Markets moved higher Wednesday, but were trending lower into the close, after an impressive earnings report from Goldman Sachs (GS) lifted the stock almost 10%. While the beat on earnings lifted the stock, they do not put to bed the ongoing investigation into the money manager by the Malaysian government, or the U.S. Federal Reserve. Markets gave back some of Wednesday’s gains after news hit the wire late afternoon, that the U.S. will be seeking criminal charges against Chinese telecom company Huawei, accusing the company of stealing trade secrets. The ongoing trade tension between China and the U.S. showed signs of progress in the latest round of talks, but the Huawei investigation looms large over the fragile negotiations. No apparent progress has been made on the continuing government shutdown, with both sides now sniping about President Trump’s scheduled State of the Union address later this month.

While pundits debate the exact economic impact the partial government shutdown is having on the economy, we are certain it is impacting the release of economic numbers on which analysts base their recommendations. The latest casualty were retail sales numbers for December, which were due to be released Wednesday, and are now delayed. Thursday we will get the release of jobless claims, which are expected to tick up slightly as more federal workers file claims. The consensus total is for 221K claims. Analysts will also take a look at the Philly Fed Business Outlook, but housing starts, also due Thursday, are delayed.

While financials continue to report Thursday, with earnings from Morgan Stanley (MS) and American Express (AXP), we’ll also hear earnings news from Taiwan Semiconductor (TSM) and Netflix (NFLX). Morgan Stanley, which suffered a dismal 2018, rallied Wednesday along with other banks, tacking on 3.75%. The company is expected to report earnings of $.92 before the market open Thursday morning.

Analysts are highly anticipating Netflix earnings, after the company announced it is raising prices for its subscription services effective immediately for new subscribers, and over a three month period for current customers. The stock has been on a blistering pace the past few weeks, and is up over 50% from an intraday low set December 26th. Investors will be looking for projections of what the price increase means for earnings going forward.

Earnings continue to roll in from financials Friday, when State Street (STT) and Suntrust Bank (STI) both report. Analysts will also hear from oil services company Schlumberger (SLB). This is Schlumberger’s first report since oil prices tanked late in 2018. Revenue is expected to drop 5% sequentially, and the company has projected a possible 15% potential revenue drop in North America, as fracking revenue has declined. After hitting a high of just below $80 in 2018 the stock has been almost cut in half, now trading at just over $41.

Friday investors can pour over industrial production numbers and consumer sentiment, from the University of Michigan survey. Consumers are expected to see a somewhat bleaker landscape, as the survey number is projected to drop to 97 from December’s final reading of 98.3. Mixed messages abound as the government shutdown is a negative, trade negotiations seem slightly positive, and the market rebound in 2019 has been strong.

[Editor’s Note: This article was originally published in September 2018. It has been updated to reflect changes in the market.]

Amazon (NASDAQ:AMZN) has been one of the more impressive stocks of the past 25 years. In fact, AMZN now has returned well over 100,000% from its initial public offering (IPO) price of $18 ($1.50 adjusted for the company’s subsequent stock splits). A large part of the returns has come from two factors. First, Amazon has vastly expanded its reach. What originally was just an online bookseller now has its hands in everything from cloud computing to online media to groceries. And its shadow is even larger …

Amazon’s buyout of Whole Foods rattled the retail market. Similarly, its entry into healthcare by buying PillPack — as well as its healthcare partnership with Berkshire Hathaway (NYSE:BRK.B) and JPMorgan (NYSE:JPM) — sent ripples through the healthcare sector. In response, Microsoft (NASDAQ:MSFT) teamed up with Kroger (NYSE:KR) to “build the grocery store of the future.” And this week, MSFT and Walgreens (NASDAQ:WBA) announced a partnership to fend off Amazon.

Secondly, as a stock, AMZN has managed the feat of keeping a growth stock valuation for over two decades. I’ve long argued that investors can’t focus solely on the company’s high price-earnings (P/E) ratio to value Amazon stock. But however an investor might view the current multiple, the market has assigned a substantial premium to AMZN stock for over 20 years now, and there’s no sign of that ending any time soon.

It’s an impressive combination, and one that’s likely impossible, or close, to duplicate. But these five stocks have the potential to at least replicate parts of the Amazon formula. All five have years, if not decades, of growth ahead. New market opportunities abound. And while I’m not predicting that any will rise 100,000% — or 1,000% — these five stocks do have the potential for impressive long-term gains.

Stocks That Could Be the Next Amazon Stock: Square (SQ)

Admittedly, I personally am not the biggest fan of Square (NYSE:SQ) stock. I like Square as a company, but I continue to question just how much growth is priced into SQ already.

