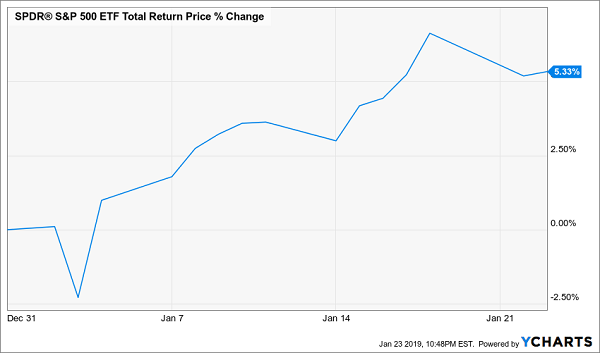

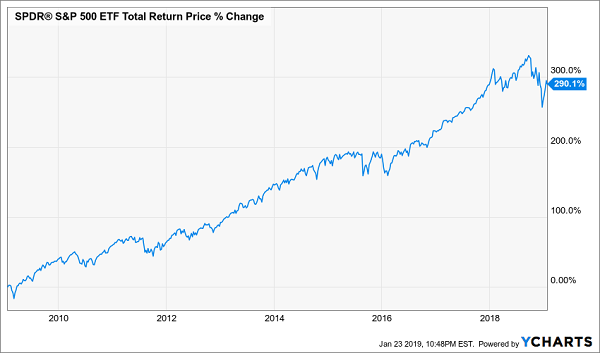

What a run! The S&P 500 is up 5.5% for January, and higher by a hefty 12.7% since hitting a multimonth low in late December. Both are unusually big gains given the limited amount of time stocks have had to dish them out.

The rally, however, has left some stocks vulnerable to a pullback, while the names left out of the marketwide advance have been exposed as perpetually, habitually weak. Both groups are likely to lose ground — or lose more ground — no matter what lies ahead. But should the broad market falter here, these equities could really lose some ground.

With that as the backdrop, here’s a rundown of 10 stocks to sell as soon as possible. They’re either overextended, in unstoppable downtrends or have a history of poor February performances. In no particular order…

Xilinx (XLNX)

Up 62% since the end of 2017, and up 28% this year alone, the momentum that Xilinx(NASDAQ:XLNX) has exhibited is intoxicating. Unfortunately, it probably wasn’t built to last.

XLNX stock jumped 18% last Thursday in response to an incredible third-quarter report. The chipmaker has made the most of the advent of 5G, and said it expects more of the same kind of growth for the foreseeable future. Investors were still buying in on Friday.

As of Monday, though, the sheer weight of the oversized gain and the gap left behind on Thursday are forcing traders to rethink everything about this name and its forward-looking P/E of 28.5. The good news, past and projected, is now priced in, and then some.

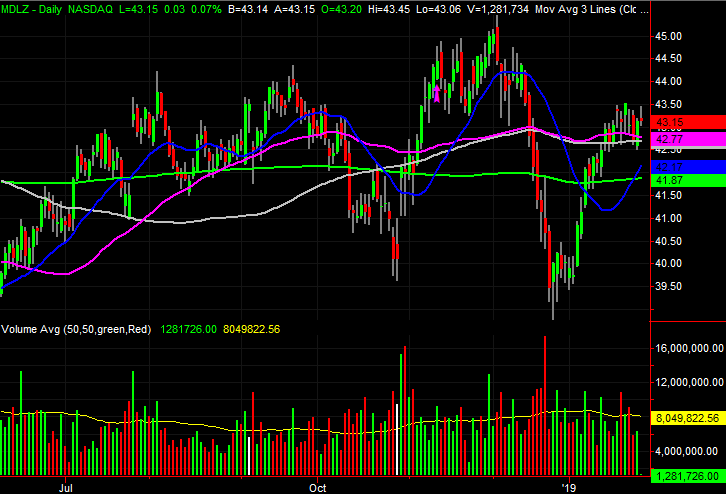

Mondelez International (MDLZ)

Mondelez International (NASDAQ:MDLZ) hasn’t earned a spot in a list of stocks to sell because it’s overextended … quite the opposite actually. Although it has moved higher with the market since late December, it has suspiciously lagged behind. A look back over the course of the past couple of years, in fact, reveals Mondelez remains more likely to make lower highs and lower lows than not.

