When the market experiences a sharp sell-off, savvy investors may choose to look elsewhere for their profit fix. Luckily enough, Morgan Stanley has just released a very intriguing report highlighting 15 stocks that are most likely to be bought in 2018. The firm singled out these acquisition targets by looking for large, liquid stocks from different sectors that are most likely to be acquired in the next 12 months. There is big value in identifying takeover targets correctly, as share prices tend to soar when a deal is announced.

From the list, we used TipRanks to identify the top stocks with a bullish Street outlook. Four of the seven stocks below boast a “Strong Buy” analyst consensus rating. Three of the stocks score a “Moderate Buy” analyst consensus rating — but for two of the stocks this is due to the lack of ratings more than than the sentiment itself. The advantage of these stocks is that they represent compelling investing opportunities — with or without a takeover deal.

TipRanks’ algorithms track and rank almost 5,000 Wall Street analysts. This allows us to: 1) see the overall analyst consensus and upside potential on any stock and 2) extract insights from the Street’s best-performing analysts.

So with this in mind, let’s take a closer look at what the Street has to say about these key stocks:

Top Takeover Targets: Domino’s Pizza (DPZ)

Domino’s Pizza Inc (NYSE:DPZ) has just experienced one of its busiest delivery days. The company expected to sell over 13 million pizza slices and 4 million chicken wings across the US on Super Bowl Sunday — boosted by multiple special offers on chicken wings and pizza toppings.

And, with strong U.S. growth under its belt, this pizza delivery giant scores a “Strong Buy” rating from the Street. This breaks down into eight buy ratings vs just two hold ratings. Meanwhile the average price target of $230 indicates upside potential of over 10% from the current share price.

Top Maxim Group analyst Stephen Anderson has a $250 price target on DPZ (18% upside). He says: “DPZ is one of our top industry picks as the valuation remains attractive.” Anderson also points out that for the first time, DPZ is now the market share leader in the Quick Service pizza category with 16.9% of total sales.

Top Takeover Targets: Graphic Packaging (GPK)

You’ve probably purchased food, beverages or other consumer products sold in packaging by Graphic Packaging Holding Company (NYSE:GPK). Immediately, we can see from the Street that GPK has a “Strong Buy” analyst consensus rating and big upside potential of 29% to boot.

RBC Capital’s Arun Viswanathan ramped up his $17 price target to $19 (23% upside) while reiterating his buy rating. He attributes the bullish move to 1) tax benefits for US-exposed packaging companies like GPK and 2) the recent $5 billion offer for KapStone Paper(NYSE:KS) from packaging company WestRock LLC (NYSE:WRK).

The deal, announced on Feb. 1, sees WRK pay a multiple of about 10x for KapStone. As a result of the tax reforms, GPK will now only pay a 24%-27% rate instead of 35.18% previously.

Top Takeover Targets: Pinnacle Foods (PF)

Pinnacle Foods, Inc. (NYSE:PF) is the business behind many famous food brands, including Birds Eye vegetables and Log Cabin syrups. Indeed its brands are so widespread that apparently 85% of US households have a Pinnacle Foods product in their kitchen right now. But most interesting of all is that Dan Loeb’s Third Point fund has just taken a stake in PF- leading the takeover rumor mill to work overtime.

Stephens analyst Farha Aslam reiterated her buy rating on Jan. 29 with a $65 price target (11% upside). She is convinced that if Loeb spearheads an activist campaign it would be for a sale instead of simply operational or management changes. Aslam suggests food giants ConAgra Foods (NYSE:CAG) or Tyson Foods (NYSE:TSN) as potential buyers with a valuation of around $67-$70 per share. Indeed Tyson Foods is not afraid of big purchases. It acquired sausage company Hillshire Brands for a whopping $8.55 billion back in 2014.

From a Street perspective, this “Strong Buy” stock has received 100% Street support over the last year. On the basis of the last three months alone, analysts see Pinnacle spiking to $67 (15% upside) from the current $60 share price.

Top Takeover Targets: Express Scripts (ESRX)

Express Scripts Holding Company (NASDAQ:ESRX) is the largest pharmacy benefit management organization in the US. TipRanks reveals that the company has a “Strong Buy” analyst consensus rating from best-performing analysts. Indeed JP Morgan’s Lisa Gill calls ESRX her top pick in Healthcare Technology & Distribution for fiscal 2018.

But most exciting here is the recent upgrade by RBC Capital’s George Hill. On Jan. 31 he ramped up his price target from $68 to a very bullish $91 (31% upside potential).

Hill reaffirms Morgan Stanley’s selection and says that Express Scripts looks like an attractive M&A target as “one of the few remaining assets at scale”. He also cites the “recent sharp pullback on Amazon.com, Inc.’s (NASDAQ:AMZN) healthcare entry” as de-risking the stock.

Top Takeover Targets: W.R. Grace (GRA)

This U.S. chemicals conglomerate has only received two recent analyst ratings — hence its “Moderate Buy” analyst consensus. However, both these ratings are firm buys. In particular, we can see that KeyBanc’s Michael Sison highlights the opportunity for large M&A as one of W.R. Grace & Co.’s (NYSE:GRA) ongoing catalysts.

Indeed, the company has just signed a $416 million deal for Albemarle Corp’s (NYSE:ALB) polyolefin catalysts and components business for $416 million. Sison highlighted the company’s improving results and reiterated his buy rating with an $87 price target (24% upside).

