Wednesday, markets were mainly in recovery mode and made up some ground after a selloff on Chinese economic weakness Tuesday. Strong earnings from International Business Machines (IBM) and Procter & Gamble (PG) propped markets up after downward revisions to global economic growth by the International Monetary Fund (IMF) earlier in the week. The market is also fighting less than stellar news on the trade front between the U.S. and China. And, growing tension on the U.S. government shutdown which appears to become more acrid by the day. The two parties are now arguing over when and where President Trump will deliver his state of the union address next week. From an economic data perspective, investors are getting fewer and fewer data points as more federal agencies stop releasing data due to worker absences.

Jobless claims, PMI composite flash data, and leading indicators will all be released Thursday morning. Jobs continue to be a bright spot in what has become a muddled economic picture, with continually weakening housing numbers, and data indicating manufacturing in the U.S. is slowing. With a lower than expected 213K last week, claims are expected to again remain below the 220.75K four week moving average. PMI flash data is expected to show a continuing sluggishness in manufacturing, with only a slight rise from December levels and still below numbers reported in November.

Thursday is a big day for earnings as Intel (INTC), Union Pacific (UNP), Bristol-Myers (BMY), Starbucks (SBUX), and American Airlines (AAL) all report. American Airlines has traded relatively flat after declining around 25% from highs set just before the selloff that began in October last year. Analysts will be looking at load count as well as the impact of oil prices. There will also likely be discussion of the impact of the government shutdown, and how that is impacting profitability. Starbucks is trading around 10% above highs set in the first half of 2018, and analysts are anticipating strength in North America to offset weakness in the Chinese market.

There is no slowdown in earnings headed into the weekend as AbbVie (ABB), Colgate-Palmolive (CP), Ericsson (ERIC), D.R. Horton (DHI), and Lear Corporation (LEA) all report Friday morning. Management for D.R. Horton will be under a microscope to give investors an expert opinion on if and when they see the housing market stabilizing, and perhaps turning up. Last quarter Colgate-Palmolive’s gross and operating margins both fell, and analysts are not expecting a turnaround this quarter. With the majority of its revenue generated internationally, the consumer goods company should serve as a canary in the coal mine, providing some indication as to whether the global economy is faltering as many believe.

The monthly Kansas City Fed Manufacturing Index is projected to decline yet again after a jaw-dropping 12 point fall last month. The index is expected to come in at 2, down only 1 point from last month’s final tally of 3. Leading economic indicators are also expected to decline for December at -0.1%. The stock market fall, combined with the aforementioned weakness in manufacturing, accounts for the December decline.

Friday we will likely not get the release of planned durable goods orders and new home sales due to the partial government shutdown. We will see data on the Baker-Hughes North American rig count to get an idea of how the rig count is trending with the continuing weakness in oil.

Nouriel Roubini (aka Dr. Doom) is a widely respected economist who is fond of pontificating on everything bitcoin cannot do. He recently earned a place in a column I wrote for our First Stage Investor newsletter when he said, “How could [the SEC] ever approve such ETFs given widespread price manipulation of bitcoin and other cryptocurrencies?”

Roubini is part of a “proud” tradition of people making dismissive predictions about new technology. IBM Chairman Thomas Watson issued one of the most famous ones in 1943.

“I think there is a world market for maybe five computers,” Watson said.

Respected astronomer Clifford Stoll joined the naysaying tradition in a 1995 Newsweek op-ed with this doozy of a statement about the internet.

“The truth is no online database will replace your daily newspaper, no CD-ROM can take the place of a competent teacher and no computer network will change the way government works,” Stoll wrote.

When technology hits a roadblock, the naysayers get louder. And when markets crash, like the crypto market did in 2018, investors immediately take it as an indictment of a technology’s viability. It’s more of a gut reaction than anything else, but it’s powerful.

The general public has soured on blockchain and crypto-related technology, and Roubini has given this largely emotional response a pseudo-intellectual sheen…

Which makes him an irresistible target for me. But you know what?

I think I’ve done him wrong. I’ve unintentionally put Roubini in the position to do the impossible. To understand what I mean, let’s back up a little.

Bitcoin wants to replace government-issued (and controlled) money and middlemen of all stripes (though Satoshi Nakamoto had mostly bankers in mind). Nakamoto’s whitepaper spelled out in broad terms the technology that could do all this.

It is precisely these claims that Roubini is trying to prove false.

I always thought Roubini’s problem was that he was judging the beginning of a movie instead of the whole thing. And that beginning he’s judging is just a few minutes of a film that will be decades long.

On the basis of the first five minutes of the movie, Roubini can make a guess on how it turns out. But how could he possibly know?

To insist that he’s right after watching a mere five minutes of the movie is, simply put, laughable. Just because Roubini’s assertion cannot be proven wrong doesn’t mean he is right or should be believed.

The truth is, there’s no proving bitcoin’s (and other crypto user cases) claims. It’s just as unprovable as, say, the claim that a teapot is orbiting the sun but is too small to be seen by current telescopes.

This analogy comes from Bertrand Russell, one of my favorite philosophers. He argues that the burden of proof should be on the ones making the unprovable (unfalsifiable, in his words) claim rather than on others (in our case, Roubini) to disprove those claims.

Bitcoin does have some followers with unwavering faith. Everybody refers to them as “believers.”

They don’t rely on proof. Many of them are technologists. They believe in the technology, in themselves and in their ability to unleash the vast potential of blockchain technology (which underpins bitcoin) on the world.

And every day I look for evidence (as opposed to proof!) that their faith in the technology and in themselves is intact. Because, to tell you the truth, I’m not a believer. I need to see that progress is being made and will continue to be made.

The good news is, I’m seeing that progress. I could give you dozens of examples of companies whose blockchain user cases are in beta with plans to go live in the near future.

But instead, I’ll let you in on one of the best ways to track progress: the growing number of “commits” (or revisions) to blockchain projects and developer tool downloads. They total in the hundreds of thousands. Check out the trends for 1,458 individual cryptocurrencies here.

It’s not a guarantee that this massive activity will be successful in turning crypto into a global industry used by billions. Time will tell. And we have to be patient.

But while Roubini and others like him continue to argue about bitcoin’s value, bitcoin’s popularity (or lack thereof) has nothing to do with its real value. Its real value will be determined and driven by a global community of developers working behind the scenes to make bitcoin’s impact felt on a massive scale.

Amid the disappointment of falling prices, the important work of bringing this technology to the masses is advancing.

Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) is a behemoth tech company and after the fourth-quarter selloff, investors are wondering if now is the time to buy Google stock. Let’s explore a few reasons why it may be time to pull the trigger.

