A game-changing story about stocks just broke—and you almost certainly missed it.

That’s why I’m writing about this surprising news today: because it’s just what you need to know if you’re struggling with how to approach this interest rate–obsessed market, especially in the wake of the recent pullback.

Why haven’t you heard it?

Because good news like this doesn’t grab as much attention as Chicken Little panic articles, so the financial press skips it. But what I’m about to tell you is crucial to your financial well-being—and something I’ve been saying on Contrarian Outlook and in our CEF Insider service for months now.

Luckily, not everyone is ignoring the story. Bloomberg Businessweek just wrote an in-depth analysis of this piece of news, which is simply this: fears of a recession are way overblown, and the market is set for strong gains in the months ahead.

(In a moment, I’ll reveal a fund set to roll higher as the market surprises the doomsayers and takes off. Best of all, this ignored fund pays a safe 6.9% dividend.)

I was glad to read this upbeat news, because it echoes a piece I wrote over a year ago. The theme of that article was simple: there are several clear recession indicators and none of them have been in the danger zone for a while. Fast-forward to today and they still aren’t—and aren’t likely to be for a long time.

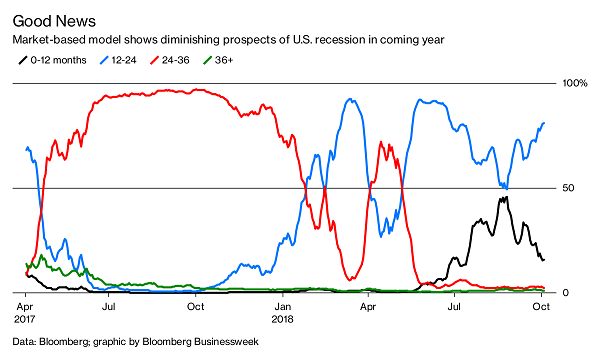

First, let’s take a look at the data Bloomberg compiled; as you can see, the chances of a recession happening in the next 0 to 12 months have nosedived:

Doomsday Predictions Turn Sunny

Also note that chances of a recession happening in the next two to three years have also plummeted, bringing all readings except for the 12- to 24-month one to at or near their lowest levels in the last couple years.

Taking this at face value, it seems the chances of a recession happening soon are diminishing.

But let’s dig a little deeper. What exactly is the data being charted by these lines? Bloomberg’s recession predictor blends a lot of information, but the factor that has caused the red and black lines above to fall steeply is US Treasuries.

The Yield-Curve Horror

A couple weeks ago, I took a close look at the “yield-curve panic” that has been facing markets in 2018. If you were paying attention in February and March, when the markets sold off, you’ll remember that the bears couldn’t stop talking about the flattening yield curve—specifically, the difference between 2-year and 10-year Treasury yields.

When this yield curve inverts (or when 2-year yields are higher than 10-year yields), a recession tends to follow in the next 12 months. And that curve has gotten flatter throughout 2018—up until my article a couple weeks ago, which said that “An inverted yield … isn’t coming yet.”

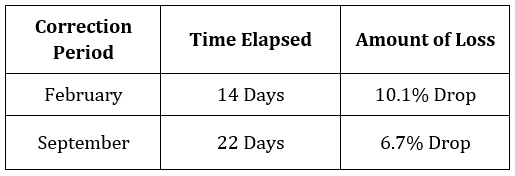

Recession Indicator Pulls a 180

Notice how this isn’t the first time that downward trend suddenly saw a reversal. The same thing happened in February.

But this time is different.

Back then, the widening yield curve happened during a sharp, sudden decline in stocks; and while stocks have had a rough few days, the decline we’ve seen (as I write, we’re just 6.7% down from the all-time high the S&P 500 set on September 20) is still well below the 10.1% plunge we saw in February. What’s more, compared to February, the current market downturn has lasted longer and been much less severe:

To call this the start of a bear market is just silly. What we are seeing over the longer term is a new trend: higher stock prices happening alongside a steeper yield curve.

