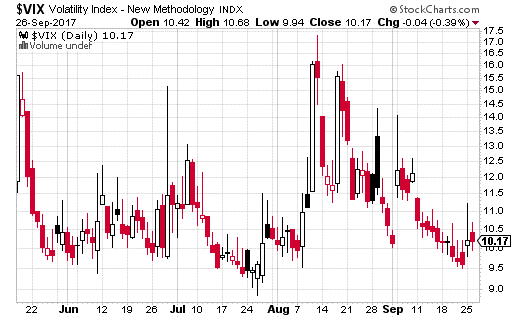

Watching stock market volatility has become quite interesting the last few weeks. I’m not talking about watching the actual day-to-day VIX moves, they’ve mostly been boring. Instead, I’m referring to how the VIX has been moving in relation to what’s going on in the world.

In other words, I find investors’ reaction to major world news items to be… quizzical. There simply doesn’t seem to be a lot going on, well, anywhere, which is cause for concern among stock investors.

At first, it seemed like the nuclear threat from North Korea was going to be a source of higher VIX levels for the foreseeable future. However, traders soon brushed off the harsh rhetoric between the US and North Korea. And, even threat of nuclear war is barely moving the needle in the VIX.

Granted, it could just be that most experts believe the only solution to dealing with North Korea is a diplomatic one. Still, you’d think even the tiniest threat of nuclear annihilation would strike a chord with investors. But fear, it seems, is at a minimum these days.

At least part of the reason volatility remains lower than expected is due to the rampant amount of volatility selling taking place. I’ve mentioned this before, but selling volatility is typically a highly successful strategy. And, it’s become a major source of yield for many traders.

Shorting the VIX is just part of it though. Actual, realized volatility has also been at its lowest levels in recent history. It’s not just the options traders who aren’t concerned – stock buyers (and sellers) are simply not moving the market very much either. It’s been the case for much of 2017.

Still, volatility can become a factor in a hurry. We know from the Financial Crisis of 2008-2009 just how high and fast the VIX can move. It’s never a good idea to totally ignore volatility. There’s nothing wrong with selling it to make money, but be darn sure you’re ready to buy it if things get dicey.

One massive trader is not convinced volatility will remain low the rest of the year. This trader made a massive bet on higher VIX levels back in the summer – and just recently rolled the enormous trade (originally set to expire in October) to December.

The trade itself is a call ratio spread financed with short puts. More specifically, the trader bought the VIX December 15 call versus two of the December 25 calls, while also selling the December 12 put. The trade was executed for a $0.20 debit, but the trader received a $0.20 credit when setting up the original October trade. In other words, this entire spread was basically done for even.

The really interesting part of this trade is just how huge it was in terms of number of contracts. The call spread was 260,000 by 520,000 contracts, with the puts also selling 260,000 times. That’s a crazy amount of options. If you include the closing/rolling of the October spread, there were 2.1 million options traded in this one gigantic trade – the highest in recorded history.

So what’s the trade mean?

Well, the strategy breaks even with the VIX between 12 and 15 on December expiration. It’s a winner from 15 up 35, with peak gains at 25. Finally, it’s a loser under 12 or above 35. Essentially, it’s a huge bet on higher volatility, or a relatively cheap way to hedge a massive stock portfolio. (By the way, peak gains would be about $250 million.)

As always, if you’re interested in betting on higher volatility or hedging your own portfolios with VIX, there are simpler ways to do so. One example is the December VIX 15-20 call spread, which can be bought for $0.75. Breakeven is at $15.75 and you can earn $4.25 max gain if the VIX spikes to 20 or above at December expiration. That’s over a 5 to 1 payout to risk ratio, which makes it a very cheap way to get long volatility if it spikes higher by the end of the year.

[FREE REPORT] Options Income Blueprint: 3 Proven Strategies to Earn More Cash Today Discover how to grab $577 to $2,175 every 7 days even if you have a small brokerage account or little experience... And it's as simple as using these 3 proven trading strategies for earning extra cash. They’re revealed in my new ebook, Options Income Blueprint: 3 Proven Strategies to Earn Extra Cash Today. You can get it right now absolutely FREE. Click here right now for your free copy and to start pulling in up to $2,175 in extra income every week.

Source: Investors Alley

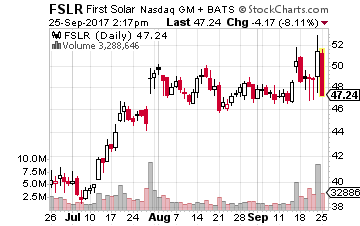

Whether you believe in the use of tariffs or not, one certain consequence of a solar tariff is sales of US manufactured panels will increase. That’s why stock investors are snapping up shares in companies like First Solar (NASDAQ: FSLR), the largest solar company in the US.

Whether you believe in the use of tariffs or not, one certain consequence of a solar tariff is sales of US manufactured panels will increase. That’s why stock investors are snapping up shares in companies like First Solar (NASDAQ: FSLR), the largest solar company in the US.

