The next U.S. economic recession is coming. Guaranteed!

It is likely that you are reading many predictions concerning the next recession. Last year the pundits were predicting one for 2019. Now I am seeing more predictions for a recession in 2020 or 2021. These predictions are mostly about marketing, because the people making the guesses on the next recession are betting on a sure thing. The economy does cycle, so at some point in the future we will go through a period of negative economic growth.

Predicting the timing of the next recession is a harder task.

At the current time I would say any prediction that ends up correct was more of a lucky guess than from astute analysis. The economy continues to chug along at a moderate 2% to 3% annual GDP growth rate. The economic indicators that traditionally are leading clues for the next economic slow down are giving mixed signals, with a slight bias towards continued growth. Yet it is good to have a plan and some investments in your portfolio that are recession resistant. There is always the possibility of an unforeseen economic event that pushes the economy into negative growth.

Recession resistant income stocks are those that meet two criteria:

First, they have businesses that will continue to generate revenue and free cash flow even in a negative growth economy.

Second, we want to own shares of companies with above average free cash flow coverage of the current dividend rate. Excess cash flow gives a company’s board of directors’ confidence to not cut dividend rates when the economy is under pressure.

Understand that in a recession driven bear market all stock prices will fall.

As high yield stock investors we want to ride through the bear market and subsequent stock recovery with our dividend earnings intact. This allows us to buy more shares when prices are down and boost portfolio income coming out the other side. Remember for the same reasons a recession is inevitable, so is the following recovery. The economy goes through cycles.

Here are three stocks that should be able to sustain and possibly grow their dividends through the next economic recession.

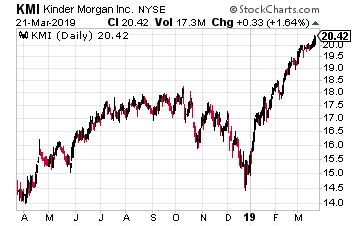

Kinder Morgan Inc. (NYSE: KMI) is a large-cap owner and operator of energy infrastructure assets.

The company owns an interest in or operates approximately 84,000 miles of pipelines and 157 terminals. The pipelines transport natural gas, refined petroleum products, crude oil, carbon dioxide and more. The terminals store and handle petroleum products, chemicals and other products.

Management guidance has 2019 distributable cash flow $5 billion, providing 2.2 times coverage of this year’s dividend payments. That is much better than the typical 1.3 to 1.5 times coverage prevalent in the energy infrastructure space.

Kinder Morgan plans to increase the dividend by 25% this year and next year.

The shares yield 4.0%.

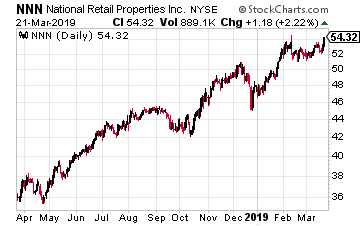

National Retail Properties, Inc. (NYSE: NNN) is a triple-net lease REIT that 3,000 single tenant retail properties in 48 states.

The properties are leased and operated by businesses that won’t go out of business in an economic recession. Think of your local convenience stores, auto parts shops and movie theaters.

For 2018, the company’s dividend payout ratio was 77% of adjusted funds from operations (AFFO). This is very solid dividend coverage for a net lease REIT.

This company has increased its dividend for 29 consecutive years, which means the dividend has grown through the last several economic recessions. That’s a record a Board of Directors will not want to stop.

NNN shares yield 3.8%.

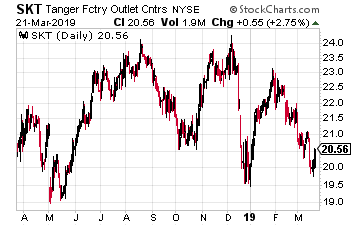

Tanger Factor Outlet Centers (NYSE: SKT) owns and operates 44 outlet center type shopping malls.

Tanger was an originator of this type of mall and is the only pure play outlet center REIT. This type of mall will outperform other retail sectors when the economy is going through a slowdown. People always will shop. They are more likely to shop at an outlet mall if they believe times are tough.

Tanger operates very conservatively, with a low debt ratio and dividend well covered by cash flow. The SKT dividend has been increased every year since the company’s 1993 IPO.

The stock currently yields 7.1%.