In today’s world, there is one certainty when it comes to investing that you need to be aware of… new technologies will disrupt nearly every industry.

Take the stodgy airline industry. The Internet of Things (IoT) is about to make airlines more profitable than they’ve ever been in the past. I’m sure you’re wondering how this will be accomplished. Simple – instead of treating their passengers as mere travelers, airlines are beginning to look at them as online consumers that just happen to be on their plane.

Before I delve into more details, let me fill you in on more background on the industry.

Airlines and Ancillary Revenues

In this age of low-cost airlines, the days of when airlines made the majority of their money from airfares are largely gone. Thanks to low-cost airlines, so-called ancillary services have become a mainstay and an important source of revenues for all of them.

A report last month from the research firm IdeaWorksCompany in conjunction with the online car rental company CarTrawler gave insight into the growth of ancillary fees. The report projected that for 2017 airlines will have received a total of $82.2 billion in ancillary revenues. That is about 10.6% of their projected total revenues for 2017.

That $82.2 billion number is also a 22% increase from 2016, with most of the ancillary revenues being garnered by the traditional airlines. Quite a contrast from just 10 years ago when the top 10 airlines (ranked by add-on services) earned only $2.1 billion from ancillary services.

One main reason is the fact that, within the domestic U.S. market and the short-haul operations of airlines outside the U.S., the prevalence of a ‘Basic Economy’ product has driven ancillary sales. The aforementioned report cites airline estimates that over 50% of passengers who purchase this product opt for higher priced bundling options.

Since IdeaWorksCompany released its first report in 2010, the growth of ancillary revenue for airlines has been significant. At that time, the total figure was $22.6 billion with an average spend per passenger of $8.42. Utilizing worldwide passenger numbers provided by IATA (International Air Transport Association), the latest report showed an average spend per passenger of $20.13, with $13.96 being accounted for by to a la carte services, up from just $4.54 in 2010.

However, the lure of buying duty-free goods on airlines is becoming stale for passengers. A 2016 report from m1nd-set Generation forecast such sales would experience an annual growth rate of minus 1.5% for airlines through 2025.

Another revenue source has to be found and quickly. And it’s there… awaiting the airlines that adopt in-flight broadband and Wi-Fi – the Internet of Things in the air.

Passengers Want to Be Connected

Passengers’ expectations of the in-flight experience is changing rapidly. They now expect the same level of connectivity at an altitude of 30,000 feet as they do on the ground.

That much was pretty clear in a study conducted by the market research firm GfK and Inmarsat PLC (OTC: IMASY), the world’s leading provider of global mobile satellite communications. Here are the quite interesting results:

- 60% of passengers believe in-flight WiFi is a necessity, not a luxury.

- 61% of passengers said Wi-Fi is more important than onboard entertainment.

- 45% of passengers said they would gladly pay for WiFi rather being stuck with the onboard entertainment options.

- 66% of passengers traveling with children would consider in-flight internet a “life saver”.

Connectivity now ranks behind only ticket prices and flight slots as a priority for passengers. That could be seen when that same survey revealed 44% of passengers would switch airlines within a year if what they considered to be a minimal level of connectivity was not available. This is especially true of business travelers, as 56% said they want the ability to work while in flight.

Shopping at 30,000 Feet

Yet, most airlines still lag in offering connectivity to their passengers. The aforementioned report from IdeaWorks found that a mere 53 of the world’s estimated 5,000 airlines offer “in-flight broadband connectivity.”

Many seem unaware that they now have access to a global, reliable broadband network in-flight. As David Coiley of Inmarsat Aviation told the Financial Times, “Airlines have to adapt to this new opportunity.”

And it is an opportunity. Consider shopping an online store at 30,000 feet filled with everything from ground transport options to tours to other destination-related activities. Or returning passengers could do their grocery shopping while in-flight to have the groceries delivered when they arrive home. The possibilities are almost endless.

Related: The Bull Market Case for Buying Airline Stocks

A study conducted by the London School of Economics and Inmarsat said that in-flight broadband – offering streaming and online shopping to passengers could create a $130 billion global market within the next 20 years. The study estimated that the airlines’ share of that total could amount to $30 billion in 2035. That’s quite a jump from the forecast $900 million in 2018.

