A startup called Basis has raised $133 million from top venture capitalists to build a “stable cryptocurrency” (also called a “stablecoin”).

A stablecoin is a cryptocurrency designed to eliminate the high volatility associated with most coins. The goal is to smooth out the ups and downs so the stablecoin is usable as an everyday currency.

Basis plans to stabilize its price by controlling coin supply, increasing it when demand is high and decreasing it when demand is low. It also mentioned possibly letting the coin’s price rise when the algorithms detect inflation. This is similar to how a central bank operates (or should operate).

The tagline on Basis’ site reads “A Stable Cryptocurrency With an Algorithmic Central Bank.”

Here’s an excerpt that describes the goal from Basis:

When demand is rising, the blockchain will create more Basis. The expanded supply is designed to bring the Basis price back down.

When demand is falling, the blockchain will buy back Basis. The contracted supply is designed to restore Basis price.

The Basis protocol is designed to expand and contract supply similarly to the way central banks buy and sell fiscal debt to stabilize purchasing power. For this reason, we refer to Basis as having an algorithmic central bank.

Basis does not plan to “peg” its price to the dollar like other successful stablecoins such as Tether (USDT) have done. Tether is currently the largest stablecoin, with a $2.3 billion market cap. (It trades within a tight range, around $1.)

Basis’ coin isn’t live yet, so we don’t know exactly how it will work in the real world. But the venture capitalists who are investing in this project clearly see huge potential.

The first signal is how much it raised: $133 million. That’s a monster round of funding for such a young company. The average funding round for a company at this stage is typically a few million dollars.

And the investors in this round include many of the best early-stage investors in the world. I almost never see a round of funding from such a prestigious group as this.

Let’s take a look at a few of the VC firms that just invested in Basis, a startup that says it’s “building a new monetary system.”

- Bain Capital Ventures: Manages $3.1 billion. Early investments include LinkedIn, Optimizely, Jet and Digital Currency Group.

- Andreessen Horowitz: Manages $2.7 billion. Early investments include Facebook, Skype, Reddit, Oculus and Box.

- Google Ventures (venture arm of Google): Manages $2 billion. Investments include Uber, Box, Jet and Nest.

- Lightspeed Ventures: Manages $4 billion. Early investments include Snapchat, DoubleClick and Brocade.

Don’t let the fact that these guys manage “only” $2 billion to $4 billion deceive you. That’s how much they’ve raised. They’re worth much more once you include the value of all the shares they hold and past profits. Lightspeed, for example, made $2 billion on its $8 million investment in Snapchat alone.

Other notable investors in Basis include leading cryptocurrency hedge funds Metastable and Polychain Capital.

This is a very powerful and influential group of investors. And they’ll need that power because they plan to take on one of the largest markets in the world: fiat money.

“Software Eating the World”

Andreessen Horowitz (usually called a16z) is a powerhouse in the venture capital world. Its investment thesis is that “software is eating the world.”

So it invests in disruptive technology companies. For example, it invested early in Skype, which, along with other chat platforms, disrupted the telecom business. It essentially killed the phone companies’ “long distance” business model.

In the case of Basis, a16z is investing in a startup that is attempting to disrupt the entire monetary system.

Competing with the dollar, euro and yen is an ambitious project, to say the least. Hence the $133 million monster round of funding…

If it can pull it off, it will be behind one of those technologies that could truly change the world: independent, stable, secure and inflation-resistant money. A system like this could immediately be utilized both as a payment platform and a store of value.

I believe it’s extremely possible to do from a technological standpoint. I strongly believe that, using blockchain technology and cryptography, a better, stable currency can be built.

The chief difficulty will be resistance from “establishment” groups. Primarily, we’re talking about governments and banks – our modern political elites.

These folks like the monetary and financial systems just fine the way they are and will likely make it hard to build a truly competitive currency. They already discourage other assets (like gold) from being used as money, primarily through regulations and taxes.

But the establishment is fighting an uphill battle in the long run. Its system of ever-increasing debt, high expenditures and easy money will ultimately collapse. At some point, people will adopt crypto despite its drawbacks. This has already begun around the world.

We’re seeing this play out acutely in Venezuela today. In the first quarter of this year, inflation in Venezuela raged at 454%. Its total inflation rate over the last 12 months is a staggering 8,900%.

Unsurprisingly, bitcoin trading volume is at an all-time high in Venezuela. LocalBitcoin, a site that facilitates person-to-person bitcoin exchanges, saw volume in the country spike from $18 million in all of March to more than $55 million in just the last week.

And in a desperate (but calculated) move, the country launched its own cryptocurrency, the Petro, this year. Venezuela’s president just officially made it “legal tender,” meaning it can be used the same way as cash and is accepted as payment by the government.

The Petro aims to be a stablecoin of sorts too, with the government “backing” every coin with a barrel of oil. Again, it’s not clear if this experiment will work, and the country has a bad record financially.

The interesting thing is this almost certainly marks the beginning of a trend.