Investors just don’t see the company overcoming its core problems anytime soon.

Besides, February is rarely a good month for MDLZ stock. On average it loses a percentage point for the month ahead, and even in a good year, shares fall short of breaking even in February.

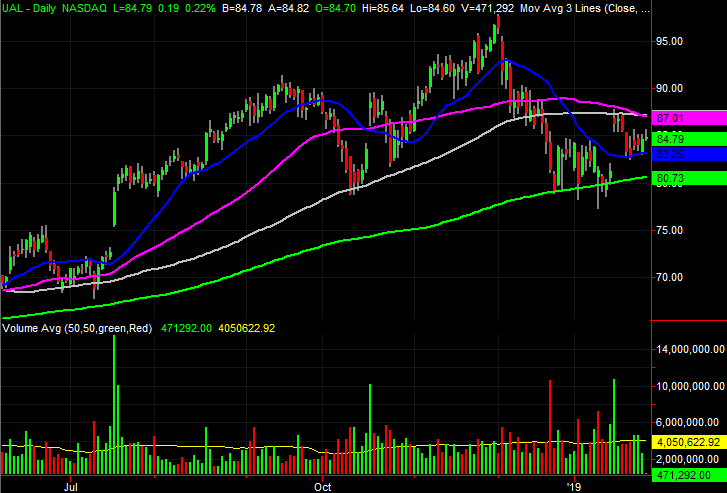

United Continental Holdings (UAL)

United Continental Holdings (NASDAQ:UAL) is another name that, for seasonal reasons, struggles during the second month of the year. On average, UAL stock loses more than 6% in February, and nothing about its performance so far in 2019 suggests the airline stock will be a screaming exception to the norm.

Admittedly, it’s not an outlook that jibes with the recent headlines. Just a few days ago, United Continental capped off an outstanding 2018 with a fourth-quarter earnings and revenue beat.

The headwind isn’t about reality though. It’s about perception. And right now, between an ongoing tariff war, a government shutdown and rebounding oil prices, the market is at least a little worried about the current quarter’s likely results.

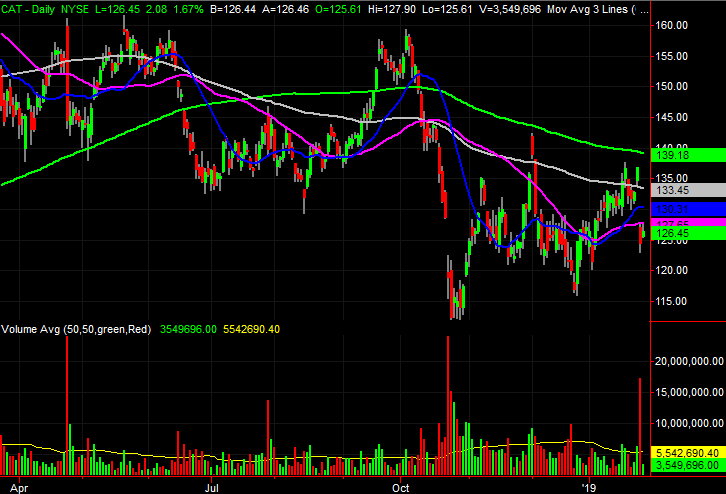

Caterpillar (CAT)

Heavy machinery maker Caterpillar (NYSE:CAT) is in a similar boat. That is, the impact of the trade war with China isn’t exactly taking a massive toll on the company’s bottom line. But, as long as the company is able to say steep tariffs — coming and going — are presenting problems, investors will assume the worst.

And that’s exactly what Caterpillar did with its fourth-quarter report posted on Monday morning. While stopping short of outright blaming it on the war of tariffs and the subsequent economic slowdown in China, the company did concede weakness in China was the cause for the 4% slump in sales for its Asia Pacific arm.

Though CAT stock fell measurably on the report, in the grand scheme of matters, they weren’t terribly shocked. Caterpillar stock is still just trending lower from its early 2018 peak, and there’s little on the radar that might reverse that trend in the coming month.

Exact Sciences (EXAS)

Exact Sciences (NASDAQ:EXAS) has been a champ of late, rallying nearly 60% from its late-December low, and up more than 70% over the course of the past twelve months.

