If you’re like most people, you’re wondering one thing right now: can stocks keep soaring following December’s nosedive—even after spiking 8% in January?

The answer? Absolutely.

To get at why I’m so sure, we’ll first go a couple steps further than headline-driven “first-level” investors do. Then I’ll give you a way you could double (or more) your rebound gains thanks to a terrific closed-end fund (CEF) yielding 7.2%—and “spring loaded” for 35% returns this year.

The Ignored Connection Between Jobs and Stocks

To get at what’s in store for the markets in 2019, we have to go back to 2009 and zero in on one thing: jobs. Because the crisis back then triggered a lost decade that only ended in 2017, when the unemployment rate finally got back to pre-crisis levels.

Then something strange happened—unemployment kept falling. In January, payroll data rose to one of the highest levels ever, blowing away even the rosiest estimates.

In such a job market, inflation seems like a sure thing. After all, when everyone who wants a job can get one and more jobs are created every day, employers will need to pay higher wages to keep the workers they have. And consumers will open their wallets, confident they’ll be earning more. But we’re not seeing that:

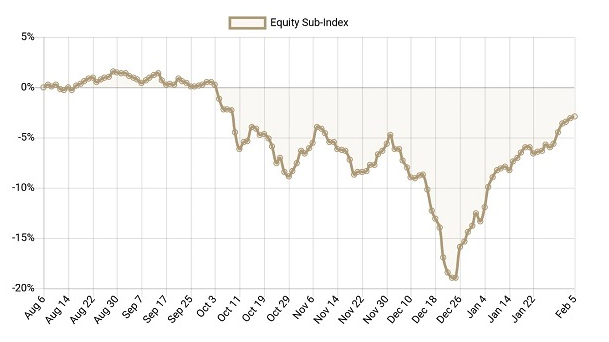

Inflation Defies Expectations

This has stumped many economists, because it’s normally a given that lower unemployment stokes inflation. But there’s a simple explanation for what’s happening today, and it comes back to folks who are unwillingly out of the workforce.

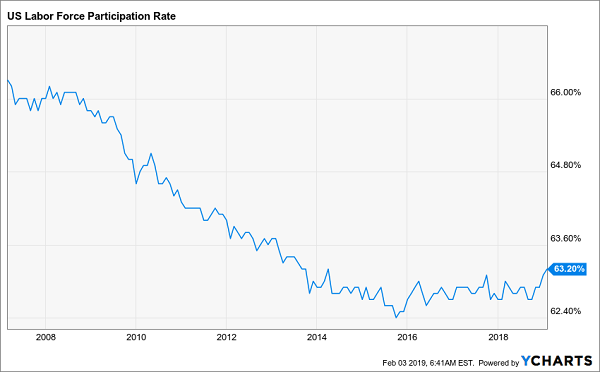

Here’s what I mean: the government measures unemployment by looking at what percentage of people are in the labor force, then looking at what percentage of those people don’t have jobs. But people can choose to be in or out of the labor force at any given time—and plenty of people have made an exit in the last decade:

US Workforce Shrinks—Till Now

For much of the 2010s, the unemployment rate wasn’t falling because more people were getting jobs—it was falling because more people gave up on getting jobs. But workforce numbers flat-lined since 2015 and began rising in late 2018. In short, Americans who’d thrown up their hands are getting back in the game.

That means inflation could be a risk in the future, when all those who left the labor force have come back, but we’re a long way from that.

In sheer numbers, think of it this way: 66% of 306 million people were in the labor force in 2007. That’s 202 million men and women. We’re now down to 63.2% of 327.16 million, or 206.8 million people. Another way to think about it: in the last 12 years, our labor force is up just 1.6% while our population is up 6.9%.

This is unsustainable: America needs more workers to keep up with its bigger population.

“A Rare Time When You Can Buy Stocks at a Discount”

This all means the market recovery will likely continue, because there’s too much demand for workers—and workers have too much money to spend—to cause a market hiccup. Better still, we’re at a rare time when you can buy stocks at a discount—and an even bigger discount is on the table for us, thanks to closed-end funds (CEFs).

Let me explain.

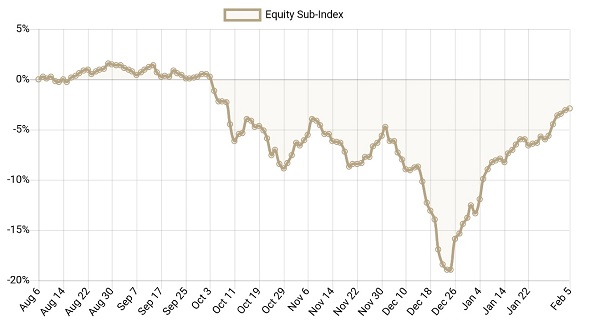

CEFs slipped in 2018, only to start recovering in early 2019:

CEFs Tumble … Then Bounce Back

But as you can see, CEFs still haven’t fully recovered—and there’s still a big gap between their 2018 peak and where they are now, even though CEFs’ year-to-date recovery has beaten the S&P 500’s 9.1% bounce, with the CEF InsiderEquity Sub-Index up 11.1% in 2019.

That tells me that this could be another year where CEFs outperform, as they did in 2017. And they’re likely to do so for the same reason: they were oversold in the prior year.

The One Fund to Buy for 35% Gains (and 7.2% Dividends) in 2019

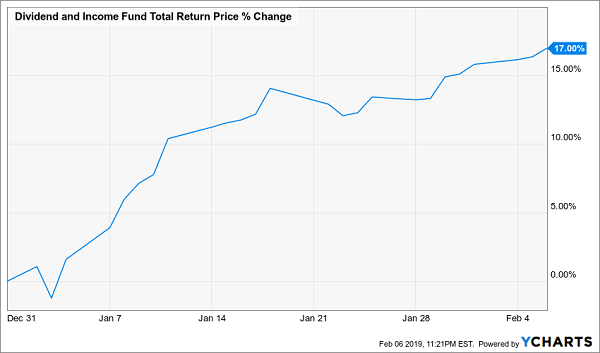

Which brings me to the Dividend and Income Fund (DNI), which focuses on bargain-priced US stocks like Apple (AAPL), Intel (INTC) and the Walt Disney Company (DIS). DNI is now signaling that it’s in the early stages of a huge recovery. Look at its outsized return in 2019 so far:

The Rally Is On!

But DNI still falls short of where it was in early 2018, so it has plenty of runway ahead:

DNI’s Ride Is Just Beginning

How high can DNI go? If we track its 2017 performance from when it got absurdly oversold at the end of 2016 (as it was absurdly oversold at the end of 2018), we see that a 35% return was in the cards:

History Looks Set to Repeat

And since DNI’s decline in ’16 wasn’t as severe as in ’18, there’s a good chance this year’s return will be even bigger than 35%.

One reason why I’m confident is that the fund’s unusually large 23% discount to net asset value (NAV, or the market price of its underlying portfolio) means that, just to sustain that discount, for every 1% its NAV gains, DNI’s price will have to go up 1.3%. If the market wants to make that discount disappear (as it did in 2017), its price will obviously have to go up much more than 1.3% for every 1% of NAV gains.

The kicker? DNI yields an outsized 7.2% now, so you’re getting around 20% of your potential 35% return in cash here.

Better still, DNI is far from your only choice: there are many other CEFs yielding as much or more than this fund and also look set to clobber the S&P 500. And these income wonders invest in similar top-notch (and cheap) US companies.

Cloud stocks are back. During the late 2018 market selloff, cloud stocks were thrown out — along with every other growth stock in the market. But as financial markets have improved in early 2019 due to stabilizing economic fundamentals, cloud stocks have come roaring back.

The First Trust Cloud Computing ETF (NASDAQ:SKYY) dropped more than 20% in late 2018. Since bottoming on Christmas Eve, the SKYY ETF has soared nearly 20%, and is now just 5% off of all-time highs.

The big rebound in cloud stocks can be chalked up to improving fundamentals and sentiment. As it turns out, the global economy isn’t spiraling downward at a rapid rate. Instead, it is simply slowing at a reasonable rate to a more steady 2-3% growth rate. Amid this slowdown, cloud services demand has remained robust, since cloud services are seen both as the future and a way to cut costs amid slowing growth.

