Think you can’t retire on anything less than a million bucks?

Many people would answer that question with a “yes.” If you’re one of them, I have great news: the “million-dollar myth” is just that, a myth.

I’ll tell you why in a second. Then I’ll reveal 4 buys throwing off a safe cash dividend yielding 8.5%—letting you fund your golden years on a lot less.

(These 4 are the tip of the iceberg, by the way. At the very end of this article, I’ll give you 20 more retirement lifesavers paying gaudy 8% average dividends, as well!)

A Million-Dollar Retirement … on $470K!?

So how much smaller of a nest egg am I talking about here?

How does $470K sound? If you’re keeping track at home, that’s 53% less than the suits say you need if you want to spend your golden years above the poverty line.

Better yet, our 4-buy “instant” retirement portfolio will pay us in equal amounts every month. It’s just like getting a regular paycheck, but you don’t have to do a thing—besides log into your brokerage account and pick up your cash!

Beyond the Big Names

A big reason why the million-dollar myth exists is that most folks predict their future income stream based on the pathetic yields popular stocks, like the so-called Dividend Aristocrats, dribble out today.

And it is true that traditional dividend plays don’t come close to the 8.5% average payout thrown off by the 4 off-the-radar buys I’ll show you in a moment.

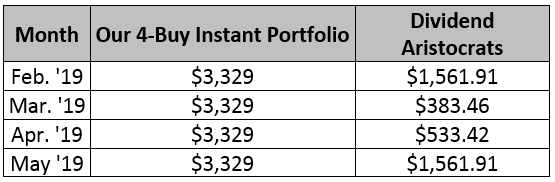

Let’s take a 4-pack of typical Dividend Aristocrats and map how much they’ll pay investors (based on that $470K nest egg I mentioned earlier) in the next few months.

4 Clicks to Smooth, Safe Monthly Payouts

The best part is that this strategy isn’t capped at $470,000. If you have managed to save a million bucks, you can buy more monthly payers like these and kick your monthly income to $7,083.

So let’s move on to the 4 stocks I have for you now—well, they’re not stocks, exactly, but closed-end funds (CEFs).

CEFs are muscular income plays that give us two advantages: outsized dividends (CEF payouts of 8%+ are common) and big discounts to net asset value (NAV), a powerful upside predictor far too few people watch.

Your Monthly “4-Pack” for an 8.5% Average Dividend

The Western Asset Emerging Markets Debt Fund (EMD) yields a gaudy 9.1% today and trades at a 13.1% discount to NAV as I write.

In English: we’re getting its portfolio of emerging market corporate and government bonds for 87 cents on the dollar!

The upshot here is that plateauing US interest rates (traders betting through the futures markets have the Federal Reserve pegged for zero hikes this year) will send income seekers abroad for higher yields—and that’s great news for EMD.

Either way, management has shown its chops since the current rate-hike cycle started three years ago, with the fund’s price (in orange below) slipping just 2.3%. But add in that monster dividend and its total return jumps to 26%!

EMD Shrugs Off Rate Woes

And EMD pulled this off in a tough time for emerging-market debt! But now, with US rates on hold and EMD’s absurd discount, the fund is poised to deliver some nice price upside, on top of its 9.1% monthly dividend.

Now let’s come back home to another sector primed for gains thanks to slowing rate hikes: US real estate. We’ll ride that trend with the Cohen & Steers Total Return Realty Fund (RQI), and its 8.5% monthly dividend.

US real estate underperformed last year, due to the same rate-hike fears that hobbled emerging-market debt:

Rate Fears Hogtie REITs

But I sensed that the Fed was about to change tack during last fall’s stock-market meltdown, which is why I pounded the table on RQI on December 28. Since then, the CEF (in red below) has dominated the benchmark Vanguard Real Estate ETF (VNQ), in blue, and the SPDR S&P 500 ETF (SPY), in orange.

Not Too Late to Grab This Winner

Sure, that rise has thinned RQI’s discount, but you’re still getting an 8.5% payout here, and the current discount (8.7%) points to more upside: just under a year ago, RQI traded at just 1% below NAV. A rise to that level (a certainty, in my view) would give us a 6% price gain while we pocket that huge payout.

