I was not supposed to be sharing my favorite income strategy (for weekly payouts) with you today. But I convinced my publisher to make an exception – so please take advantage of his rare act of leniency and read this carefully today.

As you probably know I’m the rare “income guy” who thinks that these “elevated” Treasury yields are still a joke. As I write, the 10-year IOU from Uncle Sam is rallying back towards 3%. Is anyone who is not already rich retiring off of these yields?

A 3% yield on a $1 million portfolio generates just $30,000 per year before taxes. A better idea is my now-famous “No Withdrawal” Portfolio, which currently pays a blended 7.7% yield. Put the same million bucks into it, and you’ll receive $77,000 per year in dividends – with potential gains upside to boot:

BUT – what if you don’t have $1 million? Or need more in income than $77,000 annually? That’s where my dividend accelerator comes in.

Don’t Reach for Dicey Dividends – Accelerate Secure Ones, Instead

Many income investors get desperate and reach for double-digit yields. Unfortunately most are dividend traps. (If these payouts were safe, the stocks or funds would already be in our No Withdrawal Portfolio!)

Let’s pick on Triangle Capital (TCAP), a business development company (BDC) that pays 10.2% today. On the surface, this looks great. Unfortunately for each dividend payment investors receive, they tend to lose more in price erosion:

TCAP: It’s a (Dividend) Trap!

Low yields on blue chip stocks make yield seekers thirsty enough to consider traps like TCAP. Fortunately, there’s a better way – and it’s as easy as buying or selling any blue chip stock.

Rather than “buying and hoping” that a modest paying stock will also go up in price, I prefer to accelerate its 1% or 2% yield into weekly payouts that annualize to 20%+. Here’s how.

Safer – and More Profitable – Than Buying Stocks Outright

When I mention stock options to “basic” investors, they tend to have one of two levels of experience:

- They stay away from options (perceiving them as a form of gambling), or

- They buy options (which is a form of gambling).

Few are aware of the third – vastly superior – option:

- Selling options to the gamblers, banking the premiums as weekly income.

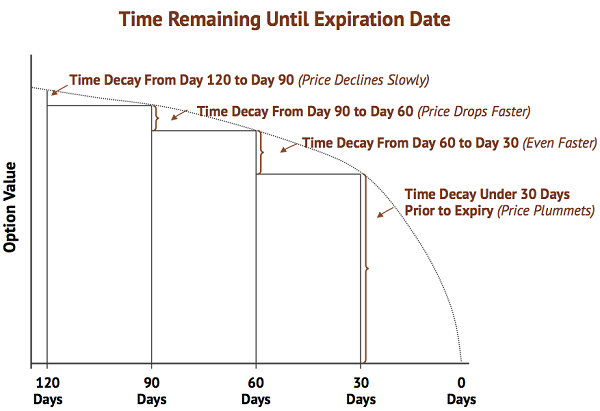

Why is it better to be a seller than a buyer? The real question is when – it’s better to be a seller than a buyer when options are within 30 days of expiration.

We have a phenomenon called “option decay” to thank. Stock options, after all, have two dimensions:

- Their strike price – the level the stock needs to be for the option to pay, and

- Their expiration date – the time-based deadline for this to happen.

Put options are bets that a stock will decline in price. Call options are bets on a bullish move higher. Both “decay” in price as they get closer to expiration, and their prices decline faster and faster the closer we get. As a seller, I like to catch the last 30 days – which really tips the odds in my favor:

I also prefer selling put options on high quality dividend payers and growers. And, if you choose right (and I’ll show you how in a minute), you’ll be amazed with the level of payouts that you can generate with this safe strategy (I’m talking about 20%+ cash returns per year).

It’s safe because we only use it on stocks we’d be happy to own outright. Selling puts on the best blue chip dividend payers gives us a “heads we win, tails we win” outcome:

- If the put expires worthless (the most likely scenario), then we bank the put premium free and clear without ever having to buy the stock.

- If the stock declines below the put price, then we still keep our premium – and we get to purchase the stock at a discount.

Once you learn this strategy, you’ll probably never want to buy a stock outright again. After all, why would you want to pay the “list price” when you can lock in a discount – or simply use the strategy to accelerate pedestrian yields to 20% or higher!