This is a really good pattern to see.

Steep yield curves indicate higher expectations for inflation and, more crucially, economic growth. Just as negative yield curves are the market saying a recession is going to come, a positive yield curve is the market saying growth is going to get faster.

And what benefits when the economy is growing faster? Stocks.

A 6.9% Dividend From Your Favorite Blue Chips

So what should you buy?

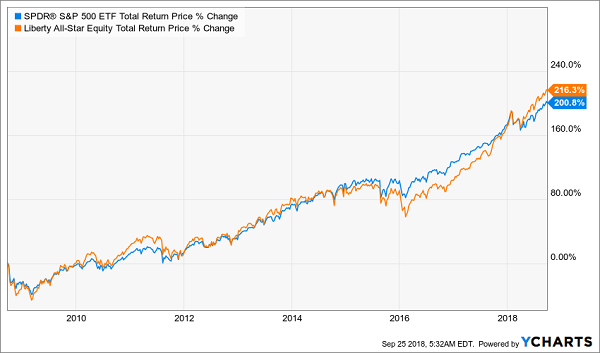

An index fund like the S&P 500 SPDR ETF (SPY) would get you exposure to the stocks that will win in such a market, but you can compound your gains and get a higher total return by buying an equity fund that’s trading at a large discount to its portfolio value, or NAV.

While ETFs almost never trade below their NAVs, closed-end funds (CEFs) do—and that unusual inefficiency in CEFs is an opportunity for contrarian investors to get high-quality stocks at a discount.

For example, the Dividend and Income Fund (DNI) has a 7.2% dividend yield while also holding high-quality stocks like Apple (AAPL), CVS Health (CVS) and AutoZone (AZO), but it trades at an almost unthinkable 24.8% discount to NAV, meaning $1 of those shares is up for sale with DNI for just 75.2 cents.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Source: Contrarian Outlook

The Morgan Stanley Cushing MLP High Income Index ETN (NYSE: MLPY) tracks the performance of an index composed of higher-yielding publicly traded midstream energy infrastructure companies, including master limited partnerships (MLPs) and non-MLP energy midstream corporations.

The Morgan Stanley Cushing MLP High Income Index ETN (NYSE: MLPY) tracks the performance of an index composed of higher-yielding publicly traded midstream energy infrastructure companies, including master limited partnerships (MLPs) and non-MLP energy midstream corporations.

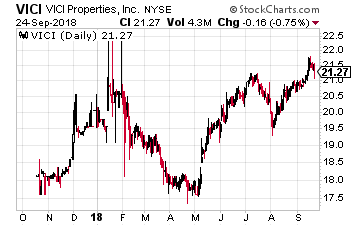

VICI Properties, Inc. (NYSE: VICI) was spun-off by Caesars Entertainment (Nasdaq: CZR) with an October 2017 IPO. The company’s portfolio includes 20 market-leading gaming properties in nine states, including the world-renowned Caesars Palace, and four championship golf courses. The properties are leased to Caesars Entertainment Corporation and operate under leading brands such as Caesars, Horseshoe, Harrah’s and Bally’s.

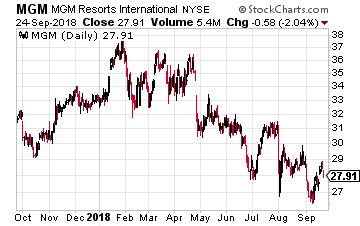

VICI Properties, Inc. (NYSE: VICI) was spun-off by Caesars Entertainment (Nasdaq: CZR) with an October 2017 IPO. The company’s portfolio includes 20 market-leading gaming properties in nine states, including the world-renowned Caesars Palace, and four championship golf courses. The properties are leased to Caesars Entertainment Corporation and operate under leading brands such as Caesars, Horseshoe, Harrah’s and Bally’s. MGM Growth Properties LLC (NYSE: MGP) was spun-off in April 2016 by MGM Resorts International (NYSE: MGM) in April 2016. The REIT currently owns 11 properties leased to and managed by MGM. All the properties are on a single master-lease, which gives the rental payments to MGM Growth Properties the highest level of safety. The lease has built in annual escalators and a profit-sharing component.