Balance Sheet

Let’s start with its balance sheet, quietly one of Alphabet’s top assets. While some companies like Apple (NASDAQ:AAPL) have opted to buyback loads of its own stock, Alphabet has let its cash hoard grow and grow. As of last quarter, it has about $106 billion in cash and short-term investments and just under $4 billion in long-term debt.

In other words, Alphabet is sitting on a $100 billion pile of cash. This gives the company staying power in a recession, as well as flexibility to invest in itself or via M&A.

Google Stock Has Assets

Let’s not forget the company’s assets either. Alphabet owns the world’s most popular website, Google.com, as well as the second most-popular website in YouTube.com. Owning those two properties in the internet world is like owning Park Place and Boardwalk in Monopoly.

However, its investments have paid off too. For instance, its self-driving car unit Waymo was valued as high as $175 billion. It owns Android, the most popular smartphone operating system in the world. Its collection of Google assets, Google Drive (think Docs), Gmail, Maps, Chrome, etc., have more than a billion users each.

Growth, Valuation and Google Stock

This next part is a two-part catalyst: Growth and valuation.

For 2018, analysts are calling for sales growth of 23% to $136.5 billion. That goes along with 29.6% earnings growth, with estimates calling for earnings per share of $41.80. In 2019, analysts expect 19% revenue growth to $162.8 billion and earnings growth of 13%.

These are solid numbers from a company this big, with Alphabet toting a market cap of $750 billion.

That said, some investors may balk at its valuation of 25 times earnings. But why? Investors continuously buy shares of Procter & Gamble (NYSE:PG), Walmart (NYSE:WMT), Clorox(NYSE:CLX) and others with P/E ratios near or north of 20 because they’re “safe” plays. That’s despite sluggish growth and pressured margins too.

I don’t have a problem paying 25 times earnings for GOOGL, a blue-chip technology company with the internet’s best assets, strong growth and a rock-solid balance sheet.

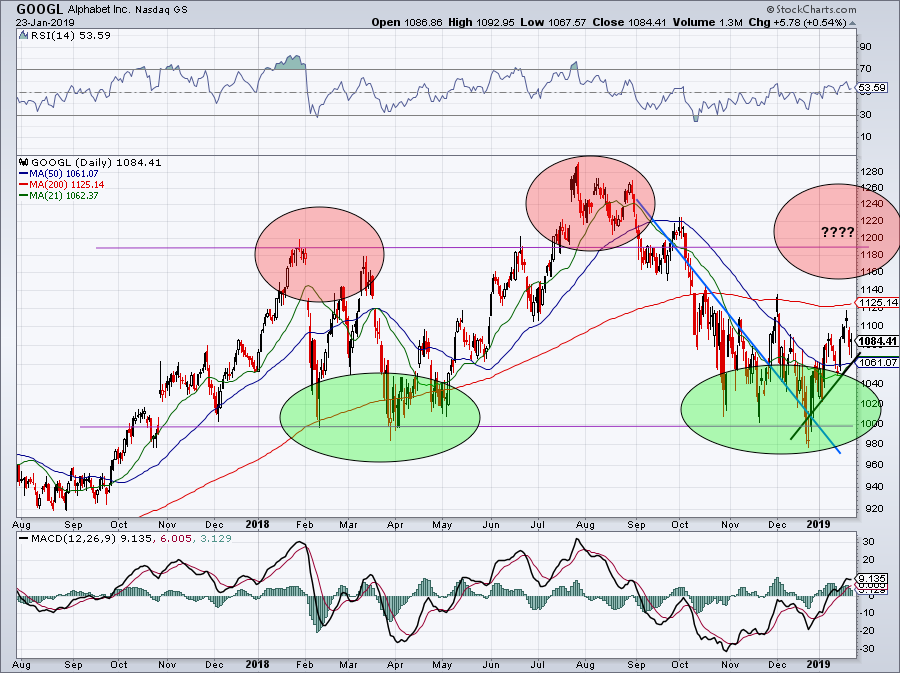

There are a lot of common-sense reasons to like Google stock, but what do the charts say? Fortunately, investors can still get Alphabet stock at a good price today.

As we have laid out at least a dozen times here on InvestorPlace, GOOGL stock remains a strong buy at the $1,000 level. Since hitting this mark in December, we’re only $85 per share off that level. If investors are debating a long-term position in Alphabet, I wouldn’t hesitate to initiate a position on a slight pullback here. That’s even with earnings coming up in early February.

Shares are riding short-term uptrend support higher (black line) and are back above the 50-day moving average. Remember, GOOGL stock has a 52-week high near $1,300.

The way the stock is bouncing between $1,200 and $1,000 does make me a little hesitant (green and red circles). That said, this is a long-term winner and I do not bet against GOOGL over the long-term.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL and GOOGL.

While stocks were likely oversold to end 2018, the action in January has been far more bullish than many expected. It’s easy to say that there’s too much buying going on, just as many thought there was too much selling over the last three months of last year.

But, stocks have a way of moving in waves, especially when volatility is higher than normal. We had a selling wave in December and now a buying wave in January. Are we going to have another selling wave in February or is the rally going to continue? Or, are we going to move sideways for a while?

Predicting market direction is never an easy task. That’s true no matter how much experience you have, how advanced your research tools are, and how many resources you have access to. There are simply too many variables to know for certain.

However, market volatility can be more predictable. That doesn’t mean it’s easy to trade volatility or volatility products. However, volatility models do tend to perform better when it comes to forecasting than directional models.

That means if I come across a big volatility trade (using ETFs or otherwise), I certainly pay attention to it. Large volatility trades can give you a clue as to what the smart money is expecting, at least in terms of future market volatility.

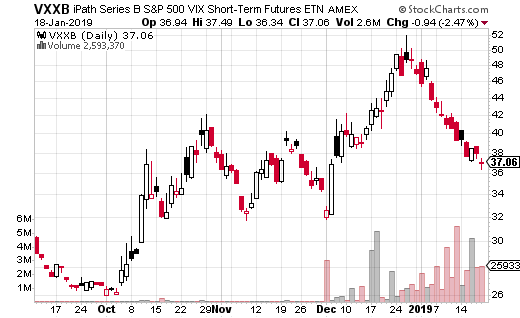

Let’s take a look at a very interesting volatility trade that I recently came across in iPath Series B S&P 500 VIX Short-Term Futures ETN (NYSE: VXXB).

First off, VXXB is taking over for VXX, which expires at the end of January. VXX is actually a note that had a 10-year life, which is about to end. VXXB will replace VXX and will be the exact same thing. In fact, when VXX goes away, VXXB will drop the B and become the new VXX.

VXXB is the easiest way to trade volatility since it trades like a stock. It tracks the first two futures that make up the VIX calculation, so is representative of short-term volatility.

