Wednesday morning was all about earnings, with markets jumping on “not bad” earnings out of Apple (AAPL) Tuesday evening, and good news from Boeing (BA) Wednesday morning. And then, Wednesday afternoon was all about the Fed. Chairman Powell seemed to take the Fed, and the fear of rising interest rates, off the table as a potential stumbling block for the market with the FOMC statement and subsequent press conference.

The Fed statement declared that the Fed “will be patient as it determines…future adjustments” to interest rates. The market interpreted that as a green light on the rate front, and added to the earnings gains achieved earlier in the day. On the trade front, high level talks began again between the U.S. and China, but reports from multiple sources say it may be slow going as several in-the-weeds details on intellectual property protection and enforcement must be worked out.

The earnings onslaught continues Thursday when Tuesday Morning (TUES) and YRC Worldwide (YRCW) report before the opening bell. Revenues at trucking company YRCW are expected to rise a few percentage points over last year, with earnings coming in at $.12 per share. Investors will be looking for an update on hiring, with trucking companies across the board citing a lack of qualified drivers. Analysts are predicting a 52% year-over-year rise in Tuesday Morning earnings to $.29 a share when the company reports. The home goods retailer has fallen sharply in the past year from highs around $4 to now trade under $2 per share.

As government agencies catch up on reports not issued due to the government shutdown, the economic numbers will be coming at a rapid pace the next few days. The Challenger Job Cut Report, jobless claims, personal income, and the employment cost index will all be released tomorrow morning. Personal income is expected to have increased .4% in December, and strong consumer spending is expected to continue, ticking up .3%. The core price index, excluding food and energy, is expected to rise .2%, or 1.9% on an annual basis. Chicago PMI and new home sales are also scheduled for release Thursday.

The first day of February will start off with the employment situation numbers, followed by both the PMI and ISM manufacturing indices. Analysts are watching the manufacturing numbers very closely to see if weakness the last few months was only an aberration. The consensus ISM number for January is a tepid 54. Construction spending, consumer sentiment, and wholesale trade numbers will also be released Friday.The November construction number, originally scheduled for release January 3, is expected to show a .2% increase.

Exxon Mobil (XOM), Chevron (CVX), Merck (MRK) and Honeywell (HON) kick off February with earnings Friday morning. Both Exxon and Chevron have bounced, along with oil prices, off of the bottom touched in December. But, on a percentage basis, both large oil companies are trailing the bounce in oil itself. Analysts will be looking for commentary from each company on where they see the price of oil headed, and whether global economic weakness will continue to impact the commodity.

Over the last four months, the U.S. stock market has turned ugly and the fear of an economic recession is in the air. There are a lot of recession predictions coming out in the financial media.

I have seen forecasts for an economic slowdown this year, next year, or further out on the future. Timing of the next recession is for entertainment value only.

However, since the economy does go through growth and recession cycles, you can be fairly positive that the economy will go through a period of negative growth at some time in the future.

To get through an economic downturn, income stock investors want to own stocks that won’t cut their dividend rates when business conditions turn rough. The easy path is to go with Dividend Aristocrat types of stocks, but the trade-of for that level of safety is low yields, with this group currently averaging around 3%.

Today I want to discuss a group of stocks that currently pay yields of 7% to 9% and have business models built to be successful through the full range of economic growth and contraction.

Finance real estate investment trusts (REITs) are companies focused on the finance side of the real estate sector. They originate or own mortgages, mortgage backed securities, or related investment securities. The finance REIT group can be further divided into those that focus on residential mortgages and those which are in the commercial property mortgage business. Interestingly, the former group are risky and a danger to your portfolio, while the commercial finance REITs provide a high level of dividend income safety.

Here are the reasons why a commercial mortgage REIT stock tends to be a solid dividend income investment.

Most commercial REITs are mortgage originators and keep the loans in their portfolio. This allows these companies to use less leverage to get attractive returns on capital.

Most commercial mortgage loans have adjustable interest rates. A commercial REIT can match its borrowings to its loan portfolio and generate steady returns through both ups and downs in market interest rates.

Commercial REITs lend at very conservative loan-to-value ratios. This means property owners will be highly motivated to keep making their mortgage payments if they want to protect their equity. If the REIT forecloses on a property, its likely the real estate can be flipped for an amount greater than the outstanding loan balance.

Here are three commercial mortgage REITs that are well run, and the stocks carry attractive yields.

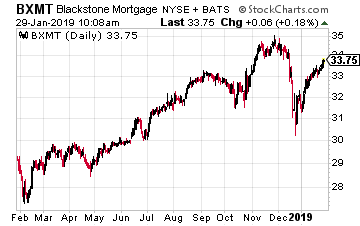

Blackstone Mortgage Trust (NYSE: BXMT) is a REIT that makes mortgage loans on commercial properties. They make loans up to $500 million on a single property, which puts them in a very small group of financial companies that will write very large loans on commercial properties.

The commercial mortgages issued by Blackstone Mortgage are retained in the company’s $13.8 billion investment portfolio. This is a conservatively managed business, with an average loan-to-property value of 62% and 2.3 times debt to equity leverage. Income is the interest earned from the mortgage portfolio minus the cost of the debt.

The portfolio is 95% floating rate loans, with debt rate matched to each loan. The result is that as interest rates increase, so will Blackstone’s profits.

BXMT currently yields 7.4%.

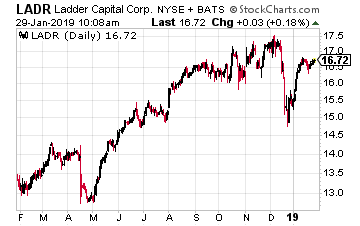

Ladder Capital Corp (NYSE: LADR) is the only commercial finance REIT listed here that is internally managed. Management also owns 12% of the stock.

Ladder has a three prong investment strategy where it owns a portfolio of commercial loans, a portfolio of commercial mortgage backed securities, and it owns commercial real estate. The balance sheet loan portfolio accounts for 76% of the total assets.

In contrast to BXMT, the average loan size for Ladder Capital is $20 million. Total company assets are $6.4 billion, which includes a $1.2 billion real estate equity portfolio. The $4.2 billion loan portfolio has a 68% loan-to-value.

The current dividend is well covered, at just 66% of core EPS.

LADR currently yields 8.3%.

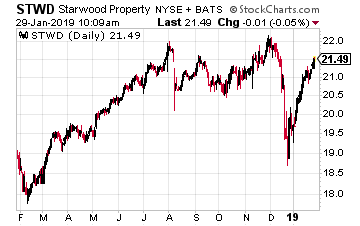

Starwood Property Trust (NYSE: STWD) is another commercial finance REIT. It originates mortgage loans for commercial properties, such as office buildings, hotels, and industrial buildings.

Starwood has two commercial lending businesses. One is to make large dollar loans to retain in its portfolio. The company also operates a fee-based CMBS origination business. The $8.0 billion commercial loan portfolio has a 62% LTV.