Here’s an Example Using an Excellent Utility Stock

“First-level” thinking says that utility stocks sink as interest rates rise. Since these “bond proxies” are nothing more than pretty yields to many investors, their payout attractiveness wanes as competition from fixed income rolls in.

This may be true for stalwarts like Duke Energy (DUK) and Southern Company (SO), which are merely giving their investors token annual raises. Their dividends have climbed only 12% and 7% respectively over the last three years combined.

These stocks are indeed basically bond proxies.

But not all utilities should be sold in advance of rising rates. There’s a notable exception that leaves these tortoises (and their middling dividends) in the dust.

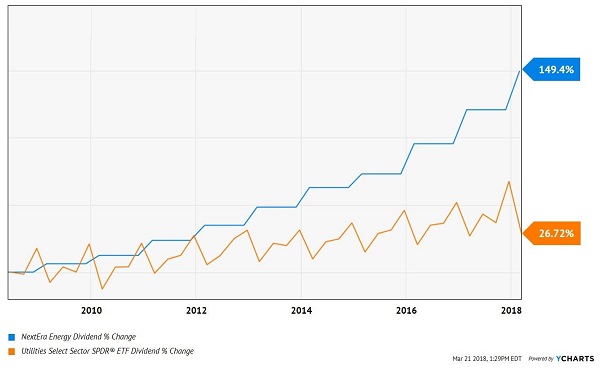

NextEra Energy (NEE) is the largest developer of renewable energy in North America. The firm has been a fast grower for decades. It’s increased its dividend for 23 straight years.

And these have been meaningful raises – NextEra has shown up its peers with 149% dividend growth over the last decade (versus just 26% for the utility sector’s widely marketed ETF):

Why NEE is the Best Utility to Buy

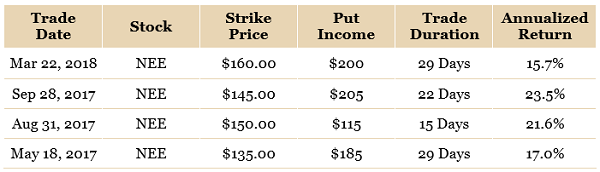

Thanks to the firm’s most recent payout raise, it now shovels out $1.11 per share per quarter (for 2.7% yearly). But we can accelerate this payout to 19.5% yearly.

That’s exactly what my Options Income Alert subscribers and I have done four times in the last fourteen months. My readers who sold 10 contracts per trade banked $7,050 in cash payouts without ever having to buy NEE!

$7,050 in Payouts in Just 4 Weeks

We turned NEE into our “personal dividend ATM.” We simply tapped it anytime I saw a setup that I liked – and then placed the put premiums directly on our pockets.

NEE’s Put Premiums: Weekly Payouts Averaging $1,762.50

And again, these trades were as simple as buying or selling any stock (or CEF). We simply sold put options on NEE instead of buying or selling the stock itself.

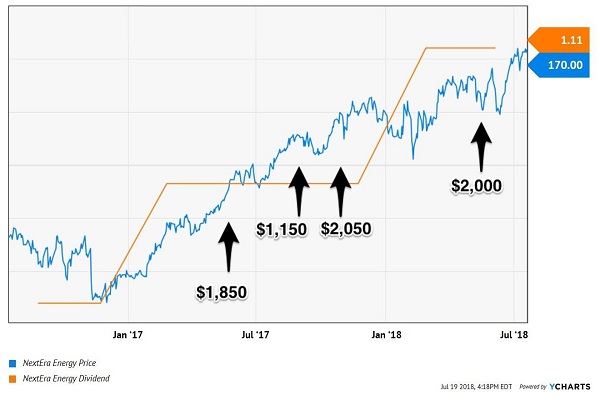

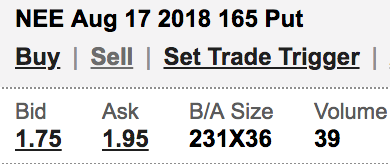

It was just a different click of the mouse. And if you’re interested in turning NEE into your personal ATM, then this click will net you $1,850 in two-and-a-half short weeks:

Click Here for $1,850 in Payouts

Can I give you a hand with the specifics? If so, I have some easy-to-follow instructions that you can get started with today.