A sophisticated trader just made a ratio call spread trade in VXXB which I think is quite illuminating. A ratio spread means the legs of the spreads aren’t all an equal amount, as you’ll see. More specifically, with VXXB at $37.25, the trader bought the March 15th 38 call 5,000 times while selling the 43 call 10,000 times.

Because twice as many 43 calls were sold versus the 38 calls, the trade generates a credit of $0.80. That means if VXXB is below $38 at March expiration, the trader earns $400,000. What’s more, the trade can make additional money from $38 to $43, with max gain at $43. In the best case scenario, the trader can make $2.5 million in appreciation plus $400,000 in credits for a total of $2.9 million.

The risk from the trade comes from the 10,000 calls sold at 43. Only 5,000 of those are protected by the purchase at 38. The other 5,000 are exposed to however high VXXB could realistically go. The trade loses $500,000 per $1 in VXXB above $43.

This ratio call spread is interesting because it can be considered both bullish and bearish on market volatility. The credit aspect of the trade is moderately bearish or neutral on VXXB. But, the long call spread feature is clearly bullish (but not too bullish). But, the trader definitely doesn’t want to see a spike in volatility due to the unlimited loss potential on the upside.

Given the risk of the trade, the strategist making this trade clearly doesn’t believe volatility is going to spike and remained elevated prior to March expiration. Still, this isn’t the sort of trade a casual trader should make.

Instead, stick to a straight 38-43 call spread in VXXB if you’re bullish on VXXB or want to hedge a long stock portfolio. For those bearish on market volatility, you can use a put spread to take the opposite side for relatively cheap.

In late 2018, financial markets tumbled on concerns regarding rate hikes, trade tensions and slowing global economic growth. The biggest victims in that market sell-off were growth stocks, which essentially required low rates and continued healthy global growth to sustain their valuations. Those things were being called into question in late 2018. As such, many of the market’s high-flying glamour stocks fell 20% or more.

Sentiment has changed sharply in 2019. Stocks had a huge, decade-large rebound rally the day after Christmas. Stocks have remained on an uptrend ever since because the Federal Reserve has sounded a much more dovish tone regarding rate hikes, U.S. and China trade talks are progressing well, and the U.S. economy appears to still be quite strong.

All in all, the risks which plagued markets in late 2018 are easing in early 2019. As they have, financial markets have rallied, and growth stocks — which were the biggest losers in late 2018 — have been among the biggest winners in early 2019.

This trend should continue. As bullishness returns to the market, money will continue to flow into growth stocks, and growth stocks will outperform.

With that in mind, let’s take a look a 10 growth stocks that could win big as markets rebound in 2019.

One growth stock that should perform well in both 2019 and over the next five to 10 years is Canadian based e-commerce solutions provider Shopify (NYSE:SHOP).

The long-term growth narrative supporting SHOP stock is quite promising. E-commerce is the future. More than that, decentralized e-commerce is the future. Today, the e-commerce market is dominated by a few big players. That won’t remain the case forever. Eventually, everyone and anyone in the retail world will have a digital footprint, and that means that over the next several years, there will be a huge influx of new digital retail operations.

Shopify provides the building blocks for those digital retail operations. As such, Shopify’s addressable market should grow by leaps and bounds over the next several years. Considering Shopify is the head-and-shoulders leader in this space, huge growth in the addressable market will translate into huge growth for the company. Reasonably speaking, huge growth at the company will lead to huge gains for SHOP stock.

The stock is already up over 25% since bottoming on Christmas Eve. Thus, a near-term pullback is healthy here and now. But that pullback should be bought, because the stock will ultimately head way higher in a multiyear window.

Tesla (TSLA)

Source: Shutterstock

Next up on this list is one of the more controversial names on Wall Street, but nonetheless one that represents huge upside potential in a multiyear window.

There has been no shortage of controversy surrounding Tesla (NASDAQ:TSLA) over the past several quarters. But in the big picture, Elon Musk has remained at the head of the company, Model 3 production and delivery ramp has been wildly successful, the company has managed to turn a profit, international expansion is progressing as planned and cash burn issues are no long front and center. Those are all positive developments. As such, Tesla stock is currently at the upper tend of its 52-week trading range.

This strength in Tesla stock will persist in the long term. At its core, this company is at the center of a huge electric vehicle growth narrative that will inevitably and perhaps rapidly sweep across the globe over the next several years. As it does, Tesla will announce more vehicles with better prices, and the company will grow its market share dramatically. Revenue growth will huge. Profit growth will be huge. Tesla stock will march higher.

Tesla stock is up 16% since Christmas Eve. That’s a pretty big rally. Much like Shopify, a near-term pullback is warranted. But, also like Shopify, that pullback is a buying opportunity, since long-term growth trends imply massive multiyear upside.

One of the biggest losers in late 2018 was payments processor Square (NYSE:SQ). But, that also means that this stock has an opportunity to be one of the biggest winners in 2019.

Square is at the heart of tomorrow’s commerce world, which will inevitably be cash-less and dominated by card and digital payments. Right now, Square dominates on the physical card payment side of things. The company is famous for its payment processors, which allow essentially any retailer with a smartphone to accept card payments. Go to any mall or street market. You will see Square machines everywhere.

The proliferation of these payment processors will continue over the next several years as cash becomes increasingly less used. But, that’s just one peg of this growth narrative. The other peg has to do with e-commerce. For a long time, Square didn’t really have an e-commerce presence. Until now. The company recently launched an in-app payments system that looks very much like PayPal (NASDAQ:PYPL). In so doing, the company has plunged itself into the e-commerce growth narrative too, and only added more firepower to the long-term growth narrative.

Square stock is up over 30% since Christmas Eve. That’s a huge rally. A pullback is warranted here. But, much like the other stocks on this list, pullbacks in Square are buying opportunities.

Salesforce (CRM)

Source: Shutterstock

A discussion of big-growth stocks has heavy overlap with a discussion of cloud stocks, and if you were to have a discussion regarding cloud stocks, that conversation would likely be dominated by Salesforce (NYSE:CRM).

CRM stock is truly at the heart of the cloud and data revolutions. Salesforce leverages data and analytics to deliver robust cloud solutions to enterprises that want data-driven insights on their customers. In this sense, the company takes data and turns it into insights via cloud solutions. That promises to be one of the most valuable processes in a world defined by Big Data.

There’s a lot of competition in this space, but Salesforce has time and time again squashed the competition. Despite rising competitive threats and tougher laps, revenue growth at Salesforce has hardly slowed over the past several years. Back in 2014, revenues grew by 33%. In fiscal 2018, revenues grew by 25%. They are projected to grow by more than 25% this year. Resilient revenue growth in a secular growth industry implies that this company has huge long term potential.

CRM stock is up 22% since Christmas Eve. But, it remains well off its all time highs, and technical indicators don’t scream overbought. As such, this stock has more runway to the upside in the near to medium terms.