Investing in Airlines Buffett Used to Hate

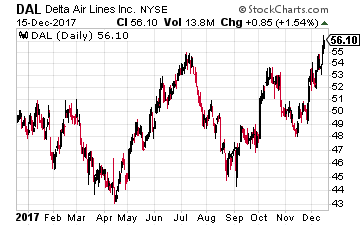

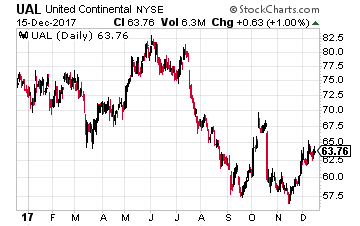

With this possibility of e-commerce revenue streams in the not too distant future, it may be time to look at the airlines. Even long-time skeptic Warren Buffett now owns airline stocks including Southwest Airlines, AmericanAirlines, Delta Air Lines (NYSE: DAL) and United Continental Holdings (NYSE: UAL).

If you are thinking of going the same route as Warren Buffett, I would stick with the airlines that have the best Wi-Fi connectivity. Conde Nast Traveler magazine reports that a survey from Routehappy found that U.S. airlines are leading the way, with at least a chance of Wi-Fi on 83% of the total seating capacity.

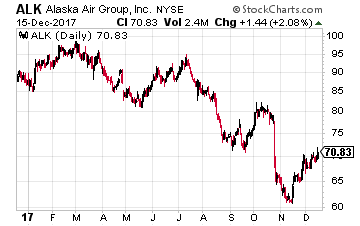

Two of the top three airlines globally with the highest percentage of seats with Wi-Fi connectivity, according to the survey, are Delta Air Lines and United. Other smaller airlines with good connectivity are JetBlue and Virgin America, which was sold to Alaska Air Group (NYSE: ALK). I would focus on Delta, United, and Alaska Air.

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually.

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually.

Despite two major U.S. hurricanes, passenger revenue per available seat mile rose 1.9% year-over-year in the third quarter. The company forecast that in the fourth quarter this metric would climb somewhere between 2% and 4%, which is encouraging.

The company’s stock is up nearly 10% year-to-date. Nevertheless, it is trying to enhance its shareholders’ wealth through dividends and share buybacks. In May 2017, Delta announced that its board of directors approved a new share repurchase program worth $5 billion and raised its quarterly dividend by more than 50%. In the third quarter, Delta returned $769 million to its shareholders through dividends ($219 million) and buybacks ($769 million).

Another plus is the company’s discipline, which is sometimes a rarity in the airline industry. In the third quarter, Delta expanded capacity less than traffic growth and thus improved load factor by 150 basis points to 86.9%.

United is the world’s largest airline, operating about 5,000 flights a day. Unlike Delta, it is not showing growth in its passenger revenue per available seat mile. But it is showing improvement – the company’s latest estimate is for it to be flat to down 2% year-over-year. That compares to the previous estimate of down 1% to 3%.

United is the world’s largest airline, operating about 5,000 flights a day. Unlike Delta, it is not showing growth in its passenger revenue per available seat mile. But it is showing improvement – the company’s latest estimate is for it to be flat to down 2% year-over-year. That compares to the previous estimate of down 1% to 3%.

Its return on equity (ROE) is 25.3% should support its robust expansion plans. Its ROE is impressive too when compared to that of the S&P 500, which comes in at only 16.1%. And it is cheap. Its trailing 12-month enterprise value to earnings before interest, tax, depreciation and amortization ratio is only 4.6. That compares to the value for the S&P 500 of 11.7.

The company’s stock has had a tough year and is down 13.25% year-to-date. Maybe that’s why it has stepped up its efforts to reward its shareholders. It has bought back $1.3 billion of stock in the first nine months of 2017. And in December, its board of directors gave the go-ahead for an additional share repurchase program worth $3 billion.

Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like its purchase of Virgin America this year, despite the rise in the amount of debt it now has. The company also owns Horizon Air.

Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like its purchase of Virgin America this year, despite the rise in the amount of debt it now has. The company also owns Horizon Air.

No denying that 2017 has not been a good year for its shareholders, with the stock down 21.5%. And like its airline peers, Alaska Air management is attempting to reward its patient shareholders through share buybacks and dividends. The company has increased its dividend every year since inception and will spend about $145 million on dividends in 2017.