Top Takeover Targets: Allergan (AGN)

Barclays’ Douglas Tsao has just upgraded Botox maker Allergan Plc. (NYSE:AGN) from “hold” to “buy.” The move comes with a bullish $230 price target (39% upside) up from $220 previously. Tsao’s shift in sentiment, after over three years on the sidelines, comes from the company’s market-leading Botox position. And he doesn’t see any cause for concern any time soon:

“While Revance’s RT-002 and, to a less extent, Evolus, represent competition, we expect Botox will retain its market leadership,” Tsao wrote on January 29. “Especially in the case of Revance, we expect new entrants to drive market expansion from current levels.” As a result he calls the Irish-based company’s aesthetics business “undervalued at current levels.”

However concerns over the stock’s longer-term outlook have led to its more cautious “Moderate Buy” analyst consensus rating. In the last three months Allergan has received nine buy ratings. However these are offset by five hold ratings. Analysts (on average) see the stock rising 29% to hit $213 in the coming months.

Top Takeover Targets: Six Flags (SIX)

Six Flags Entertainment Corp (NYSE:SIX) is one of the world’s largest theme park operators with over 135 rollercoasters to its name. Top B.Riley FBR analyst Barton Crockett is bullish on theme parks in general- and SIX specifically.

Despite a volatile 2017, Crockett is confident the stock “can maintain a premium multiple because of exposure to high-margin international licensing, a unique focus on share repurchase, and a tendency for attractive growth (ex-natural disaster interruptions from fires, earthquakes and hurricanes that impacted 2017.)” He reiterated his buy rating on Jan 26 while ramping up his price target from $71 to $78 (21% upside potential).

Bear in mind that SIX also pays out a lucrative dividend. Wedbush’s James Hardimananticipates that SIX will pay a 4.2% dividend yield on his estimated 2018 dividend payout of $3.18. Hardiman sees SIX at $76 vs the current share price of $65.

[FREE REPORT] Options Income Blueprint: 3 Proven Strategies to Earn More Cash Today Discover how to grab $577 to $2,175 every 7 days even if you have a small brokerage account or little experience... And it's as simple as using these 3 proven trading strategies for earning extra cash. They’re revealed in my new ebook, Options Income Blueprint: 3 Proven Strategies to Earn Extra Cash Today. You can get it right now absolutely FREE. Click here right now for your free copy and to start pulling in up to $2,175 in extra income every week.

Source: Investors Alley

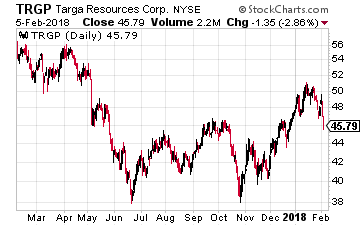

At the time of its 2010 IPO, Targa Resources Corp (NYSE: TRGP) owned the general partner interests in the midstream MLP, Targa Resources Partners LP (NYSE: NGLS). When energy prices crashed in 2015, the separate general partner and MLP business arrangement was an expense drag on the companies. In early 2016 TRGP completed the purchase of all NGLS units, which eliminated the general partner expenses. Currently Targa Resources operates four business units providing the following services:

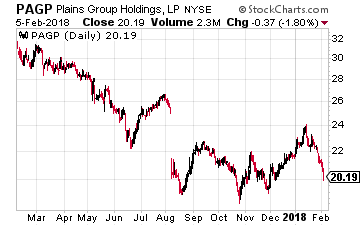

At the time of its 2010 IPO, Targa Resources Corp (NYSE: TRGP) owned the general partner interests in the midstream MLP, Targa Resources Partners LP (NYSE: NGLS). When energy prices crashed in 2015, the separate general partner and MLP business arrangement was an expense drag on the companies. In early 2016 TRGP completed the purchase of all NGLS units, which eliminated the general partner expenses. Currently Targa Resources operates four business units providing the following services: Plains GP Holdings LP (NYSE: PAGP) was also a general partner interests company, owning GP rights from large cap MLP Plains All American Pipeline, LP (NYSE: PAA). Last year, the companies restructured, eliminating the GP interests and expenses. Now each PAGP share is backed by one PAA unit. PAA is a K-1 reporting company and PAGP reports tax info on a Form 1099. In all other respects, they are shares of the same company with the same dividend rates.

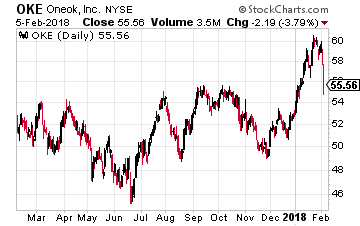

Plains GP Holdings LP (NYSE: PAGP) was also a general partner interests company, owning GP rights from large cap MLP Plains All American Pipeline, LP (NYSE: PAA). Last year, the companies restructured, eliminating the GP interests and expenses. Now each PAGP share is backed by one PAA unit. PAA is a K-1 reporting company and PAGP reports tax info on a Form 1099. In all other respects, they are shares of the same company with the same dividend rates. ONEOK, Inc. (NYSE: OKE) is another former general partner company that bought in its controlled MLP, ONEOK Partners LP. ONEOK completed the roll-up transaction in June 2017. This midstream company focuses on providing natural gas infrastructure services. Operations include a 38,000-mile integrated network of NGL and natural gas pipelines, processing plants, fractionators and storage facilities in the Mid-Continent, Williston, Permian and Rocky Mountain regions.

ONEOK, Inc. (NYSE: OKE) is another former general partner company that bought in its controlled MLP, ONEOK Partners LP. ONEOK completed the roll-up transaction in June 2017. This midstream company focuses on providing natural gas infrastructure services. Operations include a 38,000-mile integrated network of NGL and natural gas pipelines, processing plants, fractionators and storage facilities in the Mid-Continent, Williston, Permian and Rocky Mountain regions.