Trade Desk (TTD)

Source: Shutterstock

Programmatic advertising is the future of the entire advertising industry, and the company at the forefront of the programmatic advertising revolution is The Trade Desk (NASDAQ:TTD).

Ads used to be transacted through individuals and firms. You call somebody, you discuss, you negotiate a price and then you have an ad. Now, ads are bought and sold by computers. This computed-powered ad buying is called programmatic advertising. It’s the future. Through leveraging AI and data, programmatic advertising makes ad buying and selling quicker, more convenient and cheaper than ever before.

In this space, Trade Desk has emerged as a clear leader. But Trade Desk only has a $6 billion market cap. The global advertising industry measures in at $1 trillion. Eventually, all $1 trillion worth of ads will be transacted programmatically, and most of that programmatic spend will happen through Trade Desk. Thus, this is a small company attacking a huge market, and that implies huge gains ahead for TTD stock.

Right now, the stock is up 27% since Christmas Eve, and is entering a near-term overbought position. Thus, a near-term pullback is likely in the cards. But, much like other pullbacks in this stock before, the next pullback will simply be a buying opportunity.

Despite weakness in the stock, the long term bull thesis surrounding streaming giant Netflix(NASDAQ:NFLX) is only getting stronger every day.

The Netflix growth narrative is all about two things: cord cutting and content. So long as consumers cut the chord and pivot to streaming, and so long as Netflix’s content is superior to content offered by streaming peers, Netflix’s subscriber base will grow. Prices will go up without churn, too, and margins and profits will explode higher.

Those two trends are progressing favorably for Netflix. The cord-cutting trend isn’t slowing. If anything, it’s accelerating. Moreover, Netflix’s content isn’t getting worse. Again, if anything, it’s only getting better, thanks to recent hits like Bird Box and Black Mirror. As such, the two long-term growth trends here remain favorable, meaning that the long-term bull thesis on NFLX stock is only gaining credence and visibility.

NFLX stock is up a whopping 52% since Christmas Eve. This stock has fundamentally supported upside from here. But it is technically overbought, and needs to cool off and consolidate before taking another leg higher.

Roku (ROKU)

Source: Shutterstock

Among the biggest losers during the market sell-off in late 2018 was streaming player maker Roku (NASDAQ:ROKU). But the growth narrative underlying the company only strengthened in late 2018, thus implying huge rebound potential in 2019.

Much like Netflix, there are only two trends that matter in the long run with Roku: cord cutting and competition. As stated earlier, the cord cutting trend is only accelerating. That means more streaming subscribers than ever, and more streaming services than ever, too. All those subscribers need a content-neutral centralized aggregation system to curate and access all those streaming services. As such, so long as consumers keep cutting the cord, demand for Roku devices will head higher.

On the competition front, Roku has tons of competition. But, the company still commands 40% share in the streaming device market and 25% share in the smart TV market. So long as the company can defend its market leadership position, Roku will continue to convert the lion’s share of cord cutters into Roku ecosystem users.

ROKU stock is up nearly 50% since Christmas Eve. The stock needs to cool off and consolidate here. But, once that consolidation period is over, this uptrend will resume for the duration of 2019.

While many other growth stocks remain well off their all-time highs, cloud giant Twilio(NASDAQ:TWLO) is right near its all-time high, and that’s a testament to the strength of this company’s underlying growth narrative.

Over the past several quarters, Twilio has emerged as the uncontested leader in the rapidly growing and potentially huge Communication Platforms-as-a-Service (CPaaS) market. The CPaaS market largely consists of companies that are integrating real-time communication into their services. This market promises to be huge to continuous shifts towards cloud-based communication, personalized customer experience and digital engagement.

Twilio is growing its customer base and revenues rapidly in this secular growth market. They also have a 95%-plus retention rate and very high gross margins. Put that all together, and this company has all the ingredients to be a big time winner in a long-term window.

TWLO stock is just below all-time highs today. This resilience is impressive, and it means that the stock hasn’t rallied as much as the other stocks in this list over the past two weeks. As such, you don’t have any near term overbought conditions, and now could be as good a time as any to load up for the long haul.

Nvidia (NVDA)

Source: Shutterstock

Once high-flying chipmaker Nvidia (NASDAQ:NVDA) saw more than half of its value wiped out in late 2018 thanks to near-term inventory, growth, and margin issues. But, in the big picture, those issues are overstated, and NVDA remains one of the best growth stocks in the market.

The growth narrative at Nvidia is all about AI and data. Recent numbers suggest there is absolutely zero slowdown in those businesses. All businesses related to AI and data, including the data-center and automated driving businesses, reported record numbers and huge growth last quarter. Instead, all the issues with Nvidia have to do with a pop in cryptocurrency mining demand that created inventory issues which will take time to work through.

Nvidia will inevitably work through those issues. Once they do, the narrative will re-focus on this company’s long term growth drivers in AI and data. Those drivers have been very strong, are still very strong, and will remain very strong, given secular shifts towards data-driven decision making and automated technologies. So long as those drivers remain strong, NVDA stock will head higher.

NVDA stock is up 20% since Christmas Eve. That’s a solid rally. But, the stock isn’t flashing any overbought signals. As such, it looks like this rally can and will continue in the near term.

Amazon (AMZN)

Source: Shutterstock

The world’s most valuable company — Amazon (NASDAQ:AMZN) — is also one of the market’s most attractive and promising growth stocks.

We all know Amazon for its e-commerce and cloud business. Between those two businesses, Amazon has a ton of long term growth potential as e-commerce becomes the global retail norm and cloud becomes the enterprise norm.

But, that’s just the tip of the iceberg for Amazon. The company also has a $10 billion and rapidly growing digital advertising business with presumably sky-high margins. There’s the offline retail business, which started with bookstores, moved to Whole Foods and will eventually include thousands of convenience stores and potentially evenTarget (NYSE:TGT). There are also potential multi-billion logistics and pharmaceutical businesses in the pipeline. Between all these growth opportunities, it’s easy to see that Amazon is still in the early innings of arguably the market’s biggest and most exciting growth narrative.

AMZN stock is up 20% since Dec. 24. But, it’s also still 20% off recent highs. Thus, while a near term pullback is warranted and healthy, this stock still has plenty of room to rally in a medium to long term window.

As of this writing, Luke Lango was long SHOP, TSLA, SQ, PYPL, TTD, NFLX, ROKU, NVDA, AMZN and TGT.

Recent incidents involving autonomous vehicle crashes, have made industry participants assume a lower profile. While these setbacks may slow progress in the sector, it does not mean the companies involved are taking their foot off the gas pedal in developing technology to move autonomous vehicles forward.