Its after-tax return on invested capital (ROIC) is a very respectable 21.3% and its estimated 2017 pre-tax margin of 25% should lead the industry. In the first nine months of 2017, Alaska Air generated revenues passenger mile of just over 39 billion (up 6.6% year over year). Its load factor stood at 84.6%, compared with 84.2% in the first nine months last year.

The bottom line is that it has been a turbulent year for airline stocks as the combination of natural disasters and terrorist attacks have taken their toll. Not to mention industry overcapacity, high labor costs, and now rising fuel costs.

But now may be the time for contrarian investors to look past the short-term turbulence and take a small position in the airlines that are forward-looking. I fully expect we won’t recognize the industry in a decade as technology disrupts it.

Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

Source: Investors Alley

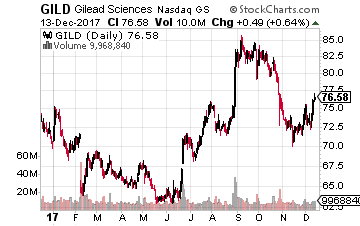

The first company I want to tell you about is Gilead Sciences (Nasdaq: GILD), which revealed results of a trial that took place at the University of Texas on December 10. The trial was conducted by what is now a subsidiary of Gilead – Kite Pharma – that was acquired in August for $11.9 billion.

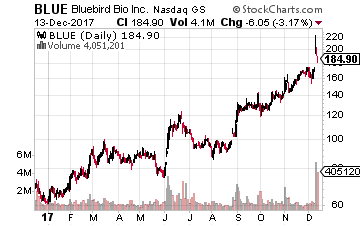

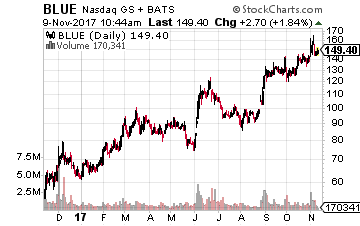

The first company I want to tell you about is Gilead Sciences (Nasdaq: GILD), which revealed results of a trial that took place at the University of Texas on December 10. The trial was conducted by what is now a subsidiary of Gilead – Kite Pharma – that was acquired in August for $11.9 billion. The second company, which revealed spectacular trial results at the Atlanta conference, is Bluebird Bio (Nasdaq: BLUE). The stock soared about 30% on December 11 and is now up about 225% year-to-date!

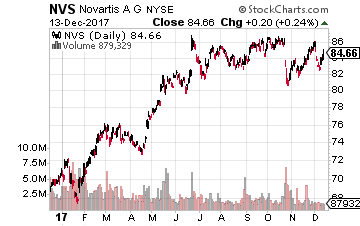

The second company, which revealed spectacular trial results at the Atlanta conference, is Bluebird Bio (Nasdaq: BLUE). The stock soared about 30% on December 11 and is now up about 225% year-to-date! That brings me to the third Car-T company with promising results presented in Atlanta, Novartis, and its Kymriah therapy, which was given the go-ahead by the FDA in August. The stock of this pharma giant is up over 15% year-to-date.

That brings me to the third Car-T company with promising results presented in Atlanta, Novartis, and its Kymriah therapy, which was given the go-ahead by the FDA in August. The stock of this pharma giant is up over 15% year-to-date.

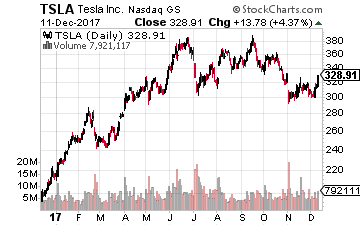

Elon Musk unveiled Tesla’s electric truck last month that has been in development for over a year. It is supposed to have a range of about 500 miles and, according to Musk, will be “impossible” to jackknife. He said that it would go into production in late 2019.

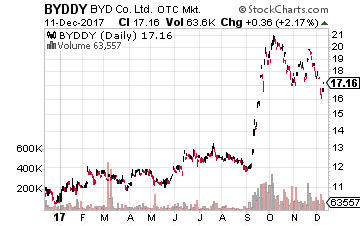

Elon Musk unveiled Tesla’s electric truck last month that has been in development for over a year. It is supposed to have a range of about 500 miles and, according to Musk, will be “impossible” to jackknife. He said that it would go into production in late 2019. Just look at China and e-buses. Just a few years ago, China only produced about 10,000 electric buses. But in 2016, output exceeded 100,000 buses. Market leader BYD (OTC: BYDDY) has also begun to churn out a good number of electric garbage trucks. The company, 8.5% owned by Warren Buffett, has been assembling them for two years at a California plant and is opening another facility in Ontario, Canada next year.

