The U.S. economy is growing nicely, with any recession at least a few years out in the future. Average wages for working folks are also starting to increase after years of stagnation. Confidence in the economy and more money in their pockets will have people more willing to spend on recreation activities. Now is a good time to consider income stocks backed by consumer discretionary spending, especially for recreation activities.

Real estate investment trusts (REITs) own a wide range of property types lease the many kinds of businesses. It is often financially more efficient for a retail or services business to lease property or buildings rather than own them. REITs typically specialize in a specific property type. This gives them expertise to generate superior returns and often help their tenants be more successful in their own businesses. As noted above, this is a good time to look at REITs with properties used in the recreation and leisure industries.

Here are three specialty REITs focused on gaming and other recreation activities.

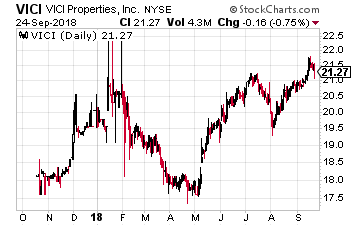

VICI Properties, Inc. (NYSE: VICI) was spun-off by Caesars Entertainment (Nasdaq: CZR) with an October 2017 IPO. The company’s portfolio includes 20 market-leading gaming properties in nine states, including the world-renowned Caesars Palace, and four championship golf courses. The properties are leased to Caesars Entertainment Corporation and operate under leading brands such as Caesars, Horseshoe, Harrah’s and Bally’s.

VICI Properties, Inc. (NYSE: VICI) was spun-off by Caesars Entertainment (Nasdaq: CZR) with an October 2017 IPO. The company’s portfolio includes 20 market-leading gaming properties in nine states, including the world-renowned Caesars Palace, and four championship golf courses. The properties are leased to Caesars Entertainment Corporation and operate under leading brands such as Caesars, Horseshoe, Harrah’s and Bally’s.

Caesars doesn’t not have an ownership position in VICI and there are no Board members common to both companies. With the spin-off, VICI is completely independent. Caesars does provide very strong 3.6 times rent coverage on the properties and contracted capex spending commitments to keep the properties at the forefront of the gaming industry. The REIT is internally managed. For growth VICI has rights of first offer (ROFO) on properties Caesar would want to capitalize through a sale lease back. The REIT can also pursue third party acquisitions.

Two dividends have been paid, with a 9.5% increase between the first and second.

The shares currently yield 4.9%.

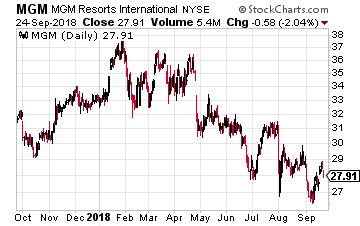

MGM Growth Properties LLC (NYSE: MGP) was spun-off in April 2016 by MGM Resorts International (NYSE: MGM) in April 2016. The REIT currently owns 11 properties leased to and managed by MGM. All the properties are on a single master-lease, which gives the rental payments to MGM Growth Properties the highest level of safety. The lease has built in annual escalators and a profit-sharing component.

MGM Growth Properties LLC (NYSE: MGP) was spun-off in April 2016 by MGM Resorts International (NYSE: MGM) in April 2016. The REIT currently owns 11 properties leased to and managed by MGM. All the properties are on a single master-lease, which gives the rental payments to MGM Growth Properties the highest level of safety. The lease has built in annual escalators and a profit-sharing component.

In contrast to VICI, MGM retains a majority ownership in MGP and pays all the operating expenses of the REIT. MGP also has ROFO on properties owned by MGM. The REIT has already made third party acquisitions.

In its history, MGP has produced steady 10% per year dividend growth.

The shares yield 5.9%.

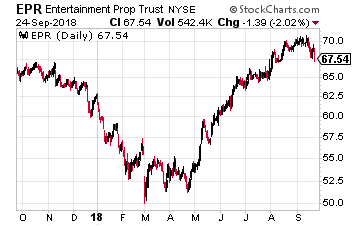

EPR Properties (NYSE: EPR) was founded in 1997 as a pure play owner of movie theater properties. Today the company 169 multiplex theater and family entertainment centers generating $280 million of annual net operating income, 80 golf entertainment complexes, ski areas, and other entertainment attractions producing $182 million of NOI, and 146 charter and private schools generating NOI of $115 million.

EPR Properties (NYSE: EPR) was founded in 1997 as a pure play owner of movie theater properties. Today the company 169 multiplex theater and family entertainment centers generating $280 million of annual net operating income, 80 golf entertainment complexes, ski areas, and other entertainment attractions producing $182 million of NOI, and 146 charter and private schools generating NOI of $115 million.

The EPR management team has great expertise in its focused property areas and helps tenants be as profitable as possible. All properties are leased to tenants on triple-net contracts. The EPR dividend has grown every year since 2010 with a 7% compound annual growth rate.