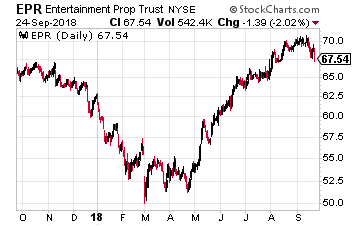

MGM Growth Properties LLC (NYSE: MGP) was spun-off in April 2016 by MGM Resorts International (NYSE: MGM) in April 2016. The REIT currently owns 11 properties leased to and managed by MGM. All the properties are on a single master-lease, which gives the rental payments to MGM Growth Properties the highest level of safety. The lease has built in annual escalators and a profit-sharing component. EPR Properties (NYSE: EPR) was founded in 1997 as a pure play owner of movie theater properties. Today the company 169 multiplex theater and family entertainment centers generating $280 million of annual net operating income, 80 golf entertainment complexes, ski areas, and other entertainment attractions producing $182 million of NOI, and 146 charter and private schools generating NOI of $115 million.

EPR Properties (NYSE: EPR) was founded in 1997 as a pure play owner of movie theater properties. Today the company 169 multiplex theater and family entertainment centers generating $280 million of annual net operating income, 80 golf entertainment complexes, ski areas, and other entertainment attractions producing $182 million of NOI, and 146 charter and private schools generating NOI of $115 million.

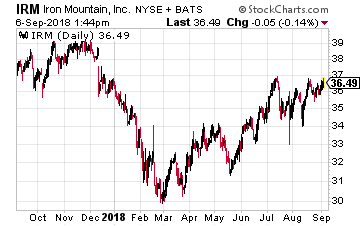

Iron Mountain Inc. (NYSE: IRM) is a niche REIT that provides information and asset storage, records management, data centers, data management and secure shredding services. The company has facilities and provides services in Asia, Europe, Africa and South America as well as in North America.

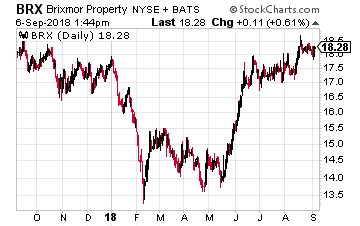

Iron Mountain Inc. (NYSE: IRM) is a niche REIT that provides information and asset storage, records management, data centers, data management and secure shredding services. The company has facilities and provides services in Asia, Europe, Africa and South America as well as in North America. Brixmor Property Group (NYSE: BRX) is an owner and operator of high-quality, open-air shopping centers. The Company’s more than 500 retail centers located primarily located in the eastern one-third of the continental U.S.

Brixmor Property Group (NYSE: BRX) is an owner and operator of high-quality, open-air shopping centers. The Company’s more than 500 retail centers located primarily located in the eastern one-third of the continental U.S. Crown Castle International Corp (NYSE: CCI) owns cell phone towers, which are leased by the various wireless services providers. The company is the nation’s largest provider of shared wireless infrastructure.

Crown Castle International Corp (NYSE: CCI) owns cell phone towers, which are leased by the various wireless services providers. The company is the nation’s largest provider of shared wireless infrastructure. Macerich Co (NYSE: MAC) focuses on the acquisition, leasing, management, development and redevelopment of regional malls throughout the United States. Currently the company owns 48 “market dominant” Class A malls located across the U.S. Macerich has paid a growing dividend for over 20 years.

Macerich Co (NYSE: MAC) focuses on the acquisition, leasing, management, development and redevelopment of regional malls throughout the United States. Currently the company owns 48 “market dominant” Class A malls located across the U.S. Macerich has paid a growing dividend for over 20 years.