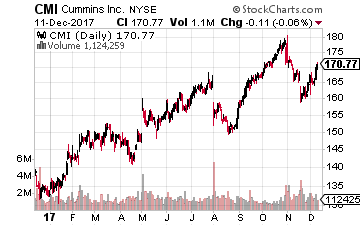

Just look at China and e-buses. Just a few years ago, China only produced about 10,000 electric buses. But in 2016, output exceeded 100,000 buses. Market leader BYD (OTC: BYDDY) has also begun to churn out a good number of electric garbage trucks. The company, 8.5% owned by Warren Buffett, has been assembling them for two years at a California plant and is opening another facility in Ontario, Canada next year. The first company is Cummins (NYSE: CMI), which will not build electric trucks. But it will supply a fully-integrated battery electronics system (with the batteries coming from an unnamed supplier. It is a leading maker of diesel and natural gas engines for commercial trucks.

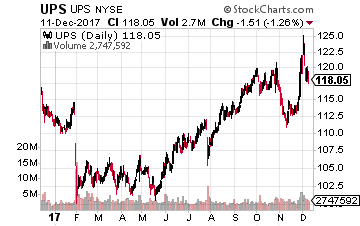

The first company is Cummins (NYSE: CMI), which will not build electric trucks. But it will supply a fully-integrated battery electronics system (with the batteries coming from an unnamed supplier. It is a leading maker of diesel and natural gas engines for commercial trucks. Daimler introduced the light-duty eCanter haulers in New York in September, supplying a fleet to several New York City non-profits as well as signing United Parcel Service (NYSE: UPS) as its first commercial customer in the U.S. The truck has a range of 60 to 80 miles between charges and is coming to market as customers insist on cleaner vehicles better-suited to rising delivery demand (e-commerce) in cities.

Daimler introduced the light-duty eCanter haulers in New York in September, supplying a fleet to several New York City non-profits as well as signing United Parcel Service (NYSE: UPS) as its first commercial customer in the U.S. The truck has a range of 60 to 80 miles between charges and is coming to market as customers insist on cleaner vehicles better-suited to rising delivery demand (e-commerce) in cities. Another European company that Tesla should worry about is Volvo AB (OTC: VLVLY).

Another European company that Tesla should worry about is Volvo AB (OTC: VLVLY).

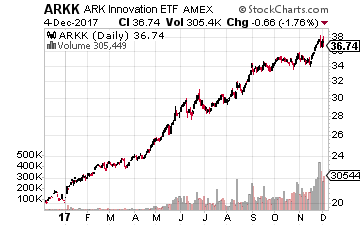

One very conservative way is through an exchange traded fund – the Ark Innovation ETF (NYSE: ARKK). The goal of this fund is to provide investors like you with exposure to innovation and new technologies across a broad range of sectors. The ARKK ETF owns a position in the aforementioned Bitcoin Investment Trust. The Bitcoin Investment Trust is the number one position in its current 53 stock portfolio and it makes up 6.79% of the overall ARKK investment portfolio. In other words, any major selloff (noted short seller Andrew Left is short GBTC) won’t devastate the fund.

One very conservative way is through an exchange traded fund – the Ark Innovation ETF (NYSE: ARKK). The goal of this fund is to provide investors like you with exposure to innovation and new technologies across a broad range of sectors. The ARKK ETF owns a position in the aforementioned Bitcoin Investment Trust. The Bitcoin Investment Trust is the number one position in its current 53 stock portfolio and it makes up 6.79% of the overall ARKK investment portfolio. In other words, any major selloff (noted short seller Andrew Left is short GBTC) won’t devastate the fund.

