With the market primed for success in 2018, I wanted to find stocks that go above and beyond the normal growth prospects. Here I looked for seven top growth stocks with huge upside potential and serious Street support. The best way to find these stocks is with TipRanks’ Top Analyst Stocks tool.

Why? Well, the tool reveals all stocks with a ‘Strong Buy’ rating from Wall Street’s best-performing analysts. You can then sort the stocks by upside potential to pinpoint compelling investing opportunities.

At the same time, I was careful to avoid stocks that have big upside potential simply because share prices have crashed recently. Check the price movement over the last three months to be sure shares are moving in the right direction.

With that being said, let’s get straight down into taking a closer look at these seven stocks — all of which I believe look undervalued right now:

Stocks With Top Buy Ratings: Cloudera (CLDR)

Big data cruncher Cloudera, Inc. (NYSE:CLDR) has upside potential of 27% say the Street’s top analysts. Currently, the stock is trading at $17.88 but analysts see it hitting $22.75 in the coming months. The stock has experienced some volatility in the last year, but it is now facing 2018 with a very promising setup. Indeed, in the last three months, shares have already improved 27%!

Abhey Lamba, a five-star Mizho analyst, notes that management has delivered results above consensus expectations in its first few quarters as a public company. He upgraded his Cloudera rating from “hold” to “buy” on Jan. 9. Here he explains why he is turning bullish on CLDR:

We can see from TipRanks that this ‘Strong Buy’ stock has 100% Street support. Indeed, in the last three months, CLDR has received five straight “buy” ratings, including an upgrade from Citigroup.

Source: Shutterstock

Stocks With Top Buy Ratings: Arena Pharma (ARNA)

Healthcare stock Arena Pharmaceuticals, Inc. (NASDAQ:ARNA) has monster upside potential of almost 50%. Shares are already up 25% in the last three months. And now top analysts say the stock can leap from its current share price of $34.36 to $51.33.

Plus, it received three very recent “buy” ratings from top analysts all with bullish price targets.

The company’s development pipeline includes two important drugs: Etrasimod for chronic bowel disease Ulcerative Colitis (UC) and Ralinepag for Pulmonary Arterial Hypertension (PAH). William Tanner, a top healthcare analyst from Cantor Fitzgerald, is excited about both.

He says:

“We remain convinced that ralinepag could be a best-in-class treatment for pulmonary arterial hypertension (PAH)… Less well appreciated may be the potential of estrasimod, Arena’s S1P receptor modulator.” Arena is planning to release key Phase 2 data for estrasimod in 1Q18, and according to Tanner “positive data could create an opportunity for meaningful share price appreciation.”

Stocks With Top Buy Ratings: Dave & Busters (PLAY)

The hybrid game arcade and restaurant chain Dave & Buster’s Entertainment, Inc. (NASDAQ:PLAY) is set for a rebound in 2018. And that means big upside potential of 43% from the current share price. That would take shares all the way from $46 to $66.

However, Maxim Group’s Stephen Anderson is much more bullish than consensus. He believes the stock can soar to $83. This suggests massive upside potential of 79% from the current share price. Even though the stock has experienced some short-term sales volatility, he says that valuation remains very compelling.

The stock is ‘deeply inexpensive relative to Casual Dining Peers’ and ultimately: “Our core thesis on PLAY, which is comprised of; (1) high-margin entertainment revenue growth; (2) robust unit expansion; and (3) longer-term comp growth of at least 2%, remains intact.” PLAY should also benefit big-time from the upcoming tax reform.

In the last three months, PLAY has received an impressive eight consecutive “buy” ratings. As a result, the stock has a ‘Strong Buy’ analyst consensus. Out of these ratings, five come from best-performing analysts.

Stocks With Top Buy Ratings: CBS Corp (CBS)

Media stock CBS Corporation (NYSE:CBS) can climb a further 23% in the next 12 months say top analysts. This would see the stock trading at over $70 vs the current share price of just under $60.

Just a couple of days ago, on January 16, Benchmark’s Daniel Kurnos reiterated his “buy” rating. This was accompanied with a very bullish $78 price target (32% upside). “At just 9x 2018E OIBDA and 11x EPS, we believe CBS represents the best value in the network space” states Kurnos.

Reassuringly, Kurnos says “that the demise of Network ad revenues is greatly exaggerated.” He even says that this bearish talk is overshadowing “the positive traction CBS is seeing in its ancillary revenue streams.” The underlying business model is very strong and “the pressure on the media sector has created a buying opportunity for the content leader.”