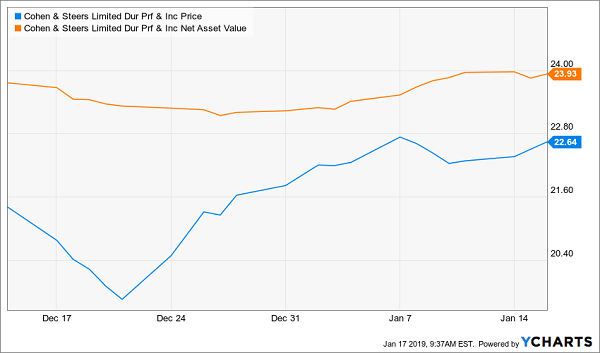

Moving along, let’s add some top-quality finance names through another CEF from Cohen & Steers: the Cohen & Steers Limited Duration Preferred & Income Fund (LDP).

As the name suggests, LDP bypasses finance companies’ regular shares in favor of their preferred stock.

Think of preferreds as stock/bond hybrids that can trade on an exchange, like stocks, but do so around a par value and dole out a fixed regular payment, like bonds.

Their biggest appeal? Outsized payouts. And you can boost those dividends even more if you buy through a CEF like LDP, which pays an outsized 8.3% now.

Another great thing about CEFs in general (and LDP in particular) is that CEF investors tend to be slow to respond to investor mood swings, which is why we can grab LDP at 5.4% below NAV—but your shot at buying cheap is evaporating!

LDP’s Buy Window Is Closing

Finally, let’s tap the Tortoise Power & Energy Infrastructure Fund (TPZ) for its 8.1% payout, while we can still do so at a 7.8% discount.

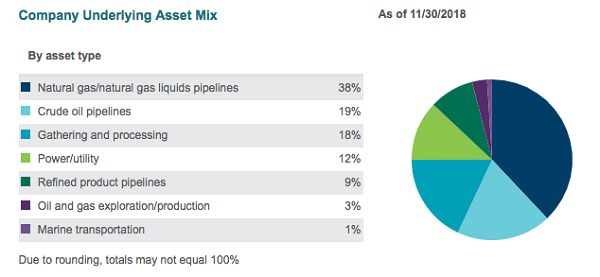

TPZ holds stocks and bonds issued by oil and gas pipelines, storage and processing firms—mostly master limited partnerships (MLPs)—plus some utility stocks:

Source: Tortoise Advisors

Most MLPs will kick you a K-1 tax form around your return deadline and annoy you and your accountant. But TPZ gets around this by issuing you one neat 1099.

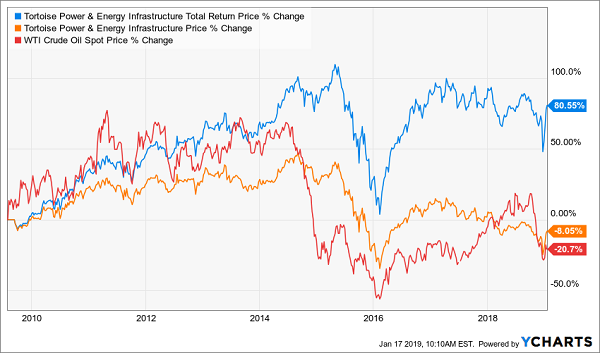

Since MLPs pipe energy, they tend to trade with oil prices. But TPZ’s management has done a great job of dampening oil’s drop since the fund’s inception in 2009.

Below we can see that TPZ’s market price (orange) has dipped 8.1% since launch, but that’s way better than the goo’s 21% crash (in red). And when you add in TPZ’s big dividend, you can see that management has handed investors a solid 81% return in just under a decade.

TPZ Bucks the Oil Plunge

The kicker? The whole time, this dividend has been a picture of serenity:

Oil Crash? What Oil Crash?

Source: CEFConnect.com

Of course, no one knows where oil will go from here, but I expect it to find a bottom in 2019. That means now is the time to make a move—because we could easily look back years from now, at the high yield and nice discount TPZ sports today, and wish we’d pounced.