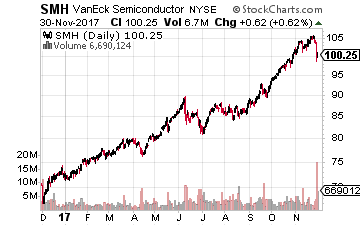

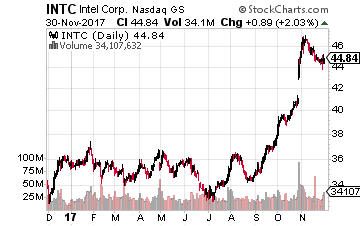

The first and the broadest way you can invest in semiconductors is the MarketVectors Semiconductor ETF (NYSE: SMH). It owns 26 of the world’s top semiconductor-related companies such as Intel. The only major stock not in this portfolio is Samsung. This ETF has, of course, done very well for its holders. It has soared over 50% over the past year and is up about 42% year-to-date.

The first and the broadest way you can invest in semiconductors is the MarketVectors Semiconductor ETF (NYSE: SMH). It owns 26 of the world’s top semiconductor-related companies such as Intel. The only major stock not in this portfolio is Samsung. This ETF has, of course, done very well for its holders. It has soared over 50% over the past year and is up about 42% year-to-date.

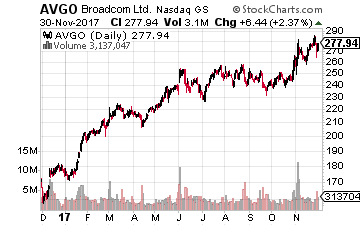

Next up is Broadcom (Nasdaq: AVGO), which is currently attempting to take over rival Qualcomm. Its stock is up 55% year-to-date and about the same amount over the past year.

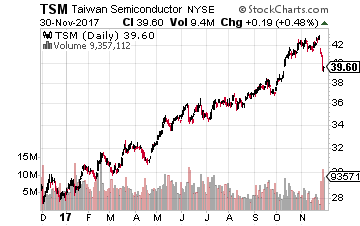

Next up is Broadcom (Nasdaq: AVGO), which is currently attempting to take over rival Qualcomm. Its stock is up 55% year-to-date and about the same amount over the past year. Finally, we come to Taiwan Semiconductor (NYSE: TSM), whose stock is up 37% year-to-date and about 33% over the last 12 months.

Finally, we come to Taiwan Semiconductor (NYSE: TSM), whose stock is up 37% year-to-date and about 33% over the last 12 months.