Note that Kurnos is ranked as #210 out of over 4,750 analysts on TipRanks. Meanwhile, out of nine recent ratings on CBS, eight are buys. This means that in the last three months only one analyst has published a “hold” rating on the stock.

Source: Shutterstock

Stocks With Top Buy Ratings: Neurocrine (NBIX)

Over the last three months, Neurocrine Biosciences, Inc. (NASDAQ:NBIX) has already spiked by 29%. And top analysts believe this biopharma still has serious growth potential left to run in 2018. Specifically, the Street sees NBIX rising 33% from $76 to just over $100.

The Street is buzzing about Neurocrine’s Ingrezza drug. This is the first FDA-approved treatment for adults with tardive dyskinesia (TD). A side effect of antipsychotic medication, TD is a disorder that leads to unintended muscle movements. Oppenheimer’s Jay Olson is very optimistic about Ingrezza’s potential. He says:

“Ingrezza performance continues to overwhelm on several dimensions, and our observations suggest Ingrezza could become a pipeline within a drug that could unlock substantial unappreciated value to shareholders.” He even suggests this drug has ‘pipeline’ potential by expanding into similar disorders like Tourette Syndrome.

Encouragingly, the stock has received no less than 10 consecutive “buy” ratings from analysts in the last three months. Seven out of the 10 of these “buy” ratings are from top-performing analysts.

Source: Shutterstock

Stocks With Top Buy Ratings: Sinclair Broadcast (SBGI)

Sinclair Broadcast Group, Inc. (NASDAQ:SBGI) is one of the U.S.’s largest and most diversified television station operators. SBGI is already up 30% in the last three months. And top analysts see 25% upside potential ahead- with the stock due to get a big tax reform boost.

Indeed, Benchmark Capital has just named SBGI as one of its Best Ideas for 1H18. Five-star Benchmark analyst Daniel Kurnos says “We see SBGI as one of the best values in the entire media landscape.” He is eyeing $55 as a potential price target (40% upside potential).

According to Kurnos, Sinclair has multiple upcoming catalysts over the next six months. This includes the pending mega deal between Sinclair and Tribune. Sinclair is currently waiting for regulatory approval for the $3.9 billion takeover would give Sinclair control of 233 TV stations.

Top analysts are united in their bullish take on this ‘Strong Buy’ stock. In the last three months, five analysts have published buy ratings on Sinclair.

Source: Shutterstock

Stocks With Top Buy Ratings: Laureate Education (LAUR)

Laureate Education, Inc. (NASDAQ:LAUR) is the largest network of for-profit higher education institutions. This Baltimore-based stock owns and operates over 200 programs (on campus and online) in over 29 countries. Over the last three months, the stock is up 10%. But analysts say bigger upside of over 19% is on the way. Currently, this is still a relatively cheap stock to buy at just $15.26.

Furthermore, Stifel Nicolaus analyst Shlomo Rosenbaum notes that Chile’s election result is a “material positive” for Laureate. He says new President Sebastian Pinera is less likely to support legislation for free post-secondary education- the prospect of which has dampened prices to date. Rosebaum currently has an $18 price target on the stock (18% upside).

Overall, Laureate certainly has the Street’s seal of approval. The stock has scored four top analyst “buy” ratings recently. This includes a bullish call from one of TipRanks’ Top 20 analysts for 2017, BMO Capital’s Jeffrey Silber.

Can a $10 Bill Really Fund Your Retirement? The digital currency markets are delivering profits unlike anything we’ve ever seen. 23 recently doubled in a single week. And some like DubaiCoin have jumped as much as 8,200X in value in 18 months. It’ unprecedented... but you won’t receive any of the rewards unless you put a little money in the game. Find out how $10 could make you rich HERE.

Source:

Investor Place

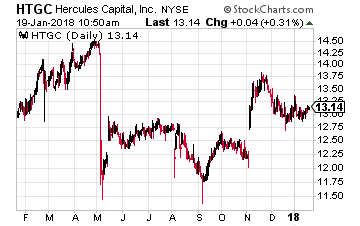

Hercules Capital Inc (NYSE: HTGC) is a business development company (BDC) that makes loans in in the venture capital space. Hercules client companies are growth businesses backed by venture capital investors that need additional capital to fulfil their growth and investment goals.