Of course, skeptics like myself have done little to dent the steady rise in AMZN stock. And valuation aside, there’s a clear case for Square to follow an Amazon-like expansion of its business. Back in January, Instinet analyst Dan Dolev compared Square to Amazon and Alphabet Inc (NASDAQ:GOOGL, NASDAQ:GOOG), citing its ability to expand from its current payment-processing base:

“In 10 years, Square is likely to be a very different company helped by accelerating share gains from payment peers and relentless disruption of services like payroll and human resources.”

Just as Amazon used books to expand into e-commerce, and then e-commerce to expand into other areas, Square can do the same with its payment business. The small business space is ripe for disruption, as Dolev points out. Integrating payments into payroll, HR, and other offerings would dramatically expand Square’s addressable market – and lead to a potential decade or more of exceptional growth.

Again, I do question whether that growth is priced in, with SQ trading at well over 90x forward earnings. But if — again, like AMZN — Square stock can combine a high multiple with consistent, impressive, expansion, it has the path to create substantial value for shareholders over the next five to 10 years.

Stocks That Could Be the Next Amazon Stock: JD.com (JD)

In China, JD.com (NASDAQ:JD) is the company closest to following Amazon’s model. While rival Alibaba (NYSE:BABA) gets most of the attention, it’s JD.com that truly should be called the “Amazon of China.”

Like Amazon (and unlike Alibaba), JD.com holds inventory and is investing in a cutting-edge supply chain. It, too, is expanding into brick-and-mortar grocery, like Amazon did with its acquisition of Whole Foods Market. A partnership with Walmart (NYSE:WMT) should further help its off-line ambitions. JD.com is even cautiously entering the finance industry.

At the moment, however, JD stock is going in the exact opposite direction of AMZN. The stock has plunged of late. An arrest of the company’s CEO has been a recent driver. So have mixed earnings reports and a Chinese bear market.

Clearly, there are myriad risks here, even near the lows. But AMZN saw a few pullbacks over the years as well. And while JD may never rise to the scale of Amazon — or even out-compete Alibaba — at its current valuation it doesn’t have to. JD now trades at near-40x forward EPS. That’s despite a series of investments depressing near-term profitability — and building out long-term capabilities — and 40% revenue growth in 2017, with expectations for a nearly 30% increase in 2018.

If investor confidence returns, JD has a path to enormous upside. And even with the near-term jitters facing the stock, the long-term strategy still seems intact, and likely the closest in the market to that of Amazon.

Stocks That Could Be the Next Amazon Stock: Shopify (SHOP)

E-commerce provider Shopify (NYSE:SHOP) probably doesn’t have quite the same opportunity for expansion as Square. And it, too, has a hefty valuation, along with a continuing bear raid from short-seller Citron Research.

But I’ve remained bullish on the SHOP story, even though valuation is a question mark, even after a recent pullback. Shopify is dominant in its market of offering turnkey e-commerce services to small businesses. That’s exactly where consumer preferences are headed: small and unique over large and bland. And because of offerings like Shopify (and Amazon Web Services), those small to mid-sized businesses can compete with the giants.

Meanwhile, Shopify does have the potential to expand its reach. Just 29% of revenue comes from overseas, a proportion that should grow over time. It’s moving toward capturing larger customers as well through its “Plus” program, picking up Ford (NYSE:F) as one key client. The development of an ecosystem for suppliers and the addition of new technologies (like virtual reality) give Shopify the ability to offer more value to customers … and to take more revenue for itself.

Like SQ, SHOP is dearly priced. But both companies have an opportunity to grow into their valuations. And considering long runways for Shopify’s adjacent markets, it should keep a high multiple for some time to come. As a stock, if not quite as a company, SHOP has a real chance to follow the AMZN formula for long-term upside.

Stocks That Could Be the Next Amazon Stock: Roku (ROKU)

Source: Shutterstock

Roku (NASDAQ:ROKU) might have the best chance of any company in the U.S. market to follow Amazon’s strategic playbook. The ROKU stock price is a concern, given that the stock more than doubled in April and it has continued to climb higher, even amid the selloff in tech stocks in October.

At 10x revenue, ROKU isn’t close to cheap.

But — perhaps even more so than Square — Roku now isn’t what Roku is going to be in ten years. The hardware business is a loss leader, but one that allows Roku to serve as the gateway to content for millions of customers. As the company pointed out after recent earnings, it’s already the third-largest distributor of content in the U.S. The Roku Channel is seeing increasing viewership. It’s already up to more than 27 million viewers!