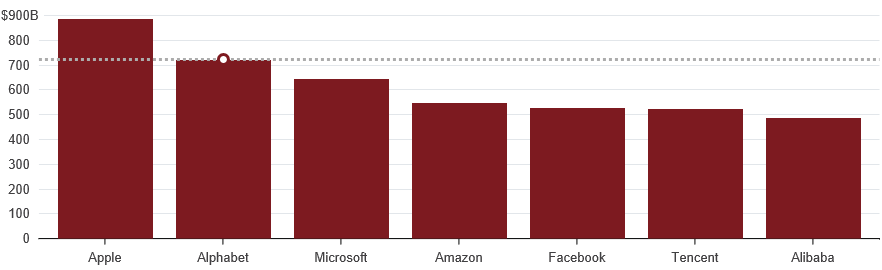

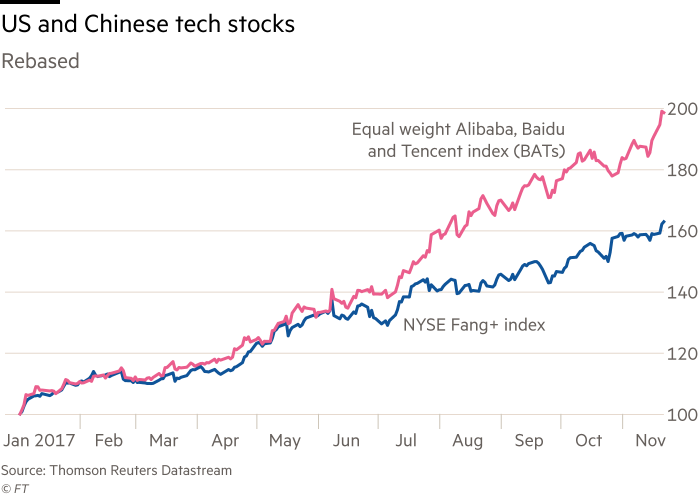

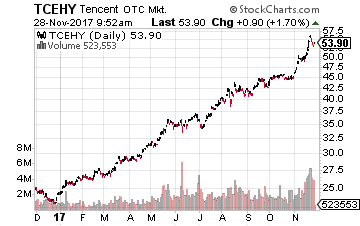

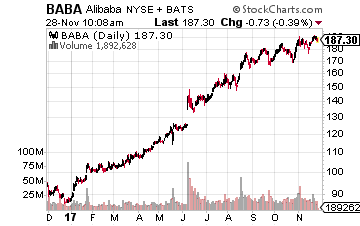

This differential came to the fore last week when, at least temporarily, Tencent surpassed Facebook in market capitalization. It became the first of the Chinese tech titans to surpass $500 billion in valuation. It temporarily pushed Facebook out of the top 5 globally in market cap.

This differential came to the fore last week when, at least temporarily, Tencent surpassed Facebook in market capitalization. It became the first of the Chinese tech titans to surpass $500 billion in valuation. It temporarily pushed Facebook out of the top 5 globally in market cap. Currently, Alibaba is number one in the sector, as its Alipay unit has a 54% market share. But Tencent’s WeChatPay is closing fast with a 40% market share.

Currently, Alibaba is number one in the sector, as its Alipay unit has a 54% market share. But Tencent’s WeChatPay is closing fast with a 40% market share.

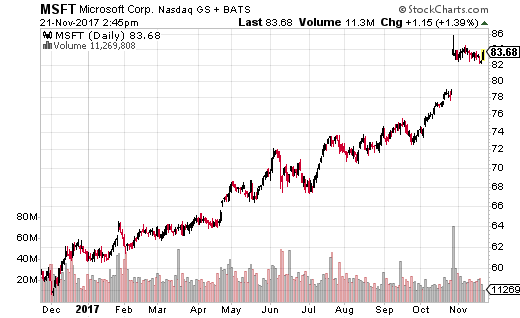

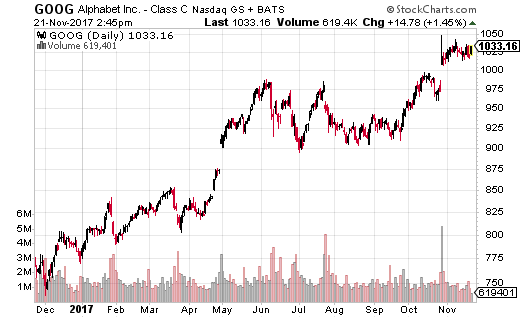

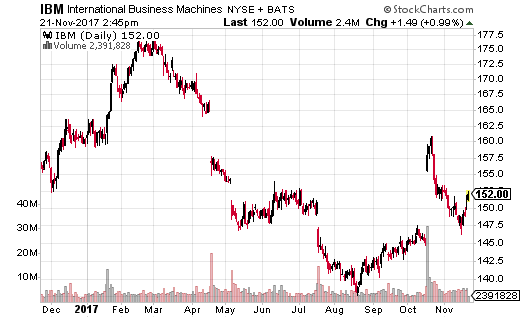

Luckily, a number of the top U.S. technology companies are working hard on scaling up quantum computing technology. The companies involved in this ‘arms race’ include as I mentioned Microsoft (Nasdaq: MSFT) as well asAlphabet (Nasdaq: GOOG) and IBM (NYSE: IBM).

Luckily, a number of the top U.S. technology companies are working hard on scaling up quantum computing technology. The companies involved in this ‘arms race’ include as I mentioned Microsoft (Nasdaq: MSFT) as well asAlphabet (Nasdaq: GOOG) and IBM (NYSE: IBM).

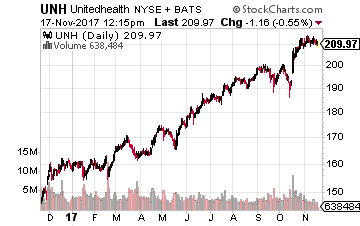

Among the companies in the prescription drug distribution sector, I believe the best of the lot is UnitedHealth Group. About 40% of its revenues come its Optum Rx PBM business, with the remaining 60% of revenues coming from its vast health insurance businesses.

Among the companies in the prescription drug distribution sector, I believe the best of the lot is UnitedHealth Group. About 40% of its revenues come its Optum Rx PBM business, with the remaining 60% of revenues coming from its vast health insurance businesses.