Consequently, the fundamentals and sentiment underlying cloud stocks have dramatically improved over the past month. As they have, cloud stocks have soared higher.

This rally is far from over. Considering only 20% of enterprise workloads have shifted to the cloud, it’s fair to say that the rally in cloud stocks is still in its early stages. With that in mind, let’s take a look a 7 cloud stocks to buy now.

Source: Shutterstock

Adobe (ADBE)

Perhaps the best-in-class cloud stock to buy now for healthy upside and limited risk is Adobe(NASDAQ:ADBE).

The core growth narrative here is quite promising. Adobe is one part stable-growth business with a huge moat, and one part hyper-growth business with a rapidly expanding addressable market. Those two parts put together are worth far more than what the market is saying today.

On the stable growth side, Adobe is a one-stop shop digital solution for creative professionals with relatively muted competition. This has always been the case. If you can’t think of any true competitors to Adobe in the creative solutions space, you aren’t alone. Just check out this list or this list of Adobe Photoshop alternatives. None of them are household names. Nor do any of them offer products even close in quality to Adobe’s offerings. As such, this creative solutions business is a stable growth business with a huge moat and no competition, implying healthy revenue and profit growth for the foreseeable future.

On the hyper growth side, Adobe is morphing into a cloud business with a unique value prop. Other cloud solutions focus on various factors. Adobe’s cloud solutions focuses on experiences and visuals, and the company is leveraging its experience in visual-oriented solutions to create cloud solutions for companies looking to enhance their consumer’s experience. As it does, Adobe’s revenue and profits will move considerably higher.

Overall, there’s a lot to like about ADBE stock. This is a big growth company that will keep growing at a big rate for a lot longer. That level of robust growth will power ADBE stock significantly higher in a long term window.

Another best-in-class cloud stock is cloud communications app maker Twilio (NYSE:TWLO)

Over the past several quarters, Twilio has emerged as the unchallenged leader in the rapidly growing Communication Platforms-as-a-Service (CPaaS) market. The CPaaS market essentially consists of companies integrating real-time communication into their services. Think of Uber or Lyft using messages to communicate with riders when their rides are approaching.

This market will be huge due to continuous shifts towards cloud-based communication, personalized customer experience and digital engagement. Quite simply, as consumers, we enjoy digital, real-time, and personalized communication about the services and products we are paying for. Twilio enables this communication. That positions this company for huge growth as the CPaaS market expands over the next several years. For what it’s worth, research firm IDC expects this market to grow five fold over the next five years.

Thanks to its huge customer and revenue growth and 95%-plus retention rate, Twilio has emerged as the clear leader in this space. As this space matures over the next several years, companies will increasingly turn towards Twilio to enable CPaaS solutions thanks to the company’s leadership position (in new industries, you always tend to trust the leader).

As such, over the next several years, Twilio will continue to grow at a rather robust rate. This big growth will ultimately power TWLO stock higher, especially against a favorable equity backdrop.

ServiceNow (NOW)

In the digitization and automation fields, the cloud stock to buy is ServiceNow (NYSE:NOW).

ServiceNow is currently in the business of digitizing corporate operations. This includes automating corporate workflows and IT tasks. But, this is just the tip of the iceberg for ServiceNow. Automation is a big, big market. Automating IT tasks represents just a fraction of what the automation market will look like at scale.

At scale, jobs across the entire corporate ecosystem will be replaced by more efficient digitized and automated solutions. ServiceNow will provide the lion’s share of these solutions. As such, as the automation revolution plays out over the next several years, ServiceNow’s revenues and profits will explode higher. As they do, NOW stock will explode higher, too, considering the valuation today remains reasonable.

Overall, NOW stock is a great way to play the automation revolution. This revolution is still in the first inning, and the next eight innings promise to have broad and immense financial implications. For ServiceNow, those implications are hugely positive. As such, NOW stock should trend consistently higher over the next several years.

Okta (OKTA)

One of the more exciting cloud stocks to consider here is Okta (NASDAQ:OKTA).

Okta is pioneering what the company calls the identity cloud. Essentially, this is a cloud solution centered on individual identity that allows millions of people across a corporate ecosystem to seamlessly, securely, and uniformly connect to the technological tools that the corporation is adopting. This may sound like a complex idea. The underlying technology is complex. But, the idea isn’t. The idea is that companies everywhere are rapidly adopting new technologies, and that the implementation of these technologies is often difficult, chunky, and risky to identities and data. Okta solves this problem, and allows companies to adopt new technologies seamlessly and within the same secure cloud solution.

This is a big idea. Big ideas have big markets. Indeed, the addressable market for Okta’s identity cloud is the whole IT space. Okta recorded revenues of just over $100 million last quarter from growth of nearly 60%. This is nothing new. Over the past several quarters, the average revenue growth rate has hovered around 60% and the average customer growth rate has hovered around 40%.

Thus, this is a small company that is consistently and rapidly growing in a huge market. Gross margins are high, and marching higher, leaving room for big profits at scale. Overall, this is a big growth company with a ton of potential. The valuation is big, but the amount of growth firepower underneath this business implies a tremendous opportunity to grow into the valuation, and then some, making OKTA stock an attractive long term investment here.

Source: Shutterstock

Salesforce (CRM)

The king of all cloud stocks is Salesforce (NYSE:CRM), and there’s good reason for that.

Salesforce is at the heart of the cloud and data revolutions. The company leverages data and analytics to deliver robust cloud solutions to enterprises that want data-driven insights. Demand for this type of service will grow by leaps and bounds over the next several years as data-driven strategies and cloud solutions become the enterprise norm. Salesforce has developed a long-standing reputation for being the best in class for delivering these services.

That won’t change any time soon. As such, Salesforce’s revenues and profits will soar higher over the next several years as the cloud and data revolutions gain mainstream traction.

This will naturally push CRM stock higher. Valuation is somewhat of a concern at nearly 60x forward earnings. But, the company has enough growth firepower through cloud and data tailwinds to grow into its valuation. Plus, valuation has been a long-running concern for this stock, and the stock has done nothing but defy those concerns and head higher over the past several years.

The same will be true over the next several years, too. Cloud and data tailwinds will propel CRM stock higher, and this stock will ultimately grow into its valuation. Indeed, numbers indicate the stock could double in the long run.

Source: Shutterstock

Amazon (AMZN)

Amazon (NASDAQ:AMZN) is better known for its giant e-commerce business. But, the true profit growth driver behind Amazon is the company’s cloud business — Amazon Web Services.

AWS is the world’s largest cloud infrastructure services business, and it’s not even close. Amazon Web Services is bigger than its four closest competitors … combined. And the company has consistently controlled more than 30% of the cloud services market.

This dominance speaks volumes about just how good AWS is. Indeed, AWS is so good that even Amazon’s commerce competitors are giving money to the company through AWS. Notably, Amazon’s e-commerce competitor Zulily migrated its infrastructure to AWS recently. Also, AWS is so good that Amazon it is the clear front-runner to win a $10 billion Joint Enterprise Defense Infrastructure (JEDI) commercial cloud contract with the U.S. government. If Amazon were to win that contract, that would be the second government contract this decade (AWS won a $600 million CIA contract in 2013).

Overall, AWS is the clear leader in the cloud infrastructure services. As this market grows over the next several years, AWS will grow, too, and that will provide a big boost to Amazon’s profits. A big boost to Amazon’s profits will give AMZN stock firepower to head higher.

Source: Shutterstock

Alphabet (GOOGL)

Much like Amazon, Alphabet (NASDAQ:GOOGL,NASDAQ:GOOG) is better known for its non-cloud businesses.

But, a significantly underappreciated and underrated aspect of Alphabet is Google Cloud. Google Cloud is a big growth, big margin business for Alphabet. To be sure, the business has lost some steam over the past several quarters as Microsoft (NASDAQ:MSFT) has gained cloud market share at a more robust pace than Alphabet recently. But, there have been some C-suite changes at Google Cloud which could give the business new direction and new firepower to regain some lost momentum.

Regardless, Google Cloud will remain a 20%-plus growth business for a lot longer. Overall, Google Cloud is the key to unlocking the next leg of value in GOOGL stock. Fortunately, this business is progressing as expected, and will continue to do so over the next several years. As it does, GOOG stock will move higher.