Dividends are paid monthly, and the yield is 6.1%.

Pay Your Bills for LIFE with These Dividend StocksGet your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.

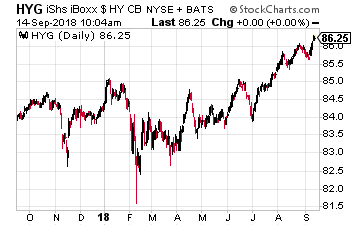

High yield bond funds such as the $16 billion in assets iShares iBoxx $ High Yield Corporate Bond ETF (NYSE: HYG) pay a more attractive current yield, but with added danger to your invested principal. High-yield is the term for non-investment grade bonds. These are also called junk bonds.

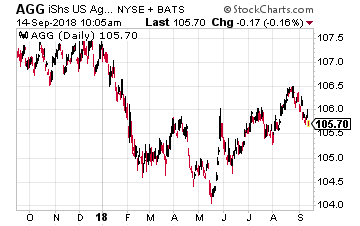

High yield bond funds such as the $16 billion in assets iShares iBoxx $ High Yield Corporate Bond ETF (NYSE: HYG) pay a more attractive current yield, but with added danger to your invested principal. High-yield is the term for non-investment grade bonds. These are also called junk bonds. The iShares Core U.S. Aggregate Bond ETF (NYSE: AGG) is the largest bond ETF with $56 billion in investor money. The fund is touted as a diversified way to cover the full range of investment grade bonds.

The iShares Core U.S. Aggregate Bond ETF (NYSE: AGG) is the largest bond ETF with $56 billion in investor money. The fund is touted as a diversified way to cover the full range of investment grade bonds.

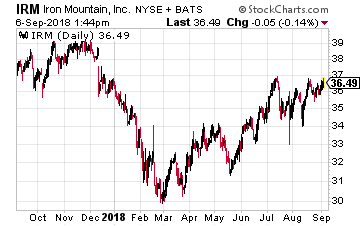

Iron Mountain Inc. (NYSE: IRM) is a niche REIT that provides information and asset storage, records management, data centers, data management and secure shredding services. The company has facilities and provides services in Asia, Europe, Africa and South America as well as in North America.

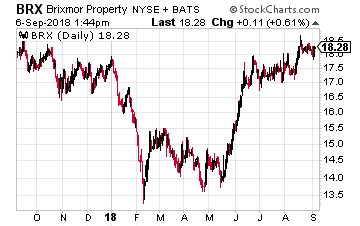

Iron Mountain Inc. (NYSE: IRM) is a niche REIT that provides information and asset storage, records management, data centers, data management and secure shredding services. The company has facilities and provides services in Asia, Europe, Africa and South America as well as in North America. Brixmor Property Group (NYSE: BRX) is an owner and operator of high-quality, open-air shopping centers. The Company’s more than 500 retail centers located primarily located in the eastern one-third of the continental U.S.

Brixmor Property Group (NYSE: BRX) is an owner and operator of high-quality, open-air shopping centers. The Company’s more than 500 retail centers located primarily located in the eastern one-third of the continental U.S. Crown Castle International Corp (NYSE: CCI) owns cell phone towers, which are leased by the various wireless services providers. The company is the nation’s largest provider of shared wireless infrastructure.

Crown Castle International Corp (NYSE: CCI) owns cell phone towers, which are leased by the various wireless services providers. The company is the nation’s largest provider of shared wireless infrastructure. Macerich Co (NYSE: MAC) focuses on the acquisition, leasing, management, development and redevelopment of regional malls throughout the United States. Currently the company owns 48 “market dominant” Class A malls located across the U.S. Macerich has paid a growing dividend for over 20 years.

Macerich Co (NYSE: MAC) focuses on the acquisition, leasing, management, development and redevelopment of regional malls throughout the United States. Currently the company owns 48 “market dominant” Class A malls located across the U.S. Macerich has paid a growing dividend for over 20 years.

National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers.

National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. Physicians Realty Trust (NYSE: DOC) is a healthcare REIT that focuses its portfolio on medical office, physician group practice clinics, outpatient care, ambulatory surgery centers, specialized hospitals, rehabilitation facilities and small specialized long-term acute care hospitals. The company owns 249 properties located in 30 states. Ninety-two percent of the holdings are medical office buildings. Even through tough economic times, the healthcare sector will still need its offices and care facilities.

Physicians Realty Trust (NYSE: DOC) is a healthcare REIT that focuses its portfolio on medical office, physician group practice clinics, outpatient care, ambulatory surgery centers, specialized hospitals, rehabilitation facilities and small specialized long-term acute care hospitals. The company owns 249 properties located in 30 states. Ninety-two percent of the holdings are medical office buildings. Even through tough economic times, the healthcare sector will still need its offices and care facilities.

