I recently interviewed Jeff Clark about using gold as an inflation hedge. Jeff asked why I never write about gold stocks. I own several – time to fess up!

Why don’t I write about gold stocks? I don’t recommend stocks, I know my limitations.

You can make a lot of money with gold stocks, but you better know what you are doing.

One of the top metals analysts is former Casey Research colleague Lobo Tiggre. He wrote for Casey under the pen-name Louis James.

One minute he would be traveling the world with his hardhat looking at explorers, then in the next, he would be in established mines looking at their economics. Lobo’s the real expert – and he agreed to an interview.

DENNIS: On behalf of our readers, thank you for taking the time for our education. Before we get into stocks, I want to discuss how gold is different.

Unlike most commodities, which are consumed, gold is primarily used as a store of wealth. When oil prices rise, demand slows – industry looks for other sources of energy. Sometimes can’t higher gold prices create additional demand? Lobo, am I correct?

LOBO: You’re partially right, Dennis. Gold is a safe-haven asset. It rises when people see rising risk (economic, political, or even on the personal safety risk). But the gold price is also seen as an indicator. Rapidly rising gold prices can act as a warning signal, creating more demand for gold.

In a gold mania, fundamentals can be overtaken by momentum, as happened in 1980 and 2011, but that’s rare.

Higher gold prices can cause increased demand for gold, but oddly enough, so can lower prices. In recent years when gold sold off in the West, instead of tanking after breaking below a “psychologically important price level,” it rebounded because the “sale” spurred a surge of buying in Asia.

There has been a massive transfer of physical gold from West to East over the last 10 years. Official Chinese reserves alone have doubled over this time, not including all the gold private individuals in China have socked away.

This win-win outlook should be very reassuring to gold investors. It tells us we should do well, whether safe-haven demand drives gold sharply upward or not.

| Help keep us on the air!We’re committed to keeping our weekly letters FREE.

It’s humbling when readers suggested we add a donations button to help us offset the costs. It’s strictly voluntary – no pressure – no hassle!Click here for more information. And thank you all! PS: You do not have to sign up for PayPal to use your credit card. |

DENNIS: I look at mining companies in different categories.

The first is exploration companies, sometimes called junior mining companies. They may be boom or bust; if/when they find gold, the payoffs can be enormous.

The second group is the big boys, they have millions invested and harvest gold all over the world.

The third group doesn’t really mine, but rather provide capital for mining companies. In addition to interest income, they also receive royalties.

LOBO: Well, there’s no “official” or uniformly accepted way of categorizing mining companies, there are some small producers, however, your explanation is as good as any.

DENNIS: I know you have recommended junior mining companies that produced tremendous rewards. What do you look for?

LOBO: When I first started, solid people with great track records, highly prospective targets, and money to explore them, seemed worth a shot. Sometimes we got lucky and landed 1000% gains or better, but too often we did not. Even the very best explorers in the business routinely struck out. A general industry guideline is only one out of 300 discoveries ever becomes a mine. Many good geologists go through thousands of targets and may never make a significant discovery in their entire career.

Today, I am extremely selective with stringent criteria. I’ll speculate on early stage exploration – but only if the company has not only great people and targets, and either revenue of some kind of joint venture partners paying for all that super-high-risk work. I also look for more advanced exploration plays, in which the company has already made a discovery, and it looks to me like a real winner.

One of my favorite speculations is in the pre-production sweet spot. At this stage, there’s no exploration risk; the discovery has already been made. There’s technical risk, but only about 5% of first-time mine builders fail to build their mines.

I’ve seen companies appreciate over 800% from the time they started building their mine until the time they poured their first bar of gold or silver. Silvercorp (SVM) was an example of this sort of extraordinary gain when it built its first silver mine in China back in 2006.

A note of caution; while 95% of first-time mine builders succeed at building their mines, not all deliver positive share price results for investors. In the end, all experience extreme volatility along the way. Traditional stop losses would have been triggered in every case, sometimes causing the investor to sell at a loss.

| The junior mining/exploration space should always be considered as a realm for speculators, not investors protecting a nest egg. |

Personally, I try to invest the money I need cautiously and speculate only with money I can afford to lose.