As of this writing, Luke Lango was long ADBE, TWLO, CRM, AMZN and GOOG.

Do you remember the “browser wars” in the 1990s? It started when young upstart Netscape took the world by storm with its web browser.

At the time, Microsoft – with its Windows operating system – dominated the computing industry. It was a behemoth feared by all. Apple, IBM and HP were mere flecks in Microsoft’s rearview mirror.

Yet Microsoft knew that the web (and Netscape) represented an existential threat. It could be the only thing to drive Microsoft out of business.

So Microsoft pivoted. It embraced the internet and the web. And it created Internet Explorer. It was Microsoft’s bid to own access to the web.

Microsoft bundled Internet Explorer for free with its Windows operating system in an effort to crush Netscape and any other company that might have the temerity to launch its own browser.

The company’s efforts didn’t work. But they did define the competitive landscape for the better part of a decade.

Just like Microsoft more than 20 years ago, Facebook and Google have been hard at work trying to determine how they want to approach crypto – and the blockchain.

And this week, we learned more about their efforts.

Last May, David Marcus left Facebook’s Messenger product to lead Facebook’s blockchain initiatives. In December, media reports suggested Facebook was developing a cryptocurrency to be used on its WhatsApp messaging platform. And this week, Facebook hired away Chainspace’s top talent (Mashable).

The move, first reported by Cheddar, gives Facebook a talented crypto team that had been working on building smart contracts and a payment ecosystem (Cheddar).

Facebook didn’t get Chainspace’s technology. But Facebook doesn’t need the tech. It now has the talent and resources to build its own crypto ecosystem. And Facebook’s existing user base (2.32 billion monthly active users) could drive mainstream adoption. That makes Facebook a crypto force to be reckoned with.

Google, meanwhile, is entering crypto in typical Google fashion – by making it searchable. Google has uploaded the entire bitcoin and ethereum blockchains to its BigQuery cloud database and provided open-source tools to search it. It’s in the process of uploading litecoin, zcash, dash, bitcoin cash, ethereum classic and dogecoin to BigQuery. And independent programmers are uploading their own crypto datasets to BigQuery so they can search them (Forbes).

This is a remarkable development. One of the biggest regulatory issues facing crypto is market surveillance. But with the right programming or AI (artificial intelligence) in place, that problem can be solved. In fact, a Google developer has already spotted bitcoin cash being hoarded and autonomous agents moving ethereum around.

An independent developer used Google’s tools to find a specific smart contract flaw. Another created a heat map of XRP flow.

Google’s new foray into crypto has the potential to be transformational. And the entire crypto community should be on notice. Google and Facebook are playing for keeps. Everyone else needs to raise their game.

Speaking of MedMen, it’s been an interesting few months for James Parker. In the beginning of November, he was MedMen’s chief financial officer. In mid-November, MedMen announced his resignation. And by the end of January, Parker was suing MedMen for breaching its fiduciary responsibility to shareholders (Seeking Alpha).

A Florida judge has struck down a law that limits the number of medical marijuana facilities an operator can have (Orlando Sentinel).

And in Arizona, medical marijuana is legal – except when a county prosecutor says it isn’t (ABC15).

Okay, let’s follow the bouncing ball here. Arizona voters legalized medical marijuana in 2010. In 2017, a cancer patient was told by his oncologist that he should try medical marijuana. He obtained a medical marijuana card from the state and visited a legal medical marijuana dispensary where he bought some wax to help with his nausea.

A few days later, he was stopped by police for a traffic violation. And when they discovered the wax in his car, they arrested him and charged him with possession of a narcotic. He faces a 10-year prison term if convicted.

Whether this Arizona man gets convicted depends on the Arizona Supreme Court. The court is hearing a similar case about an Arizona man currently serving time for the same “crime.”

The legal “argument” at play is that the medical marijuana law says only the plant form of marijuana can be used for medical purposes. All other forms are illegal.

It’s a technicality – one that ignores the fact that he purchased the wax legally. And even the state’s attorney general doesn’t want anything to do with this case.

But the conviction has already been upheld once. Here’s hoping the Arizona Supreme Court does the right thing and frees these men from this legal nightmare.

Startups

Spotify is betting big on podcasts. It just bought podcast startups Gimlet and Anchor to fortify its strategy. The two startups had raised about $43 million combined from venture capital funds (Fortune). Spotify spent about $230 million on Gimlet and wants to spend about $500 million this year on acquisitions (Recode).

And Jetty, a startup that sells rental insurance, just raised $25 million in a Series B funding round. The round was led by Keith Rabois from Khosla Ventures (The Real Deal).

Crypto

Twitter CEO Jack Dorsey recently revealed that the only cryptocurrency he owns is bitcoin. Why bitcoin?

“Bitcoin is resilient,” Dorsey said on Twitter. “Bitcoin is principled. Bitcoin is native to internet ideals. And it’s a great brand” (Daily Hodl).

And in Argentina, 37 cities now accept bitcoin as payment for buying bus and metro (train/subway) passes (Bitcoinist).

And that’s your News Fix.

Have a great weekend!

Vin Narayanan Senior Managing Editor, Early Investing

It happened so quietly, you may not have even noticed. But the script has flipped on interest rates—and today I’m going to give you my favorite way to profit. (hint: this buy pays an 8.8% dividend—enough to hand you $8,800 a year in cash on every $100k invested—and is poised for quick 10% price upside, too!).

Let’s start at the beginning.

A Low-Key 180

I’m sure I don’t have to tell you that the big story of the last three years has been the Fed’s aggressive rate hikes. But the big story of the next three years will likely be a lack of aggressive rate hikes.

The change happened fast—at just one Fed meeting in January—and the market now expects zero hikes in 2019. Funny thing is, our best buy for this new world is a group of investments that, if you relied solely on the headlines, you’d think are some of the worst things you could own now.

I’m talking about floating-rate loans, which should rise in value as rates go up. But the Fed’s move to no hikes this year has actually created a great contrarian buying opportunity here.

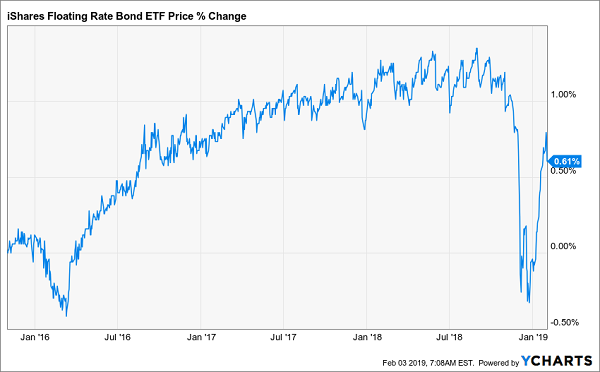

Floating-Rate Loans Have Been a Wildcard

Floating-rate loans were touted as a way to profit from higher rates since the Fed started hiking in late 2015, but there’s been a problem: reality kept butting against this theory.

Floating-Rate Loans Freeze Up

Despite the rising-rate cycle kicking off in December 2015, the benchmark iShares Floating Rate Bond ETF (FLOT) went nowhere following a brief, small bump in early 2016. And investors were no doubt frustrated with the 1% gain they got in the years they held FLOT, before kissing most of that gain goodbye in the late-2018 market panic.

In short: floating-rate loans, for much of this period, didn’t work as planned.

But now is a great time for floating-rate loans, even though the Fed rate is likely to flat-line. Because just as theory didn’t translate to reality by using these loans to profit from higher rates, the theory that their value will go down in value as rates fail to rise is equally unrealistic.

That’s because the recent fall in floating-rate-loan values has nothing to do with interest rates.

The floating-rate loan market saw a huge drop in late 2018 for two reasons: 1) There was a record number of loans in the market, due to lenders choosing floating-rates over corporate bonds (thus increasing supply and limiting price growth); and 2) There was a panic as investors feared lenders would default on their loans due to bankruptcies caused by an economic crash.

The second fear is already proving to be nonsense: not only is there no crash, but employment and corporate earnings seem likely to keep improving in 2019, even after a strong 2018. The first issue, however, is also disappearing—but many people don’t know about it.