To further diversify the company has acquired a portfolio of stable returns real estate assets and has added an infrastructure lending arm. The final piece of the pie is a special servicing division, which will turn very profitable if the commercial real estate sector experiences a downturn. Large commercial loans account for 55% of net earnings. The diversified businesses bring in the balance.

Investors can expect to earn the dividend, which currently gives the shares a 9.5% yield.

What a run! The S&P 500 is up 5.5% for January, and higher by a hefty 12.7% since hitting a multimonth low in late December. Both are unusually big gains given the limited amount of time stocks have had to dish them out.

The rally, however, has left some stocks vulnerable to a pullback, while the names left out of the marketwide advance have been exposed as perpetually, habitually weak. Both groups are likely to lose ground — or lose more ground — no matter what lies ahead. But should the broad market falter here, these equities could really lose some ground.

With that as the backdrop, here’s a rundown of 10 stocks to sell as soon as possible. They’re either overextended, in unstoppable downtrends or have a history of poor February performances. In no particular order…

Xilinx (XLNX)

Up 62% since the end of 2017, and up 28% this year alone, the momentum that Xilinx(NASDAQ:XLNX) has exhibited is intoxicating. Unfortunately, it probably wasn’t built to last.

XLNX stock jumped 18% last Thursday in response to an incredible third-quarter report. The chipmaker has made the most of the advent of 5G, and said it expects more of the same kind of growth for the foreseeable future. Investors were still buying in on Friday.

As of Monday, though, the sheer weight of the oversized gain and the gap left behind on Thursday are forcing traders to rethink everything about this name and its forward-looking P/E of 28.5. The good news, past and projected, is now priced in, and then some.

Mondelez International (MDLZ)

Mondelez International (NASDAQ:MDLZ) hasn’t earned a spot in a list of stocks to sell because it’s overextended … quite the opposite actually. Although it has moved higher with the market since late December, it has suspiciously lagged behind. A look back over the course of the past couple of years, in fact, reveals Mondelez remains more likely to make lower highs and lower lows than not.

Investors just don’t see the company overcoming its core problems anytime soon.

Besides, February is rarely a good month for MDLZ stock. On average it loses a percentage point for the month ahead, and even in a good year, shares fall short of breaking even in February.

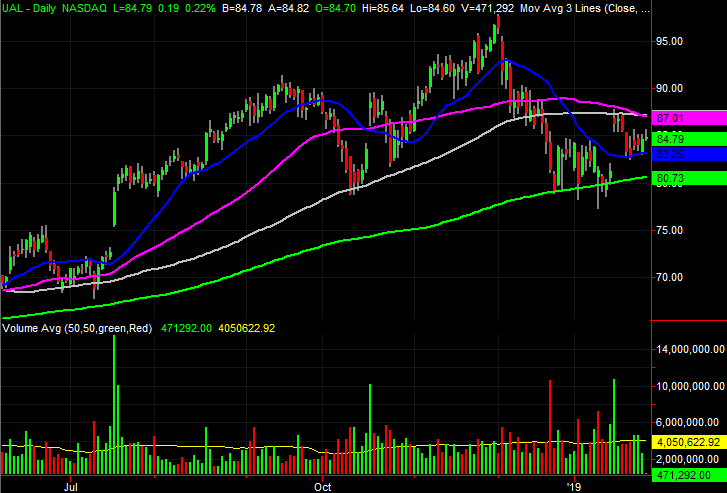

United Continental Holdings (UAL)

United Continental Holdings (NASDAQ:UAL) is another name that, for seasonal reasons, struggles during the second month of the year. On average, UAL stock loses more than 6% in February, and nothing about its performance so far in 2019 suggests the airline stock will be a screaming exception to the norm.

Admittedly, it’s not an outlook that jibes with the recent headlines. Just a few days ago, United Continental capped off an outstanding 2018 with a fourth-quarter earnings and revenue beat.

The headwind isn’t about reality though. It’s about perception. And right now, between an ongoing tariff war, a government shutdown and rebounding oil prices, the market is at least a little worried about the current quarter’s likely results.

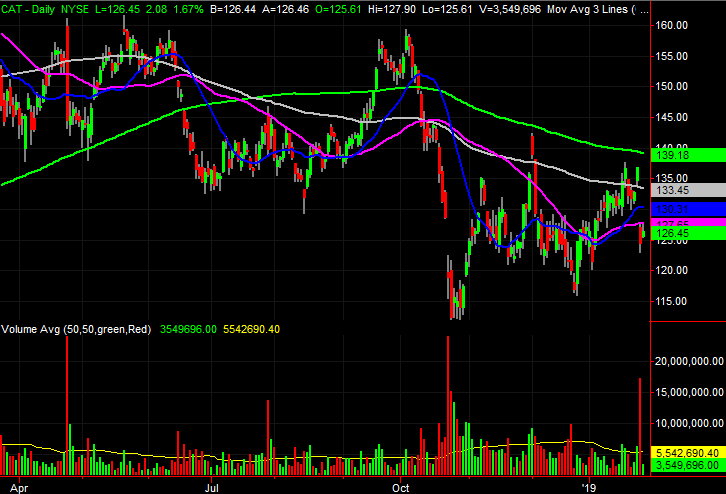

Caterpillar (CAT)

Heavy machinery maker Caterpillar (NYSE:CAT) is in a similar boat. That is, the impact of the trade war with China isn’t exactly taking a massive toll on the company’s bottom line. But, as long as the company is able to say steep tariffs — coming and going — are presenting problems, investors will assume the worst.

And that’s exactly what Caterpillar did with its fourth-quarter report posted on Monday morning. While stopping short of outright blaming it on the war of tariffs and the subsequent economic slowdown in China, the company did concede weakness in China was the cause for the 4% slump in sales for its Asia Pacific arm.

Though CAT stock fell measurably on the report, in the grand scheme of matters, they weren’t terribly shocked. Caterpillar stock is still just trending lower from its early 2018 peak, and there’s little on the radar that might reverse that trend in the coming month.

Exact Sciences (EXAS)

Exact Sciences (NASDAQ:EXAS) has been a champ of late, rallying nearly 60% from its late-December low, and up more than 70% over the course of the past twelve months.

EXAS stock, however, is a name with a history of major ebbs and flows. The big move we’ve seen since Dec. 26 has been made two, and arguably three, times since early 2018, and in each case a huge swath of that gain was given back. It’s unlikely this time will pan out differently. It’s just a habit this cancer diagnostics stock has developed.

Conversely, though due for a sizeable setback soon, the pattern Exact Sciences has developed also says it would be a compelling buy after a tumble.

Alphabet (GOOG, GOOGL)

It’s difficult to bet against the company that essentially owns the gateway to the internet. But, add Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) to your list of stocks to sell before getting too deep into the month of February. On average, GOOGL shares lose a little more than 2% during the second month of the year, and more than half the time it loses ground in February.

