Fast-casual food chain Chipotle (NYSE:CMG) will report third-quarter numbers after the bell on Thursday, and I think those numbers will be good enough to spark a bounce-back rally in recently beaten up Chipotle stock.

The story here is pretty simple. After the recent correction, CMG is finally entering reasonably valued territory. Meanwhile, the stock is down more than 10% since the last earnings report. That combination of recent declines and reasonable valuation imply that if third-quarter numbers are strong, Chipotle stock could stage a meaningful rally.

I think that is exactly what will happen. The restaurant backdrop is exceedingly favorable right now. Macro research firms point to red-hot restaurant sales, while fast-casual peers have mostly reported strong third-quarter numbers recently. Also, it appears that Chipotle’s new initiatives with menu innovations and delivery are progressing nicely.

All in all, CMG looks attractive ahead of the third-quarter print. You have a really beaten up stock with a reasonable valuation heading into a report that should be pretty good. Put that all together and you could get a nice post-earnings rally in Chipotle stock.

Third Quarter CMG Numbers Should Be Good

There is a good chance that Chipotle reports above-consensus third-quarter numbers that impress investors. Why? Two major reasons. One, the whole restaurant industry is on fire right now. Two, Chipotle’s strategic menu innovation and delivery initiatives are doing well.

With respect to the first reason, there is little doubt out there about the strength of the U.S. restaurant industry at the present moment. According to research firm TDn2K, the restaurant industry saw its biggest sales and traffic growth in three years during the third quarter. Meanwhile, retail sales at food services and drinking places were up a robust 8.8% year-over-year during the past three months.

This strong macro data is corroborated by what has been a string of positive earnings reports from fast-casual chains. Most of those chains that have reported third-quarter numbers so far have reported strong double-beat-and-raise quarters, headlined by McDonald’s (NYSE:MCD), Dunkin’ (NYSE:DNKN) and Darden (NYSE:DRI).

Broadly speaking, then, the whole restaurant industry has beenperforming extremely well. It is reasonable to assume that this is a rising tide that lifted all boats, Chipotle included, especially considering it has been largely (but not entirely) out of the spotlight recently when it comes to health scares.

Moreover, CMG’s strategic initiatives in menu innovation and delivery were smart moves, and I have faith those initiatives continued to yield material benefits this past quarter. Menu innovations keep customers interested and attract new customers, and Chipotle kept up the menu innovations in the quarter (earlier in the quarter, they were testing bacon and nachos). On the delivery front, Chipotle stock has deepened its partnership with Postmates, and that is a good thing as it extends reach.

If the report is as good as these developments suggest, you could get a nice post-earnings pop in Chipotle stock.

Chipotle Stock Could Pop

Chipotle stock could pop on strong third quarter numbers for two reasons. The valuation has depressed into reasonable territory, and the stock has been beaten up since the last earnings report, implying low buy-side expectations.

On the valuation front, the simple truth about Chipotle stock is that at $250, it was way undervalued, and at $500, it was way overvalued. This is a company which is on a steady, but not explosive, sales recovery trajectory.

Meanwhile, margins will continue to be pressured by lower unit performance, higher wages and new initiatives spend. Thus, in the big picture, the Chipotle profit recovery is happening, but not quickly. Under those assumptions, this is a company which I think can do about $30 in EPS in five years. Throw a McDonald’s-level 20X forward multiple on that, and discount back by 10% per year. You arrive at a 2018 price target of $450.

Thus, at $250, Chipotle stock was undervalued. At $500, it was overvalued. Now, at $420, it is reasonably valued.

Meanwhile, Chipotle stock is down more than 10% since the last earnings report, and more than 20% off recent highs. That means buy-side expectations for Q3 are low. With expectations low and the valuation now in reasonable territory, Chipotle stock is positioned for a nice rally in the event Q3 numbers are strong.

There are reasons to be cautiously optimistic on Chipotle stock ahead of the Q3 print. You have a beaten up stock with a reasonable valuation heading into a Q3 print which could be quite good. That set-up implies that in the event of good numbers, Chipotle stock could stage a healthy rally.

As of this writing, Luke Lango was long CMG and MCD.

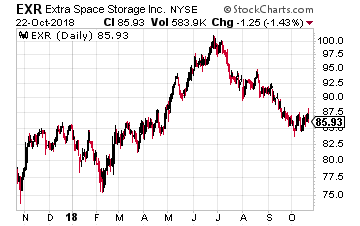

Extra Space Storage (NYSE: EXR) owns or manages almost 1,600 self-storage properties with 115 million rentable square feet. EXR is a real estate investment trust, which means it must pay out the majority of net income as dividends to investors.

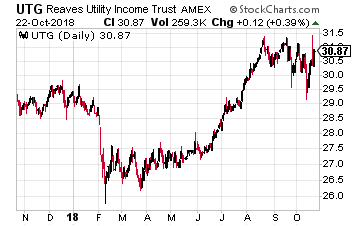

Extra Space Storage (NYSE: EXR) owns or manages almost 1,600 self-storage properties with 115 million rentable square feet. EXR is a real estate investment trust, which means it must pay out the majority of net income as dividends to investors. For this market sector I like the Reaves Utility Income Fund (NYSE: UTG). This is a closed-end fund that owns a diversified portfolio of utility and related stocks. Reaves Asset Management focuses only on utility and infrastructure stock investments.