DENNIS: What do you look for in the big mining companies?

LOBO: I start with the standard metrics: Price to Earnings Ratio (P/E), dividend yield, Earnings Per Share (EPS), Free Cash Flow (FCF) and such. I look for companies that manage to keep growing and delivering net income.

Operationally, growth is key. Mines are depleting assets. If a miner doesn’t have growth on tap, it’s going to shrink. You must discover or buy more, or you mine yourself out of business!

The tricky variable is political risk, which can change in an instant. Countries that are solidly pro-mining can go off the deep end for many reasons; an unfortunate election, a fiscal crisis, or a mine accident in some other part of the world. Generally, they increase taxes and regulations on once-profitable mines. It takes some work, but it’s essential to stay ahead of the curve on this.

Even the biggest mining companies can be extremely volatile. For example, In 2008 Teck Resources (TECK) dropped from about $50 per share to just over $3. While it was a market-wide crash – almost 94% is scary! In two years the stock rebounded to over $60 per share. The rout was an opportunity for the most courageous among us.

Gold stocks, even in the biggest and best companies in the world, are always going to be much more volatile than blue-chip stocks most investors are used to. Different strategies and risk tolerance are required.

DENNIS: The third group is royalty companies. What should an investor look for here?

LOBO: I love the royalty space. These companies get paid based on the top line of a miner’s production. Investor’s profit from the price of gold/silver without the risk of discovering and mining it. You can do well, but don’t expect the kind of extraordinary gains that a junior mining company many produce.

In addition to sound company metrics, I look for a good dividend and stock with a track record of rising by some multiple of the movements in gold prices. If gold goes up 1% or 2% in a week, I’d like to see the royalty company’s shares rise 4% to 10%. This happens – but again, it happens when gold drops as well.

| If your only investment goal is to protect your nest egg, frankly, there isn’t a gold stock in the world for you. The prudent thing to do is to buy gold itself, which will hold some level of value no matter what happens. |

DENNIS: Lobo, can you tell readers what you are doing and how they can find you?

LOBO: While I’m greatly appreciative of what Doug Casey taught me, I no longer work for Casey Research. In 2015, to avoid conflicts of interest company policy was changed. I couldn’t buy the stocks I wrote about; putting my money where my mouth was.

Today I foresee a major commodities boom; particularly precious metals. I want to participate. And my readers want me to be in the trenches, suffering and celebrating the consequences of my work alongside them.

I’ve started my own newsletter – www.IndependentSpeculator.com. We provide educational material for investors of all levels. Our monthly newsletter outlines the actual speculative investments I’m making. I post evidence of all my trades, including capital committed, prices bid, fees paid, everything. The goal is 100% transparency.

“Independent Speculator”, is what we are all about. I’m truly independent; none of the companies I write about pay me to do so. Investments are highly speculative and should only be considered by people with capital to allocate to speculation. My goal is to make money for my readers and myself.

DENNIS: Today you heard from a true expert. Lobo, thank you for your time.

| NOTE: I have no financial arrangement with Lobo of any kind. I’m happy to promote his new venture in exchange for him sharing his expertise with our readers. |

LOBO: My pleasure, Dennis.

Dennis here. I currently own stock in 3 mining companies and 2 royalty companies, all paying dividends. One is up 158%, and the other four are down about 60%. I hope I never have to sell my

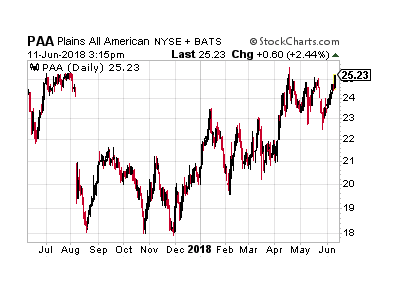

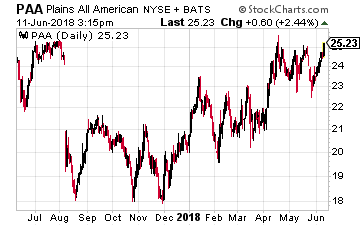

Plains All American Pipeline LP (NYSE: PAA) is a $30 billion enterprise value MLP focused on crude oil pipelines and terminals. Plains has focused on the Permian and is investing $1.6 billion in growth capital to expand its crude oil gathering and pipeline takeaway capacity in the Basin.

