Many income investors own shares of the iShares Mortgage Real Estate Capped ETF (NYSE: REM) as a stock market investment that pays a high (just over 10%) current dividend yield. The problem with REM is that it holds a lot of the highly leveraged, dangerous to your wealth, residential mortgage-backed securities, or as they are regularly referred to – MBS REITs.

The REM share price has tumbled over the last two months, dropping by 10% before regaining about half that loss. That drop indicates that for many companies in the fund’s portfolio, higher interest rates and a flat yield curve are a danger to profits and continued dividend payments.

A better option for the high-income focused investor is to build a portfolio from the financially strongest stocks out of the REM holdings list.

According to the tax rules that govern their operation, a REIT can own real estate property or participate in the financing of real estate assets. REITs that focus on owning real estate are referred to as equity REITs, while those that focus on the mortgage side of real estate are called finance REITs.

The finance REIT side of the REIT universe typically carries much higher dividend yields, which are very attractive to income-focused investors. For comparison, REM currently yields 10% while the largest equity REIT ETF, the Vanguard REIT Index Fund (NYSE: VNQ), yields 4.8%.

The finance REIT side of the REIT universe typically carries much higher dividend yields, which are very attractive to income-focused investors. For comparison, REM currently yields 10% while the largest equity REIT ETF, the Vanguard REIT Index Fund (NYSE: VNQ), yields 4.8%.

A significant number (I would hazard a guess of most) of finance REITs employ a business model that involves owning government agency guaranteed MBS and leveraging their MBS portfolios to turn the 4% bond yields paid by these safe MBS into the cash flow to pay a double-digit dividend yield.

Changing interest rates at either the short or long end of the yield curve will eat into one of these company’s cash flow generation ability. If you look at their histories, most are now paying dividends that are much lower than just a few years ago.

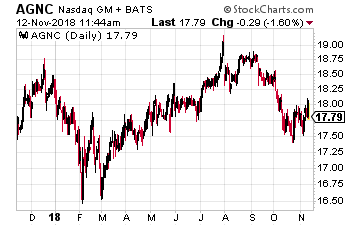

For example, consider the case of one of the larger and more popular agency MBS REITs, American Capital Agency Corp. (NASDAQ: AGNC), which yields an attractive 12%. Digging deeper shows the current dividend rate at just 43% the size of the dividend AGNC investors were earning in 2012. Put another way, the AGNC dividend has been cut by more than half over the last 6 years. With the Treasury yield curve continuing to flatten, I would not be surprised by another dividend cut soon.

For example, consider the case of one of the larger and more popular agency MBS REITs, American Capital Agency Corp. (NASDAQ: AGNC), which yields an attractive 12%. Digging deeper shows the current dividend rate at just 43% the size of the dividend AGNC investors were earning in 2012. Put another way, the AGNC dividend has been cut by more than half over the last 6 years. With the Treasury yield curve continuing to flatten, I would not be surprised by another dividend cut soon.

As a fund that owns a portfolio of 40 different finance REITs, the REM dividend has shrunk from $7.43 per share paid in 2013 to most recent trailing four quarters run rate of $4.41. That is an average 9.2% per year shrinkage of the dividend. Historically, despite the high dividend yield, REM has generated a negative average annual total return. That return is further reduced by the tax bite on the dividends paid. For long-term, income focused investors REM is a fund to avoid.

To build a min-REM portfolio that gives a higher yield and does not destroy principal value, the strategy is to buy those finance REITs that have not been slashing dividend rates because their business models failed to adjust for changing interest rates. Here are five stocks out of the REM holdings that have not reduced dividends in the last five years:

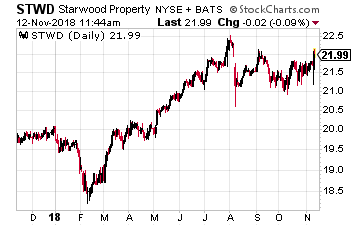

Starwood Property Trust, Inc. (NYSE: STWD) is a commercial mortgage lender. Starwood has a diverse business which includes a portfolio of commercial mortgages, an energy infrastructure loan business and holdings, a commercial mortgage servicing company and some commercial property investments.