Instead of using floating-rate loans, as they did in 2018, more US companies are going back to raising cash by issuing corporate debt in the form of bonds. They are even doing this in unusual and unexpected situations. The Financial Times tells the story of TransDigm (TDG), an aircraft-component manufacturer that used corporate bonds instead of floating-rate loans to fund its $3.8-billion acquisition of aerospace-component maker Esterline.

Commenting on the deal, TwentyFour Asset Management Head of Credit David Norris told the Financial Times: “I would typically have expected a company like this, doing an acquisition, to go to the loan market. But they didn’t do that. There are opportunities right now in the high-yield bond market.”

With the decline in the number of floating-rate loans, demand for those still in existence (and the few new ones coming to market) will likely drive up prices, especially since overblown default fears have kept floating-rate loans below their pre-crash levels.

That means there’s a huge buying opportunity for savvy buyers—especially if we get our floating-rate-loan exposure through closed-end funds (CEFs).

Floating-Rate Confusion Hands Us an 8.8% Cash Payout

Since CEFs often pay huge dividends, your chance to grab 7%+ yields from floating-rate funds is now. But which funds to pick?

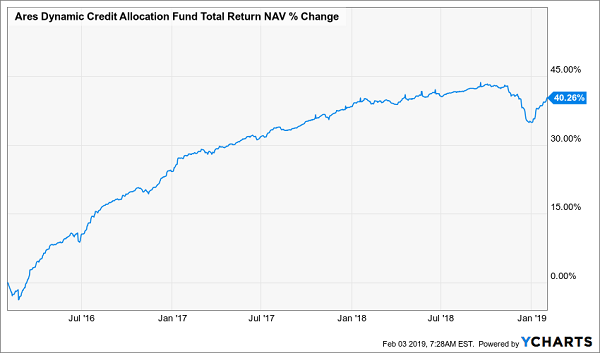

One of the most discounted floating-rate funds also has one of the biggest yields: the Ares Dynamic Credit Allocation Fund (ARDC) pays a massive 8.8%. It also gets “bounce-back” upside from its 13.1% discount to net asset value (NAV, or the what its underlying loan portfolio is worth). That’s well below the 7.2% discount it achieved in the past year.

As you might suspect, the fund’s name comes from its management team: Ares Management, which runs a number of funds and companies that provide credit to medium-sized businesses, including its business-development company, Ares Capital Corporation (ARCC). Ares Capital is the biggest BDC, with $12.3 billion in assets under management.

That size is important, because it means Ares has deep connections with many borrowers and knows which can pay their bills and which can’t. That has meant an impressive run-up for ARDC since interest rates started rising:

“In the Know” Management Delivers

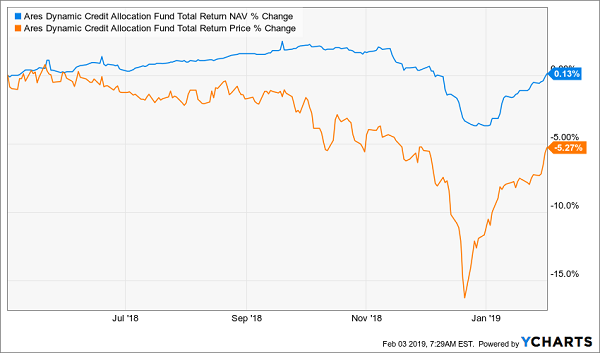

While investors typically reward ARDC with a steadily rising market price to match its portfolio’s fundamental strength, the fund’s price return is still lagging:

A Rare Buying Opportunity

The takeaway? Now is a great time to tap ARDC for its 8.8% income stream and hold while my expected 10% capital gain from both a strengthening floating-rate-loan market and the fund’s shrinking discount start to appear.

I want to follow up on my renewable energy article from Monday with another look at the renewable energy sector. And later I will fill you in on three renewable energy stocks leading the way that hail from Europe.

First though, let’s look at some of the raw numbers on renewable energy investment worldwide.

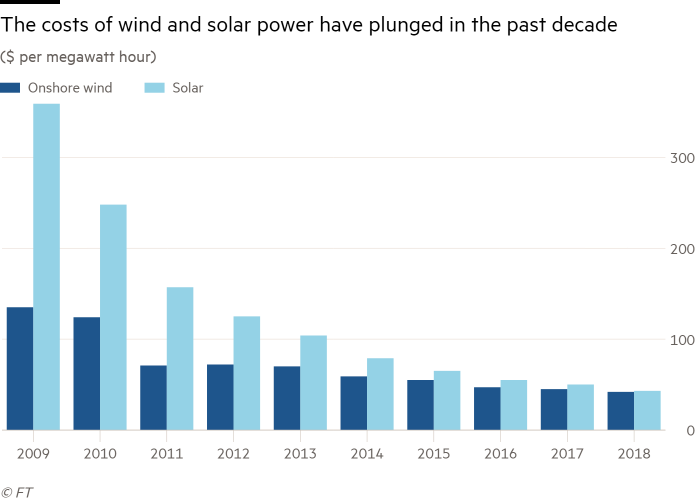

Clean energy investment globally actually declined 8% in 2018, according to Bloomberg New Energy Finance, to reach $332.1 billion, because of two factors – a Chinese crackdown on solar subsidies and the falling cost of wind and solar projects.

This latest data from BloombergNEF, considered to be the most definitive account of clean energy spending worldwide, shows that the biggest drop came in China, where renewable energy investment fell by a third after a new government policy slashed subsidies for solar projects beginning in June.

However, this is a case where a cursory glance at the raw numbers does not give a valid picture of what is going on in the renewable energy space. Actual additions globally of new wind and solar projects still increased year on year despite the decline in investment, because the costs of solar and wind energy projects have seen steep falls.

Angus McCrone, chief editor of BNEF, explained: “It’s not really a slowdown at all. Every year investment in clean energy has to run faster to stand still, because of the reduction in costs.” Renewable energy investment will fall again in 2019, he predicts, even though the amount of new capacity added will increase slightly because the reduction in costs will continue.

Costs Continue to Fall

There is no doubt that the costs of renewables — led by solar and wind power — are now materially cheaper than they ever have been. These costs have fallen to the point at which the International Energy Agency, in its latest short term outlook, sees prices falling to between $20 and $50 per megawatt hour. That means wind and solar can compete with other fuels, even if some of the costs of providing back up to cover the intermittency of renewable supplies are included. In a growing number of markets, neither subsidies nor protected market shares will be necessary.

Even here in the U.S., the cost of new wind and solar power generation has fallen below the cost of running existing coal-fired plants in many parts of the country. New estimates published in November by the investment bank Lazard show that it can often be profitable for U.S. utilities to shut working coal plants and replace their output with wind and solar power.

According to Lazard, the all-in cost of electricity from a new wind farm in the U.S. is $29-$56 per megawatt hour (MWh) before any subsidies — such as the federal Production Tax Credit, which is being phased out by 2024. The marginal cost of operating a coal plant is $27-$45 per MWh.

So there are times and places where building a wind farm, even without any subsidy, would make sense. Add in the PTC, which can cut the cost of wind power to as little as $14 per MWh, and the case becomes even stronger. This turns into a win-win situation, with higher returns for the utility companies and lower bills for their customers.

Here in the U.S., the outlook for wind power is brighter than that for solar power at the moment because of tariffs placed on solar panels by the Trump Administration.

Installations of new solar power capacity in the U.S. slowed in the third quarter of 2018 to the weakest rate since 2015. The projects most affected were the large utility-scale projects, which are much more sensitive to the cost of solar panels.

These tariffs came into effect last February at an initial rate of 30% with the intent of protecting domestic panel manufacturers. But the Solar Energy Industries Association, which represents developers and installers as well as manufacturers, said the tariffs had put a brake on investment and had cost more than 20,000 jobs.

It is this apparent anti-renewable energy sentiment from the Trump Administration that has me looking to Europe for the best-performing companies and stocks in the sector. I particularly like the wind power-related companies in Europe. Here are just three of them…

Three European Wind Power Stocks You Can Buy Here in the U.S.

Europe is home to some of the world’s best wind turbine companies, which is good news since the prospects for the wind business remain sound. Installations worldwide are expected to reach 72 gigawatts per year by 2025 – a 5% compound annual growth rate. My two favorite are:

Vestas Wind Systems (OTC: VWDRY) and Siemens Gamesa Renewable Energy (OTC: GCTAY). Vestas’ stock here in the U.S. is much more liquid than Gamesa’s, but both companies are doing very well.

