The Turing Test, which is considered one of the best ways to identify artificial intelligence (AI), requires that a human being is unable to distinguish a computer from another human being when asking both of them the same questions. It’s a great academic exercise, but not especially helpful in determining which company in the AI area you should invest in.

When it comes to predicting the size of the the “AI market” we find projections for market size in 2025 from well-respected firms ranging anywhere from $37 billion to $1.2 trillion. A large part of the deviation in estimates is due to the lack of clarity in defining AI, and how the technology will benefit companies able to employ AI in their business models.

As Eliezer Yudkowsky, an American writer who has warned on the danger of AI laments, “By far, the greatest danger of AI is that people conclude too early that they understand it.” So here we stand. We don’t know exactly what AI is, we have difficulty defining the market, and we don’t know what the future capabilities of the technology look like.

A Forbes article earlier this month by Kathleen Walch, was actually titled Artificial Intelligence is Not a Technology. Ms. Walch, an AI expert, considers AI to be a “journey” with technology spun off along the way.

While we may have many questions about what AI is, we do know that the two leading countries in terms of AI research are China and the U.S. China has published more research papers on AI, and the government announced last year the country would become, “a principal world center of artificial intelligence innovation.” But, some question the quality of China’s research and most believe the U.S. has a slight lead in the technology.

We also know that many companies are attacking big problems using the current state of AI, and that the technology will have a major impact on our everyday lives. For example, Deere (NYSE: DE) recently bought a company called Blue River Technology. The company uses robots and AI to fertilize, water, and harvest crops. The result is the use of less fertilizer, less water, and better yielding crops. In this way, AI is already being used to prevent pollution, conserve water, and feed more people.

As investors we should also know that one form of AI, machine learning, is already being used by many of the largest companies on Wall Street. Andrew Ng, Stanford professor and founding lead of Google Brain defines machine learning as “the science of getting computers to act without being explicitly programmed.”

Let’s go a just a little further down the machine learning rabbit hole in order to understand where companies plug into the machine learning ecosystem. Machine learning can be broken down into two stages. First, there is the “training” of the computer. This involves providing patterns, e.g. videos, pictures, and any other of a wide variety of data, to the computer and asking it what the pattern is. The computer is allowed to get the answer wrong over and over, until eventually getting it right. In this way the computer “learns” what information presented in a specific manner means to humans.

The second stage is “inference”. In this stage the computer takes what it has learned in the training stage and “infers” an answer based on the learning that has taken place. Inferring involves massive amounts of data and must often be done in a split second.

Think of the inference stage in a driverless car. While traveling 55 MPH, surrounded by other cars, a driverless car “sees” a child’s ball roll into the road ahead. The car must simultaneously recognize the fact that it is a child’s ball, determine there is a high probability a child may follow the ball into the street, communicate with the other driverless cars around it what it sees, and then decide whether the best course of action is to brake, change lanes, or take some other evasive action.

Clearly the inference must be fast and correct. One company working to insure inferences are arrived at in a timely manner is:

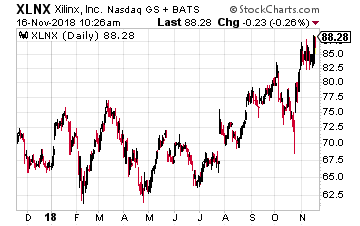

Xilinx (Nasdaq: XLNX)

Xilinx (Nasdaq: XLNX)

Xilinx is known today as the field programmable gate array (FPGA) company. They compete with companies like NVIDIA (Nasdaq: NVDA) that make graphics processing units (GPU). Demand for NVIDIA’s GPUs, driven by video gaming, data centers, cryptocoin mining, and AI, has driven the company’s stock up over 788% from the beginning of 2016 to highs reached earlier this year.

While FPGAs and GPUs both process data, FPGAs are generally faster and use less power, but GPUs are cheaper. When comparing the two options, chiefly cost constraints, in both crypto coin mining and video gaming platforms, has historically GPUs the technology of choice, and in the process powered NVIDIA’s stock skyward.

GPUs are also favored for the “training” stage of machine learning, because speed is not a vital component of training as it is for inference.

But, I believe that growth in the inference market, as a variety of technologies come online in the next few years e.g. 5G, IoT, and driverless automobiles, will concurrently drive sales of Xilinx FPGAs. XLNX grew earnings in its latest reported quarter by 25.37% year-over-year, and is expected to grow full year earnings 16.08%.

The company also recently introduced of a new technology, which is one reason I believe now is a good time to get into the stock. The new chip from Xilinx, which combines FPGA, GPU and CPU capabilities on one chip, may be its ace in the hole.

In October Xilinx CEO Victor Peng introduced a new chip aimed squarely at the inference market. The Adaptive Compute Acceleration Platform (ACAP) chip is code named Everest, and according to Xilinx the chip can “infer” 2x-8x faster than Nvidia’s GPUs, and do so with 4x less energy. The Everest chip is featured in the company’s Versal line of products, short for “versatile” and “universal”.

