Every holiday season I’m reminded of my first few years living as an immigrant in the United States.

You see, when I first came to this country, I’d never heard of Thanksgiving Day. In fact, I spent the first few years that I lived here believing that Thanksgiving was a national holiday dedicated to appreciating whatever you were most thankful for in your life.

And while I would eventually go on to learn all about American history and the story of the harvest festival, this time of year still makes me humble. It forces me to take a step back and think about what I’m most grateful for.

I would encourage you to do the same this holiday season. The markets are now closed in observance of Thanksgiving, so take some well-deserved time this weekend to enjoy the presence of your loved ones.

There will be plenty of time to worry about the markets next week, so I’m going to use this article as an opportunity to tell you about two brand-new mega trends I’ll be looking to add to my flagship newsletter, Profits Unlimited, in 2018.

Blockchain Is Creating A Truly Decentralized Economy

The first of these new themes is going to be blockchain as it relates to finance.

Blockchain is an online global ledger that anyone can use, but that also doesn’t exist in any master location. Think of it like an Excel spreadsheet that exists on multiple computers at the same time and that automatically updates itself every 10 minutes.

The decentralization aspect of this ledger makes it impossible for hackers to encrypt it and also makes it communal, because anyone who has an internet connection and who wants the database can do so.

This technology has turned the financial industry on its head, because for the first time in history, two different parties can come together to make a safe exchange without having to involve intermediaries, such as banks, rating agencies or bodies of government.

Add in the fact that our traditional banking system is overrun with fraud, additional fees and lots of paperwork, and you can immediately see why more and more people are turning to blockchain to make their transactions.

Given how completely disruptive this technology is, it’s no surprise that the global banking community is scrambling to implement blockchain technology into its existing infrastructure. But banks aren’t the only entities about to be disrupted by blockchain.

Imagine a truly decentralized economy where the middleman could be cut out of all transactions. It would affect every single industry in the world, from retail to transportation, to crowdfunding initiatives.

This is the kind of game-changing technology I want to be a part of, because the returns it could bring early investors are potentially limitless.

Ridiculous Amounts of Energy

Having said that, there is one major drawback to blockchain that also affects the Internet of Things mega trend. Both emerging industries require ridiculous amounts of energy output.

In fact, a 2014 study by researchers Karl J. O’Dwyer and David Malone showed that the bitcoin network alone was likely to take up as much electricity consumption as the entire country of Ireland. So, imagine how much energy we would need if all the banks in the world started to move toward digital currencies just to keep up with their competition.

That’s just not sustainable with our current energy grid, and it’s the reason why I’ll be looking to bring storable, renewable, natural energy-solution companies into my Profits Unlimited portfolio next year.

I don’t want to give anything away just yet, but between my current mega trends and the two new themes I’m beginning to track, I can promise you that next year will be a very exciting time to be a Profits Unlimited reader.

If you’d like to get in on the action and join me as I unearth companies taking advantage of these brand-new themes.

I’m going to end there for this week, but from my family to yours, I wish you the happiest holiday season.

Regards,

Paul Mampilly

Editor, Profits Unlimited

Right now, an untapped ocean of energy—found underneath all 50 states—is about to transform the world’s energy industry. In fact, there’s enough of this energy in the first six miles of the earth’s crust to power the United States for the next 30,000 years. Wanna know this untapped energy source? Learn NOW! And as companies rush to extract this energy from the ground, they’ll need the help of one Midwestern company’s technology to make use of it. This is your chance to take advantage of John D. Rockefeller-type fortunes. Early Bird Gets The Worm...

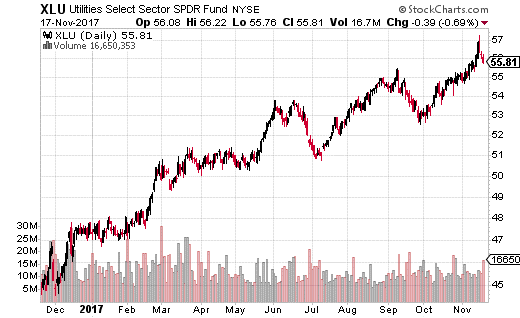

Utilities are already known to be a slow moving asset. So, if someone with big bucks is selling straddles in utilities, you can bet the range is going to be extremely tight. In this case, the straddles don’t expire until January of 2019 – so utilities may remain in a narrow range for all of 2018.

Utilities are already known to be a slow moving asset. So, if someone with big bucks is selling straddles in utilities, you can bet the range is going to be extremely tight. In this case, the straddles don’t expire until January of 2019 – so utilities may remain in a narrow range for all of 2018.

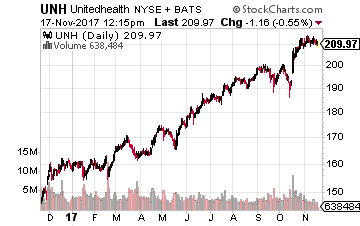

Among the companies in the prescription drug distribution sector, I believe the best of the lot is UnitedHealth Group. About 40% of its revenues come its Optum Rx PBM business, with the remaining 60% of revenues coming from its vast health insurance businesses.

Among the companies in the prescription drug distribution sector, I believe the best of the lot is UnitedHealth Group. About 40% of its revenues come its Optum Rx PBM business, with the remaining 60% of revenues coming from its vast health insurance businesses.