MICHAEL A. ROBINSON

MICHAEL A. ROBINSONI hope you had the chance to catch my recent interview with legendary investor Frank Holmes. We talked about the need for investors to look beyond struggling cryptocurrencies to understand the enormous potential of the blockchain – the technology “underneath” that makes crypto work.

What kind of potential? Well, I believe – conservatively – that the technology could impact some $8 trillion in global transactions

See, the world’s total GDP runs at around $80 trillion a year. And blockchain tech could eventually underpin all of that buying and selling.

But I’m only assuming blockchain grabs a 10% market share of systems that have been archaic and outdated for years now.

Here’s the thing. As amazing as it sounds, trillions of dollars in trade each year still relies on rickety, less-than-totally-secure computer networks and, in some cases, even paper contracts!

Thanks in part to blockchain technology, that’s all about to change. In a big way.

That’s why today, I want to show you four industries where blockchain technology could add security and transparency – and greatly reduce business costs. I think this could boost bottom lines to the tune of $21 billion in 2019 alone – another conservative estimate – for the innovative firms using this technology.

This is the kind of “strategic info” that could make you look smart at your office Christmas party or next family gathering.

Better yet, put it to use wisely, and it could help you pinpoint your next few triple-digit winners – and that’ll be even more fun to share with friends and family.

So check it out…

Why an $8 Trillion Future Is Just the Start

Obviously, my estimate of blockchain’s impact on global business is very bullish; there are some pretty significant sums involved.

So I want to put my estimate of blockchain’s impact in some perspective. Gartner says blockchain tech will create $3.1 trillion in global business value by 2025.

Stunning: Tom Gentile has once again disrupted the financial industry – 15.8 billion calculations per second reveal daily double-your-money trade opportunities. Watch now…

That’s a big number, too, of course, but there’s a problem with it: It understates how quickly this radical new tech platform is going mainstream. Last year, according to Gartner, blockchain value came in at $4 billion – and will rise to $21 billion next year.

That’s a 425% one-year increase – a 77,400% growth rate in just nine years. So my $8 trillion estimate is in line with that, meaning at that growth rate we’ll easily get there by 2030 – and probably sooner.

Now then, most folks think of blockchain in terms of cryptocurrencies like Bitcoin (BTC) and Ethereum (ETH).

And it’s certainly true: All cryptos need access to a blockchain to be mined, distributed, and secured.

And once cryptos like Bitcoin see more widespread adoption, it’s going to send prices soaring to $100,000. That day is going to come sooner than many imagine, because, as I type, computer scientists are working furiously on Bitcoin’s “Lightning Fix.” This fix will essentially allow users to pay for everyday items like coffee or a pizza with Bitcoin.

But blockchain is much bigger than any one cryptocurrency. Its use as a global, secure, distributed ledger for smart contracts is proving irresistible to businesses and individuals alike.

You see, industries across the board can adopt this technology – and they don’t have to rely on any one centralized entity to be a gatekeeper or potential source of vulnerability.

In fact, a key feature of public blockchains is that they are decentralized. Moreover, blockchain can greatly reduce transaction costs and improve cybersecurity. It might shock you to learn that, even in 2018, it can take days for a “conventional” electronic banking transaction to fill and finally settle – that incurs costs and security risks. With blockchain, settlement times could be measured in seconds, not days.

Another benefit of blockchain tech is that, unlike centralized databases, the blockchain serves as not only an up-to-date database, but as a historical one as well. That simply means that all of the information of a given transaction that’s put on a blockchain will remain there, available for scrutiny at any time.

With that in mind, I’ve identified four sectors I believe will benefit greatly from this technology. Call them 2019’s “Blockchain Targets.”

Take a look…

Blockchain Target No. 1: Global Finance and Banking

The $1.45 trillion financial services industry has been an early adopter of blockchain technology, and that will remain so for the foreseeable future.

That’s because at its heart, blockchain tech serves as an excellent means to disentangle the dense layers of centralized bureaucracy, redundant paperwork, and exorbitant fees this sector has come to rely on.

Look at exchanges. Many financial industry players are using blockchain tech to develop auditing systems with almost instant clearing and consensus-based verification, according to a recent report by PricewaterhouseCoopers.

Trade finance is another area that’s ripe for disruption from blockchain technology. As it stands today, the $17 trillion industry is high volume, costly, and time consuming.

Thousands are being shortchanged out of their money

Financial institutions have begun using blockchain technology to reduce their reliance on manual processes and digitizing trade documents like letters of credit to slim costs and increase efficiency.

And major international banks are joining forces to build their blockchain solutions. Firms like BNP Paribas SA (OTC: BNPQY), HSBC Holdings Plc.(NYSE: HSBC), and The Royal Bank of Scotland Group Plc. (NYSE: RBS) are among those leading these efforts.

They’re setting up smart contracts to help track and monitor cross-border transactions, digitally discount receivables, and secure credit risk insurance, among other back-office functions.

Blockchain Target No. 2: the Oil and Gas Industry

About a year ago, a group of the large oil companies – and their banks and trading houses – formed an alliance to launch a blockchain-driven platform for energy commodity training.

The alliance is headed up by firms like BP Plc. (NYSE: BP), Royal Dutch Shell Plc. (NYSE: RDS), and ING Group NV (NYSE: ING).