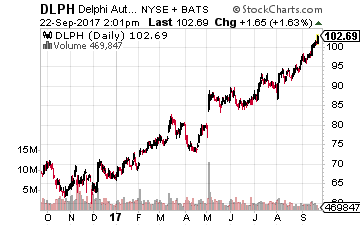

At the top of the list is a company that was once part of General Motors (NYSE: GM), Delphi Automotive PLC (NYSE: DLPH). The spinoff was completed in 1999, as sadly, GM management listened to Wall Street advice about streamlining operations by getting rid of a business “going nowhere.”

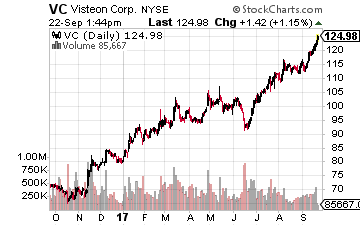

At the top of the list is a company that was once part of General Motors (NYSE: GM), Delphi Automotive PLC (NYSE: DLPH). The spinoff was completed in 1999, as sadly, GM management listened to Wall Street advice about streamlining operations by getting rid of a business “going nowhere.”  The next company to consider was also a spinoff – this time from Ford in 2000 – Visteon (NYSE: VC). The reasons were similar to those of General Motors.

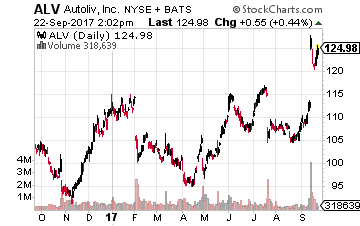

The next company to consider was also a spinoff – this time from Ford in 2000 – Visteon (NYSE: VC). The reasons were similar to those of General Motors. The third company has been a relative laggard, with its stock only up about 8.5% so far in 2017, the Swedish auto parts giant Autoliv (NYSE: ALV). Most of that upward movement in the stock price happened after a recent announcement.

The third company has been a relative laggard, with its stock only up about 8.5% so far in 2017, the Swedish auto parts giant Autoliv (NYSE: ALV). Most of that upward movement in the stock price happened after a recent announcement.

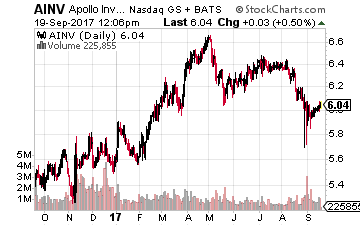

Apollo Investment Corp. (NASDAQ: AINV) is a $1.4 billion market cap BDC. The company reduced its dividend by 25% in 2016. AINV trades at a 10% discount to NAV. The current yield is 10.0% and the company’s net investment income just covered the dividend for the 2017 second quarter.

Apollo Investment Corp. (NASDAQ: AINV) is a $1.4 billion market cap BDC. The company reduced its dividend by 25% in 2016. AINV trades at a 10% discount to NAV. The current yield is 10.0% and the company’s net investment income just covered the dividend for the 2017 second quarter.

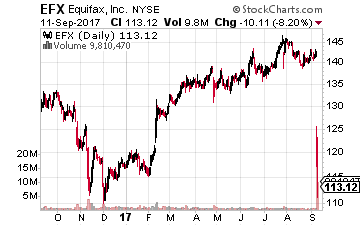

But first, more on this nasty underside of life in the 21stcentury coming to the fore again as the credit-reporting agency Equifax (NYSE: EFX) revealed a massive breach of its cyber defenses.

But first, more on this nasty underside of life in the 21stcentury coming to the fore again as the credit-reporting agency Equifax (NYSE: EFX) revealed a massive breach of its cyber defenses. Of course, massive data breaches aren’t confined to just this industry. Last December, Yahoo (now part of Verizon (NYSE: VZ) revealed that attacks between 2013 and 2016 had compromised the personal information of more than a billion users. The data stolen included names, phone numbers, birth dates and passwords.

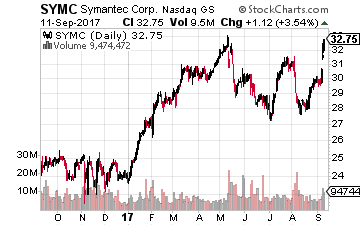

Of course, massive data breaches aren’t confined to just this industry. Last December, Yahoo (now part of Verizon (NYSE: VZ) revealed that attacks between 2013 and 2016 had compromised the personal information of more than a billion users. The data stolen included names, phone numbers, birth dates and passwords. According to a report from cyber security company Symantec (Nasdaq: SYMC), hackers have breached the operational systems of utility companies in the U.S. Symantec says they are lying in wait with the ability to switch off the power and sabotage computer networks.

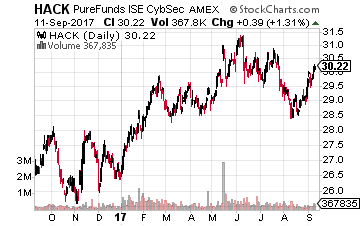

According to a report from cyber security company Symantec (Nasdaq: SYMC), hackers have breached the operational systems of utility companies in the U.S. Symantec says they are lying in wait with the ability to switch off the power and sabotage computer networks. For the broadest possible exposure to the sector, I like the ETFMG Prime Cyber Security ETF (NYSE: HACK). It is up nearly 13% year-to-date and just 10% over the 52 weeks.

