One of the great things about options is how flexible they can be for custom-designing strategies to meet your needs. With options, even something as mundane as hedging can be done in an interesting and creative manner.

This is especially true since volatility ETPs (exchange traded products) have become widely popular among traders and investors. Being able to buy or sell volatility (related to the level of the VIX) is something which used to be restricted to the realm of the professional options trader.

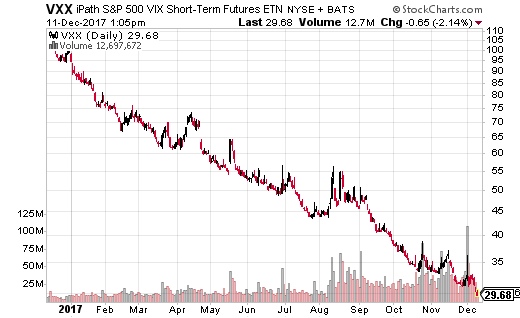

Now, a fund like iPath S&P 500 VIX Short-term Futures ETF (NYSE: VXX) is as commonly traded as just about any individual stock or ETF on the market. In fact, VXX is one of the top 10 most actively traded equities, period. It’s a useful instrument for betting for (or against) a short-term spike in volatility. In particular, it makes for a great hedging tool for long stock portfolios.

Speaking of hedging, here’s a very interesting trade that hit the wire just recently in VXX…

With the VXX price at $31.50, someone sold a January 29 put while simultaneously buying a January 35 call. This kind of trade is called a risk reversal and it’s clearly bullish on VXX. The short put is used to help finance the long call.

In this case, selling the put brought down the price of the call to $0.57 (it would have cost $1.88 without the premium collected from the put sale). The risk reversal traded 7,000 times, so the trade cost the buyer $342,000 in premium – a substantial amount lower than what the call would cost straight up.

Still, that’s a lot of premium to spend on a product known for mostly going down (as you can see in the chart). As such, this trade is likely a creative way to hedge against volatility risk through mid-January. If VXX stays where it is, all that’s lost is the premium amount (not bad for a hedge on what is likely a big portfolio). However, if VXX climbs above roughly $35.50, the position makes $700,000 per $1 higher.

On the other hand, the position could lose $700,000 per $1 below $29 (along with the premium spent) due to the short put. However, VXX isn’t likely to plummet that quickly due to macro event risk. Rather, it is more likely to move down slowly – giving the trader time to adjust the risk reversal as necessary.

I think it’s an interesting way to hedge risk, as long as you are able to make adjustments as VXX moves lower. It wouldn’t be too difficult (or overly expensive) to buy back the short puts as VXX approaches $29.

Keep in mind, this isn’t the sort of method most of us should use for trading VXX. If you want to use VXX to hedge (or speculate due to event risk), buying straight up calls or a call spread has defined risk. For keeping costs low, a call spread is the better choice.

For instance, the January 32-37 call spread (with VXX around $31.50) only costs about $1. That’s a breakeven point of $33, and a max gain of $4. You can only lose the $1 you spent in premium, so your payout ratio is 4:1. That’s a reasonably cheap way to hedge, and balances your payoff with reasonable costs.

[FREE REPORT] Options Income Blueprint: 3 Proven Strategies to Earn More Cash Today Discover how to grab $577 to $2,175 every 7 days even if you have a small brokerage account or little experience... And it's as simple as using these 3 proven trading strategies for earning extra cash. They’re revealed in my new ebook, Options Income Blueprint: 3 Proven Strategies to Earn Extra Cash Today. You can get it right now absolutely FREE. Click here right now for your free copy and to start pulling in up to $2,175 in extra income every week.

Source: Investors Alley