Any advanced technology industry will encounter growing pains, and as I said in my latest report, this space is just getting interesting. Allied Market Research puts the global autonomous vehicle market at $54 billion this year and $556 billion in 2026, growing at 40% per year. Even if these numbers are off by 25%, we’re still looking at a rapidly growing market.

And while the regulatory issues are real, there is growing economic pressure to solve the regulatory puzzle. Over 68% of freight travels on U.S. roads for an extended period of time. And with the trucking industry unable to fill driver positions, even with increasing pay and benefits, the American Trucking Association reports delays and costs are rising.

This lack of drivers, combined with an explosion in delivery of everything conceivable that consumers may purchase, as we recently looked at in our piece on the sharing economy, is placing growing pressure on regulators to formulate solutions to the autonomous vehicle problem. Trusting these issues will be resolved, let’s take a look at a few companies that are forging ahead in the autonomous vehicle space.

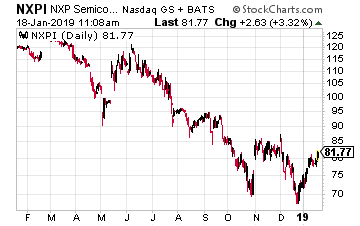

NXP Semiconductors (Nasdaq: NXPI)

Netherlands based NXP Semiconductors is the world’s largest supplier of automotive semiconductors, and will have a major role to play as cars and trucks move to autonomy. One of the things I like about NXP is the fact that it is already deeply embedded in the auto industry. This gives the company insight into customer needs as autonomous vehicles move through the Levels of Autonomy I detailed in my previous article.

NXP is aggressively expanding its relevance in autonomous vehicles, both through internal development of products as well as through acquisitions. Late last year the company acquired OmniPHY, a pioneer in high-speed automotive Ethernet IP. Through the acquisition, NXP is ensuring it can maintain the speed and number of connections necessary as vehicles become increasingly autonomous.

As Ian Riches, Executive Director of Strategy Analytics Global Automotive Practice puts it, “One of the vexing questions of the Autonomous Age is how to move data around the car as fast as possible. Cameras and displays will ramp the number of high-speed links in the car to 150 million by 2020 and by 2030 autonomous car systems will aggressively drive that number to 1.1 billion high-speed links.”

By purchasing OmniPHY, NXP is enhancing its capability to capture the entire value chain in the connected automobile. Controlling connectivity points is a major strategic competitive advantage, and allows NXP to work not only with automakers, but with other equipment and sensor companies, cementing NXP as a vital player in the autonomous vehicle ecosystem.

From a valuation perspective, NXP trades at a 13 PE ratio, and pays just over a 1% dividend. The company has grown earnings per share an average of 62% over the past 5 years, and currently has profit margins of over 28%. NXP shares have never fully recovered from a failed merger attempt with Qualcomm (Nasdaq: QCOM) in 2018 after a prolonged, almost 2 year courtship. The deal fell through and many NXP stock owners, who had been in the stock only for the merger, abandoned ship. The stock appears to have bottomed around $70, and now trades close to $80, well off the pre-merger prices in the $120s.

A combination of value and strategic market positioning makes NXP a buy at these levels. The company has ensured its relevance in the autonomous vehicle market and should reap the benefits as this market matures.

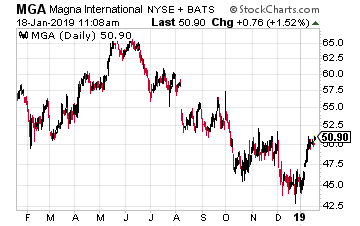

Magna International (NYSE: MGA)

Magna International is a Canadian company that wants to ensure the autonomous vehicle is not only safe and secure, but retains the style and design each automotive manufacturer has heavily invested in. As Magna explains, it does not want the autonomous car to look like a science experiment with vehicle sensors, such as LIDAR, mounted obtrusively all over the car.

Using what it terms MAX4, Magna has developed a self-driving system that can enable up to Level 4 autonomous capabilities, while at the same time disguising the fact that the automobile is anything different than what the manufacturer has on the showroom floor today. The MAX4 system can be mounted on an automobile, such as a Jeep Grand Cherokee, with the LiDAR, radar, and ultrasonic sensors all contained within the bumpers and other currently existing cavities of the car.

While I’m not a huge fan of the company, the Tesla (Nasdaq: TSLA) business model does demonstrate consumers want not only the latest technology, they want functionality wrapped in design. And they will pay premium prices for this combination. Magna ensures that each automaker can retain and enhance vehicle look and design, without concern that the sensor requirements of the autonomous vehicle impinge on their branded look.

And, Magna is not only offering the ability to retain design, the company is also forward thinking in addressing the changing needs, and look and feel, of the interior of future autonomous vehicles. The company recently released its flexible seat configuration design for autonomous vehicles.

The seating system allows for three variations in seating patterns that are fully automatic, with seats moving electrically along tracks mounted in the vehicle floor. Consumers have the option of a “campfire” seating arrangement with all seats facing the middle of the vehicle, a “cargo” configuration where seats move to the front of the car to provide a large cargo area in back, and a seating configuration with electronically insulated sound barriers which allows for private phone conversations in a ride sharing environment. Magna is closer to the ride share business than other companies, with a $200 million private investment in sharing economy company Lyft (Nasdaq: LYFT, pre-IPO).

Magna currently trades with a PE of 7 and pays just over 2.5% in dividends each year. The company has averaged 14% earnings growth over the past 5 years, and is projected to grow earnings 13% this year. As with NXP, a pullback in the stock in 2018 is providing an excellent entry price at these levels. Magna’s innovative designs and technology should provide earnings expansion as the company outfits the car of the future.

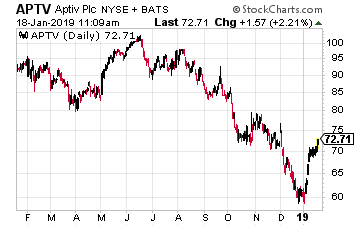

Aptiv (NYSE: APTV)

Finally, I would like to revisit a portfolio holding of the Growth Stock Advisor service, Aptiv. Aptiv is an Ireland based company that was spun out of Delphi Technologies (NYSE: DLPH), formerly Delphi Automotive, in late 2017.

Delphi Technologies is now the “powertrain” part of the business providing propulsion, combustion and electronic solutions. This is the old industrial commodity side of the business, and the stock has performed abysmally since the spinoff of Aptiv.

Aptiv is, as former Delphi Automotive, and now Aptiv CEO Kevin Clark stated, focused on “active safety, autonomous driving, enhanced user experiences, and connectivity”. Aptiv provides the sensors, connectivity, and most importantly deep industry and product expertise, which is so important to establishing credibility and trust from automotive manufacturers moving into the autonomous vehicle space.