The company offers pinpoint targeting of advertisements — without the messy data problemsafflicting Facebook (NASDAQ:FB).

Roku is becoming increasingly embedded in TVs, though a deal between Amazon and Best Buy (NYSE:BBY) raised some fears about those software efforts going forward. It has a plan to roll out home entertainment offerings like speakers and soundbars, creating a long-sought integrated experience. It could even, as it grows, look to develop or acquire content itself, positioning Roku not as just a conduit to Netflix (NASDAQ:NFLX) but a rival.

The bull case for Roku stock is that its players are like Amazon’s books — not a great business on their own, but a way to garner customers and get a foot in the door of the exceedingly valuable media business. What Roku does now that it has entered will determine the fate of ROKU stock. But the amount of options and still a somewhat modest market cap (under $5 billion) mean that betting on its strategy could be a lucrative play.

Stocks That Could Be the Next Amazon Stock: Workday (WDAY)

Source: Workday

Workday (NASDAQ:WDAY) is starting to look like the enterprise software version of Amazon. Its core HR product has driven huge gains in WDAY stock, which now has a $36 billion market cap. But Workday is just getting started.

The company previously announced that it would buy Adaptive Insights to build out its financial planning capabilities. It has already rolled out analytics and PaaS (platform-as-a-service) offerings that add billions to its addressable market.

Here, too, valuation looks stretched, to say the least, but the story here still looks attractive. Workday is never going to be as famous as Amazon, or as large. But if its strategy works, it will be as important to, and as embedded with, its corporate customers as Amazon is with its consumers.

As of this writing, Vince Martin has no positions in any securities mentioned.

The main takeaway I got from the annual Consumer Electronics Show (CES) in Las Vegas was that enthusiasm for autonomous (driverless) vehicles among the world’s auto makers has really cooled.

Just a year or two ago, car and some tech companies could hardly restrain their excitement over the next revolution in mobility – driverless vehicles. But now, as the next step in driving automation comes closer to reality, some auto industry executives seem keen to back away from implementation and move directly on to the next step. Let me explain…

Levels of Vehicle Autonomy

First, let me fill you in on the levels of autonomy for a vehicle as set by the standards organization, the Society of Automotive Engineers International. There are six levels of autonomy, from zero for absolutely no autonomy to Level 5, which would be complete autonomy. In other words, completely controlled by computers. This technology is probably a decade away.

Here are brief descriptions of the other levels of autonomy:

Level One: Driver Assistance: At this level, the automobile includes some built-in capabilities to operate the vehicle. The vehicle may assist the driver with tasks like steering, braking or acceleration. For several years now cars have been manufactured with controls on the steering column that allow the driver to maintain a constant speed or gradually increase or decrease speed. These functions are enacted by the driver and not automatically performed by the automobile. Most modern cars fit into this level. If your vehicle has adaptive cruise control or lane-keeping technology, it’s probably at level one.

Level Two: Partial Automation: At this level of automation, two or more automated functions work together to relieve the driver of control. An example is a system with both adaptive cruise control and automatic emergency braking. This is referred to as an advanced driver assistance system (ADAS). Examples of level two include Tesla Autopilot, the Mercedes-Benz Distronic Plus and the General Motors Super Cruise.

Level Three: Conditional Automation: This level is marked by both the execution of steering and acceleration/deceleration and the monitoring of the driving environment. In levels zero through two, the driver does all the monitoring. At level three, the driver is still required, but the automobile can perform all aspects of the driving task under some circumstances. Levels three and higher qualify as automated driving systems (ADS). There’s a big jump in capability between levels two and three. The driver still has to keep his eyes on the road, ready to take over at a moment’s notice. But a level three vehicle can handle certain parts of the trip on its own – mainly highway driving.

Level Four: High Automation: Level four vehicles don’t need a human driver. The vehicle can do all the driving, but the driver can intervene and take control as needed. This level of automation means that the car can perform all driving functions “under certain conditions.” The test vehicles currently on the road would fall under this category. Google’s Waymo is testing level four vehicles.

The Level Three Barrier

However, many auto companies are reluctant to even move to Level 3 autonomy. And it’s easy to see why – that’s the first point at which full responsibility — and legal liability — shifts from the driver to the car. Both automakers and regulators are wary about whether transferring control between car and driver can work effectively in an emergency.

That could lead to a legal nightmare when accidents do occur. And it’s why Audi has never turned on its Level 3 software on its vehicles sold here in the U.S.