It doesn’t appear to be in any major technical trouble right now, but it rarely does in late January.

As was the case with Exact Sciences stock though, any dip from here could be a buying opportunity. GOOGL stock tends to start recovering in March or April to kick off a phenomenal second half of the year.

Illumina (ILMN)

Illumina (NASDAQ:ILMN) is another name that’s suspect simply because it has failed to rebound with the rest of the market.

Of course, the doubters had some help coming to their lackluster conclusions. In early January, the company cautioned investors that while its fourth-quarter revenue would be better than expected, 2019’s sales wouldn’t. CEO Francis deSouza was willing to offer 2019 earnings guidance slightly in excess of analysts’ estimates, but for a stock priced at more than 40 times its forward-looking earnings estimates, investors need more assurance the premium they’re paying is justified.

The fiscal outlook might be changed after Tuesday’s post-close report. But, with ILMN stock already below all of its key moving average lines and in a well-framed downtrend, investors are hinting they’re ready to see the glass as half-empty.

Fiserv (FISV)

The knee-jerk reaction to the news that Fiserv (NASDAQ:FISV) would be acquiring First Data(NYSE:FDC) was a decidedly bearish one. Shares fell as much as 8.6% on Jan. 18, with many shareholders convinced the company was overpaying for an asset it didn’t exactly need. Things took a dramatic turn beginning that very day though. The intraday loss was cut in half, and as of Tuesday FISV stock was 22% above the low made on Jan. 18. As it turns out, investors love the prospect of the pairing after all.

Still, the big move is overdone. As of Tuesday, would-be profit-takers are testing the waters, and it’s unlikely the stock’s going any higher until investors get a clear idea of what a combined Fiserv and First Data would look like.

AbbVie (ABBV)

There’s nothing inherently wrong with AbbVie (NYSE:ABBV). Though it missed its fourth-quarter revenue and earnings estimates, it’s still a cash cow that’s expected to grow its top and bottom lines this year. It’s dirt cheap too, valued at only 8 times this year’s expected profits.

Nevertheless, like a handful of the other stocks to sell in the coming month, AbbVie is facing an uphill battle of perception. Most drugmaker stocks are losing ground on fears that new drug-pricing legislation could be forthcoming. Meanwhile, ABBV has developed a strong downtrend of its own since peaking a year ago on worries about the fading patent protection of its blockbuster drug Humira.

Keysight Technologies (KEYS)

Finally, Keysight Technologies (NYSE:KEYS) is one of a handful of stocks to sell for February after an incredible January rally that won’t likely last.

Since its late-December low, KEYS stock has gained more than 28%, mostly thanks to the market’s realization of the company’s role in the rollout of 5G wireless connections. Once Verizon Communications (NYSE:VZ) launched an at-home 5G broadband platform in October, the technology became very real for investors. On the hunt for overlooked names in the business, investors found and fell in love with Keysight.

They arguably overshot though. Since it’s now overbought much like it was a couple of different times last year, a reversion to the mean looks likely.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.

Each year I read about the promise of virtual reality / augmented reality (VR/AR) and how this is THE year for the technology to take hold. Most of these predictions center around either gaming or the ability to watch live sporting events in a VR/AR environment. In other words, you can sit at home on your couch, but also be courtside at a Lakers game, and at halftime you can play Fortnite in a VR environment with friends around the world.

And, while I believe the technology, as well as the supporting marketing, infrastructure, and necessary consumer buy-in, will eventually converge and become a major industry, as they say, the key is in the timing. 5G will be a major boon to this industry, and as the new network technology rolls out in the next few years, VR/AR will be one of the major beneficiaries.

When most investors think of VR/AR the first thing that comes to mind is Facebook (Nasdaq: FB) and its Oculus Rift, or newer Oculus Go. Or, Lenovo (NYSE: LNVGY) the world’s largest AR headset maker. But, there is another ecosystem of VR/AR that is flying largely under the mainstream investment community radar with its focus on gaming.

Industry 4.0, shorthand for the connectivity and digitization of manufacturing, which includes increased use of digital tools for manufacturing, training, and marketing, is one area where VR/AR is making an impact. Another is the use of VR/AR to enhance capabilities in high pressure, high stakes professions, such as doctors, pilots, and soldiers. And in yet one more part of this ecosystem, are VR/AR capabilities to enhance safety and security for consumers. An example being the use of VR/AR in autonomous vehicles.

Each of these fast growing areas are already being aided by VR/AR technology to either enhance current systems, provide institutional memory and training for an increasingly nomadic workforce (see my previous article on the gig economy), or to increase the safety of the public and our military. These are a few of the companies that are employing a VR/AR solution today, and not waiting for next year.

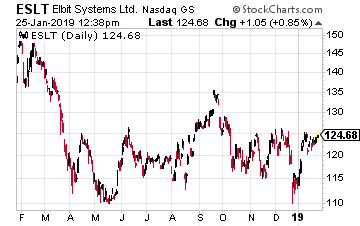

Elbit Systems (Nasdaq: ESLT)

Elbit Systems is an Israeli based aerospace and defense company which has been working on an AR cockpit for both commercial and military use. Elbit, known for its HUD (head-up display), which can display flight information to the pilot without the need to look down, purchased Universal Avionics last year. Universal brought a flight management system (FMS) to the merger.

Late last year, Elbit introduced a new product, combining the HUD with the functionality to operate the FMS. This was truly science fiction type technology only a few years ago. The fully functional product can be both retrofitted to older aircraft, without a complete rewiring of the aircraft, as well as built into new aircraft.

Using the system, a pilot can program and change their flight path, select or change a runway, and select and update waypoints, all with just their eyes. The system is also integrated with technology mounted on the outside of the aircraft, which allows for a virtual projection of terrain onto the cockpit window. This makes for a safer and more accurate depiction of reality in bad weather or low altitude flying.

Elbit is using AR not only in the air, but on the ground as well. One of the dangers faced by tactical spotter teams, forward observers that locate and identify military targets, is that an enemy will be able to see and counter their moves when they use a laser to “paint” a target. Using a combination of AR and other technologies, late in 2018 Elbit introduced the HattoriX system, which provides an AR overlay providing command and control capabilities (C2). This allows the forward spotter team to identify a target and feed coordinates to the necessary team delivering a payload on the target, without endangering the forward team by using a laser to paint the target.

Both of these technologies, the HUD VR cockpit, and the ground based forward spotter HattoriX system, make the jobs of their users safer and more efficient. They provide great examples of using VR technology in combination with platforms that are already in place. And, give an idea of what an acceleration in VR use is capable of. I fully expect Elbit to introduce more and more VR based products, and believe now is the time to buy the stock.

Elbit is a solid company expected to grow earnings next year over 14%, with a long term 5 year projection of an average 11% earnings growth per year. And, the company currently pays a 1.42% dividend.