As I detailed in my latest report on autonomous vehicles, there are hurdles to full autonomy, one of which is working out the legal liability issues that arise from a fully autonomous vehicle. But, Aptiv is making the incremental improvements that ensure the autonomous vehicle will be ready when the regulatory issues are resolved.

After getting the lowdown at CES on the Aptiv fleet of Lyft cars that is ferrying passengers around Las Vegas, Extreme Tech put the Aptiv advancements over last year this way, “For example, implementing RTK (Real-Time Kinematic GPS augmentation) has allowed the cars to locate themselves within 2.5 cm (instead of 10 cm). That makes the difference between not knowing and knowing whether a pedestrian is standing on the edge of the curb or in the crosswalk.” Advancements like these are crucial to the developing regulatory framework, and to putting fleets of autonomous vehicles on every road, not just in test environments like that taking place in Las Vegas.

Aptiv is continually advancing technology, and with deep roots in the automotive industry, it is one of the purest autonomous vehicle plays available to investors. The company has a forward PE of 13, and is expected to grow earnings this year 31%.

Each of these companies offers a great way to play advancements in the autonomous vehicle industry as it matures in the coming years. Whether through the brains and connectivity of NXP, the technology and design of Magna, or the autonomous integration provided by Aptiv, it’s hard to go wrong with these top players in the space.

Markets were closed Monday for the Martin Luther King, Jr. holiday, but may take their cue from overseas markets when they reopen for business Tuesday. European markets were flat to lower as they digested final GDP numbers out of China for 2018. The Chinese economy grew 6.6% in 2018, its slowest growth in almost 30 years.

When markets reopen Tuesday, they will also return to the stalemate in Washington, with nothing being resolved over the long holiday weekend. President Trump’s offer to extend the DACA program for three years in exchange for funds to build a border wall with Mexico was announced dead on arrival by Democratic leaders.

In addition to impacting federal workers and the businesses they frequent, the extended shutdown is preventing companies, like Uber (UBER, pre-IPO) and Lyft (LYFT, pre-IPO), from proceeding with their IPOs. A skeleton staff at the Securities and Exchange Commission (SEC) is on duty to police market misconduct, but not to approve IPOs and other registration filings.

Tuesday analysts will see the release of Redbook retail data. A major economic victim of the government shutdown has been retail data. The Redbook data has therefore taken on more importance in recent weeks. Last week showed a 6.7% rise in sales year-over-year. This weekly data is being watched closely for any cracks in consumer confidence. Also released Tuesday are existing homes sales numbers.

Investors will get a reading on brokerage earnings Tuesday when TD Ameritrade (AMTD) and Interactive Brokers (IBKR) report. With several reports showing investors moving to the sidelines in late 2018, analysts will be monitoring the level of trading activity at these brokerage firms, given the swift rebound so far this year. Did investors reengage in the market, or are they still waiting for an all clear? Also releasing earnings Tuesday are Johnson & Johnson (JNJ), International Business Machines (IBM) and The Travelers Companies (TRV).

Proctor and Gamble (PG), United Technologies (UTX), Texas Instruments (TXN), ASML NV (ASML) and Las Vegas Sands (LVS) report earnings Wednesday. Like the other casino stocks, Las Vegas Sands started trending lower in mid-2018, but looks to have found a bottom in the mid-$50s. The company is expected to report $.86 per share on Wednesday. Investors will be looking for an update from United Technologies on its plans to separate into three different companies. Announced in 2018, the company has said that the reorg could take as much as two years to complete.

Mortgage applications, the FHFA House Price Index, and the Richmond Fed Manufacturing Index will all be released Wednesday. With both orders and shipments contracting unexpectedly in December, when the Index came in at -8, investors are keeping a close eye on the Richmond Fed numbers for January. Projected to bounce slightly to -3, the number is an important gauge of where the economy may be heading in early 2019.

Think you can’t retire on anything less than a million bucks?

Many people would answer that question with a “yes.” If you’re one of them, I have great news: the “million-dollar myth” is just that, a myth.

I’ll tell you why in a second. Then I’ll reveal 4 buys throwing off a safe cash dividend yielding 8.5%—letting you fund your golden years on a lot less.

(These 4 are the tip of the iceberg, by the way. At the very end of this article, I’ll give you 20 more retirement lifesavers paying gaudy 8% average dividends, as well!)

A Million-Dollar Retirement … on $470K!?

So how much smaller of a nest egg am I talking about here?

How does $470K sound? If you’re keeping track at home, that’s 53% less than the suits say you need if you want to spend your golden years above the poverty line.

Better yet, our 4-buy “instant” retirement portfolio will pay us in equal amounts every month. It’s just like getting a regular paycheck, but you don’t have to do a thing—besides log into your brokerage account and pick up your cash!

Beyond the Big Names

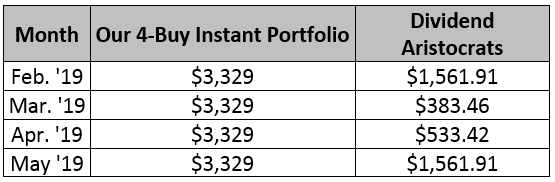

A big reason why the million-dollar myth exists is that most folks predict their future income stream based on the pathetic yields popular stocks, like the so-called Dividend Aristocrats, dribble out today.

And it is true that traditional dividend plays don’t come close to the 8.5% average payout thrown off by the 4 off-the-radar buys I’ll show you in a moment.

Let’s take a 4-pack of typical Dividend Aristocrats and map how much they’ll pay investors (based on that $470K nest egg I mentioned earlier) in the next few months.

4 Clicks to Smooth, Safe Monthly Payouts

The best part is that this strategy isn’t capped at $470,000. If you have managed to save a million bucks, you can buy more monthly payers like these and kick your monthly income to $7,083.

So let’s move on to the 4 stocks I have for you now—well, they’re not stocks, exactly, but closed-end funds (CEFs).

CEFs are muscular income plays that give us two advantages: outsized dividends (CEF payouts of 8%+ are common) and big discounts to net asset value (NAV), a powerful upside predictor far too few people watch.

Your Monthly “4-Pack” for an 8.5% Average Dividend

The Western Asset Emerging Markets Debt Fund (EMD) yields a gaudy 9.1% today and trades at a 13.1% discount to NAV as I write.

In English: we’re getting its portfolio of emerging market corporate and government bonds for 87 cents on the dollar!

The upshot here is that plateauing US interest rates (traders betting through the futures markets have the Federal Reserve pegged for zero hikes this year) will send income seekers abroad for higher yields—and that’s great news for EMD.

Either way, management has shown its chops since the current rate-hike cycle started three years ago, with the fund’s price (in orange below) slipping just 2.3%. But add in that monster dividend and its total return jumps to 26%!