EXAS stock, however, is a name with a history of major ebbs and flows. The big move we’ve seen since Dec. 26 has been made two, and arguably three, times since early 2018, and in each case a huge swath of that gain was given back. It’s unlikely this time will pan out differently. It’s just a habit this cancer diagnostics stock has developed.

Conversely, though due for a sizeable setback soon, the pattern Exact Sciences has developed also says it would be a compelling buy after a tumble.

Alphabet (GOOG, GOOGL)

It’s difficult to bet against the company that essentially owns the gateway to the internet. But, add Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) to your list of stocks to sell before getting too deep into the month of February. On average, GOOGL shares lose a little more than 2% during the second month of the year, and more than half the time it loses ground in February.

It doesn’t appear to be in any major technical trouble right now, but it rarely does in late January.

As was the case with Exact Sciences stock though, any dip from here could be a buying opportunity. GOOGL stock tends to start recovering in March or April to kick off a phenomenal second half of the year.

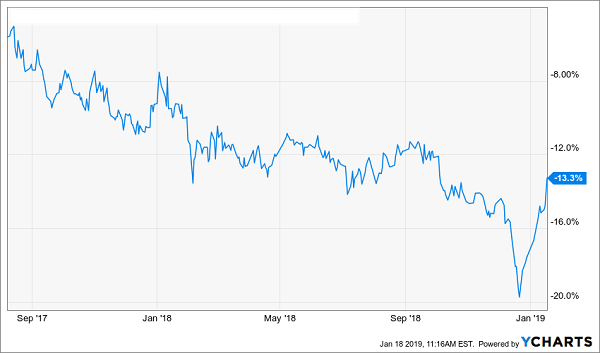

Illumina (ILMN)

Illumina (NASDAQ:ILMN) is another name that’s suspect simply because it has failed to rebound with the rest of the market.

Of course, the doubters had some help coming to their lackluster conclusions. In early January, the company cautioned investors that while its fourth-quarter revenue would be better than expected, 2019’s sales wouldn’t. CEO Francis deSouza was willing to offer 2019 earnings guidance slightly in excess of analysts’ estimates, but for a stock priced at more than 40 times its forward-looking earnings estimates, investors need more assurance the premium they’re paying is justified.

The fiscal outlook might be changed after Tuesday’s post-close report. But, with ILMN stock already below all of its key moving average lines and in a well-framed downtrend, investors are hinting they’re ready to see the glass as half-empty.

Fiserv (FISV)

The knee-jerk reaction to the news that Fiserv (NASDAQ:FISV) would be acquiring First Data(NYSE:FDC) was a decidedly bearish one. Shares fell as much as 8.6% on Jan. 18, with many shareholders convinced the company was overpaying for an asset it didn’t exactly need. Things took a dramatic turn beginning that very day though. The intraday loss was cut in half, and as of Tuesday FISV stock was 22% above the low made on Jan. 18. As it turns out, investors love the prospect of the pairing after all.

Still, the big move is overdone. As of Tuesday, would-be profit-takers are testing the waters, and it’s unlikely the stock’s going any higher until investors get a clear idea of what a combined Fiserv and First Data would look like.

AbbVie (ABBV)

There’s nothing inherently wrong with AbbVie (NYSE:ABBV). Though it missed its fourth-quarter revenue and earnings estimates, it’s still a cash cow that’s expected to grow its top and bottom lines this year. It’s dirt cheap too, valued at only 8 times this year’s expected profits.

Nevertheless, like a handful of the other stocks to sell in the coming month, AbbVie is facing an uphill battle of perception. Most drugmaker stocks are losing ground on fears that new drug-pricing legislation could be forthcoming. Meanwhile, ABBV has developed a strong downtrend of its own since peaking a year ago on worries about the fading patent protection of its blockbuster drug Humira.

Keysight Technologies (KEYS)

Finally, Keysight Technologies (NYSE:KEYS) is one of a handful of stocks to sell for February after an incredible January rally that won’t likely last.

Since its late-December low, KEYS stock has gained more than 28%, mostly thanks to the market’s realization of the company’s role in the rollout of 5G wireless connections. Once Verizon Communications (NYSE:VZ) launched an at-home 5G broadband platform in October, the technology became very real for investors. On the hunt for overlooked names in the business, investors found and fell in love with Keysight.

They arguably overshot though. Since it’s now overbought much like it was a couple of different times last year, a reversion to the mean looks likely.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.

Source: Investor Place