More disruption is headed to the healthcare industry, challenging the power of the incumbents in the sector. I’ve already told you about the recently announced effort by JPMorgan, Warren Buffett’s Berkshire Hathaway and Amazon.com (Nasdaq: AMZN) to get into the healthcare space. Their aim is to create a not-for-profit healthcare company to try to lower the cost of healthcare for their collective one million employees.

Now, it seems that Apple (Nasdaq: AAPL) is also getting serious about its push into healthcare. The hint about Apple’s seriousness came at a keynote speech by CEO Tim Cook in September 2017 when he said the sector is one where Apple can have a “meaningful impact”.

At the recent shareholders meeting, Cook again was critical of the healthcare system in the United States. He said it “doesn’t always motivate the best innovative products”. Healthcare companies are designed based on reimbursements rather than the patients’ best interests, he said.

Apple Seizing the Opportunity

Cook said that Apple sees healthcare and wellness as a core part of its app, services and wearables strategy. Cook added that the healthcare market makes the smartphone market look small by comparison. He’s right – with over $7 trillion in healthcare spending annually (about half of that in the U.S.), it’s already about 10% of global GDP.

And think about Apple’s built-in opportunity… the company has over 85 million iPhone users and over one billion Apple devices are actively being used around the globe. That is a number than dwarfs what any health insurer or healthcare provider can boast.

Apple has been slowly building its push into healthcare over the past several years.

Apple’s first foray into the health segment occurred in 2014, with the release of the Health app and HealthKit. Then in March 2015 came the release of ResearchKit and the Apple Watch. Apple has used its HealthKit and ResearchKit software and data platforms to connect users’ health information across third-party apps and into clinical research projects.

The move by Apple into health accelerated in 2016 with the purchase of the digital health company Gliimpse, along with some health-related hires such as experts in remote health monitoring. In 2017, Apple joined with start-up Health Gorilla to advance its quest to turn the iPhone into a comprehensive repository of users’ electronic health records.

Today, Apple is working with Stanford University on a study to see if the Apple Watch’s sensors can detect heart abnormalities. Apple is also working on a number of other health-related solutions, usually using the Apple Watch, such as non-invasive blood glucose monitoring.

Today, Apple is working with Stanford University on a study to see if the Apple Watch’s sensors can detect heart abnormalities. Apple is also working on a number of other health-related solutions, usually using the Apple Watch, such as non-invasive blood glucose monitoring.

And with an upcoming software update, iPhone owners will be able to download their electronic medical records directly from some US hospitals. In January, Apple announced it was teaming up with 12 major hospital systems, such as John Hopkins, to enable patients to see all of their medical records on their iPhone.

And now Apple is taking an even bolder step…

Last month came word that Apple was preparing to launch a network of medical clinics for its employees and their families. The network is named the AC Wellness Network and is scheduled to launch this spring. On Apple’s website, it is described as an “independent medical practice dedicated to delivering compassionate, effective healthcare to the Apple employee population”.

Apple Partners

This move to open its own medical practice doesn’t mean Apple isn’t willing to work with some of the incumbents in the sector. Here are just several examples:

In November, the company came to an agreement with Aetna (NYSE: AET) to distribute more than 500,000 Apple Watches to its customers in 2018, broadening a pilot program that gave Apple Watches to Aetna employees. The special Watches will be loaded with apps co-developed by the two companies to do things like reminding users when to take their medications.

The goal is to, when the technology is perfected, to give the Watch to all of Aetna’s health-insured population. This Apple strategy strikes me as sharing parallels with Apple’s initial strategy of using carriers to subsidize the cost of the initial iPhone, essentially using the carriers as distribution channels.

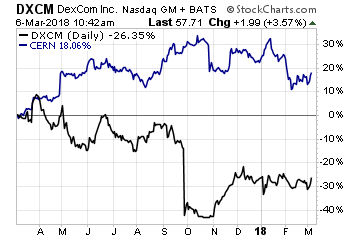

Apple has also teamed up with several medical device makers to create iPhone-enabled devices, including Dexcom (Nasdaq: DXCM) for glucose monitoring and Cochlear (OTC: CHEOY) for hearing aids. As software becomes more and more important for medical device companies going forward, Apple could be positioning itself as an analytics, software, and patient health platform for these companies to plug into rather than having to build these capabilities themselves.

