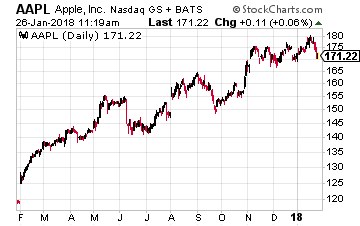

Apple (Nasdaq: AAPL) just set a record for the most profitable quarter in the company’s history. Not surprising since Apple executives said in November that they were expecting its “biggest quarter ever” and a return to double-digit revenue growth for the first time in years.

But not all is well with the world’s largest company by market capitalization. One needs look no further than the stock’s relative performance to the S&P 500 index over the last three month period. Apple has been a definite laggard.

I expect that relative underperformance to continue. Here are two reasons why:

Reason #1 – Overpriced iPhoneX?

Apple may have made a classic mistake and priced the new iPhoneX too high, thinking its fans would pay any price for its phones.

This phone is the first from Apple with an organic light-emitting diode (OLED) display. It also features facial recognition and wireless charging. But many complain it lacks groundbreaking new technologies when compared to some of Apple’s previous models. In other words, the same old complaint under the leadership of Tim Cook – a lack of innovation.

The iPhoneX price starts at $999 here in the U.S. And in the very important China market, the cost starts at a whopping $1,334! This is crucial since, in December, the flagship Mate 10 Pro from China’s Huawei was launched at a starting price of just over half the cost of the iPhoneX. In the latest survey of Chinese consumers, Apple still lags Huawei in what brand their next smartphone purchase will be. As recently as 2015, Apple was named by twice as many consumers as Huawei was.

What really caught my eye though was the article last week in the Nikkei Asian Review that revealed Apple had told its Asian suppliers it was slashing its production target for the iPhoneX by half for the first three months of 2018. Production was slashed because sales had failed to meet Apple’s lofty expectations. If sales are faltering, that means the whole Wall Street tale about the iPhoneX supercycle was a myth.

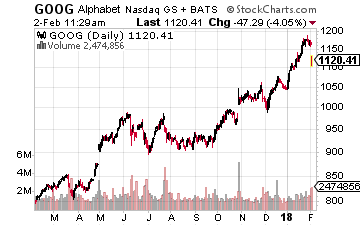

And let’s not forget that there continues to be intensifying competition in the premium smartphone market. Alphabet (Nasdaq: GOOG) officially closed its $1.1 billion deal with HTC Corp., adding more than 2,000 smartphone specialists in Taiwan. This is expected to help Google chase Apple in the increasingly cut-throat premium handset market.

And let’s not forget that there continues to be intensifying competition in the premium smartphone market. Alphabet (Nasdaq: GOOG) officially closed its $1.1 billion deal with HTC Corp., adding more than 2,000 smartphone specialists in Taiwan. This is expected to help Google chase Apple in the increasingly cut-throat premium handset market.

Reason #2 – Smart Speaker Delay

In relation to the entire innovation question, I do wonder what Apple’s next act will be after the iPhone? The iPhone is still responsible for about 70% of the company’s revenues.

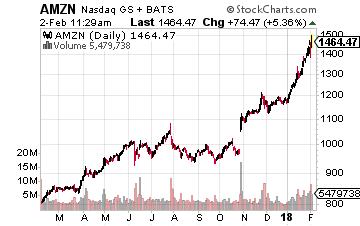

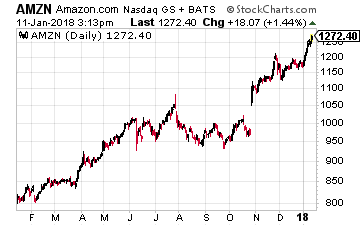

One bright hope was the smart speaker market. After all, Apple’s Siri was the leader in the virtual assistant space. But it has now taken a back seat to smart speaker products from both Google (Home) and, of course, Amazon.com (Nasdaq: AMZN)and Alexa. Amazon’s Echo speaker was launched in 2014 while we still wait for Apple’s entry.

One bright hope was the smart speaker market. After all, Apple’s Siri was the leader in the virtual assistant space. But it has now taken a back seat to smart speaker products from both Google (Home) and, of course, Amazon.com (Nasdaq: AMZN)and Alexa. Amazon’s Echo speaker was launched in 2014 while we still wait for Apple’s entry.

