three months. Their average price target stands at $123 (20% upside potential). Get the MSFT Stock Research Report.

Top Stocks To Buy: Intuitive Surgical (ISRG)

When an analyst upgrades a stock, it’s time to pay attention. Especially if it comes from a top-performing analyst. So it’s no surprise that robotic surgery stock Intuitive Surgical, Inc.(NASDAQ:ISRG) has caught my eye. The stock has just received an upgrade from five-star Canaccord Genuity analyst Jason Mills (Track Record & Ratings).

Following the move, ISRG now boasts 8 recent buy ratings from top analysts. This is versus just 1 hold rating. We can also see that this comes with a $617 average analyst price target (28% upside potential).

Remember, this is the company behind the groundbreaking Da Vinci robotic system. The system has already brought minimally invasive surgery to more than 3 million patients worldwide. It allows the surgeon’s hand movements to be translated into smaller, precise movements of tiny instruments inside the patient’s body.

The analyst comments “While valuation is not cheap, it has moderated materially in this latest market downdraft. Importantly, we think the robotics revolution, which ISRG looks primed to continue to lead via massive investment in next-generation technology, is actually gaining momentum.”

Mills concludes: “We would accumulate shares notwithstanding expected strength in the stock on the heels of its robust Q3 print.” He has a $610 price target on the stock. Get the ISRG Stock Research Report.

Top Stocks To Buy: Gray Television (GTN)

If you are looking for a lower-priced stock that still packs a big punch, look no further. Gray Television (NYSE:GTN) has received 3 recent buy ratings — all from top analysts. These analysts (on average) see prices surging from $16.60 to $23.67. In other words, this means upside potential of over 42%.

The stock has two primary revenue sources: owning and operating TV stations in the US and selling internet ads on its stations’ websites. But what really gives the company its investing edge is, that’s right, political dollars. This is because its strong positioning in its markets (i.e. holding the #1/#2 spot) makes its stations a must buy for political candidates and political action committees (PACs).

“Gray’s appealing fundamentals are led by its proven ability to capitalize on available political dollars as a direct consequence of its exceptional dominance in local news” gushes five-star Barrington analyst James Goss (Track Record & Ratings). This is all the more so given 1) 2018 midterms 2) highly competitive senator and governor races and 3) higher level of voter engagement which has spurred political fundraising through the roof. Get the GTN Stock Research Report.

Top Stocks To Buy: Centene Corp (CNC)

Speaking of upgrades, Leerink Partners has just shifted Centene Corporation (NYSE:CNC) from Hold to Buy. The company is a multi-line healthcare enterprise that provides services to government healthcare programs.

Ana Gupte (Track Recrd & Ratings) — a top-performing analyst at Leerink — also ramped up her CNC price target from $130 to $155. She made the move following solid Q3 earning results, citing “the blessing of consensus 2019E EPS on the Q3 commentary.” Moreover, a soft 2018 performance year-to-date means that margin risk is finally priced in the analyst adds.

Also worthy of note: Oppenheimer’s Michael Wiederhorn is even more bullish on Centene’s potential. Following earnings, he took his price target from $158 to $165 (27% upside potential).

“We view the margin opportunity as significant, as the company’s large new-member population is likely to take time to mature to legacy margins” Wiederhorn explains. “As a result, we believe Centene will continue to boast strong revenue and earnings growth prospects for years to come.”

With 6 recent buy ratings vs 1 hold rating, Centene’s consensus stands at ‘Strong Buy’ while its upside potential pushes past 23%. Get the CNC Stock Research Report.

TipRanks.com offers exclusive insights for investors by focusing on the moves of experts: Analysts, Insiders, Bloggers, Hedge Fund Managers and more. See what the experts are saying about your stocks now at TipRanks.com. As of this writing, Harriet Lefton did not hold a position in any of the aforementioned securities.

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

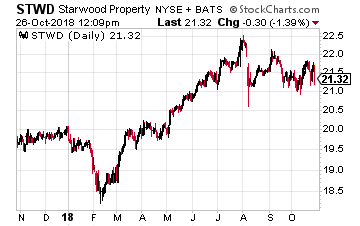

Starwood Property Trust (NYSE: STWD) is a commercial property finance REIT. The book of loans is very conservative with a 62% LTV.

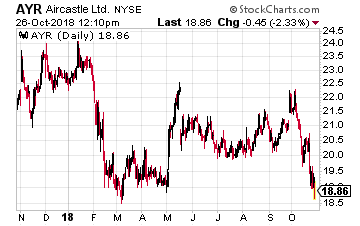

Starwood Property Trust (NYSE: STWD) is a commercial property finance REIT. The book of loans is very conservative with a 62% LTV. Aircastle Limited (NYSE: AYR) may be my personal favorite stock to buy in a bear market. Aircastle is an aircraft leasing company with client airlines around the world.

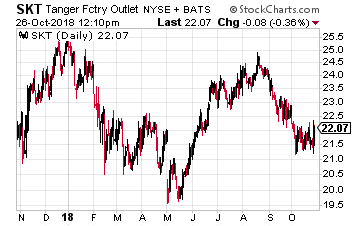

Aircastle Limited (NYSE: AYR) may be my personal favorite stock to buy in a bear market. Aircastle is an aircraft leasing company with client airlines around the world. Tanger Factory Outlet Centers (NYSE: SKT) is the only pure play owner of outlet type shopping centers. In tougher economic times people still like to shop but are more likely to go to an outlet mall to score some deals.

Tanger Factory Outlet Centers (NYSE: SKT) is the only pure play owner of outlet type shopping centers. In tougher economic times people still like to shop but are more likely to go to an outlet mall to score some deals.