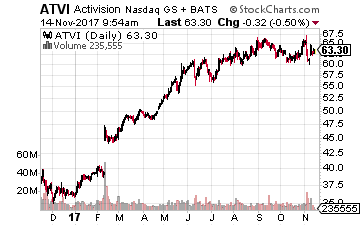

At the top of my buy list is the aforementioned Activision Blizzard, which also has a live streaming channel called Major League Gaming. It acquired the firm in 2016 for $46 million.

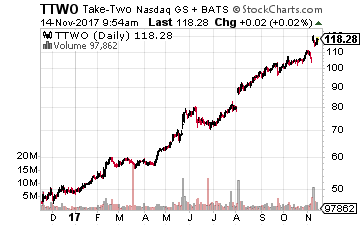

At the top of my buy list is the aforementioned Activision Blizzard, which also has a live streaming channel called Major League Gaming. It acquired the firm in 2016 for $46 million. Next on the list is a rival of Activision, Take Two Interactive Software (Nasdaq: TTWO), which is best known for its Grand Theft Auto franchise. Its stock soared nearly 10% after its recently-released earnings report.

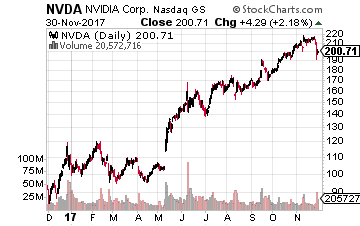

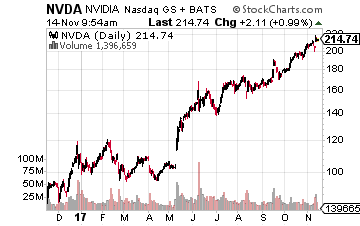

Next on the list is a rival of Activision, Take Two Interactive Software (Nasdaq: TTWO), which is best known for its Grand Theft Auto franchise. Its stock soared nearly 10% after its recently-released earnings report. Finally, an alternative way to play the e-sports trend is through the semiconductor company, Nvidia (Nasdaq: NVDA). Its stock has soared 101% year-to-date and 144% over the past 52 weeks. As I’m sure you may know, Nvidia is a worldwide leader in visual computing technologies and the inventor of the graphic processing unit, or GPU.

Finally, an alternative way to play the e-sports trend is through the semiconductor company, Nvidia (Nasdaq: NVDA). Its stock has soared 101% year-to-date and 144% over the past 52 weeks. As I’m sure you may know, Nvidia is a worldwide leader in visual computing technologies and the inventor of the graphic processing unit, or GPU.

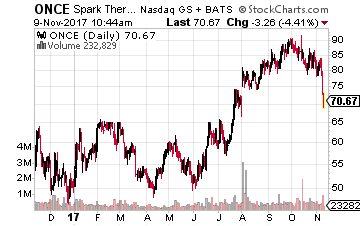

Let’s start with Spark Therapeutics. Most of the company’s $2.8 billion market capitalization is not due to Luxurna. The real excitement for the company comes from several early-stage gene therapy projects that are aimed at hemophilia.

Let’s start with Spark Therapeutics. Most of the company’s $2.8 billion market capitalization is not due to Luxurna. The real excitement for the company comes from several early-stage gene therapy projects that are aimed at hemophilia. Gene Therapy Stock #2 – Bluebird Bio

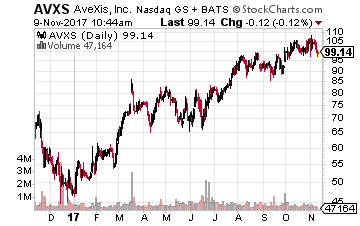

Gene Therapy Stock #2 – Bluebird Bio The third clinical-stage company worth a look is AveXis (Nasdaq: AVXS). The company’s primary focus is on gene therapies to develop a cure for Spinal Muscular Atrophy (SMA), Rett Syndrome and a genetic basis for ALS (Lou Gehrig’s disease).

The third clinical-stage company worth a look is AveXis (Nasdaq: AVXS). The company’s primary focus is on gene therapies to develop a cure for Spinal Muscular Atrophy (SMA), Rett Syndrome and a genetic basis for ALS (Lou Gehrig’s disease).