Mr. Peng took over the CEO position at Xilinx in January after joining the company in 2008 and most recently served as Chief Operating Officer. With the launch of the new more powerful technology, Mr. Peng is already attempting to leap ahead of the competition by changing the company’s branding.

“…we have to say no, we’re not the FPGA company. With ACAP, at the moment nobody even knows what that is – but they will understand over time.” The combination of rising demand for their FPGA product with an aggressive move to expand the new ACAP technology, should put Xilinx in the sweet spot of a coming machine learning boom.

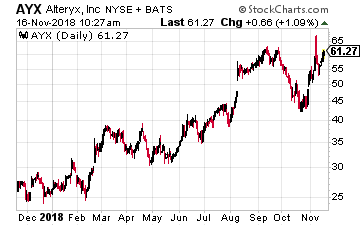

Alteryx (NYSE: AYX)

Alteryx (NYSE: AYX)

While Xilinx makes the hardware necessary for the inference stage, Alteryx uses machine learning to provide the end user with the ability to gather the inference and make it actionable. Alteryx is a “self-service data analytics” company. They provide data processing and presentation software allowing companies to turn data into human consumable presentations and graphs which can be used to make business management decisions.

The Alteryx solution allows customers to combine data from a variety of sources, e.g. warehouse data, combined with customer data, combined with purchasing data, to present a holistic and repeatable picture of business health. The software, which includes various aspects of machine learning, provides insights without the user having to use or know computer code. Easily combining data from a variety of databases, and being able to present a coherent representation of that data, is a major boon to large corporations.

In its recently reported Q3 earnings, CEO Dean Stoecker reported the company grew revenue 59% year-over-year. But, more importantly, sustained net revenue retention, a measure of customers staying with the company and purchasing additional services, was 131%. The company has also grown earnings by over 46% year-over-year as of its latest quarterly report. Analysts are projecting a 5 year average earnings growth rate of 8% going forward.

This marked the eighth consecutive quarter the customer retention number was over 130%. This is important as it shows me that Alteryx is not just good at marketing, but actually has a product that customers want and are using more and more of. Having been able to continuously obtain new customers, while increasingly monetizing current customers, is one of the reasons I believe the stock is a buy here.

Another thing I like about the company’s growth is that they are diversifying their customer base both across industries and across geographies. Their clients now include Cowen and Company, J.Crew, Cisco Systems, McDonald’s and Textron, as well as AkzoNobel Sourcing in the Netherlands, Anheuser in Belgium, and Oxford University Press in the U.K.

As CEO Stoecker stated in the latest earnings call, using Alteryx allows customers to realize “significant time savings and reduced expenses…” An economic slowdown could actually increase demand for the company’s services as cost cutting comes back into vogue.

While Xilinx and Alteryx are already benefiting from the AI revolution, both companies appear poised to accelerate their growth. Whether it be through the introduction of new technology, or the ability to grow and retain their customer base, as the AI technology “journey” progresses to the next stage these companies should be highly considered for your AI portfolio allocation.

Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

Source: Investors Alley

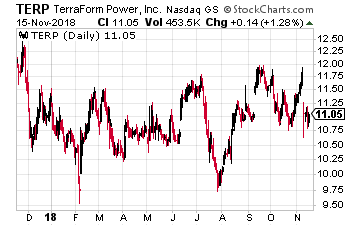

TerraForm Power (Nasdaq: TERP) is a $2.3 billion market cap which owns wind and solar power production assets. The company has gone through significant transformation over the last year. In October 2017 Brookfield Asset Management took over sponsorship of TERP and became a 51% shareholder in the Yieldco.

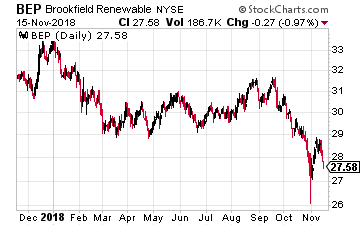

TerraForm Power (Nasdaq: TERP) is a $2.3 billion market cap which owns wind and solar power production assets. The company has gone through significant transformation over the last year. In October 2017 Brookfield Asset Management took over sponsorship of TERP and became a 51% shareholder in the Yieldco. Brookfield Renewable Partners (NYSE: BEP) was operating like a Yieldco long before the term was invented. The company owns 260 hydro power plants, which account for 76% of production. 35% of production is done outside of North America. Also, 90% of power production is purchased on long-term contracts.

Brookfield Renewable Partners (NYSE: BEP) was operating like a Yieldco long before the term was invented. The company owns 260 hydro power plants, which account for 76% of production. 35% of production is done outside of North America. Also, 90% of power production is purchased on long-term contracts. Clearway Energy (NYSE: CWEN) is another Yieldco that recently went through a change of sponsorship. Clearway was started by utility company NRG Energy (NYSE: NRG).

Clearway Energy (NYSE: CWEN) is another Yieldco that recently went through a change of sponsorship. Clearway was started by utility company NRG Energy (NYSE: NRG).