Apple’s HomePod smart speaker will finally be launched on February 9, after missing the Christmas selling season. But unlike the debut of the iPhoneX, Apple Watch Series3 or AirPods, pre-orders for the HomePod have not sold out ahead of the launch date.

That is likely due to the relatively high price tag (again). The HomePod will sell for $349 while you can get a speaker from Amazon for $50 to $150. This market will be extremely important long-term as the hub in many people’s homes. Canalys Research forecast that sales for smart speakers will soar by 70% in 2018 to 56.3 million. In other words, it is the biggest consumer electronics products since the smartphone.

Performance will matter when it comes to the virtual assistants in our homes.

Tests comparing Alexa to Siri to Google Home’s assistant have shown Google the winner in general knowledge with Siri performing the worst. And when it comes to shopping, Alexa was tops with the HomePod again bringing up the rear. The only areas where the HomePod came out on top was in regard to privacy and music.

Apple’s Future

Another growing negative for Apple is that sentiment toward the company has shifted, albeit slightly so far. The whole incident regarding the company intentionally slowing down its older devices was handled very poorly. So poorly in fact that now Apple faces a wave of class-action lawsuits as well as regulatory inquiries from both the Department of Justice and the Securities and Exchange Commission.

Money-wise, the investigations will be nothing Apple can’t handle. But the danger is there of a major sentiment shift against Apple from both the public at large and the investment community.

If sentiment further shifts, you may see Apple’s stock continuing to underperform the general market.

For me, that turns the race between the stocks of Apple and Amazon into a very real one. Already, Amazon is within $190 billion and closing very rapidly. . .the gap at the end of 2017 was $326 billion. And I expect to close further in 2018, unless Apple begins to innovate again, justifying the premium pricing on its products.

Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

Source: Investors Alley

Based on the recent earnings call from United Continental Holdings (NYSE: UAL), it looks like another airfare price war is just around the corner.

Based on the recent earnings call from United Continental Holdings (NYSE: UAL), it looks like another airfare price war is just around the corner. Apple (Nasdaq: AAPL) garnered a lot of headlines recently when it said it would make a one-off $38 billion tax payment on the repatriation of some of its overseas profits. That led to speculation by the Trump Administration and others about how other technology companies would follow Apple’s lead.

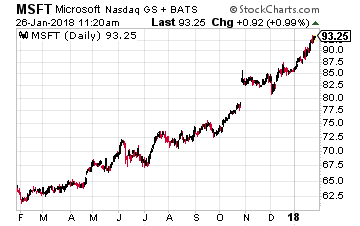

Apple (Nasdaq: AAPL) garnered a lot of headlines recently when it said it would make a one-off $38 billion tax payment on the repatriation of some of its overseas profits. That led to speculation by the Trump Administration and others about how other technology companies would follow Apple’s lead. One prime example is Microsoft (Nasdaq: MSFT). In early December, its stock was down to $81 over worries about the tax bill. Now it is over $92 a share and still climbing. There are lots of reasons why, but I’m sure Wall Street has by now realized the new tax law won’t hurt Microsoft. Again, never make an investment decision solely on something like taxes.

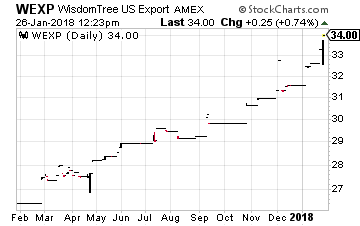

One prime example is Microsoft (Nasdaq: MSFT). In early December, its stock was down to $81 over worries about the tax bill. Now it is over $92 a share and still climbing. There are lots of reasons why, but I’m sure Wall Street has by now realized the new tax law won’t hurt Microsoft. Again, never make an investment decision solely on something like taxes. One other investment for you to consider is the WisdomTree U.S. Export and Multinational Fund (NYSE: WEXP). It is filled with blue-chip U.S. multinationals such as Microsoft, Boeing, Johnson & Johnson, Apple and Alphabet.

One other investment for you to consider is the WisdomTree U.S. Export and Multinational Fund (NYSE: WEXP). It is filled with blue-chip U.S. multinationals such as Microsoft, Boeing, Johnson & Johnson, Apple and Alphabet.

