Semiconductor stocks are typically the forward indicators for technology stocks. So when Micron Technologies (NASDAQ: MU) confounded the markets with its consistent single-digit price-to-earnings ratio last year, investors should have exercised caution. The good news is that the patient investor may wait out the cyclical downturn in the chip sector. It will take another six to nine months before reaching a demand and supply equilibrium. Within the graphics chip space, Nvidia (NASDAQ: NVDA) has the clearest headwinds to work through. In knowing what inventory it needs to work through, NVDA stock could start recovering within one or two quarters.

Nvidia experienced excess inventory in the channels, which hurt its revenue forecasts. It blamed the crypto hangover for the excess supply imbalance. At significantly lower prices, cryptocurrency is not likely to recover any time soon. This is the bad news for anyone holding crypto. For NVDA and Advanced Micro Devices (NASDAQ:AMD) shareholders, chances are good that the excess GPUs on the market will clear.

The two firms likely benefited from an increase in sales during the holiday season, after retailers offered rebates and discounts on graphics cards. Once the last-generation card supplies are cleared, game developers will embrace Nvidia’s ray-tracing. RTX card sales slumped in the last quarter and will be weak again for the next two quarters due to cheaper models still on the market.

The fact that Electronic Arts (NASDAQ:EA) was the only big name embracing RTX through its Battlefield 5 title did not help RTX sales. Worsening Nvidia’s near-term prospects was the significant drop in sales of BF V.

Market Opportunity for Ray-Tracing

Nvidia’s Turing brought ray-tracing to games, but pushes its technology forward through the Pro Visualization business. For the last 10 years, the industry simulated such effects as the reflection of light and rays of light bouncing off objects. Ray-tracing processes these effects in real-time. In performance terms, it should bring a 25% – 30% improvement over the Pascal architecture. And at the top-end, performance is 10-fold better.

Within the enterprise space, such as TV, film and Photoshop work, RTX will speed up the development of special effects. Nvidia inserted its graphics technology in around 1.5 million servers, which is worth a few billion dollars in business revenue. As companies slowly embrace RTX, investors should expect the company maintaining and even growing its profit margin.

At a $133 share price, NVDA stock is trading at a more reasonable multiple of around 19 times earnings. With earnings-per-share growth of 15.5% over the next five years, the stock is valued at a PEG of 1.20 times and 19 times forward earnings. AMD, despite falling to $18, still trades at a 30 times P/E multiple.

Fair Value

Analysts did not yet lower their price target on Nvidia. At a $228.50 average price target, based on 30 analysts, the 76% upside (per Tipranks) appears out of touch.

| Analyst | Firm | Position | Price Target | Date |

| Mitch Steves | RBC Capital | Buy | $200.00 | 7 days ago |

| Timothy Arcuri | UBS | Hold | $190.00 | 17 days ago |

| Vijay Rakesh | Mizuho Securities | Buy | $230.00 | 20 days ago |

| Rick Schafer | Oppenheimer | Buy | $250.00 | 21 days ago |

| Atif Malik | Citigroup | Buy | $244.00 | 21 days ago |

| John Pitzer | Credit Suisse | Buy | $225.00 | Last month |

| Ivan Feinseth | Tigress Financial | Buy | — | Last month |

| Matt Ramsay | Cowen & Co. | Buy | $265.00 | Last month |

| Louis Miscioscia | Daiwa | Buy | $203.00 | Last month |

Source: tipranks

As shown in the table above, only one analyst from RBC Capital posted a report on Nvidia stock. The other analysts did not change their view in the last month.

NVDA Is Too Cheap to Ignore

At a P/E now in the teens, markets severely punished Nvidia for failing to forecast GPU demand.

The selloff, which started in October, is now over-done. When the company reports results in February, it will have a better idea on RTX sales for the year, along with the progress slimming down Polaris inventory.

Investors may consider starting a position in NVDA stock at these levels.

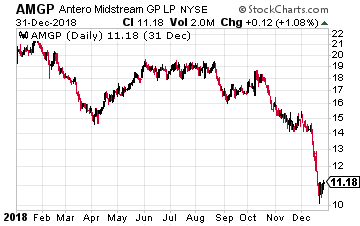

Antero Midstream GP LP (NYSE: AMGP) is an energy midstream services company in transition. The company came to market with a May 2017 IPO. The assets at that time were general partner incentive distribution rights (IDR) ownership interest in high growth, midstream MLP, Antero Midstream Partners (NYSE: AM). The MLP was sponsored and controlled by Marcellus natural gas producer Antero Resources (NYSE: AR).

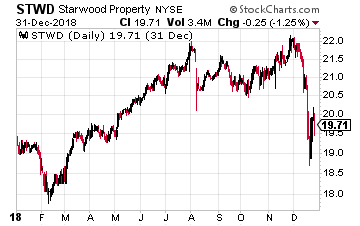

Antero Midstream GP LP (NYSE: AMGP) is an energy midstream services company in transition. The company came to market with a May 2017 IPO. The assets at that time were general partner incentive distribution rights (IDR) ownership interest in high growth, midstream MLP, Antero Midstream Partners (NYSE: AM). The MLP was sponsored and controlled by Marcellus natural gas producer Antero Resources (NYSE: AR). Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT whose primary business is the origination of commercial property mortgages. As one of the largest players in the field, Starwood Property trust focuses on making large loans with specialized terms. This gives them a competitive advantage over banks and smaller commercial finance REITs.

Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT whose primary business is the origination of commercial property mortgages. As one of the largest players in the field, Starwood Property trust focuses on making large loans with specialized terms. This gives them a competitive advantage over banks and smaller commercial finance REITs.