This Can Happen Day After Day: $2,775 on Monday, $2,575 on Tuesday, $4,350 on Wednesday, $3,125 on Thursday, $2,975 on Friday. Click here to see for yourself…

Together, they have developed a blockchain platform known as Vakt, which will aid the energy industry’s transition from paperwork-driven transactions to smart contracts. That in turn can bring efficiency gains to trading, reduce the risk of errors, and cut back on the amount of time employees spend on paperwork.

Lyon Hardgrave, Vakt’s product development vice president, says that blockchain members will save up to 40% by speeding up processing trades much more quickly and cutting down on data errors.

Now, the platform will not yet be used to trade or settle any transactions – and not a single bit of cryptocurrency will be involved. But it will include deal recaps, confirmations, contracts, logistics, and invoicing.

The global energy market is worth $1.4 trillion, according to Advanced Energy Perspectives. Look for blockchain to save the sector tens of billions of dollars – or more – as it is further rolled out.

Blockchain Target No. 3: Prescription Drugs & Biotechnology

Meanwhile, the $1.2 trillion global drug industry is ripe for blockchain adoption.

To understand blockchain’s role here, you need to know about the Drug Supply Chain Security Act. This legislation outlines a 10-year time frame that will help track, verify, and notify anyone in the supply chain when counterfeit drugs enter the system.

Here again, we’re talking about a highly secure – and immutable – shared ledger of information that would be open to any and all participants.

By using the blockchain, any movement of counterfeit drugs into the system will be immediately flagged. That’s because there will be no record of it going back to the production source.

Oil is failing, but this form of new energy is keeping its promise

“The public availability of the ledger would make it possible to trace every drug product all the way back to the origin of the raw material used to make it,” Tapan Mehta, an executive with DMI, a mobile technology and services company, told IT Healthcare News.

That’s bad news for the purveyors of counterfeit drugs that earn around $200 billion per year.

But it’s great for consumers that will soon be able to stop worrying about the risk of taking what’s known in the industry as substandard, spurious, falsely labeled, falsified, and counterfeit (SSFFC) drugs.

Blockchain Target No. 4: the U.S. Defense Industry

The U.S. military is rolling out its own blockchain system, under the name Pathfinder. This platform will offer far more security, not to mention a permanent record of every single item the Pentagon buys.

Simply put, the military can’t rely on the unsecure public cloud to transmit and store sensitive data. Global hackers, often sponsored by governments in China, Russia, and Iran, are constantly trying to access vital defense department data.

And when it comes to data encryption, nothing beats what blockchain can offer. Which explains why nearly every defense contractor is expected to adopt blockchain over the next several years.

Last July, Boeing Co. (NYSE: BA) said it is working with privately held SparkCognition Inc. to adopt blockchain technology for tracking and allocating flight corridors for drones.

Defense giant Lockheed Martin Corp. (NYSE: LMT) is working with Guardtime Federal LLC to provide blockchain cybersecurity. Lockheed, the nation’s largest defense contractor, counts cyber as a core product.

But civilian branches of the government intend to get in on the action as well. Last June, the $26.3 billion General Services Administration began piloting the federal government’s first blockchain project with vendors Sapient and United Solutions.

Add it all up, and you can see there is enormous potential for blockchain tech – and the firms that develop the products these sectors seek.

Now then, there are no pure blockchain tech plays I can recommend at present. But the companies I’ve just mentioned are hard at work carving out an unbeatable blockchain edge, and I expect bottom lines to fatten accordingly.

That said, there are some firms moving forward aggressively with developing the blockchain itself.

So you can bet I’ll be keeping a close eye on them as we move into 2019. I’m going to have plenty more to say about blockchain technology this year.

Source: Money Morning

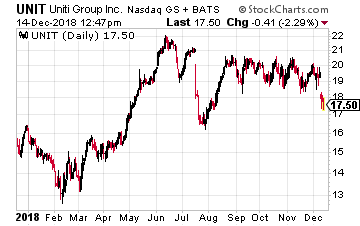

Uniti Group (Nasdaq: UNIT) is a telecommunications REIT focused on fiber optic assets. In recent years the company has focused on acquiring backhaul fiber assets. These are fiber connections between cell towers and the wired Internet.

Uniti Group (Nasdaq: UNIT) is a telecommunications REIT focused on fiber optic assets. In recent years the company has focused on acquiring backhaul fiber assets. These are fiber connections between cell towers and the wired Internet.

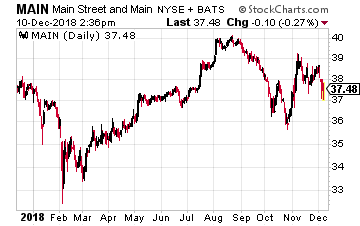

Main Street Capital (NYSE: MAIN) is a monthly dividend paying business development company (BDC). The company has also paid semi-annual, supplemental dividends since 2013. The next supplemental payout lands in investor brokerage accounts on December 27 and is equal to 150% of the normal monthly dividend.

Main Street Capital (NYSE: MAIN) is a monthly dividend paying business development company (BDC). The company has also paid semi-annual, supplemental dividends since 2013. The next supplemental payout lands in investor brokerage accounts on December 27 and is equal to 150% of the normal monthly dividend.