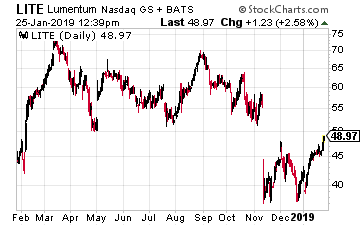

Lumentum (Nasdaq: LITE)

Lumentum has three main areas of business. First, their photonic division works to move the growing amount of data generated each day more efficiently over networks. Second, they produce lasers which are used in precision manufacturing to make sure parts are manufactured to exacting specifications.

And third, and the area I’m interested in today, is a 3D sensing technology that can be placed in mobile devices and autonomous vehicles to provide a virtual reality picture. Lumentum is the largest supplier of 3D laser sensors globally.

These 3D diode lasers produced by Lumentum are more accurate and reliable than radar and camera based technologies, which still play a role in producing a 360 degree picture around an autonomous vehicle. As I’ve pointed out in a few different articles over the past month, a regulatory structure is of paramount importance to the autonomous vehicle market. To enact this structure, vehicles must have extremely reliable and accurate instrumentation with the ability to measure and predict the movement of objects around the car.

In mobile applications, 3D sensors are used for facial recognition, robotic sensing, and IoT (Internet of Things) applications, to name a few. Lumentum provides not only the lasers to perform 3D sensing, but a complete turnkey solution which can be placed in any manufacturer’s mobile device. With a likely expansion into most, if not all future smartphones, robotics, the IoT, and autonomous vehicles, Lumentum may be on the cusp of an earnings explosion. Lumentum occupies a great position at the convergence of emerging 5G networks, with smartphones and the IoT.

Lumentum currently has a PE of 7.88 and is projected to grow earnings in the coming year at over 21%. And, with cash on hand of almost $12 a share, the company has the necessary capital to build out production in an expanding market. Lumentum was caught up in the issues with Apple (Nasdaq: AAPL) last quarter, which resulted in a drop in the stock. But, I believe slowing iPhone sales could accelerate an expansion in its customer base, which would be in addition to the customer base expansion from autonomous vehicles, IoT, and robotics. This pullback could represent a great buying opportunity in the stock.

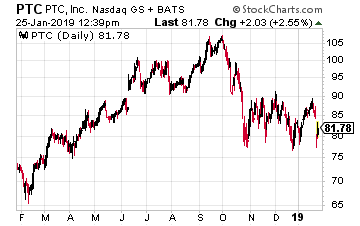

PTC Inc. (NYSE: PTC)

PTC is on the cutting edge of helping industrial companies convert to digital. With an array of offerings in AR, 3D printing, IoT, and industry 4.0, the company is moving large industrial giants into the future.

Using their Vuforia virtual reality platform the company provides the tools and software to record a manufacturing or business process. The software then creates an AR view of that process that can be used to teach new employees, provide the best training possible around the world, or have established experts within or outside the company review and improve the process without ever entering the manufacturing facility.

“We delivered another strong [quarter of] growth with AR bookings growth,” stated Jim Heppelmann, PTC CEO in its latest conference call last week. “Another strong quarter with AR bookings growth of over 75% versus Q1 of 2018. The main use cases for AR in the industrial world are service and maintenance work instructions, factory operator Instructions, and virtual product demonstrations. While it’s still early, AR commercial adoption within the industrial market is broadening.”

Unlike in the gaming world, where VR is still largely a gimmick, in the industrial world real products are being used by massive companies to drive productivity growth. PTC is well positioned, and now is a great time to get in on this burgeoning trend. PTC’s customers include John Deere (NYSE: DE), British based BAE Systems (NYSE: BAE), Sinotruk (OTCMKTS: SHKLY) automotive in China, and Sony (NYSE: SNE) in Japan. The addressable market for PTC products is basically any company that manufactures or sells products, or provides a service which can be demonstrated via AR.

PTC stock pulled back slightly last week when Mr. Heppelmann said they were seeing some softness globally, but not enough to lower 2019 estimates. This pullback offers a better entry into the stock, which is expecting over 50% earnings growth in the upcoming year, and is projected to grow earnings over the next 5 years at an average 36%.

Growth in the AR/VR market is already taking place. Whether it is in aerospace and defense with Elbit, in safety and security with Lumenum, or in manufacturing with PTC, you can take advantage of the growth in this market today by adding these names to your portfolio.

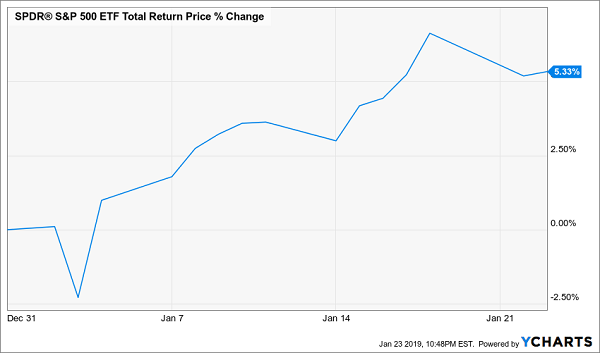

With the market on the rise from its Christmastime lows, it’s natural to wonder if you’ve missed out on the rebound.

Good news: you haven’t—and today I’m going to tell you why we’re still looking at a terrific buying opportunity, even though stocks have gained more than 5% since bottoming in late December:

The Recovery Is Here

The 5.3% jump since the start of 2019 isn’t the result of fundamentals (those haven’t changed), new news (there haven’t been any significant developments) or an end to political gridlock (the shutdown has remained in effect). Instead, it’s been a clearly psychological change: with the new year, the market has a new attitude.

When it comes to short-term trends, psychology is by far the most important factor. People sell when they panic and buy when they’re greedy—which is why the contrarian, seeking long-term profits and a stable income stream, does the opposite and buys when people panic (because they’re overselling cheap assets) and sells when people are greedy (because they’re overbidding assets beyond their true value).

And that’s the biggest reason why bear markets aren’t to be feared—they’re to be embraced in a bear hug your portfolio will eventually enjoy.

Another Reason to Love the Bears

That isn’t the only reason to not fear bear markets, however. There’s one key factor you should cling to during every downturn—and take into account when you’re on the hunt for contrarian bargains: the length of a bear market.

First, the facts.

On average, bear markets have lasted 14 months from beginning to end since World War II, with the average decline being 33% from top to bottom.

However, on average, bear markets have recovered to their pre-bear-market high in an average of 14 months—meaning that the average investor who ignores short-term volatility will find that their portfolio fully recovered in about as much time as they saw it weaken.