Tied for second on the list are Mastercard (NYSE: MA) and International Business Machines (NYSE: IBM). The latter was one of the very first big companies to see the promise of blockchain, contributing code to an open-source effort and encouraging start-ups to try the technology on its cloud for free. What really caught my eye regarding IBM’s blockchain efforts was a recent announcement.

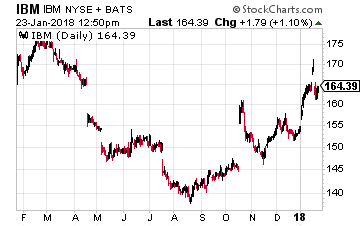

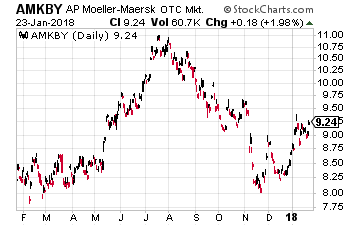

Tied for second on the list are Mastercard (NYSE: MA) and International Business Machines (NYSE: IBM). The latter was one of the very first big companies to see the promise of blockchain, contributing code to an open-source effort and encouraging start-ups to try the technology on its cloud for free. What really caught my eye regarding IBM’s blockchain efforts was a recent announcement. The words supply chain bring me to what I consider to be a major announcement last week from IBM and the world’s largest shipping company, AP Moller Maersk A/S (OTC: AMKBY). The two firms are setting up a joint venture to use blockchain technology in order to help make the companies’ supply chains more efficient.

The words supply chain bring me to what I consider to be a major announcement last week from IBM and the world’s largest shipping company, AP Moller Maersk A/S (OTC: AMKBY). The two firms are setting up a joint venture to use blockchain technology in order to help make the companies’ supply chains more efficient.

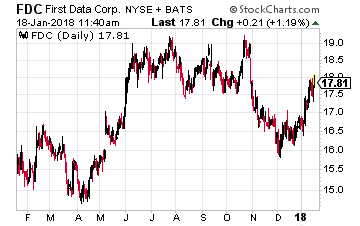

First Data (NYSE: FDC) provides merchant transaction processing; credit, debit and retail card issuing and processing; prepaid services and check verification and other similar services.

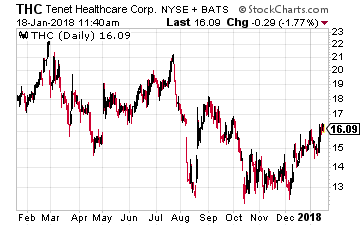

First Data (NYSE: FDC) provides merchant transaction processing; credit, debit and retail card issuing and processing; prepaid services and check verification and other similar services. Tenet Healthcare (NYSE: THC) owns and operates hospitals and other healthcare facilities. It is one of the largest investor-owned healthcare delivery systems in the United States.

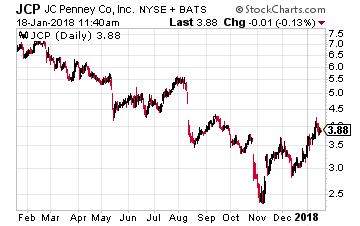

Tenet Healthcare (NYSE: THC) owns and operates hospitals and other healthcare facilities. It is one of the largest investor-owned healthcare delivery systems in the United States. JC Penney (NYSE: JCP) is a well-known department store chain with still 875 stores across the U.S. It is almost a poster child for being Amazoned. Adding to all the woes it faces on the competitive front is its heavy debt burden in excess of $4 billion.

JC Penney (NYSE: JCP) is a well-known department store chain with still 875 stores across the U.S. It is almost a poster child for being Amazoned. Adding to all the woes it faces on the competitive front is its heavy debt burden in excess of $4 billion.

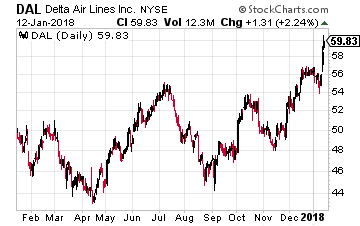

Take Delta Air Lines (NYSE: DAL), for example. Just last week it said that the tax cut will boost its earnings by about $800 million a year. That translates to about $1 per share in increased earnings for 2018. Delta management raised their earnings per share guidance for 2018 to a range of $6.35 to $6.70, up 20% to 30% from the year earlier level.