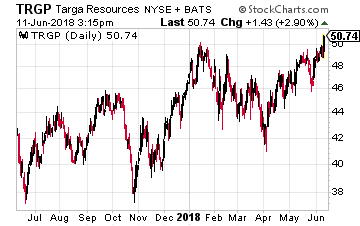

Plains All American Pipeline LP (NYSE: PAA) is a $30 billion enterprise value MLP focused on crude oil pipelines and terminals. Plains has focused on the Permian and is investing $1.6 billion in growth capital to expand its crude oil gathering and pipeline takeaway capacity in the Basin. Targa Resources Corp (NYSE: TRGP) is an $11 billion market cap energy midstream company focused on the gathering, processing, transport and export of natural gas liquids (NGLs). These energy liquids are a big part of the value process of energy production in the Permian, North Texas and Oklahoma.

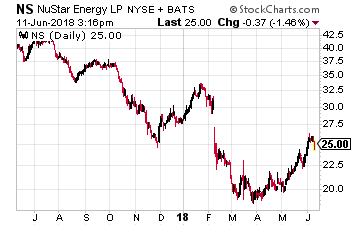

Targa Resources Corp (NYSE: TRGP) is an $11 billion market cap energy midstream company focused on the gathering, processing, transport and export of natural gas liquids (NGLs). These energy liquids are a big part of the value process of energy production in the Permian, North Texas and Oklahoma. NuStar Energy LP (NYSE: NS) is an MLP whose business operations are a balance of pipelines and storage facilities for both crude oil and refined energy projects. In May 2017 the company acquired an integrated crude oil and transport system in the heart of the Permian Basin.

NuStar Energy LP (NYSE: NS) is an MLP whose business operations are a balance of pipelines and storage facilities for both crude oil and refined energy projects. In May 2017 the company acquired an integrated crude oil and transport system in the heart of the Permian Basin.

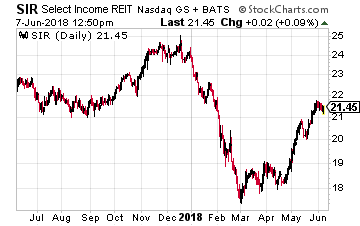

Select Income REIT (Nasdaq: SIR) owns 100 buildings, containing 17 million square feet that are 88.7% leased. In January the company spun off its 266 industrial properties into a new REIT, Industrial Logistics Properties Trust (NYSE: ILPT). SIR retained 69% ownership in the new REIT and consolidates the industrial company results to its income statement. Revenue growth is generated by built in rent escalators and the development of raw land industrial properties at ILPT.

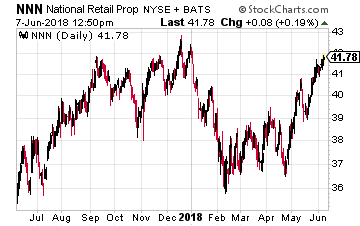

Select Income REIT (Nasdaq: SIR) owns 100 buildings, containing 17 million square feet that are 88.7% leased. In January the company spun off its 266 industrial properties into a new REIT, Industrial Logistics Properties Trust (NYSE: ILPT). SIR retained 69% ownership in the new REIT and consolidates the industrial company results to its income statement. Revenue growth is generated by built in rent escalators and the development of raw land industrial properties at ILPT. National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. The top types of businesses are convenience stores, casual and fast food restaurants, auto service shops, fitness outlets, movie theaters and auto parts stores. When acquiring new properties NNN focuses on buying stores with great locations over high quality tenants. The good locations mean that the tenants will be successful and be able to pay the rents. Also, if a tenant does leave, it will be easier to re-lease a property in a great location.