Gamesa was an independent Spanish wind company that combined its wind assets with Germany’s industrial powerhouse Siemens to form a top-notch company.

In its recently reported quarter, results were much better than expected, sending the stock soaring from a beaten-down low (there were doubters as to the wisdom of the merger). Revenue increased in the quarter by 6% year-on-year, to 2.26 billion euros, driven by the offshore wind business and by its services business. Wind turbine volume increased by 7%, to 2,129 megawatts of energy, due to the strong contribution by the offshore segment, which sold 609 megawatts (+76% year-on-year).

Net profit amounted to 18 million euros, contrasting with the 35 million euro loss reported in the same period of the previous fiscal year.

Siemens Gamesa logged orders worth 11.5 billion euros in the last twelve months (+3% year-on-year), driven particularly by a 28% increase in onshore orders (6.8 billion euros). Order intake in the first quarter amounted to 2.5 billion euros, with solid performance by onshore wind turbines (1.8 billion euros, +7% year-on-year).

The order book stands at 23 billion euros (+8% year-on-year), of which 15.7 billion euros worth are orders to be filled after the 2019 fiscal year. This lends greater visibility to its future growth and covers 92% of the revenue target for the current year. The offshore wind business is projected to attain 27% annual growth, from 2 gigawatts of installations in 2018 to 12 gigawatts in 2025.

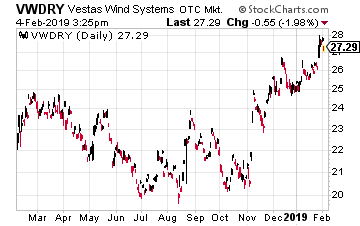

Vestas will announce earnings on February 7th, but it has already pre-announced good news. Based on preliminary reporting, Vestas upgraded its expectations for 2018 free cash flow to approximately 400 million euros. That compares to its prior expectation of a minimum of 100 million euros.

The company said the marked improvement was primarily driven by a strong order intake and indeed the company’s order book is at a record high, with over 10 gigawatts of orders in 2018. One example of a major order it won here in the U.S. was announced in December to supply 100 of its V120-2.2 megawatt turbines for a wind project.

Another major wind power-related company is Denmark’s Orsted A/S (OTC: DNNGY), which has transformed itself from a hydrocarbon energy company into a renewable energy company.

It last earnings report, in November, blew away analysts estimates (pardon the pun) with a 31% rise in earnings from offshore wind generation. And the company raised its guidance for 2019.

Orsted also said its green energy generation had increased substantially, with renewables now accounting for 71% of its heat and power output, up from 60% in the year ago period. It recently expanded its reach into onshore wind in the U.S. with the purchase of Lincoln Clean Energy and it also bought a U.S. offshore wind developer, Deepwater Wind.

Most of these stocks have done well, despite 2018 being a very poor year for stocks. The returns over the past year for these three companies’ ADRs are: Siemens Gamesa – 1%, Vestas – 25% and Orsted – 25%. The only laggard has been Gamesa, but it is up 35% over the past three months.

I expect the outperformance from these stocks to continue in 2019.

Today, I’m going to show you one of the best penny stocks you can buy right now. You see, this stock is a play on the solar industry, which is absolutely booming.

A lot has happened over a short period with respect to the solar power industry. For much of 2018, oil prices were soaring and reached their peak in November at close to $70. Most of this increase was due to higher interest rates from the U.S. Federal Reserve and a strong dollar.

As crude prices climbed, so did the price of solar stocks.

This wasn’t just a small bump, either. In just a few short months, there were jumps of 50% or more on some of the top solar stocks.

Sadly, this rally was short-lived.

Toward the end of 2018, there was a market rally in bonds and another interest rate hike took the dollar much lower.

The price of crude oil dropped when the dollar lost momentum and traders pulled out of solar stocks to lock in profits.

Market volatility didn’t help either. What began as a 50% bump in solar stocks ended up being losses of almost 20%.

This wasn’t the first time this has happened with solar stocks either.

There was a major rally with solar stocks several years ago when the price of oil was over $100 per barrel. The solar industry was young at that time, and some of the early investments were followed by share price losses.

However, investors were not fazed.

Compared to where they trade today, solar stocks were trading at prices that were three and four times higher.

So, why get excited about solar stocks now?

The truth is that we’ve seen this before, and there is still plenty of evidence that the next solar boom is right around the corner…

There Is a Massive Solar Boom on the Horizon

The solar industry has experienced some major breakthroughs in the past several years that make this the perfect time to invest

To start, there are more green initiatives than ever, which has been a windfall for solar companies.

And those initiatives will continue into the coming years.

Solar Estimate reports that solar energy is now the cheapest way to power a home.

According to some estimates, there were an estimated 2 million residential solar installations in the United States by the middle of 2018. This is a figure that is expected to double over just four years.

Plus, a stronger dollar environment and rising interest rates will be ideal for solar stocks.

Long term, an investment today could double or triple in value.

Knowing this, what are the best solar stocks to buy?

The market has been volatile of late, but the economy continues to do well. This is evidence for a stronger dollar in 2019 and good news for the solar industry.

When it comes to picking solar stocks, the best ones will be positioned so that they benefit from green initiatives. These are primarily companies that deal with solar installations.

As oil prices go higher, this will be an additional catalyst for these types of stocks to move up.

This is a solar company that was founded in 2011 that’s focused on the installation of residential, commercial, and industrial solar systems throughout the United States.

Shares of VSLR were trading at over $15 when crude oil was priced over $100 back in 2014.

Today, you can pick up the stock for just over $4 per share.

When crude prices jumped again in the first three quarters of 2018, Vivint stock peaked just below $6 per share.

Granted, the company still isn’t profitable, which explains why it trades in the penny stock range.

The good news is that its revenue continues to grow, with analysts expecting sales to hit $291 million in 2018 and reach $331 million this year. This is a growth of 14% in just one year.

Since it’s already hit $6 in the past year, it can certainly do so again. Going from $4 to $6, investors would gain 50% on this profit play.

If crude oil prices soar once again, VSLR stock could even jump as high as $10 per share with a repeat of 2014 prices. This would represent a 150% gain over today’s price.

The difference is that the company is now pulling in more revenue and edging closer to being profitable.

Fintech, which is short for “financial technology,” has been a booming category during the past few years. Some of the drivers include smartphones, cloud computing, blockchain and artificial intelligence.

Many fintechs are still private, like Stripe, Betterment, Ellevest and Robinhood. According to a report from KPMG, VCs (venture capitalists) invested $14.2 billion across 427 companies during the first half of 2018. In fact, we’ll probably see some of them hit the IPO market this year.

But there are still plenty of fintech companies that are publicly traded. Keep in mind that old-line operators, such as Mastercard (NYSE:MA) and Visa (NYSE:V), are considered part of this class.

With that in mind, here are five of the best fintech stocks to invest in now.

Source: Shutterstock

PayPal (PYPL)

A key Silicon strategy is to disrupt massive industries. While this can result in enormous profits, it is extremely tough to pull off. There are some industries that are quite resilient, such as financial services.

In light of this, PayPal (NASDAQ:PYPL) has taken a collaborative approach. Part of this has been about integrating many types of payment options, which is what customers prefer. But there has also been an aggressive focus on forming strategic alliances. A prime example is a deal with Walmart (NYSE:WMT) to get a piece of the unbanked market segment.

For the most part, PYPL’s strategy has worked extremely well. In the latest quarter, the net new active accounts increased by 9.1 million to 254 million and the transaction volume jumped by 27% to 2.5 billion. A major driver for engagement has been from mobile devices.

Another strong catalyst for PYPL stock is Venmo, which provides peer-to-peer payments services. Note that the app is a must-have for the Millennial generation. From 2016 to 2018, the total payment volume has gone from 3.2 billion to 16.6 billion.

While still early, PYPL is seeing lots of traction with monetization, with 24% of the user base participating. In fact, Venmo is likely to be a strong lever of growth in the coming years.

Finally, PYPL has a rock solid balance sheet. There is currently about $10.5 billion in liquid assets. In other words, the company has the resources to engage in aggressive M&A to further bolster its strong fintech platform.