The idea of a driverless car that can hand back control to a human with little warning has always divided the auto industry. Carmakers such as Toyota, Volvo and Ford, as well as Waymo have always been skeptical about the idea of Level 3 vehicles. These companies believe it is safer to wait longer for more advanced forms of automation that require no human intervention.

Daimler Trucks, the world’s biggest maker of commercial vehicles, also turned its back on Level 3 recently. It said that the technology sent a confusing message to drivers: they are encouraged to switch their attention to something other than the road, but expected to be ready to retake control at a moment’s notice. Other car companies, such as BMW, are moving ahead – its iNext vehicle in 2021 will feature Level 3 technology enabling hands-free, pedal-free driving.

Driverless Vehicle Investments

So what companies seem best poised to benefit from the move toward greater autonomy for vehicles?

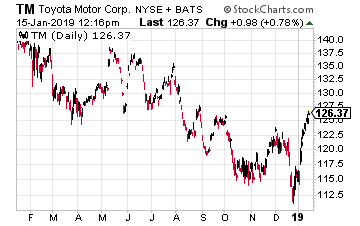

I do like Toyota Motors (NYSE: TM) because it seems to be moving on its own independent path, separate from the other automakers with regard to new technologies. I like their skepticism toward Level 3 vehicles.

And their skepticism toward electric vehicles is interesting. Instead, it is concentrating its efforts on both solid state batteries and fuel cell vehicles. I will be discussing Toyota’s and Japan’s move toward a hydrogen economy in a future article.

I find solid state batteries fascinating. They are capable of holding more electricity and recharging more quickly than their lithium-ion counterparts. These batteries could do to lithium-ion power cells what transistors did to vacuum tubes: render them obsolete.

As the name implies, solid-state batteries use solid rather than liquid materials as an electrolyte. That is the stuff through which ions pass as they move between the poles of a battery as it is charged and discharged. Because they do not leak or give off flammable vapor, as lithium-ion batteries are prone to, solid-state batteries are safer (lower fire hazard). They are also more energy-dense (leading to higher power capacity) and thus more compact. Solid-state batteries are also a promising power source for internet-of-things devices that are coming into wider usage daily.

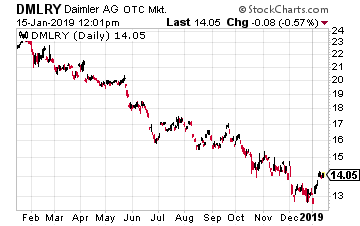

I also like Daimler AG(OTC: DMLRY). Its Freightliner Cascadia will go on sale this year and be the first truck in North America to feature partially-automated driver assistance.

And Daimler is heading straight from level two to level four, in which a truck can operate without user intervention on specific routes because the company says level three “does not offer truck customers a substantial advantage”. Unlike Tesla, it considers Level 3 to be a dead end since it would have to rely on human attention during the crucial 1% of the time after telling the driver not to pay attention 99% of the time. With truckers on long haul routes, I see sleep and Level 3 not being compatible.

Finally, if I must go with a company that is pursuing Level 3 automation, I’ll go with General Motors (NYSE: GM) instead of the cult stock known as Tesla.

Its Level 3 system is better than Tesla’s. If the driver still doesn’t take control after several prompts, the system will gradually bring the vehicle to a complete stop, activate the hazard warning flashers, and call for help (using GM’s OnStar system.) GM also built a slew of additional safeguards into Super Cruise to try to ensure that it’s only used in circumstances it can safely handle. For example, if the vehicle isn’t on a highway, the road’s lane markings aren’t clearly visible, or the system thinks that the driver isn’t fully attentive – it won’t even switch on.

And GM is challenging Tesla in the electric car space. It is re-casting its luxury Cadillac brand as an electric brand. GM says the premium marque would be the company’s “lead electric vehicle brand and will introduce the first model from the company’s all-new battery electric vehicle architecture”. Tesla has long dominated sales of premium electric vehicles, but it faces fresh challenges, not only from the upcoming electric Cadillac, but also from European premium nameplates.

GM is making a lot of right moves, from cost cutting to getting major investments from Honda and Softbank. That led it to recently forecast higher than expected 2018 profits. It also said earnings will rise further in 2019, despite flat or declining car sales in both the U.S. and China, its two primary profit drivers. The automaker expects adjusted earnings per share for 2018 to exceed the guidance given in October of $5.80 to $6.20, and 2019 EPS to rise to $6.50 to $7.00 per share, above market estimates.

Stay tuned to this space though, the race for autonomous vehicles is just getting interesting.