Stablecoins’ Massive Potential

Stablecoin projects are some of the most promising in the crypto world. They could offer the world an alternative to inflationary fiat currencies, which are usually losing value. And done well, they won’t have the extreme volatility of bitcoin and other traditional cryptos.

This could actually change the world. One day we might be paid our salaries in a stablecoin (or a basket of stablecoins).

I don’t believe stablecoins’ primary challenge will be technological. I’m confident better fundamental currencies can be built with blockchain tech and VC money.

Naturally, stablecoins don’t have the same profit potential as coins like bitcoin. They don’t have the appeal that has been a big part of crypto’s viral success.

But I’m betting those stablecoins that can find a balance between price appreciation and stability will be extremely attractive assets. A truly stable crypto investment would be incredibly useful. And if it has some price increase potential too, that would be great.

We’re going to see some amazing developments in the stablecoin space over the coming years. Clever models will emerge that reward holders, spenders and people who refer friends.

Good investing,

Adam Sharp

Co-Founder, Early Investing

Can a $10 Bill Really Fund Your Retirement? The digital currency markets are delivering profits unlike anything we’ve ever seen. 23 recently doubled in a single week. And some like DubaiCoin have jumped as much as 8,200X in value in 18 months. It’ unprecedented... but you won’t receive any of the rewards unless you put a little money in the game. Find out how $10 could make you rich HERE.

Source: Early Investing

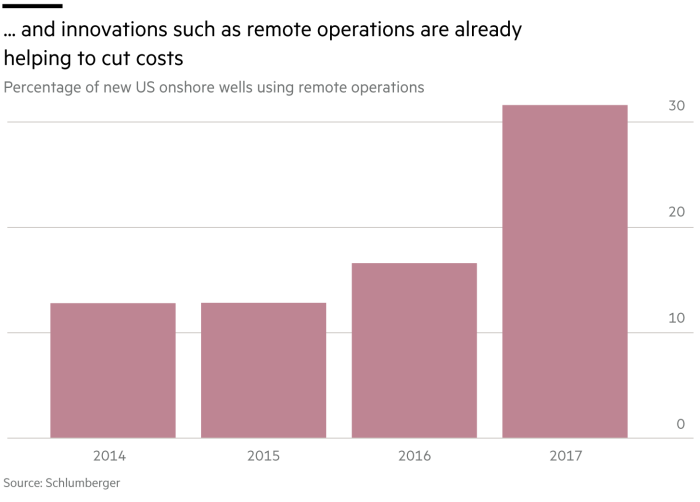

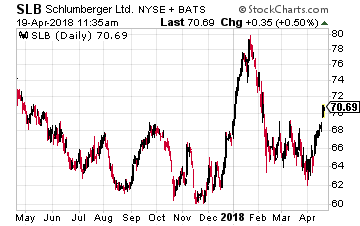

The number one company here is the world’s largest oil field services firm, Schlumberger (NYSE: SLB), which was founded in 1926. A sign of the change in its business since then is the fact that today it has a software technology innovation center that sits at the heart of Silicon Valley.

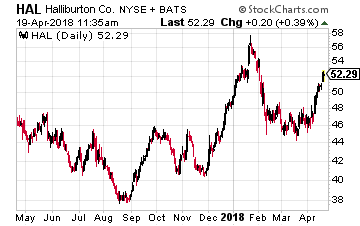

The number one company here is the world’s largest oil field services firm, Schlumberger (NYSE: SLB), which was founded in 1926. A sign of the change in its business since then is the fact that today it has a software technology innovation center that sits at the heart of Silicon Valley. The next company is Halliburton (NYSE: HAL), which is the world’s number two oil field services provider. Like Schlumberger, it is also working with Nvidia on adapting technology for viewing and analyzing seismic data.

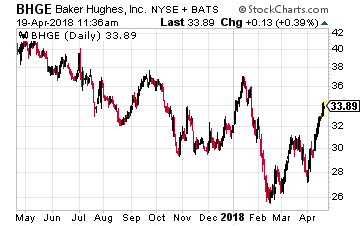

The next company is Halliburton (NYSE: HAL), which is the world’s number two oil field services provider. Like Schlumberger, it is also working with Nvidia on adapting technology for viewing and analyzing seismic data. Finally, there is Baker Hughes (NYSE: BHGE), which is currently 62.5% owned by General Electric. I expect GE to spin this off in the not-too-distant future.

Finally, there is Baker Hughes (NYSE: BHGE), which is currently 62.5% owned by General Electric. I expect GE to spin this off in the not-too-distant future.

But this new tax intended to tax overseas income earned by U.S. technology and pharmaceutical firms and their trademarks and patents has hit closer to home with the railroad company Kansas City Southern (NYSE: KSU), which has a substantial business in Mexico.

But this new tax intended to tax overseas income earned by U.S. technology and pharmaceutical firms and their trademarks and patents has hit closer to home with the railroad company Kansas City Southern (NYSE: KSU), which has a substantial business in Mexico.