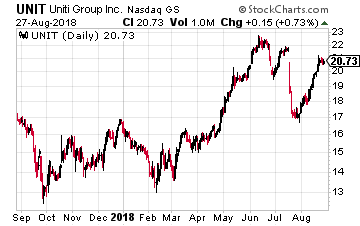

Uniti Group Inc. (Nasdaq: UNIT) is a real estate investment trust (REIT) that owns telecommunications network assets. The company was spun-off by Windstream (Nasdaq: WIN) in 2015 to own a large portion of WIN’s fiber and copper wireline network.

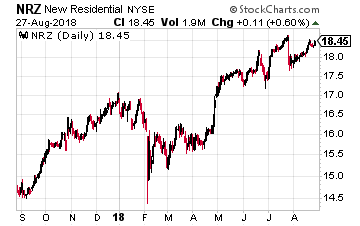

Uniti Group Inc. (Nasdaq: UNIT) is a real estate investment trust (REIT) that owns telecommunications network assets. The company was spun-off by Windstream (Nasdaq: WIN) in 2015 to own a large portion of WIN’s fiber and copper wireline network. New Residential Investment Corp. (NYSE: NRZ) is a finance REIT that owns a diversified portfolio of residential mortgage related assets. This has been one of the great high-yield investments of the last five years.

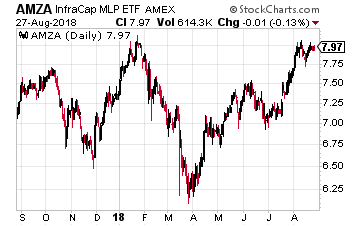

New Residential Investment Corp. (NYSE: NRZ) is a finance REIT that owns a diversified portfolio of residential mortgage related assets. This has been one of the great high-yield investments of the last five years. The InfraCap MLP ETF (NYSE: AMZA) is an exchange traded fund (ETF) that owns an actively managed portfolio of master limited partnerships (MLPs). The MLP sector is comprised of publicly traded partnerships that provide energy infrastructure services such as pipeline, storage terminals, export facilities and processing services.

The InfraCap MLP ETF (NYSE: AMZA) is an exchange traded fund (ETF) that owns an actively managed portfolio of master limited partnerships (MLPs). The MLP sector is comprised of publicly traded partnerships that provide energy infrastructure services such as pipeline, storage terminals, export facilities and processing services.

The Walt Disney Company (NYSE: DIS) has a historic yield range of 0.8% to 1.6%. The current yield is 1.5%, which under the IQ Trends system is a strong indicator that DIS is undervalued and should move higher from here.

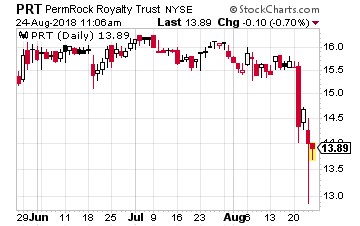

The Walt Disney Company (NYSE: DIS) has a historic yield range of 0.8% to 1.6%. The current yield is 1.5%, which under the IQ Trends system is a strong indicator that DIS is undervalued and should move higher from here. PermRock Royalty Trust (NYSE: PRT) is a new investment I revealed to the presentation attendees. This is not a company, but instead the trust has a right to 75% of the net income from crude oil production from dedicated acreage in the Permian Basin.

PermRock Royalty Trust (NYSE: PRT) is a new investment I revealed to the presentation attendees. This is not a company, but instead the trust has a right to 75% of the net income from crude oil production from dedicated acreage in the Permian Basin.

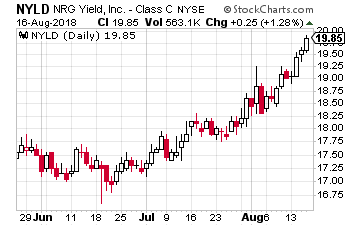

NRG Yield Inc. (NYSE: NYLD) owns a nationally diverse portfolio of conventional, solar, thermal, wind, and natural gas electricity production assets. The company was spun out in 2012 by NRG Energy (NYSE: NRG), a regulated electric utility company. Renewable energy assets developed by NRG were sold to NYLD to support the growth of NYLD.

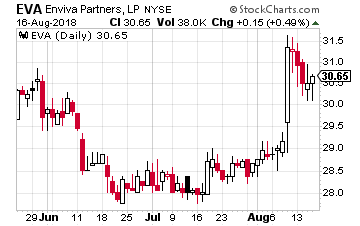

NRG Yield Inc. (NYSE: NYLD) owns a nationally diverse portfolio of conventional, solar, thermal, wind, and natural gas electricity production assets. The company was spun out in 2012 by NRG Energy (NYSE: NRG), a regulated electric utility company. Renewable energy assets developed by NRG were sold to NYLD to support the growth of NYLD. Enviva Partners, LP (NYSE: EVA) is a publicly traded master limited partnership (MLP) that takes a different type of natural resource, wood fiber, and processes it into a transportable form, wood pellets. The pellets are sold on long term contracts to companies in the UK and Europe where they are burned to produce electricity.