Apple has also teamed up with several medical device makers to create iPhone-enabled devices, including Dexcom (Nasdaq: DXCM) for glucose monitoring and Cochlear (OTC: CHEOY) for hearing aids. As software becomes more and more important for medical device companies going forward, Apple could be positioning itself as an analytics, software, and patient health platform for these companies to plug into rather than having to build these capabilities themselves.

And at this week’s HIMSS18 annual conference, Apple is teaming up with Cerner (Nasdaq: CERN) to showcase to make health care records accessible in the Apple Health app. Cerner will also be offering a look at virtual health solutions that empower individuals to manage their health via telemedicine and remote monitoring technologies as well as intelligent solutions for hospitals as they adjust to rising costs and new technologies.

Brave New Healthcare World

The bottom line for you is that technology is finally changing healthcare as we know it. The one sector where costs have continued to inflate every year looks to be set for technology to have its deflationary effect.

That means the middlemen companies in the sector – with the fat profits – are going to be going on a ‘diet’. In other words, profits will be squeezed as Apple, Amazon and others move in.

Related: Sell These Healthcare Middlemen About to Get Amazoned

Healthcare could end up being a major part of the services business for Apple in a few years. Bad news for the incumbents, unless they have smart managements like the aforementioned companies and are teaming up with Apple and other technology firms.

All those in the health field now need to remember the old saying, “An Apple a day…”

Get Your Hands on Stocks Growing Revenues (and Stock Prices!) Faster than Google and Apple

I’d like to reveal to you the blue chip stocks – one in particular – that could literally be worth millions of dollars to you over the next decade.

Revenue for one firm in particular is growing faster than that of Google and Apple, the darlings of Wall Street. Investors have watched the stock price shoot up over 100% this past year and we’re just getting started.

You need to get in this stock before April 1st (it’s closer than you think!).

Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

Source: Investors Alley

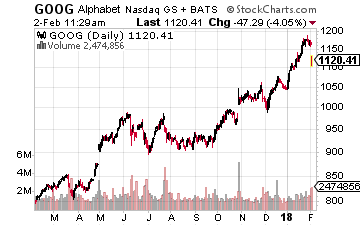

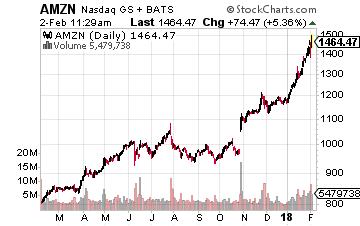

And let’s not forget that there continues to be intensifying competition in the premium smartphone market. Alphabet (Nasdaq: GOOG) officially closed its $1.1 billion deal with HTC Corp., adding more than 2,000 smartphone specialists in Taiwan. This is expected to help Google chase Apple in the increasingly cut-throat premium handset market.

And let’s not forget that there continues to be intensifying competition in the premium smartphone market. Alphabet (Nasdaq: GOOG) officially closed its $1.1 billion deal with HTC Corp., adding more than 2,000 smartphone specialists in Taiwan. This is expected to help Google chase Apple in the increasingly cut-throat premium handset market. One bright hope was the smart speaker market. After all, Apple’s Siri was the leader in the virtual assistant space. But it has now taken a back seat to smart speaker products from both Google (Home) and, of course, Amazon.com (Nasdaq: AMZN)and Alexa. Amazon’s Echo speaker was launched in 2014 while we still wait for Apple’s entry.

One bright hope was the smart speaker market. After all, Apple’s Siri was the leader in the virtual assistant space. But it has now taken a back seat to smart speaker products from both Google (Home) and, of course, Amazon.com (Nasdaq: AMZN)and Alexa. Amazon’s Echo speaker was launched in 2014 while we still wait for Apple’s entry.

{kind=link}