EMD Shrugs Off Rate Woes

And EMD pulled this off in a tough time for emerging-market debt! But now, with US rates on hold and EMD’s absurd discount, the fund is poised to deliver some nice price upside, on top of its 9.1% monthly dividend.

Now let’s come back home to another sector primed for gains thanks to slowing rate hikes: US real estate. We’ll ride that trend with the Cohen & Steers Total Return Realty Fund (RQI), and its 8.5% monthly dividend.

US real estate underperformed last year, due to the same rate-hike fears that hobbled emerging-market debt:

Rate Fears Hogtie REITs

But I sensed that the Fed was about to change tack during last fall’s stock-market meltdown, which is why I pounded the table on RQI on December 28. Since then, the CEF (in red below) has dominated the benchmark Vanguard Real Estate ETF (VNQ), in blue, and the SPDR S&P 500 ETF (SPY), in orange.

Not Too Late to Grab This Winner

Sure, that rise has thinned RQI’s discount, but you’re still getting an 8.5% payout here, and the current discount (8.7%) points to more upside: just under a year ago, RQI traded at just 1% below NAV. A rise to that level (a certainty, in my view) would give us a 6% price gain while we pocket that huge payout.

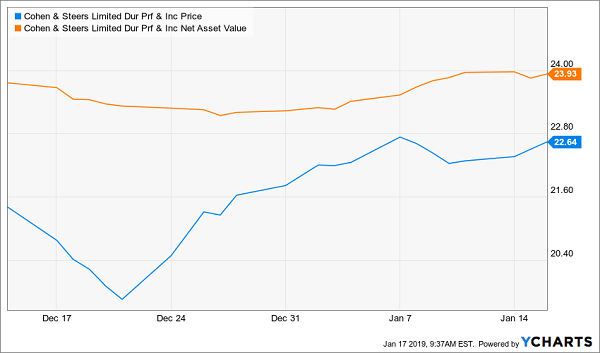

Moving along, let’s add some top-quality finance names through another CEF from Cohen & Steers: the Cohen & Steers Limited Duration Preferred & Income Fund (LDP).

As the name suggests, LDP bypasses finance companies’ regular shares in favor of their preferred stock.

Think of preferreds as stock/bond hybrids that can trade on an exchange, like stocks, but do so around a par value and dole out a fixed regular payment, like bonds.

Their biggest appeal? Outsized payouts. And you can boost those dividends even more if you buy through a CEF like LDP, which pays an outsized 8.3% now.

Another great thing about CEFs in general (and LDP in particular) is that CEF investors tend to be slow to respond to investor mood swings, which is why we can grab LDP at 5.4% below NAV—but your shot at buying cheap is evaporating!

LDP’s Buy Window Is Closing

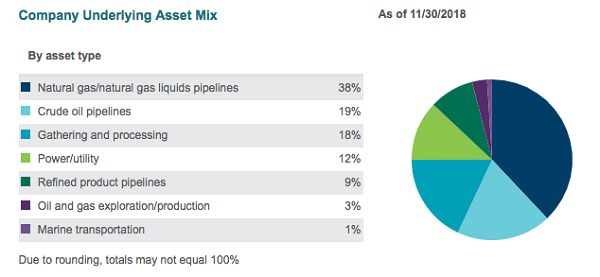

Finally, let’s tap the Tortoise Power & Energy Infrastructure Fund (TPZ) for its 8.1% payout, while we can still do so at a 7.8% discount.

TPZ holds stocks and bonds issued by oil and gas pipelines, storage and processing firms—mostly master limited partnerships (MLPs)—plus some utility stocks:

Source: Tortoise Advisors

Most MLPs will kick you a K-1 tax form around your return deadline and annoy you and your accountant. But TPZ gets around this by issuing you one neat 1099.

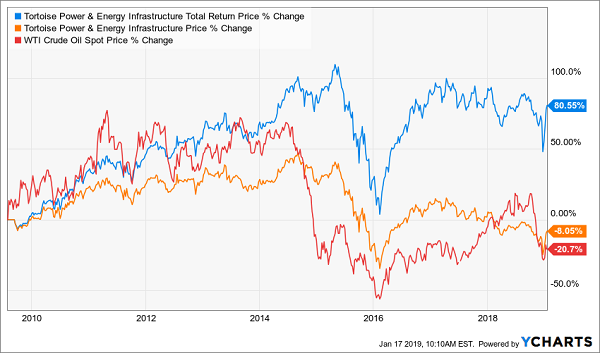

Since MLPs pipe energy, they tend to trade with oil prices. But TPZ’s management has done a great job of dampening oil’s drop since the fund’s inception in 2009.

Below we can see that TPZ’s market price (orange) has dipped 8.1% since launch, but that’s way better than the goo’s 21% crash (in red). And when you add in TPZ’s big dividend, you can see that management has handed investors a solid 81% return in just under a decade.

TPZ Bucks the Oil Plunge

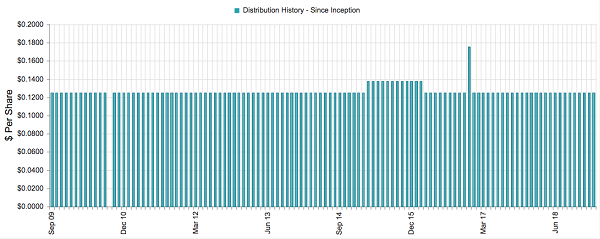

The kicker? The whole time, this dividend has been a picture of serenity:

Oil Crash? What Oil Crash?

Source: CEFConnect.com

Of course, no one knows where oil will go from here, but I expect it to find a bottom in 2019. That means now is the time to make a move—because we could easily look back years from now, at the high yield and nice discount TPZ sports today, and wish we’d pounced.

Markets that were already moving up, got a boost Friday when it was reported Chinese trade negotiators had offered to address the trade imbalance with the U.S., and essentially eliminate the imbalance by 2014. The offer to purchase $1 trillion of U.S. goods, provided hope to investors that the trade dispute will not only be settled, but will be a boon for the U.S. Trade bellwether Caterpillar (CAT) was up over 2% on the news. And, markets finished up over 1% across the board. With this bounce off of the late December lows, pundits are now concerned markets may be overshooting to the upside and setting up for potential headline risk to send them lower. Cheerleaders of the bull move point to earnings, which though uneven, have been coming in somewhat better than expected, and do not appear to be indicating a recession is in the cards in 2019.

U.S. Markets are closed Monday for Martin Luther King, Jr. Day. But, the release of economic numbers resumes Tuesday with Redbook retail data and existing home sales. The November data, showing 5.32 million homes sold, was down 7% year-over-year and epitomized the state of housing sales, which fell off a cliff in the final quarter of 2018. Analysts are anticipating a positive effect from falling mortgage rates which may boost the December number. Wednesday, the housing data continues as investors will analyze mortgage applications and the FHFA House Price Index data. The Richmond Fed will release its manufacturing Index Wednesday morning.