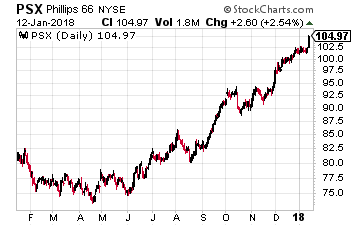

Take Delta Air Lines (NYSE: DAL), for example. Just last week it said that the tax cut will boost its earnings by about $800 million a year. That translates to about $1 per share in increased earnings for 2018. Delta management raised their earnings per share guidance for 2018 to a range of $6.35 to $6.70, up 20% to 30% from the year earlier level. And it’s not just the big oil firms to benefit. The oil refining segment should really get a major boost. The largest company in the segment, by market capitalization, Phillips 66 (NYSE: PSX), will receive a 16% boost to 2018 earnings according to an estimate from Piper Jaffray’s Simmons & Company energy investment bank unit.

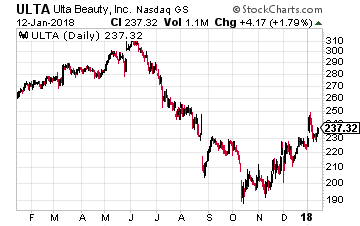

And it’s not just the big oil firms to benefit. The oil refining segment should really get a major boost. The largest company in the segment, by market capitalization, Phillips 66 (NYSE: PSX), will receive a 16% boost to 2018 earnings according to an estimate from Piper Jaffray’s Simmons & Company energy investment bank unit. One of my favorites in the sector is Ulta Beauty (Nasdaq: ULTA), which operates 1,058 stores and generated $4.8 billion in revenues in 2016. It should get a double boost – not only from the tax cut itself, but from consumers with a little extra in their pocket spending on simple luxuries like makeup, lip gloss, etc. Perhaps that’s why the stock is already up over 6% year-to-date.

One of my favorites in the sector is Ulta Beauty (Nasdaq: ULTA), which operates 1,058 stores and generated $4.8 billion in revenues in 2016. It should get a double boost – not only from the tax cut itself, but from consumers with a little extra in their pocket spending on simple luxuries like makeup, lip gloss, etc. Perhaps that’s why the stock is already up over 6% year-to-date.

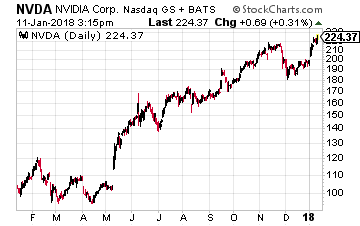

Let me start by talking about a company that was unavoidable at this year’s CES – Nvidia (Nasdaq: NVDA). Their graphics processing units (GPUs) are at the core of many machine learning and artificial intelligence solutions, including for automobiles.

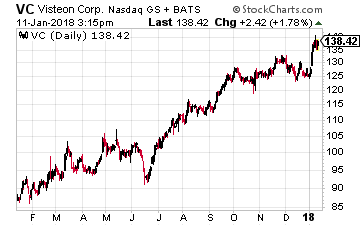

Let me start by talking about a company that was unavoidable at this year’s CES – Nvidia (Nasdaq: NVDA). Their graphics processing units (GPUs) are at the core of many machine learning and artificial intelligence solutions, including for automobiles. A company to consider is Visteon (NYSE: VC), which designs and manufactures electronics products for automakers. Visteon provides everything from standard gauges to high resolution, reconfigurable digital 2D and 3D displays to infotainment and audio systems.

A company to consider is Visteon (NYSE: VC), which designs and manufactures electronics products for automakers. Visteon provides everything from standard gauges to high resolution, reconfigurable digital 2D and 3D displays to infotainment and audio systems.

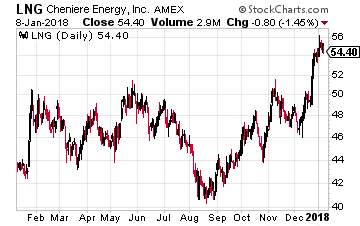

Primary among U.S. LNG exporters is Cheniere Energy (NYSE: LNG), which is the owner of the first LNG export terminal in the U.S. that has been operating since early 2016. It is exporting at its Sabine Pass facility with three trains and a capacity of about two billion cubic feet of gas per day. Its total capacity is expected to be about five billion cubic feet per day once all five trains are completed (the fourth train was recently completed). An LNG train is a liquified natural gas plant’s liquefaction and purification facility.