Enviva Partners, LP (NYSE: EVA) is a publicly traded master limited partnership (MLP) that takes a different type of natural resource, wood fiber, and processes it into a transportable form, wood pellets. The pellets are sold on long term contracts to companies in the UK and Europe where they are burned to produce electricity.

Starwood Property Trust, Inc. (NYSE: STWD) is one of the largest commercial lenders of any business type – including banks. The company currently has a $12.6 billion loan portfolio with a 62% loan to value. Since launching in 2009 the company has put out almost $40 billion in loans and investments with zero realized losses.

Starwood Property Trust, Inc. (NYSE: STWD) is one of the largest commercial lenders of any business type – including banks. The company currently has a $12.6 billion loan portfolio with a 62% loan to value. Since launching in 2009 the company has put out almost $40 billion in loans and investments with zero realized losses. Ladder Capital Corp (NYSE: LADR) uses a three-prong approach to its investment portfolio. The three legs are commercial mortgage loans, which account for 75% of the company’s capital allocation; commercial real estate equity investments for 12%; and commercial MBS bonds accounting for 8%. The business plan is that the three groups shift as more or less attractive through the commercial real estate cycle. Leverage is a comfortable 2.7 times equity. Since it paid its first dividend for Q1 2015, Ladder has steadily increased the quarterly payout at an average 8% annual growth rate.

Ladder Capital Corp (NYSE: LADR) uses a three-prong approach to its investment portfolio. The three legs are commercial mortgage loans, which account for 75% of the company’s capital allocation; commercial real estate equity investments for 12%; and commercial MBS bonds accounting for 8%. The business plan is that the three groups shift as more or less attractive through the commercial real estate cycle. Leverage is a comfortable 2.7 times equity. Since it paid its first dividend for Q1 2015, Ladder has steadily increased the quarterly payout at an average 8% annual growth rate. Blackstone Mortgage Trust, Inc. (NYSE: BXMT) is a pure commercial mortgage lender. The REIT receives high quality mortgage lending leads from its sponsor, The Blackstone Group L.P. (NYSE: BX).

Blackstone Mortgage Trust, Inc. (NYSE: BXMT) is a pure commercial mortgage lender. The REIT receives high quality mortgage lending leads from its sponsor, The Blackstone Group L.P. (NYSE: BX).

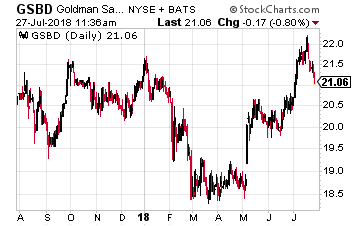

Goldman Sachs BDC, Inc. (NYSE: GSBD) is a newer BDC managed by the famed investment bank. The company launched with a March 2015 IPO. The dividend has been level at $0.45 per share since the IPO.

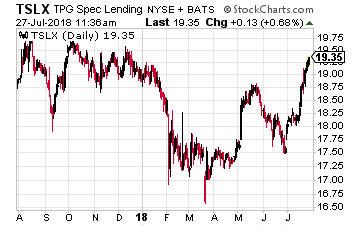

Goldman Sachs BDC, Inc. (NYSE: GSBD) is a newer BDC managed by the famed investment bank. The company launched with a March 2015 IPO. The dividend has been level at $0.45 per share since the IPO. TPG Specialty Lending (NYSE: TSLX) has been a publicly traded since March 2014. The BDC is managed by private asset manager TGP, which has $80 billion under management. The management team has demonstrated excellent discipline in its approach to making portfolio loans. As a result, the company has shown slow but steady NAV appreciation.

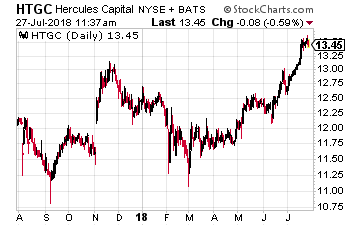

TPG Specialty Lending (NYSE: TSLX) has been a publicly traded since March 2014. The BDC is managed by private asset manager TGP, which has $80 billion under management. The management team has demonstrated excellent discipline in its approach to making portfolio loans. As a result, the company has shown slow but steady NAV appreciation. Hercules Capital (Nasdaq: HTGC) is an internally managed BDC exclusively focused on making loans and equity investments in the venture capital space.

Hercules Capital (Nasdaq: HTGC) is an internally managed BDC exclusively focused on making loans and equity investments in the venture capital space.