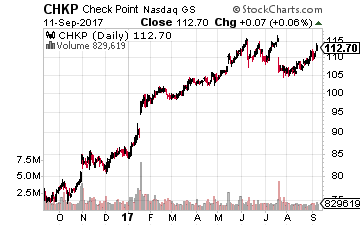

For the broadest possible exposure to the sector, I like the ETFMG Prime Cyber Security ETF (NYSE: HACK). It is up nearly 13% year-to-date and just 10% over the 52 weeks. Palo Alto Networks offers network security solutions, such as next-generation firewall products, to businesses, service providers and governments. As of the end of 2016, the company was third in the security appliance segment (in terms of revenues) trailing only Cisco Systems and Check Point Software Technologies (Nasdaq: CHKP).

Palo Alto Networks offers network security solutions, such as next-generation firewall products, to businesses, service providers and governments. As of the end of 2016, the company was third in the security appliance segment (in terms of revenues) trailing only Cisco Systems and Check Point Software Technologies (Nasdaq: CHKP).

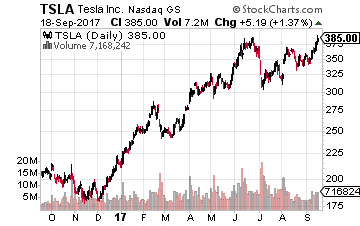

So let’s ‘imagine’ a bit… I’m going to reveal to you the best ways to play this milestone for the electric vehicle industry. And it does not involve buying Elon Musk’s Tesla Motors (Nasdaq: TSLA).

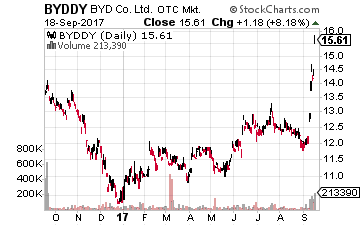

So let’s ‘imagine’ a bit… I’m going to reveal to you the best ways to play this milestone for the electric vehicle industry. And it does not involve buying Elon Musk’s Tesla Motors (Nasdaq: TSLA). Leading the race already in China is BYD (OTC: BYDDY), of which Warren Buffet owns 8.25%. It is currently the world’s largest electric car maker and produced nearly 47,000 electric and hybrid vehicles in the first seven months of 2017.

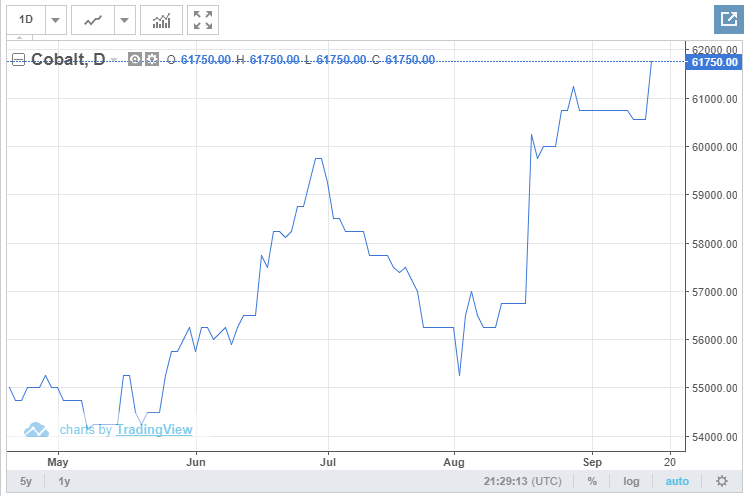

Leading the race already in China is BYD (OTC: BYDDY), of which Warren Buffet owns 8.25%. It is currently the world’s largest electric car maker and produced nearly 47,000 electric and hybrid vehicles in the first seven months of 2017. That hottest of all commodities sector centers on the key elements needed in lithium-ion batteries – lithium and cobalt (needed for the cathodes). These commodities account for roughly 60% of the cost of a lithium-ion battery, so says Simon Moores of the specialized consultancy, Benchmark Mineral Intelligence.

That hottest of all commodities sector centers on the key elements needed in lithium-ion batteries – lithium and cobalt (needed for the cathodes). These commodities account for roughly 60% of the cost of a lithium-ion battery, so says Simon Moores of the specialized consultancy, Benchmark Mineral Intelligence. Investors almost got it right this past week when they poured money into the Global X Lithium & Battery Tech ETF (NYSE: LIT). Investors sent the price of this ETF up by 10.25% last week, pushing this year’s gain to 55.25%.

Investors almost got it right this past week when they poured money into the Global X Lithium & Battery Tech ETF (NYSE: LIT). Investors sent the price of this ETF up by 10.25% last week, pushing this year’s gain to 55.25%.