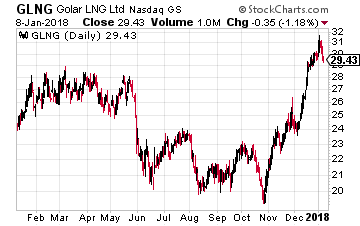

Primary among U.S. LNG exporters is Cheniere Energy (NYSE: LNG), which is the owner of the first LNG export terminal in the U.S. that has been operating since early 2016. It is exporting at its Sabine Pass facility with three trains and a capacity of about two billion cubic feet of gas per day. Its total capacity is expected to be about five billion cubic feet per day once all five trains are completed (the fourth train was recently completed). An LNG train is a liquified natural gas plant’s liquefaction and purification facility. Golar LNG (Nasdaq: GLNG) – its stock is up nearly 20% over the past year. The company is one of the world’s largest independent owners and operators of marine-based LNG midstream infrastructure and is involved in the liquefaction, transportation and regasification of natural gas.

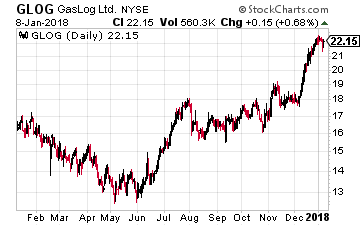

Golar LNG (Nasdaq: GLNG) – its stock is up nearly 20% over the past year. The company is one of the world’s largest independent owners and operators of marine-based LNG midstream infrastructure and is involved in the liquefaction, transportation and regasification of natural gas. If you are looking at more of a pure-play LNG shipper, there is Gaslog Ltd. (NYSE: GLOG), whose stock is up nearly 30% over the last year, with most that gain occurring in the last three months.

If you are looking at more of a pure-play LNG shipper, there is Gaslog Ltd. (NYSE: GLOG), whose stock is up nearly 30% over the last year, with most that gain occurring in the last three months.

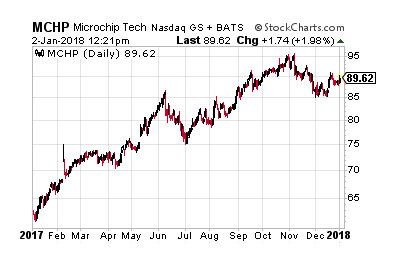

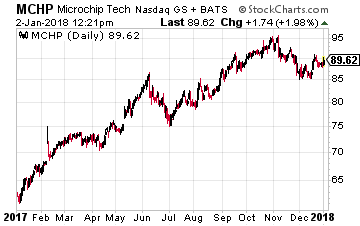

Let me fill you in now on Microchip Technology, whose microcontrollers are likely all through your home – from your garage door opener to your coffee machine to your children’s or grandchildren’s toys.

Let me fill you in now on Microchip Technology, whose microcontrollers are likely all through your home – from your garage door opener to your coffee machine to your children’s or grandchildren’s toys.

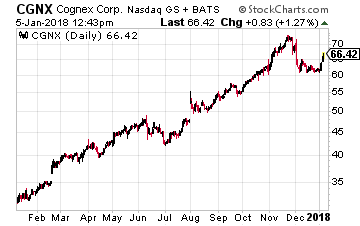

Foremost in this sector is Cognex (Nasdaq: CGNX), which is the leader globally in providing vision systems, vision software, vision sensors and industrial ID readers. It sells its vision systems to most of the big players in the industrial robotics industry including ABB, Yaskawa Electric and Germany’s Kuka AG. The only exception is Fanuc, which makes its own vision systems. This translates to Cognex having a 30% share of the vision systems market.

Foremost in this sector is Cognex (Nasdaq: CGNX), which is the leader globally in providing vision systems, vision software, vision sensors and industrial ID readers. It sells its vision systems to most of the big players in the industrial robotics industry including ABB, Yaskawa Electric and Germany’s Kuka AG. The only exception is Fanuc, which makes its own vision systems. This translates to Cognex having a 30% share of the vision systems market.