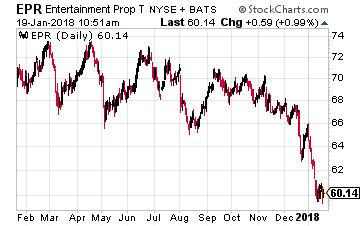

Hercules Capital Inc (NYSE: HTGC) is a business development company (BDC) that makes loans in in the venture capital space. Hercules client companies are growth businesses backed by venture capital investors that need additional capital to fulfil their growth and investment goals. EPR Properties (NYSE: EPR) is a very well-run net lease REIT that has done a great job of growing the business and generating above average dividend growth for investors. With the net-lease (NNN) model, the tenants that lease the properties owned by EPR are responsible for all the operating costs like taxes, utilities and maintenance. EPR’s job is to collect the rent checks. Typically, NNN leases are long term, for 10 years or more, with built-in rent escalations.

EPR Properties (NYSE: EPR) is a very well-run net lease REIT that has done a great job of growing the business and generating above average dividend growth for investors. With the net-lease (NNN) model, the tenants that lease the properties owned by EPR are responsible for all the operating costs like taxes, utilities and maintenance. EPR’s job is to collect the rent checks. Typically, NNN leases are long term, for 10 years or more, with built-in rent escalations.

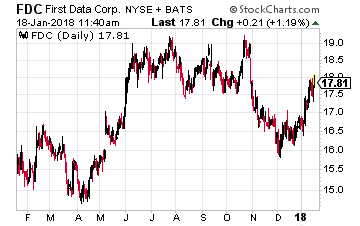

First Data (NYSE: FDC) provides merchant transaction processing; credit, debit and retail card issuing and processing; prepaid services and check verification and other similar services.

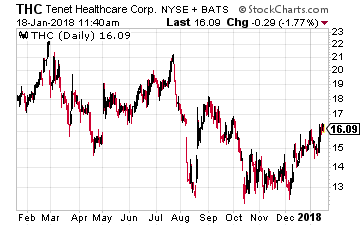

First Data (NYSE: FDC) provides merchant transaction processing; credit, debit and retail card issuing and processing; prepaid services and check verification and other similar services. Tenet Healthcare (NYSE: THC) owns and operates hospitals and other healthcare facilities. It is one of the largest investor-owned healthcare delivery systems in the United States.

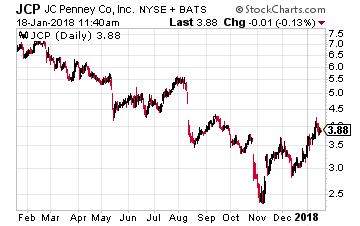

Tenet Healthcare (NYSE: THC) owns and operates hospitals and other healthcare facilities. It is one of the largest investor-owned healthcare delivery systems in the United States. JC Penney (NYSE: JCP) is a well-known department store chain with still 875 stores across the U.S. It is almost a poster child for being Amazoned. Adding to all the woes it faces on the competitive front is its heavy debt burden in excess of $4 billion.

JC Penney (NYSE: JCP) is a well-known department store chain with still 875 stores across the U.S. It is almost a poster child for being Amazoned. Adding to all the woes it faces on the competitive front is its heavy debt burden in excess of $4 billion.