Let’s dig deeper. Since 1945, we have had a total of nine bear markets with an average 35.8% decline among them. Also, unsurprisingly, the longer the bear market, the deeper the decline:

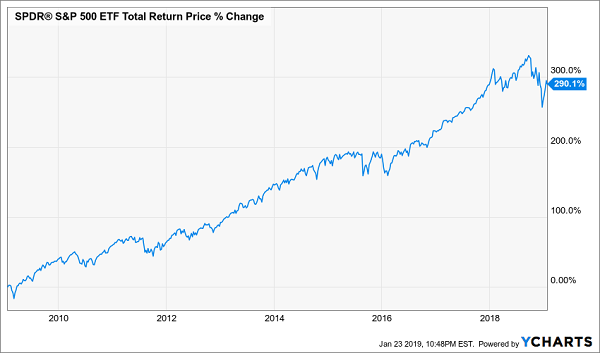

Note how the biggest decline of them all was the most recent: the 2007–09 Great Recession is the sort of once-in-a-lifetime event we aren’t likely to see again anytime soon. That didn’t stop many Americans from bailing on stocks during its depths, meaning they missed out on the 48 months of recovery that followed it and the 290% gains in the decade since:

Buying in ’08/’09 Led to the Ultimate Payoff

Of course, we can’t only buy stocks when they’re at their weakest—but every bear market is a clear buying opportunity, because it’ll take just about a year for the market to recover to its pre-bear-market levels—which means massive profits for people who bought when stocks were at their bear-market lows.

How Will 2018’s Bear Market Be Remembered?

My table above doesn’t include the 2018 bear market, for one reason: it isn’t over yet.

If the market continues on its uptrend, we can say that the bear market itself lasted a total of three months (really a bit less, since the market bottomed on December 24 after starting to fall on October 3).

And if we assume the same rate of recovery as we’ve seen since the market’s Christmas low, a very rough estimate would say that we’re halfway through the recovery after it lasting about a month. That would mean the total recovery time will be two months in total, shorter than the length of the downturn and far too little time in the long haul to get worked up about.

So what’s the key takeaway now? Simply this: the time to buy stocks is now—before this bear market’s short-term low prices have fully disappeared.

On that note, I want to show you …

4 Red Hot Buys for 20% GAINS (and 8%+ dividends!) in 2019

You’ll do even better if you buy the 4 closed-end funds (CEFs) I’m pounding the table on now.

Closed-end what?

Don’t worry if you’ve never heard of CEFs. Because there are only two things you really need to know about these retirement-altering cash machines:

These funds throw off GIANT dividends: Safe yields of 8% and up are common in the CEF space, and …

The selloff has knocked CEFs to ridiculously cheap levels. And because CEF investors are always slower to react to market shifts than folks who buy big-name stocks, we’ve still got a terrific opportunity to rack up BIG profits here.

How big?

Each of the 4 incredible funds I’ll show you when you click here is locked in for 20%+ in “snapback” gains in 2019 alone as their silly discounts revert to normal.

One of these picks, for example, trades at an unusually large 13% discount to net asset value (NAV, or the value of its underlying portfolio). That simply can’t last, especially when you consider that this discount was as narrow as 5% in August 2017 and has been near (and above) par many times in the past!

Don’t Let This Deal Get Away

Now is the time to buy this one—before it makes its next move higher.

Markets declined Monday, after lower-than-expected Caterpillar (CAT) earnings and an Nvidia (NVDA) warning, both due to weakness in China, began to bring the global economic slowdown into focus. Whirlpool (WHR), reporting after the close, also blamed lowered 2019 guidance on weakness mainly in the Chinese market. A new round of trade talks between the U.S and China are slated to begin later this week. The question is whether the downward momentum in the Chinese economy will continue despite an agreement, or whether stimulus by the Chinese government, combined with a trade agreement, will be enough to turn the flailing economy around.

Pfizer (PFE), Verizon (VZ), and 3M (MMM) all report earnings Tuesday morning. Verizon has rallied nicely after the recent dip in the market. Analysts will be looking for updates on spend to build out the 5G network, and how the company sees that investment outflow in 2019. Tuesday evening all eyes will be on Apple (AAPL) when the company report earnings after the close. Investors will want an update on the situation in China, and whether prices will be cut for the newest iPhones. Some analysts see no way around a price cut, whether a trade deal is reached with China or not. Also reporting after the close are Stryker (SYK) and Ebay (EBAY).

Tuesday is the beginning of a Federal Open Market Committee (FOMC) meeting which will conclude with an interest rate announcement Wednesday at 2 pm. The Fed is not expected to raise rates at this meeting. International trade in goods and retail and wholesale inventories will also be released Tuesday morning, assuming the numbers have been compiled given the recently ended government shutdown. Analysts will also be focusing on the S&P Corelogic Case-Schiller Home Price Index which is predicted to rise .3% month-over-month. Consumer confidence will also be released.

GDP, scheduled for release Wednesday, will be delayed due to the government shutdown. The current projection is for a 2.6% increase for Q4. The ADP employment report and MBA mortgage applications are also scheduled for release Wednesday morning. Pending home sales are expected to rise .1% for December when the data is released Wednesday. Following the Fed announcement, Chairman Powell is scheduled to give a press conference at 2:30 pm. This will be a closely monitored event, as the Chairman has greatly impacted rate perceptions in his appearances and speeches the past few months.

Wednesday, before the open, we’ll see earnings reports from Alibaba (BABA), Boeing (BA) and McDonald’s (MCD). Many, fearing a slowing in airline traffic, are looking to BA for any signs of cracks in the earnings report. China will also loom large when the airplane builder reports. Alibaba should provide some insight into the Chinese consumer, and how rapidly the Chinese economy is cooling. They may even shed some light on how stimulus efforts, undertaken by the Chinese government, are working.

After the close Wednesday analysts will dissect earnings from Microsoft (MSFT), Facebook (FB) and PayPal (PYPL). While turning up from a short term bottom, Microsoft has not yet been able to retake highs it achieved near the end of 2018. Facebook continues to come under pressure on its advertising practices. Investors will be listening for some clarity on those practices, as CEO Mark Zuckerberg has recently taken to the media to defend the company’s advertising format.

Where should you look for the best stock opportunities right now? With all the volatility recently, there are some top-notch stocks that appear woefully under-priced. That’s according to recent reports from top analysts. I used TipRanks market data to pinpoint cheap stocks that analysts believe are bargains right now, ones that and are primed for a strong 2019. Indeed, as you will see, the upside potential from the current share price is extremely encouraging.

As Blackstone’s investment strategist Joseph Zidle told CNBC, “This is a buying opportunity. We see the market (the S&P 500 index) up 15% in 2019. This is just not a recessionary environment.”

With this bullish analysis in mind, let’s take a closer look at these seven cheap stock picks now:

Gilead (GILD)

Source: Shutterstock

There’s no denying it, Gilead Sciences (NASDAQ:GILD) is a stock with a rocky past. But it’s now at the point where it’s starting to look compelling all over again. So are you ready to take a fresh punt on this biopharma?