Founded in 1983, Intuit (NASDAQ:INTU) is a pioneer among fintech stocks. The company started off with simple check-balancing methods. But since then, INTU has expanded into lucrative categories like small business accounting and personal/business taxes.

These segments certainly generate substantial amounts of data, which allows for interesting use-cases. One example is QuickBooks Capital. It is a lending service that uses Intuit’s accounting data to make loans. Because of Intuit’s data advantage, about 60% of customers have obtained approvals for loans that would generally be deemed “un-lendable” by traditional financial institutions. The loss rate is also less than half the industry average.

It’s also important to note that INTU is bolstering its market opportunity by moving beyond its small business focus. Just look at QuickBooks Online Advanced. This is for the mid-market category (where the employee base ranges from 10 to 100). The market size in the U.S. is about 1.5 million.

In light of the innovation and diversified business assets, it should be no surprise that INTU has been a consistent grower. From 2010 to 2018, revenues have more than doubled to $6 billion.

Source: Shutterstock

Envestnet (ENV)

Envestnet (NYSE:ENV) develops sophisticated cloud-based technologies for financial advisors, such as independent providers and small- or mid-size firms. EVN’s software provides a full suite of services for front, middle and back office needs.

The company has built a solid base, with about 93,000 advisors (up 5% in the latest quarter). There are over $2.8 trillion in assets and more than 10 million investor accounts on the system.

One of the attractions of ENV is its open architecture. For the most part, the company strives to provide as many options for its advisors as possible. Note that there are over 18,000 products and more than 20,000 data sources.

ENV is also poised to benefit from a secular trend in the financial services industry, as more advisors transition from commissions to fee-based compensation. According to Cerulli, the amounts are expected to go from $9.7 trillion in 2017 to $16.7 trillion in 2021.

If you do not want to pick individual fintech stocks to invest in, then you can invest in an exchange-traded fund (ETF) that tracks the fintech markets. And a good choice is the Global X FinTech ETF (NASDAQ:FINX), which has about $288 million in assets.

The fund includes 37 stocks that have an average market cap of $9.4 billion. The top five holdings include PYPL, Square (NYSE:SQ), Fiserv (NASDAQ:FISV), SS&C Technologies Holdings (NASDAQ:SSNC) and Fidelity National Information Services (NYSE:FIS). What’s more, about 30% of the portfolio companies are based outside the U.S.

In terms of the themes for the FINX ETF, they are fairly broad. They are P2P/marketplace lending, enterprise solutions, blockchain/cryptocurrencies, crowdfunding and personal finance software/automated wealth management.

The fund has an expense ratio of 0.68% and no dividend yield.

Wondering if it’s too late to jump on this market recovery? I have great news: it absolutely is not.

But you won’t reap the biggest gains by, say, putting cash into your typical S&P 500 name—or in a passive index fund like the SPDR S&P 500 ETF (SPY).

Because while rising corporate profits will likely propel the market higher this year, you’ll put yourself in a much better position by hitting out at the two sectors (and two specific buys) I’ll reveal now.

Both sectors will be on my personal list this year, and I’ll be recommending stocks from each one to members of my Contrarian Income Report service, too.

Let’s dive right in.

Buy No. 1: A 4.3% Dividend Today—a 34% Dividend Tomorrow

Real estate investment trusts (REITs) are famous for high dividends, but the one I’m going to show you today is in another league. It pays an already-decent 4.2% dividend now.

And thanks to its strong dividend growth, a yield on your original buy will likely soar to double digits in short order—just like the lucky folks who bought 10 years ago—they’re yielding an amazing 34% on their original buy today.

More on that in a moment.

First, the stock I’m talking about is CubeSmart (CUBE) a hidden gem in the ignored self-storage space—a business so boring it would make even the most conservative investor sleepy.

And check out how CUBE has lagged REITs overall, represented here by the Vanguard Real Estate ETF (VNQ), so far this year:

The Convoy Rolls by CUBE

In fact, CubeSmart is far from alone in lagging VNQ: all six publicly traded self-storage REITs have done so this year.

That’s partly due to worries that there are too many of these handy little mini-garages spread across the US. To be honest, that’s always a risk in a business like self-storage, which has fairly low barriers to entry.

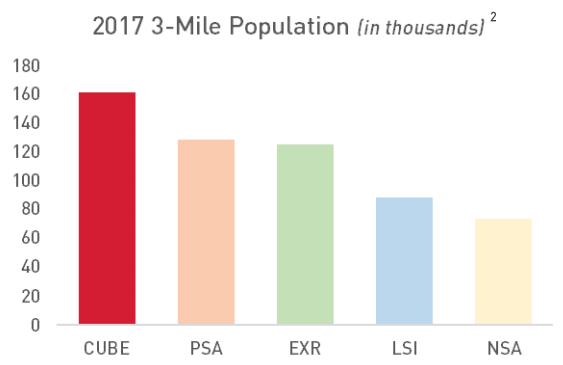

But CubeSmart sidesteps that problem in a couple ways: one is by targeting cities with scores of renters. Check out how many thousands of people live within just three miles of its 1,072 stores:

Source: November 2018 CubeSmart investor presentation

The other safety valve? The company runs more than half its locations through deals with outside owners. That gives it steady fee revenue and cuts its risk.

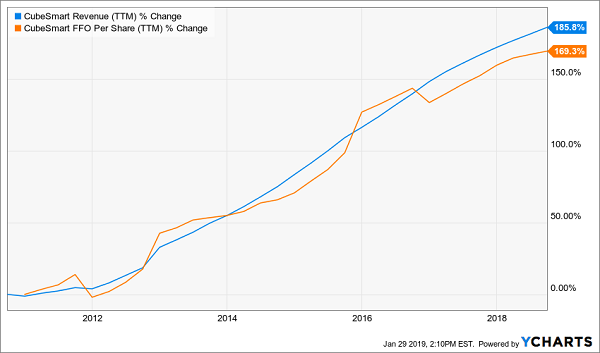

This targeted approach has paid off in soaring revenue, which has hauled per-share funds from operations (FFO, the REIT equivalent of earnings per share) up with it:

Turning Empty Space Into Cash

That leads us back to CUBE’s spectacular payout growth: the quarterly dividend has spiked 1,180% in the last decade! So if you’d bought in 2009, you’d be yielding an amazing 34% on your investment now.

This dividend is almost certain to keep rising, helped by CUBE’s low (for a REIT) payout ratio: just 73% of FFO. And thanks to the overwrought negativity around self-storage REITs we can grab this one for just 18.5-times trailing-twelve-month FFO. A great deal.

Buy No. 2: This 8% Dividend Is a Bargain (for now)

CUBE isn’t the only discounted dividend left over from the selloff. You’ll find more in the too-often-ignored preferred-share space—and I’m about to reveal the perfect “one-click” way to profit (paying a fat 8% cash dividend every month, to boot).

Preferreds are the best-kept secret in investing: they look a bit like stocks (they can trade on a market, for example) and a bit like bonds (they trade around a par value and send out a fixed regular payment).

The best thing about them: outsized payouts! Which is why preferreds took a licking last year, as first-level investors fretted that rising rates would sideswipe them.

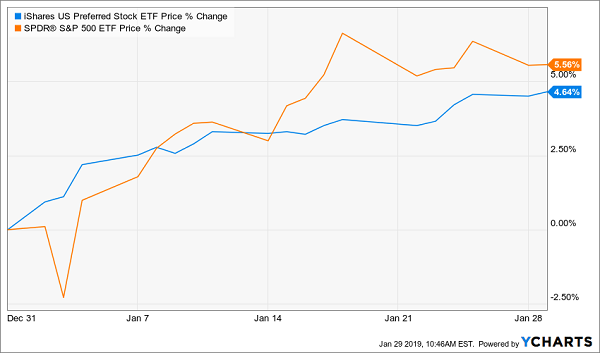

But now, with the Fed likely to take a breather, the pressure is off. The herd knows it, too: they’ve sent the passive iShares Preferred Stock ETF (PFF) up nearly as much as the S&P 500 since January 1.

A Headline-Driven Spike

But don’t worry, you can still get a deal in this space, thanks to the John Hancock Preferred Income III Fund (HPS), a closed-end fund (CEF) boasting a “hidden” discount that’s leading us to serious upside in 2018.