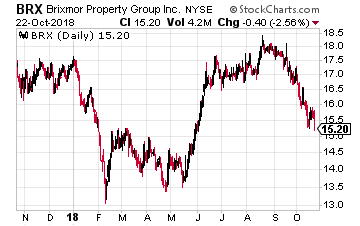

For this market sector I like the Reaves Utility Income Fund (NYSE: UTG). This is a closed-end fund that owns a diversified portfolio of utility and related stocks. Reaves Asset Management focuses only on utility and infrastructure stock investments. Brixmor Property Group (NYSE: BRX) owns 471 open air shopping centers. The company focuses on centers that are the center of their communities. Anchor tenants are the main revenue drivers for Brixmor, and over half of those tenants are grocery stores.

Brixmor Property Group (NYSE: BRX) owns 471 open air shopping centers. The company focuses on centers that are the center of their communities. Anchor tenants are the main revenue drivers for Brixmor, and over half of those tenants are grocery stores.

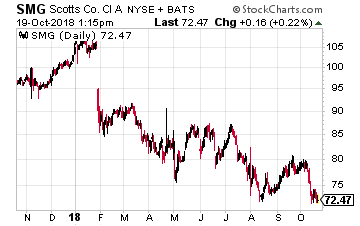

It is very possible that you are familiar with The Scotts Miracle-Gro Company (NYSE: SMG). Scotts is the world’s largest marketer of branded consumer lawn and garden products. In the case of the pot market, the company offers the necessary solutions to enhance the abilities of a marijuana business to produce product.

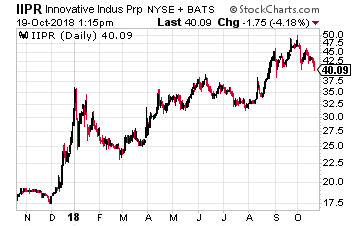

It is very possible that you are familiar with The Scotts Miracle-Gro Company (NYSE: SMG). Scotts is the world’s largest marketer of branded consumer lawn and garden products. In the case of the pot market, the company offers the necessary solutions to enhance the abilities of a marijuana business to produce product. Innovative Industries Properties (NYSE: IIPR) is a REIT that calls itself “The Leading Provider of Real Estate Capital for the Medical-Use Cannabis Industry.”

Innovative Industries Properties (NYSE: IIPR) is a REIT that calls itself “The Leading Provider of Real Estate Capital for the Medical-Use Cannabis Industry.”

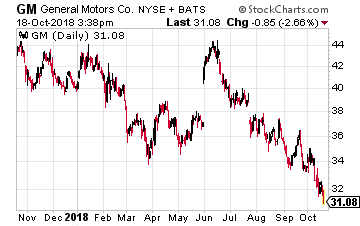

Or as GM president Dan Ammann said recently to the Financial Times, “We see this as the race to the starting line.” In other words, the real race hasn’t even started.

Or as GM president Dan Ammann said recently to the Financial Times, “We see this as the race to the starting line.” In other words, the real race hasn’t even started. General Motors (NYSE: GM) seems to have bolstered its claim to be the leading carmaker developing self-driving systems after Hondainvested $750 million into its Cruise division, with the promise of a total of $2.75 billion over 12 years.

General Motors (NYSE: GM) seems to have bolstered its claim to be the leading carmaker developing self-driving systems after Hondainvested $750 million into its Cruise division, with the promise of a total of $2.75 billion over 12 years.

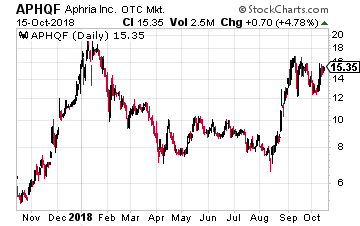

Finally, we have Big Tobacco moving into the marijuana space also. The biggest U.S. cigarette company, Altria Group (NYSE: MO) is reportedly in talks to buy a stake in Aphria (OTC: APHQF).

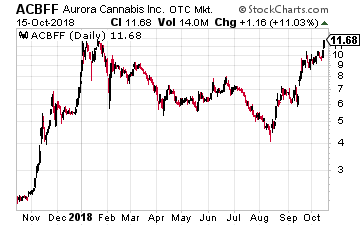

Finally, we have Big Tobacco moving into the marijuana space also. The biggest U.S. cigarette company, Altria Group (NYSE: MO) is reportedly in talks to buy a stake in Aphria (OTC: APHQF). A better choice is Canada’s second-biggest marijuana company, Aurora Cannabis (OTC: ACBFF), which is the company Coke is believed to talking to about a deal. Its $2 billion deal to take over rival MedReLeaf in May was the largest deal in the sector at the time.

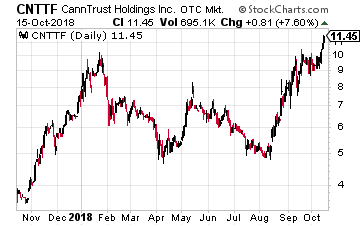

A better choice is Canada’s second-biggest marijuana company, Aurora Cannabis (OTC: ACBFF), which is the company Coke is believed to talking to about a deal. Its $2 billion deal to take over rival MedReLeaf in May was the largest deal in the sector at the time. Another company I would consider is CannTrust Holdings (OTC: CNTTF), which will be listing soon also on a major U.S. stock exchange. It is in active discussions with a number of firms in the beverage, food and cosmetics industries and expects to announce a deal within the next two months.

Another company I would consider is CannTrust Holdings (OTC: CNTTF), which will be listing soon also on a major U.S. stock exchange. It is in active discussions with a number of firms in the beverage, food and cosmetics industries and expects to announce a deal within the next two months.