Maybe this will convince you — Oppenheimer’s Hartaj Singh (Track Record & Ratings) has just boosted his GILD rating from “hold” to “buy.” He explained his upgrade as a result of multiple catalysts set to take place in 2019.

Prepare yourself for 1) the addition of a savvy industry veteran in Daniel O’Day as the new CEO (announced 12/10/18), (2) year-on-year sales growth, and (3) important mid/late-stage clinical readouts for budding franchises in inflammation (filgotinib) and NASH (selonsertib, NASH combination trials).

Net-net Gilead is poised to get its mojo back. That’s because the combination of all the factors above “could start to rerate a biotech bellwether, a name that is among the cheapest in large-cap biotech” says Singh.

He has an $85 price target on the stock (24% upside potential), with the Street even slightly more bullish at $88 (29% upside). Note that shares lost 13% in December, but are already up 9% in 2019. Interested in Gilead stock? Get a free GILD Stock Research Report.

Source: Shutterstock

Shares in Goldman Sachs Group (NYSE:GS) surged 11% after its excellent earnings report.

The move caused Oppenheimer’s Chris Kotowski (Track Record & Ratings) to exclaim: “We went to business school like most analysts and have a general faith in efficient markets, but the past six weeks tests our faith.”

Goldman did print a good quarter of $6.04 versus consensus $5.61, but, the analyst asks, was that really enough for a 9.5% gain on the day and a 30% gain off the Dec. 24 low?

“No, it wasn’t the quarter. Rather it was that the December 24 low was (in our view) what we would technically term “stupid cheap,” and so it was this morning and after this move the stock is way too cheap” Kotowski tells investors.

Indeed, even after this move, the stock is still 28% below its March high, even though consensus estimates are now higher than in March.

Plus Kotowski’s $272 price target indicates shares have a further 37% upside potential left to run. Get the GS Stock Research Report.

Source: Shutterstock

Buy low buy now buy ‘nets. That’s the word from top-ranked RBC Capital analyst Mark Mahaney (Track Record & Ratings).

He spies an “unusually positive valuation set-up” for internet stocks right now. And none more so than Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL). The stock is currently trading within 10% of 52-week lows.

“Amongst large cap ‘Nets [internet stocks] in our coverage universe, 7 are trading at or within one turn of 3-year trough multiples” says the analyst. He has a $1,400 price target on the stock (28% upside potential).

The analyst continues on this bullish note: “We note the last time the ‘Net was close to being ‘on sale’ like this was at the beginning of ’16. This set-up could cause FANG Trounce – FANG to materially outperform S&P 500, as it has done 3 of past 4 years.”

As for Alphabet specifically, this is a company with extremely consistent fundamental trends and $100 billion-plus of net cash on its balance sheet — dry powder for extra confidence amid market turbulence.

Meanwhile the stock has a strong set up for the future. Investments in Hardware, Cloud, internet-connected homes, and Autonomous Vehicles set GOOGL up for more years of premium growth & profits. Get the GOOGL Stock Research Report.

Philip Morris (PM)

Source: Shutterstock

So the staples stocks may not be the most appealing group of stocks right now. The macro outlook is weak and some valuations appear pretty stretched right now.

But there are still compelling opportunities to be found- you just need to know where to look.

“We still see pockets of opportunity in Staples, particularly in the beaten down Tobacco sector — our sub-sector rankings remain No. 1: Tobacco; No. 2: Beverages; and No. 3: HPC” says Wells Fargo’s Bonnie Herzog (Track Record & Ratings).

Her number one top stock pick is Marlboro maker Philip Morris International (NYSE:PM). The company is diversifying into “heat not burn” smokeless cigarette devices IQOS. According to Philip Morris, its goal is to replace cigarettes with these smoke-free products.

Shares are down 19% on a three-month basis, but have rallied 8% since the start of the year.

Indeed Herzog believes the stock has now reached an inflection point. She believes the set-up for 2019 is positive due to: easy comps, right sized iQOS inventories in Japan, new iQOS innovation and strong cigarette fundamentals/pricing. This is reflected in her $100 price target.- 36% upside potential from the current share price.

“We reiterate our bullish outlook on the Tobacco sector given very attractive valuations, pricing power, strong & recurring cash flow streams, attractive dividend yields and upside from reduced-risk products” explains Herzog. Get the PM Stock Research Report.

Nashville-based Pinnacle Financial Partners (NASDAQ:PNFP) bank has just released its fourth-quarter earnings results.

Operating EPS of $1.25 beat Street estimates of $1.23, while the quarter also included core NIM expansion (+6bps) for the first time in several quarters.

Additionally, PNFP repurchased $21 million of its $100 million buyback authorization during the quarter.

“Despite softer 4Q loan growth, we were impressed with the ~16% annualized core NII growth during the quarter and continue to view the stock as too cheap given this core top-line growth and core profitability profile” commented Stephens’ Tyler Stafford (Track Record & Ratings) post-results.

Stafford has a $60 price target on PNFP right now. Plus, in a further sign of confidence, two analysts also ramped up their price targets on the stock in the last week.

Also note — UBS has just upgraded the stock from “sell” to “hold.” While this isn’t quite a full blown shout of confidence, it’s still a worthy start! Get the PNFP Stock Research Report.

Source: Shutterstock

Our second internet stock on this list is file sharing site Dropbox (NASDAQ:DBX). Welcome to a stock that offers both internet scalability and SaaS predictability.

Now there are some investors who don’t like Dropbox. They believe that Dropbox is not well differentiated vs. peers such as Microsoft & Google. Other sceptics argue that storage is a commoditized product, and that it comes for free with other offerings such as Microsoft 365 and G Suite.

But I would argue that these concerns are overplayed. First of all, the company believes that they have built the best product for end users. Their product is operating system agnostic, and indeed, users like to use their product better than peers.

In fact, this dynamic has now evolved into a partnership, with G Suite & Microsoft being two of their largest partners.

RBC’s Mark Mahaney (Track Record & Ratings) is firmly on-side. His $37 price target translates into extremely attractive upside potential of 61%. That’s with shares down 7% on a three-month basis.

“Each quarter, we have become increasingly impressed with DBX’s business and financial model. Best of breed FCF margins (33% in Q3) coupled with robust, consistent revenue growth.”

DBX’s freemium model enables highly cost-efficient customer acquisition, very high customer retention levels, and substantial revenue visibility with plenty of upsell opportunities he concludes.

Overall, the Street has a “strong buy” consensus on DBX with a $34.50 price target (50% upside potential). Get the DBX Stock Research Report.

Constellation Brands (STZ)

Source: Shutterstock

Last but not least comes drinks giant Constellation Brands (NYSE:STZ). In the last three months, the stock has plunged 26%. That’s despite healthy momentum in beer (as just revealed at a beer segment update in Chicago) and a neat play on cannabis.

Top-rated Jefferies analyst Kevin Grundy (Track Record & Ratings) calls STZ his top pick for 2019. He finds an attractive buying opportunity in the stock’s near-term weakness.