So what is this discount, and why do we say it’s hidden?

The discount I’m referring to is the gap between HPS’s market price and its NAV, or portfolio value. In a nutshell, it’s a quirk of CEFs you and I tap for some nice gains. Here’s how:

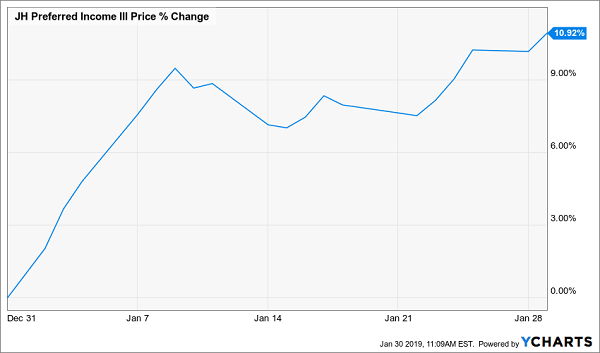

Right now HPS trades right around par, and the gap has narrowed from 1.5% earlier this year. That may not sound like much of a move, but it’s helped catapult the fund’s price up an amazing 11%.

HPS’s Discount “Slingshot”

This is how powerful a narrowing discount to NAV can be in CEFs, and HPS is just getting started. How do I know? Simple history.

Consider that the last three times HPS’s discount turned into a significant premium (here I’m talking 1.7% and above) fell in September, October and November 2018—all times when rate-hike fears were at their wildest!

But now that the Fed has shifted into park, the runway is clear for HPS to soar to even bigger premiums (and more price upside). Let’s get in now and start tapping its outsized 8% monthly dividend while we prep for its next leg up.

As investment strategist at CEF Insider, it’s my job to tip you off to the best closed-end funds (CEFs) out there. But it’s also my job to steer you away from those that are, well, terrible.

So today we’re going to zero in on four CEFs whose massive dividends (up to 12.7%!) might tempt you to buy. But doing so will lock you into an ever-shrinking income stream while the share price crumbles beneath your feet.

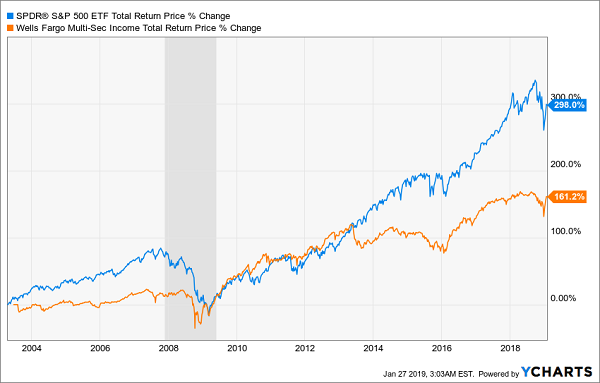

The first red flag? All four of these funds are from Wells Fargo (WFC), a bank that’s been at the center of various scandals for years now, starting with the 2016 fake-account fraud that took down Wells’ CEO at the time.

Wells’ Woeful Venture Into CEFs

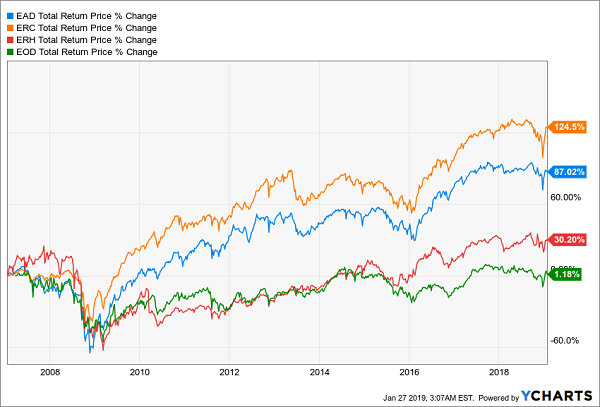

Don’t be surprised if you haven’t heard that Wells offers CEFs; it does so through its tiny Wells Fargo Asset Management business. Its CEFs are the Wells Fargo Income Opportunities Fund (EAD), the Wells Fargo Multi-Sector Income Fund (ERC), the Wells Fargo Utilities & High Income Fund (ERH) and the Wells Fargo Global Dividend Opportunity Fund (EOD).

You should never buy any of these funds, despite their enticing yields: EOD pays a monster 12.7%, for example, with ERC’s payout clocking in at 10.9%. (EAD and ERH yield 9.6% and 7.5%, respectively.)

Don’t be tempted—because these seemingly attractive payouts are warning signs.

The Dividend Trap

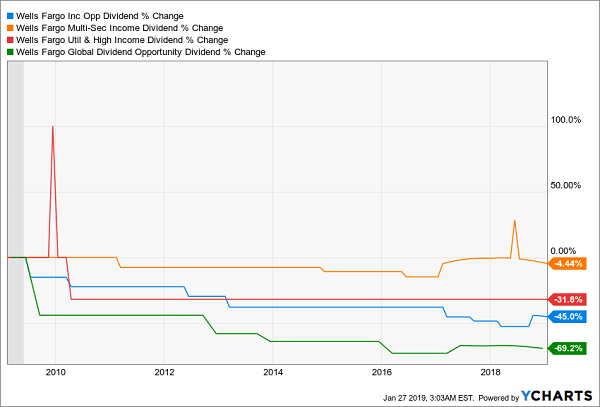

While many CEFs have great, sustainable payouts upwards of 7%, in the case of all four of Wells’s funds, high yields are masking awful news. To see what I mean, look at this chart:

Payouts in a Death Spiral

Since the recession, all of these funds’ payouts have fallen, with only ERC’s dividend (in orange) showing any signs of not going down the tubes. But if you’re thinking of buying ERC for its 10.9% income stream, don’t bother.

Massive Underperformance

One of the reasons I like some CEFs is that they’ve crushed the “dumb” index funds over a long period. ERC, however, is not one of these stout performers.

Lagging the Index

Since inception, ERC has returned slightly more than half of what the SPDR S&P 500 ETF (SPY), a low-cost index fund that simply tracks the S&P 500, would have given you. And ERC has underperformed almost all of its CEF peers in this time.

And this is the best CEF Wells can offer!

All Laggards

As you can see, not one of Wells Fargo’s funds has managed to beat the fund that couldn’t match the S&P 500. And EOD just recently went from a loss to a measly 1.2% return in total over the last decade! Such obscene underperformance doesn’t deserve anyone’s money. And it definitely doesn’t deserve any fees.

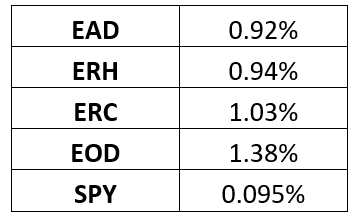

High Fees—But for What?

All of Wells Fargo’s CEFs charge fees, of course, but the scandalous thing is how high those fees are, particularly compared to SPY (which outperformed all of them, let’s remember).

At the cheapest, EAD’s fees are 9.7 times higher than those of SPY, while EOD’s are over 14 times higher. I’m not averse to paying higher fees if they mean better performance—but not only do these funds lag SPY, they lag many other funds that invest in the same type of assets.

The Amazing Shrinking Funds

With that in mind, you should avoid these funds for another reason: as they shrink, Wells Fargo will have less motivation to properly oversee them, and you only have to look at the headlines to see what can happen when the bank takes its eye off the ball.

The following chart shows the net asset value of each of these funds, or the total value of each CEF’s portfolio:

Wells’ CEF Assets Evaporate

The $1 billion EAD once had has shrunk to less than $600 million, with no end in sight, while all of Wells Fargo’s other CEFs continue to shrink. As these funds become a smaller part of Wells Fargo, whose net income was over $20 billion for 2018, the bank could wind end up shutting them down—only after their value and income streams have further melted away.

Your 2019 Action Plan: Beat Wall Street With These 5 Safe 8% Dividends

I don’t know about you, but I’m sick of big Wall Street names like Wells locking in billions in profits while offering us subpar investments like these four funds.

It’s an outrage! Especially when you consider that Wells could easily afford to hire top talent to run these CEFs and deliver a proper return to their investors.