Starwood Property Trust, Inc. (NYSE: STWD) is a commercial mortgage lender. Starwood has a diverse business which includes a portfolio of commercial mortgages, an energy infrastructure loan business and holdings, a commercial mortgage servicing company and some commercial property investments.

The commercial loan portfolio is all adjustable rate mortgages, which means income will go up in a rising rate environment.

STWD currently yields 8.9%.

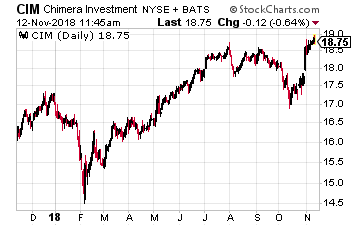

Chimera Investment Corporation (NYSE: CIM) aims to provide attractive risk-adjusted returns by investing in a diversified investment portfolio of residential mortgage securities, residential mortgage loans, real estate-related securities and various other asset classes.

Chimera Investment Corporation (NYSE: CIM) aims to provide attractive risk-adjusted returns by investing in a diversified investment portfolio of residential mortgage securities, residential mortgage loans, real estate-related securities and various other asset classes.

The company primarily owns non-investment grade MBS and has not reduced its dividend since early 2012. This is an area of mortgage loans that requires a higher level of analytical skills.

CIM currently yields 10.6%.

MFA Financial, Inc. (NYSE: MFA) owns a diversified portfolio of mortgage securities. This is the most traditional agency MBS owning REIT on this list. However, it has avoided the rising interest rate challenges that has resulted in deep dividend cuts from its peer REITs.

MFA Financial, Inc. (NYSE: MFA) owns a diversified portfolio of mortgage securities. This is the most traditional agency MBS owning REIT on this list. However, it has avoided the rising interest rate challenges that has resulted in deep dividend cuts from its peer REITs.

The company invests in residential mortgage assets, including Non-Agency MBS, Agency MBS, and residential whole loans.

The MFA dividend has been stable over the last seven years and has not changed for the last five years.

MFA yields 11.2%.

Apollo Commercial Real Est. Finance Inc. (NYSE: ARI) is a real estate investment trust that primarily originates and invests in senior mortgages and mezzanine loans collateralized by commercial real estate throughout the United States and Europe.

Apollo Commercial Real Est. Finance Inc. (NYSE: ARI) is a real estate investment trust that primarily originates and invests in senior mortgages and mezzanine loans collateralized by commercial real estate throughout the United States and Europe.

Commercial real estate loans typically are adjustable rate, which gives a huge advantage to REITs doing commercial loans compared to those operating in the residential mortgage space.

The ARI dividend has been steady for the last three years. There is potential for dividend growth, and the company will increase the payout when business conditions allow it.

The shares currently yield 9.7%.

Blackstone Mortgage Trust (NYSE: BXMT) is a pure play originator of commercial real estate mortgages. The company focuses on larger loans, where competition for the business is less fierce.

Blackstone Mortgage Trust (NYSE: BXMT) is a pure play originator of commercial real estate mortgages. The company focuses on larger loans, where competition for the business is less fierce.

This REIT’s ace in the hole is the relationship with and management provided by The Blackstone Group LP (NYSE: BX).

This large cap asset management company uses its resources and contacts to provide great loan leads to the REIT.

BXMT currently yields 7.5%.

Out of the 40 stocks owned by the REM ETF, that is what I found: five that have produced solid five-year returns and no significant reduction in their dividends. With this group, you would have earned more than double the REM total return. More importantly, these give a much higher level of safety to dividend payments going forward.

Starting today you can stop worrying about the market and instead fundamentally transform your income stream from a string of near misses to a steady, reliable flow of income right into your bank account.