Right now the base business (ex.Canopy) is trading at 12.5x NTM EV/EBITDA (staples 13.5x) despite best-in-class financial profile.

Here Grundy tells investors why they should be diving into STZ right now. “We model <10% beer sales growth over the next 3-5yrs with strong growth for Mexican imports. Reasonable margin ests, and Canopy stake provides unique exposure to the cannabis market.”

Indeed, his $258 price target works out at upside potential of 56%. Also notice that Goldman Sachs’ Judy Hong has just upgraded STZ from hold to buy. “Importantly, we believe Constellation Brand shares could outperform even if investors assign $0 to its investment in Canopy,” Hong said. Get the STZ Stock Research Report.

TipRanks.com offers exclusive insights for investors by focusing on the moves of experts: Analysts, Insiders, Bloggers, Hedge Fund Managers and more. See what the experts are saying about your stocks now at TipRanks.com. As of this writing, Harriet Lefton did not hold a position in any of the aforementioned securities.

Markets rallied for a fifth straight week Friday as a trifecta of good news was enjoyed by investors. President Trump announced a temporary reopening of the U.S. government after reaching a deal with Congress. Unless a final deal is reached before mid-February, another shutdown could ensue. But, traders are hopeful this is a sign that a permanent solution can be reached.

The WSJ reported the Fed may be close to halting its program of quantitative tightening. This could give markets the breathing room they need to regather for another rally. And, finally, positive news on the trade front is raising confidence that additional tariffs will be avoided in coming months.

We are in the heart of earnings season, and the last week of January will start off with a bang. Monday morning analysts will get right to work dissecting earnings from Caterpillar (CAT) and then interpreting releases from Whirlpool (WHR) and Celanese (CE) after the close. Caterpillar has been a bellwether in the recent trade dispute between the U.S and China, rising when there is good news and falling when tensions between the countries rise. Analysts will be looking for the real impacts of the trade dispute when Cat reports. Whirlpool has long been viewed as a measure of how the consumer is holding up. The company is expected to report $4.30 per share, with the main question being whether the company is seeing inflationary pressures from its suppliers.

The Dallas Fed Manufacturing Survey and the Chicago Fed National Activity Index will both be released Monday. The Chicago numbers could be particularly interesting as they pick up activity nationwide, and should give a better reading on how weak manufacturing has become. Last month’s reading came in at .22, and the current three month average is .12. The positive numbers indicate manufacturing is still growing above trend, even with the recent falloff reported by regional Fed Banks. Tuesday analysts will look through Redbook retail numbers, international trade numbers, and the Corelogic Case-Schiller Home Price Index (HPI). The HPI October numbers were relatively flat.

Apple (AAPL) will be the headliner Tuesday when the company reports earnings. Investors are anticipating an update on sales in China, and many analysts feel price cuts are coming in the newest iPhones. Pfizer (PFE), Verizon (VZ) and 3M (MMM) also report Tuesday. The hits keep coming Wednesday when Microsoft (MSFT), Facebook (FB), and Visa (V) all report. Facebook’s Mark Zuckerberg will likely comment on Facebook’s advertising practices after penning a piece for the WSJ addressing the issue on Friday.

Mortgage applications, impending home sales, and the ADP employment report are all released Wednesday morning. Also on the slate are GDP numbers. GDP is expected to come in at 3.4% for the quarter. Wednesday afternoon will also mark the close of a two day Federal Open Market Committee meeting, with any interest rate changes announced at 2 pm. Traders do not expect any move by the Fed, but will be watching the statement closely for any deviation in wording from the Feds last comments.

Thursday we’ll hear from Amazon (AMZN), Mastercard (MA) and General Electric (GE) as they report quarterly earnings. Investors will likely get an update on how the standup of the new Amazon headquarters is progressing. Friday will be all about big oil as both Exxon Mobil (XOM) and Chevron (CVX) report before the opening bell.

Jobless claims and the employment cost index will be released Thursday. And on the first day of February, consumer sentiment, employment situation numbers, and the PMI manufacturing index will all be released Friday. Non-farm payrolls are expected to come in at 312K and the unemployment rate is projected to be 3.9%.

[Editor’s note: This story was originally published in August 2018. It has since been updated and republished to reflect changes in stock price, although the writer’s opinions may have changed.]

The stock market is a mess right now. Ever since Facebook (NASDAQ:FB) dropped the ball, the whole tech sector has rolled over and markets have dropped. The broad market volatility, however, does not change the bull thesis on cheap stocks. In the group of stocks under $5, macro market movements can cause some noise in shares. But, the investment thesis on cheap stocks is predicated on huge moves higher in the long-term. Thus, near-term, macro-driven movements amount to nothing more than a sideshow.

From this perspective, now might be a good time to pile into some stocks under $5. These stocks are a high-risk bunch. But, they do have high-reward potential, too. Just look at the three stocks under $10 that I recommended buying in late March, including Pandora (NYSE:P).

All three stocks were considered high-risk losers at the time. But since then, P stock has risen nearly 80%.

With that in mind, here is a list of five cheap stocks, which I think have equally big upside potential over the next several months.

Source: Shutterstock

Pier 1 (PIR)

PIR Stock Price: 71 cents

Furniture retailer Pier 1 Imports (NYSE:PIR) has had a tough time getting its act together for several years.

Peer Restoration Hardware (NYSE:RH) has seen its stock rise 30% over the past year thanks to a red-hot housing market and robust demand for home furnishings. PIR stock, however, has collapsed during that same stretch. These problems aren’t new. Over the past five years, this stock has lost more than 90% of its value.

Having said that, there is visibility for a turnaround in PIR stock in the near future.

At its core, Pier 1 has been killed by rising e-commerce threats creating huge pricing and traffic headwinds. Pier 1, which stands somewhat square in the middle of price and quality, doesn’t really have anything special about the business to protect against these headwinds. Consequently, sales and margins have dropped in a big way.

But, the company recently unveiled a three-year strategic plan to turn the business around. The plan includes a re-launch of the Pier 1 brand this fall and bigger investments into omni-channel commerce capabilities and marketing.

No one knows whether or not this plan will actually work. But, home furnishings is a market with enduring demand, so that helps. Plus, search interest related to the company is actually starting to grow on a year-over-year basis, illustrating that this plan is off to a good start.

Meanwhile, PIR stock is dirt cheap. This company used to have earnings power of $1 per share. Even half of that earnings power (50 cents) would be huge for a $2 stock. At 50 cents per share in earnings power, it wouldn’t be unreasonable to see this stock hit $8 (a market-average 16x multiple).

Source: Shutterstock

Groupon (GRPN)

GRPN Stock Price: $3.63

Much like Pier 1, savings-king Groupon (NASDAQ:GRPN) feels like one of those companies that were loved yesterday but will be forgotten tomorrow. But, I don’t think that’s true. I get that the savings and deals market is commoditized now. I also understand that Groupon really isn’t a household name for coupons like it used to be.