Earnings are set to flow Tuesday as we hear from Johnson & Johnson (JNJ), International Business Machines (IBM), UBS AG (UBS) and Capital One Financial (COF). Investors will be expecting JNJ to provide an update in the ongoing battle over contaminated baby powder, which plaintiffs claim was intentionally sold by the company. Proctor and Gamble (PG), Abbott Labs (ABT), Comcast (CMCSA) and United Technologies (UTX) all report earnings Wednesday. JP Morgan (JPM) raised its price target on P&G Friday, from $100 to $106. The consumer giant’s stock has flattened in the low $90s in recent months, after moving off of lows just above $70 in May of last year.

Market behemoth Intel (INTC) reports earnings Thursday after the close, and will be joined by Starbucks (SBUX) and Intuitive Surgical (ISRG). Though not a staple of tech stocks, investors are keen to learn if Intel will be raising its dividend for 2019. The company currently pays a rate of 2.48% annually to its shareholders. China will be the question on the earnings call when Starbucks reports Thursday. Analysts expect a 3% uptick in U.S. business, but fear this may be offset by a weak consumer in China. Colgate-Palmolive (CP), Ericsson (ERIC), and D.R. Horton (DHI) will close out the week when they report earnings next Friday.

Jobless claims, the PMI flash numbers, and leading indicators will all be released Thursday. The leading indicators are expected to tick up .2% for December. Also on the way Thursday is the Kansas City Fed Manufacturing Index. Durable goods orders and new home sales numbers will be released on Friday. Durable goods are expected to increase .8% month-over-month.

The end of last year brought something not seen in a while—a bear market. As a result, many investors were reeling as stock prices—particularly in the tech industry—massively declined. However, when stocks decline, there is one silver lining that benefits cash-rich investors: cheap stocks.

Many of the best stocks are now trading at low prices. Moreover, when companies with cheap stocks maintain or improve their growth rates, many investors often look to buy their shares. As we begin the new year, the following cheap stocks have those characteristics, leaving them well-positioned to skyrocket in the coming months and years.

Cheap Stocks to Buy: Bank of America (BAC)

More than ten years after the financial crisis, Bank of America (NYSE:BAC) is again on a list of cheap stocks. BAC has come a long way since it fell to $2.50 per share at the height of the crisis. Now, it trades at almost $29 per share. Moreover, it resumed annual increases of its dividend in 2014. Today, it returns 60 cents per share of dividends to its shareholders each year, yielding about 2.1%.

However, the forward price-earnings ratio of about ten is what really makes BAC one of the best stocks. The multiple is well below the stock’s five-year average of about 19.

Also, companies whose stocks have single-digit PEs rarely generate double-digit profit increases, but BAC is in that category. Wall Street analysts on average expect the bank’s profits to rise 10.6% this year. Moreover, according to the consensus estimate, BAC’s average annual profit increase over the next five years will be 20.7%.

The stock fell in 2018 amid a number of headwinds. Among these headwinds were the declining results of its investment banking unit, the negative market environment and fears of an inverted yield curve.

However, amid these headwinds, Warren Buffett continues to buy BAC, indicating that the Oracle of Omaha considers it to be one of the best stocks in the market. Also, one can likely assume BAC has become his favorite bank stock. He now has a bigger position in BAC than in Wells Fargo (NYSE:WFC), which used to be his favorite bank stock. Assuming the economy doesn’t nose dive, investors can, like Buffett, profit handsomely from one of the best stocks to buy in the market, BAC stock.

Cheap Stocks to Buy: CannTrust (CNTTF)

Although it’s not among the more inexpensive stocks in the S&P 500, Canadian cannabis company CannTrust (OTCMKTS:CNTTF) makes the cheap stocks list because it’s inexpensive compared to its peers in the marijuana industry. Unlike most cannabis companies, CannTrust is already profitable, and CNTTF stock has a forward price-earnings ratio of about 29.8. In an environment in which an industry leader, Canopy Growth (NYSE:CGC), trades at 100 times its sales, CNTTF is a screaming bargain and one of the best stocks in the market.

Canadian marijuana stocks have suffered from a “sell the news” phenomenon since the companies’ principal product became fully legal in their home market.

However, CannTrust is poised to benefit from many trends. For one, it has applied for a listing on the New York Stock Exchange. Joining the Big Board should open up CNTTF stock to a new class of investors. Secondly, although cannabis remains on the list of Schedule 1 drugs in the U.S., the recent legislation that legalized hemp should give all Canadian marijuana firms a foothold in the U.S. market.

The company’s focus on pharma also provides the stock with another potential catalyst. CannTrust sent its first shipment of cannabis oil to Denmark in the third quarter of 2018. It has also entered the Asia-Pacific market, through a partnership with Australia-based Cannatrek. Consequently, even if the company fails to meaningfully penetrate the U.S. market, it still can benefit from overseas expansion.

Furthermore, even though CannTrust’s valuation is lower than that of its major peers, its growth should remain strong for the foreseeable future. On average, analysts predict that its profits will increase by almost 155% this year, making CNTTF a very cheap stock, despite its forward price-earnings ratio of nearly 30. As CannTrust moves into other developed countries and possibly the U.S., a revived interest in cannabis should enable its valuation to catch up with that of its peers.

Cheap Stocks to Buy: Intel (INTC)

Few PC-era stocks have suffered as much as Intel (NASDAQ:INTC) has. Once the world’s largest chip maker, Intel stagnated as consumers increasingly turned away from PCs. Intel’s PC-era peers such as Microsoft (NASDAQ:MSFT), Nvidia (NASDAQ:NVDA), and even AMD (NASDAQ:AMD) built new business lines and resumed growing. However, INTC stock continued to languish. The high turnover of its top management, as well as security-related issues, also weighed on Intel stock.

However, INTC looks ready to again become one of the best stocks to buy in tech. The company has invested heavily in data-center technology. As a result, its Data Center group appears poised to overtake its PC Client group in size over the next few years.

Due to Intel’s purchase of Mobileye, INTC has become a leader in the autonomous-vehicle market. That, along with the company’s Internet of Things (IoT) products, should help INTC stock rise. And as the advent of 5G makes more advanced applications possible, Intel will benefit even more from these trends.

INTC is a cheap stock due to its price-earnings multiple. It trades at a forward PE ratio of about 10.6, showing that investors have yet to fully appreciate Intel’s comeback.

Due to a temporary glut of chips, Intel ‘s profit growth will be slow this year. However, its profits should resume growing by double-digit percentage rates in 2020. Once investors begin to realize that Intel has resumed a leadership role in the tech industry making it one of the best stocks in the market, it should again command valuations comparable to its peers in big tech.

{kind=link}