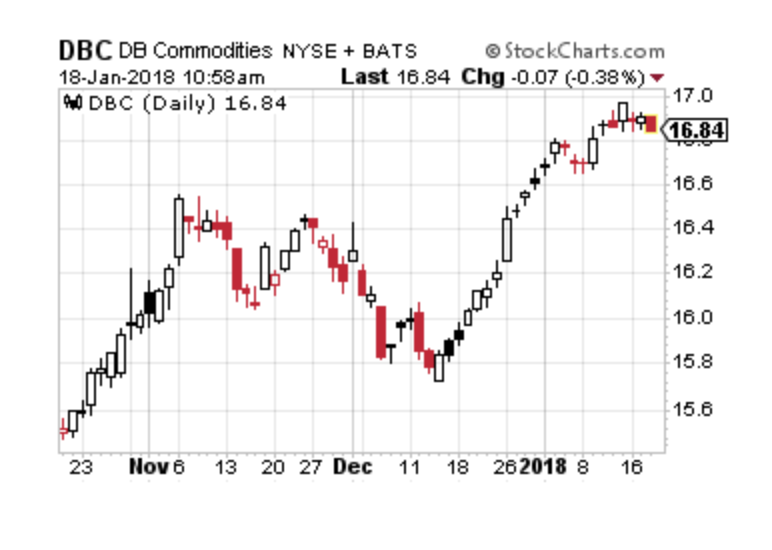

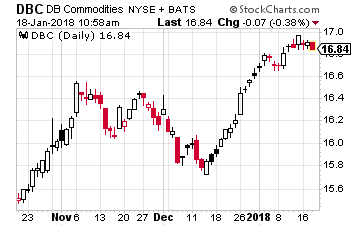

It’s probably not a surprise, but traders may be positioning for a rise in commodities pricing. The usually not-too-heavily-traded PowerShares DB Commodity Tracking Index (NYSE: DBC)had a fair amount of action last week, for example.

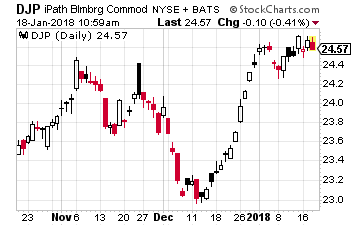

It’s probably not a surprise, but traders may be positioning for a rise in commodities pricing. The usually not-too-heavily-traded PowerShares DB Commodity Tracking Index (NYSE: DBC)had a fair amount of action last week, for example. For a broad-based ETF, I actually want all the important commodities to be as equally weighted as is reasonable. A much better product for this type of weighting is the iPath Bloomberg Commodity Total Return ETN (NYSE: DJP).

For a broad-based ETF, I actually want all the important commodities to be as equally weighted as is reasonable. A much better product for this type of weighting is the iPath Bloomberg Commodity Total Return ETN (NYSE: DJP).

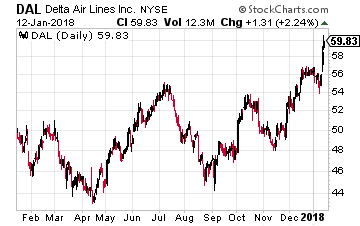

Take Delta Air Lines (NYSE: DAL), for example. Just last week it said that the tax cut will boost its earnings by about $800 million a year. That translates to about $1 per share in increased earnings for 2018. Delta management raised their earnings per share guidance for 2018 to a range of $6.35 to $6.70, up 20% to 30% from the year earlier level.

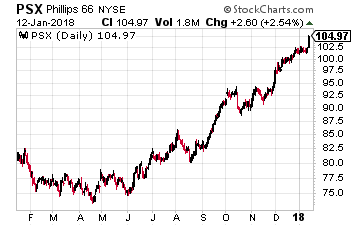

Take Delta Air Lines (NYSE: DAL), for example. Just last week it said that the tax cut will boost its earnings by about $800 million a year. That translates to about $1 per share in increased earnings for 2018. Delta management raised their earnings per share guidance for 2018 to a range of $6.35 to $6.70, up 20% to 30% from the year earlier level. And it’s not just the big oil firms to benefit. The oil refining segment should really get a major boost. The largest company in the segment, by market capitalization, Phillips 66 (NYSE: PSX), will receive a 16% boost to 2018 earnings according to an estimate from Piper Jaffray’s Simmons & Company energy investment bank unit.

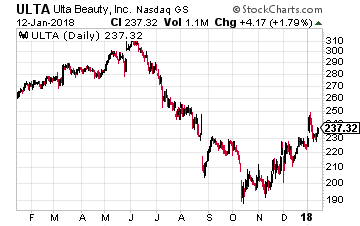

And it’s not just the big oil firms to benefit. The oil refining segment should really get a major boost. The largest company in the segment, by market capitalization, Phillips 66 (NYSE: PSX), will receive a 16% boost to 2018 earnings according to an estimate from Piper Jaffray’s Simmons & Company energy investment bank unit. One of my favorites in the sector is Ulta Beauty (Nasdaq: ULTA), which operates 1,058 stores and generated $4.8 billion in revenues in 2016. It should get a double boost – not only from the tax cut itself, but from consumers with a little extra in their pocket spending on simple luxuries like makeup, lip gloss, etc. Perhaps that’s why the stock is already up over 6% year-to-date.

One of my favorites in the sector is Ulta Beauty (Nasdaq: ULTA), which operates 1,058 stores and generated $4.8 billion in revenues in 2016. It should get a double boost – not only from the tax cut itself, but from consumers with a little extra in their pocket spending on simple luxuries like makeup, lip gloss, etc. Perhaps that’s why the stock is already up over 6% year-to-date.