But, I’m a numbers a guy. And the numbers are pretty good here. The customer base is actually still growing (up more than 2% year-over-year last quarter). Thus, global popularity of the Groupon platform is only growing.

Meanwhile, margins are improving thanks to management’s focus on higher-margin businesses. Operating expenses are also being removed from the system, so the company’s overall profitability profile is dramatically improving.

Aside from the numbers, Groupon launched an aggressive 2018 advertising campaign with hyper-relevant Tiffany Haddish that scored just shy of 100 million views. I think this campaign will have a long-term positive effect on usage, which could drive the stock higher.

I’m not a huge fan of the mobile gaming sector. It’s a tough space plagued with competition and low margins. Plus, competition is only building thanks to social media apps becoming increasingly multi-purpose.

But, mobile gaming company Zynga (NASDAQ:ZNGA) seems to have found the key to success in the mobile gaming world.

Zynga used to be a mega-popular browser game company with tons of users. But then the company overreached by branching into games that had heavy overlap with the traditional video game market, like sports titles. They couldn’t compete in that market. Eventually, the over-extension sparked user churn, and ZNGA stock spiraled downward.

That forced Zynga to re-invent itself into something much more relevant and defensible. They did just that. Zynga has transitioned its business model from web-focused to mobile-first while narrowing its gaming title focus. This pivot has streamlined operations, re-invigorated top-line growth, cut costs and improved profitability.

Consequently, the numbers supporting Zynga are pretty good. Mobile revenue growth was up 9%in the third quarter. Mobile bookings growth hit 23% year-over-year. The company also reported a huge audience of 22 million mobile daily active users (+10%) and 87 million mobile monthly active users (+9%).

From where I sit, this pivot appears to be in its early stages. Mobile is a secular growth narrative, and ZNGA has developed a gaming portfolio that is focused and tailored to that growth narrative. Thus, so long as mobile engagement heads higher, Zynga’s numbers should get better. Better numbers will inevitably lead to a higher stock price.

There is no hiding the fact that the defense sector is hot right now.

President Donald Trump came into office, upped the ante on defense and military spending, and in response, the whole world is spending more on defense and military.

Defense contractors win when this happens. That is why mega-cap defense contractors like Lockheed Martin (NYSE:LMT) and Boeing (NYSE:BA) have been on fire for the past several quarters.

But one micro-cap defense contractor that has missed out on this rally is Arotech (NASDAQ:ARTX). Over the past several years, the financials at Arotech haven’t gained any ground. Five years ago, revenues were $88 million and operating profits were $3.5 billion. Last year, revenues were $98 million and operating profits were $2.9 million.

In other words, profits haven’t risen in five years. When profits don’t go up, the stock tends not to go up. It is a simple relationship.

But, profits are stabilizing. When profits go from declining to stabilizing, they usually go to growth next.

And, when profits go up, stocks tend to go up.

As such, it looks like Arotech is finally joining the tide when it comes to big boosts in defense and military spending. This tide will inevitably lift Arotech’s earnings power substantially, and ARTX will rally as a result.

Source: Shutterstock

Blink Charging (BLNK)

BLNK Stock Price: $1.73

When it comes to cheap stocks, there are few as volatile as Blink Charging (NASDAQ:BLNK).

Over the past two years, BLNK stock has gone from $30 to $5, and popped from $5 to $15 … it now sits at a paltry $1.73. This volatility won’t give up any time soon. Thus, if you want to avoid volatility, I’d say avoid BLNK stock.

That being said, if this company’s secular growth narrative surrounding building a network of electric vehicle charging stations globally materializes within the next five years, this stock could be a 5-to-10 bagger.

It is a big risk. But, eventually, global infrastructure will need to match demand. At that point in time, there will be some huge contracts awarded to electric vehicle charging station companies.

Will Blink be one of them? Perhaps. Tough to tell. But if they do land some big contracts, this stock could have another huge pop in a short amount of time.

As of this writing, Luke Lango was long FB, PIR, GRPN and ARTX.

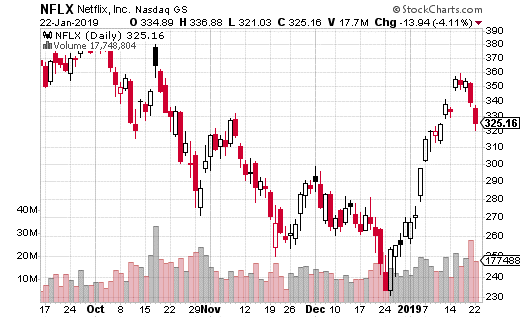

The FANG stocks can be quite polarizing for investors, and Netflix (NASDAQ: NFLX) is no exception. The streaming video giant (and the N in FANG) also may be the most volatile of the four. You can usually count on it for some action every few weeks or so.

Of course, NFLX just posted earnings so there was bound to be a lot of volatility associated with the event. But even before earnings, the stock had been plenty active. As you can see from the chart, there’s over a hundred point range in less than a month.

Last earnings period in 2018, NFLX beat earnings substantially. But, poor market conditions (and a high valuation) led to a steep decline in the share price. The drop ended and the reversal began right at the end of the year. Since that time, the stock has mostly gone straight up until just recently pulling back.

Along with momentum from the stock market recovery, NFLX headed higher in January due to higher viewership numbers. And then, the company announced it would be raising prices. Since NFLX appears to be a fairly inelastic good, most customers will continue their subscriptions after the price hike. That means a bigger bottom line for the company.

On the other hand, the recent earnings news wasn’t stellar. The results weren’t exactly disappointing, but they don’t blow away expectations either. And, the company’s high cash flow needs are a clear reason why raising subscription prices had to take place.

So what’s in store for NFLX next? Let’s take a look at the options action…

A well-capitalized trader just made an expensive bullish bet on NFLX that expires in April. The trader purchased the April 320-330 call spread (buying the 320 call and selling the 330 at the same time) for $5.40 with the stock price at $321.90. The trade was executed 2,680 times for a total cost of $1.4 million.

The cost of the trade, the $1.4 million in premium, is the max risk on the trade. The trade breaks even at $325.40, and can achieve max gain at $330 or above by April. The $4.60 in max gains translates to $1.2 million in profits, or 85% gains.

Now, it may seem like $1.4 million is a lot to spend to only make 85% – at least for a volatile stock like NFLX. However, keep in mind that the trade is already in the money. There’s $1.90 in intrinsic value already in the spread, so really the trader is only paying an extra $3.50 for the position. Moreover, being in the money substantially increases the probability of the trade’s success.

This is an expensive call spread on NFLX, but it has 3 months to expiration and is higher probability than most large call spreads you’ll see. If you are bullish on NFLX, this is a reasonable idea for a trade if you have a bit more money to spend on premiums.