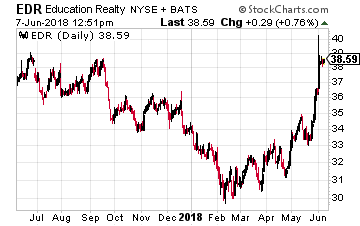

National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. The top types of businesses are convenience stores, casual and fast food restaurants, auto service shops, fitness outlets, movie theaters and auto parts stores. When acquiring new properties NNN focuses on buying stores with great locations over high quality tenants. The good locations mean that the tenants will be successful and be able to pay the rents. Also, if a tenant does leave, it will be easier to re-lease a property in a great location. EdR, Inc. (NYSE: EDR) develops, acquires, owns and manages collegiate housing communities located near university campuses. Currently the company owns 79 (up 13 in the last year) communities in 50 different university communities. These communities are located 1/10th to 1/3rd of a mile from the campuses. The college housing business model has produced stable revenue growth, averaging 3.7% per year same store gains. Development and acquisitions boost that core growth rate.

EdR, Inc. (NYSE: EDR) develops, acquires, owns and manages collegiate housing communities located near university campuses. Currently the company owns 79 (up 13 in the last year) communities in 50 different university communities. These communities are located 1/10th to 1/3rd of a mile from the campuses. The college housing business model has produced stable revenue growth, averaging 3.7% per year same store gains. Development and acquisitions boost that core growth rate.

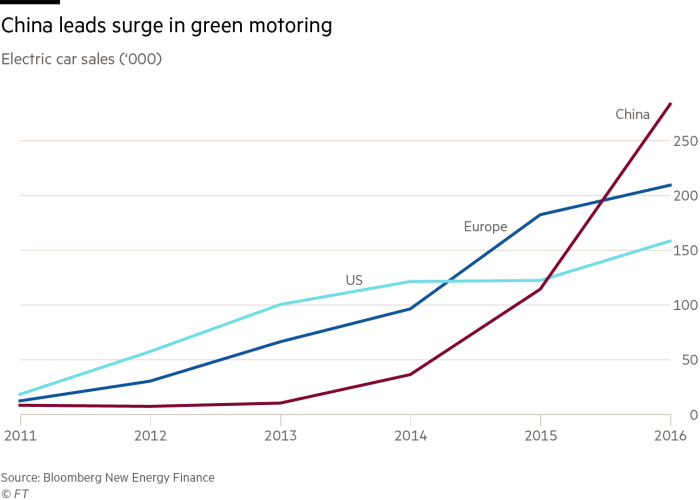

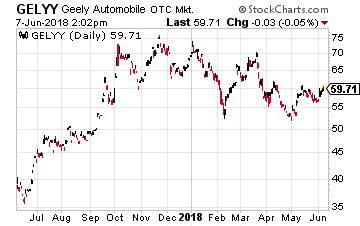

Another quality Chinese vehicle company is Geely Automobile Holdings (OTC: GELYY), which is also down 13% year-to-date, but is up 66% over the past year.

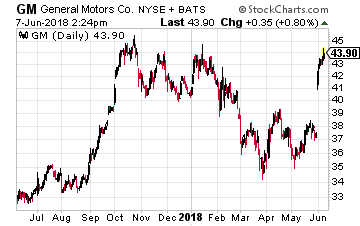

Another quality Chinese vehicle company is Geely Automobile Holdings (OTC: GELYY), which is also down 13% year-to-date, but is up 66% over the past year. Finally, how about the old American standard, General Motors (NYSE: GM)?

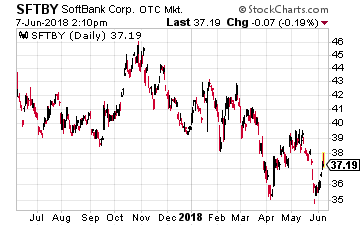

Finally, how about the old American standard, General Motors (NYSE: GM)? And GM looks to be one of the leaders in autonomous vehicles worldwide too. It got a major vote of confidence from Softbank’s (OTC: SFTBY) $100 billion fund, which said it would invest $2.25 billion into GM’s self-driving car unit, Cruise Holdings. The investment values Cruise at $11.5 billion and will give Softbank a 19.6% stake in Cruise.

And GM looks to be one of the leaders in autonomous vehicles worldwide too. It got a major vote of confidence from Softbank’s (OTC: SFTBY) $100 billion fund, which said it would invest $2.25 billion into GM’s self-driving car unit, Cruise Holdings. The investment values Cruise at $11.5 billion and will give Softbank a 19.6% stake in Cruise.