The worst part is that dud funds like these mask the fact that there are many amazing CEFs out there throwing off safe 8%+ cash dividends.

Better yet, many of these top-quality funds are trading at incredible discounts right now, thanks to the recent selloff.

But you won’t hear from them from your advisor—and especially not from big banks like Wells, which are 100% focused on selling their own products, which all too often are unacceptable funds like the ones I just showed you.

With much of the U.S having just gone through what has been described by some media outlets as the coldest temperatures EVER in the Midwest, let’s talk about something on everyone’s mind, air conditioning. No, I’m not crazy. The World Economic Forum, in the midst of this major cold snap in the U.S., just published a piece on one of the predicted major drivers of energy demand growth in coming years. Yes, it’s air conditioning.

Of course, air conditioning itself isn’t suddenly en vogue when it wasn’t before. It’s a byproduct of economic growth and a rising global standard of living. While 90% of homes in the U.S. and Japan have air conditioning, that number drops to a staggering 8% for people who live in some of the hottest regions of the world. The number of air conditioners, driven mainly by populations in China, India, and Indonesia, is expected to increase over 250% in the next 30 years, to something around 5.6 billion.

And, that demand for space cooling, is expected to be one of the major drivers of electricity demand moving forward. An International Energy Agency (IEA) report predicts that peak electricity demand in India, which is currently comprised of 10% air conditioning demand, has air conditioning becoming 45% of peak demand in 2050. As the report states, “Growing demand for air conditioners is one of the most critical blind spots in today’s energy debates.”

Now, my use of the predicted rise in demand for air conditioning, in the midst of a major cold snap in the U.S., is somewhat tongue in cheek. But, the global rise in energy demand, which the IEA puts at between 30 and 40% by 2040, is real. And, the need to address this rising demand, be it for air conditioners, data centers, increased usage of electronic devices, or simply a rise in the standard of living, has companies and governments turning to renewable energy to solve some of the problem.

The result, the renewable energy market is growing. Driven by both this rising demand, and fairly recent advances in technology, which have renewable energy sources rapidly approaching the cost of old school fossil fuels. Companies are increasingly profitable and projecting long-term growth in this area. Here are a few of the names I like, and recommend you take a look at, in the renewable energy sector.

NextEra Energy (NYSE: NEE)

When you think of NextEra it’s highly unlikely you think of renewable energy. Most investors who know NextEra recognize them as the owner of Florida Power and Light (FPL) and one of the largest regulated utilities in the U.S. But they are much more than your average utility company.

NextEra Energy Resources, the renewable energy arm of NextEra, counts solar, wind, natural gas, and nuclear properties among its holdings. The company is rapidly moving forward on the renewable energy front, and CEO James Robo believes the cost of solar and wind generated energy will be the same as that of power generated by coal, and oil and gas fired power generation units very soon.

Robo has said that combining new energy production technology in wind and solar, combined with new technology being developed in power storage, will drive prices of renewables to the point that they will “…be massively disruptive to the nation’s generation fleet and create significant opportunities for renewable growth well into the next decade.”

NextEra has done a great job of moving from a staid electrical utility to quickly becoming the face of renewable energy on a large scale, while at the same time maintaining profitability for its shareholders.

Robo points out that by NextEra executing well on its business operations, “…FPL’s typical residential bill is more than 30% below the national average, the lowest of all 54 electric providers in the State of Florida and nearly 10% below the level it was in 2006.” And, this has been achieved, while bringing record amounts of renewable energy online in both 2017 and 2018. One of the main reasons I like the company here.

Since 2005 NextEra has delivered compounded annual growth in earnings of over 8.5%. It is expected to grow earnings this year 18.5% and pays a dividend just over 2.5%. The company’s profit margins are just over 50%, and it has a PE of just over 13.5. The company looks well positioned among the major utilities to continue expanding profitably into the renewable energy space for years to come.

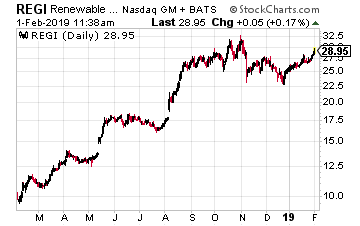

Renewable Energy Group (Nasdaq: REGI)

Renewable Energy Group is focused on turning your fast food remains, specifically the oil used to cook that food, into energy and profits. Using its proprietary BioSynfining technology, in the first 9 months of 2018, REGI prevented 2.9 million metric tons of carbon dioxide from release into the atmosphere. That is akin to removing 600,000 cars from U.S. highways for one year.

Renewable Energy has 14 refineries that turn vegetable oil, greases and sugars into biomass-based diesel fuel. One reason I like the company is the possibility of a new joint venture with Phillips 66 (NYSE: PSX) in which the two companies will build a large west coast biodiesel refining facility. California is one of REGI’s major customer states, and a new facility, currently planned for Washington state, alongside a Phillips 66 facility, would add valuable capacity to the Renewable Energy biodiesel offering.

Demand for biodiesel has risen 30% over the past two years, and REGI has been increasing production numbers to keep pace. They produced 11% more biodiesel in the first nine months of 2018 than 2017, and have increased production by 16% in the third quarter of 2018 alone.

REGI is also operating in a favorable regulatory environment. Despite tweets from the Commander-in-Chief negatively referencing global warming, that may have you thinking otherwise, the EPA is set to release updated regulations on biomass-diesel that would increase demand for the product. As Renewable Energy CEO Randolph Howard states, the new rules should “…ensure meaningful growth in both the biomass-based diesel and advanced biofuels category.”

In addition to these rules, and one of the reasons the company should be bought now, is a pending long term extension of the Biofuel Tax Credit (BTC). Howard says, “We’re pleased that participants across the various industries associated with biomass-based diesel remain united in the desire for a long-term extension of the BTC. This support is broad-based from feedstock suppliers, including farmers and ranchers, to producers, to blenders and, ultimately, to the end users represented largely by the trucking industry.”

REGI is projected to grow earnings 15% annually over the next five years, and has profit margins just north of 19%. Renewable Energy is well positioned as the major player in an industry that is seeing increasing demand, favorable tax and regulatory treatment, and a growing desire on the part of major players in the space to be seen as environmentally friendly. The company should continue to be the top player in biodiesel for the foreseeable future.

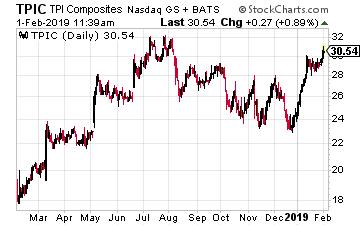

TPI Composites (Nasdaq: TPIC)

With origins in building sailboats, TPI Composites is a manufacturer of composite wind blades for wind power generation. The company has manufacturing facilities in the U.S., four cities in China, Denmark, India, Mexico and Turkey. The wind power generation business is projected to reach $100 billion by 2025, with much of that growth coming from China, where TPI has a strong footprint.

2018 was an investment and transitioning year for the company, as they invested in a large number of start-up blade lines and moved a large amount of production to larger blades. The company is on track to complete, and begin reaping the benefits of, this investment in 2019. This is one reason I believe now is a good time to buy TPIC.

Management is already seeing an above projection interest in its new lines, and CEO Steve Lockard addressed the transition year in their latest conference call stating, “While we’ve had some execution challenges and delays relating to both start-ups and transitions this year, we’re getting better with our customer support at both start-ups and transitions making them happen faster and therefore, less costly.”

It appears the company has learned from this process and is projecting more incremental changes to its products moving forward. This should reduce cost, while still improving the efficiency of its blades. Management also believes the size of current blades is close to the maximum size practicable, and that future blades will be more modular in nature, which should point to increasing profit margins at TPIC.

TPI Composites has averaged 49% earnings growth the past 5 years and is projected to grow earnings 35% annually over the next 5 years. And with this growth profile, the company trades at a PE multiple of only 11. I would like to see a higher profit margin than the current 2%, but I believe the end of the transition period in 2018, along with a move to more modular products, will address that issue.

The demand for renewable energy is rising. Whether in the form of a large utility like NextEra, a biodiesel play like Renewable Energy, or a global wind energy company like TPI Composites, you should take advantage of this rising tide, and place a renewable energy stock in your portfolio.