Is it possible to double your money – quickly – buying safe dividend stocks? You bet. Let me explain how…

“Basic” income investors are enamored with higher current yields. These are OK for payouts today, but they’re not going to get us 100%+ gains.

For triple-digit profits we must pay attention to the underrated dividend hike. These raises not only increase the yield on your initial investment, but they trigger stock price increases, too.

For example, if a stock pays a 3% current yield and then hikes its payout by 10%, it’s unlikely that its stock price will stagnate for long. Investors will see the new 3.3% yield and buy more shares. They’ll drive the price up, and the yield back down – eventually towards 3%.

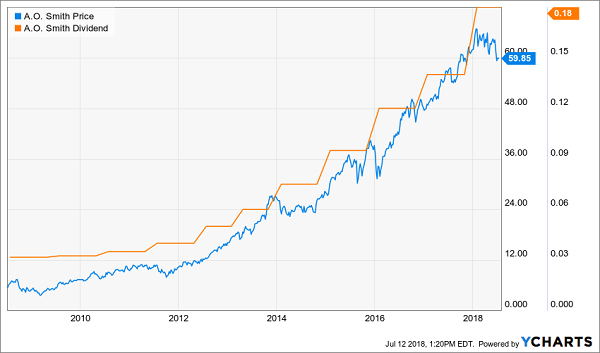

This is why many Dividend Aristocrats don’t pay high current yields: Their prices just rise too fast. Just look at A.O. Smith (AOS), which perpetually yields in the low 1% range. The low yield isn’t from a lack of dividend hikes – in fact, AOS keeps hiking its payout more aggressively over time. But investors just keep chasing the stock too high!

A.O. Smith (AOS): A Boring Company With a Breathtaking Trajectory

What a “problem” to have!

If you’re looking for a “dividend stock double” to bring you secure gains of 100% or better, consider these ten payers. Don’t be fooled by their modest current yields – these dividends will probably always look modest thanks to soaring share prices.

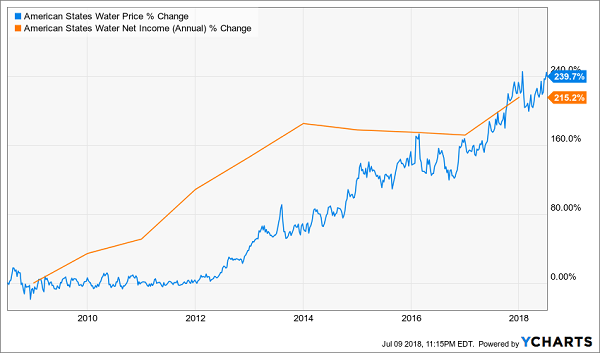

American States Water (AWR)

Dividend Yield: 1.7%

I’ll start off with American States Water (AWR) delivers water up and down California – an absolutely necessary service that its 1 million-plus customers can’t go without. That results in a steady stream of revenues and income – profits that tick higher over time as American States Water slowly raises rates. It’s a well-worn utility story.

What’s a little less common about AWR is its absurd growth.

American States Water (AWR): Is This a Utility … Or a Chip Stock?

Up next for AWR? The company likely will announce its 64th consecutive dividend increase sometime in very early August.

Dover Corporation (DOV)

Dividend Yield: 2.6%

American States Water may have an impressive dividend-growth streak, but it’s not actually a member of the Dividend Aristocrats given its small-cap nature and exclusion from the S&P 500. But Dover (DOV) is full-fledged dividend royalty, touting an equally impressive streak of 62 consecutive years – the longest streak among Aristocrats and the third-longest among all publicly listed companies.

Dover is a widely diversified industrial company whose products range from product-tracing technologies to bench tools to chemical dispensing systems to commercial refrigeration units. That kind of product breadth has allowed the company to weather even the worst economic environments with the dividend not only intact, but growing each and every year.

As a note: A look at a Dover chart shows a big dip in May. Don’t worry. This wasn’t the effect of a nasty earnings surprise, but instead a reflection of the spinoff of Apergy (APY), its oil-and-gas equipment-and-technology business.

Consecutive dividend hike No. 63 should be announced sometime during the first full week in August.

First American Financial Corporation (FAF)

Dividend Yield: 3.0%

Trying to get decent yield from a financial stock is like trying to wring blood from a monkey wrench. The Financial Select Sector SPDR Fund (XLF) exchange-traded fund of banks, insurers and other financial companies yields a miserable 1.6%. That’s why it’s refreshing to come across companies such as First American Financial Corporation (FAF).

FAF sounds like a bank, but it’s actually a top title insurance and settlement services provider used by real estate and mortgage companies. And, like similar companies, it offers a wide array of other products, from home warranties to property and casualty insurance to even investment advice.

First American’s dividend increase schedule has been a little variable over the past five years, but it manages to get the job done at some point. The best bet for FAF’s next increase announcement is sometime in mid-August, with the payout itself coming a month later.

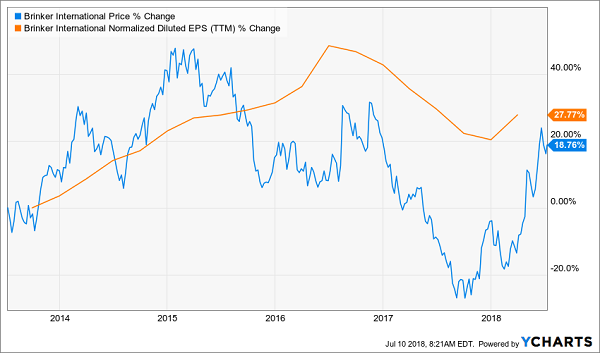

Brinker International (EAT)

Dividend Yield: 3.1%

Brinker International (EAT) isn’t nearly as recognizable a name as the brands that it owns – specifically, Chili’s and Maggiano’s Little Italy restaurants, which combine for more than 1,600 locations worldwide.

Brinker had been struggling mightily amid the “restaurant recession” of the past few years that saw giant chain restaurants but together a huge string of monthly same-store sales declines. Brinker itself delivered a couple disappointing earnings reports that sent investors fleeing EAT shares.

That said, the company is back on the rebound in 2018 as various changes, including a heavily scaled-back menu, are bearing fruit. Brinker scored a beat in its most recent quarterly report (in May), and while same-store sales dipped a bit, the company still is tracking a potential growth year in comps.

Brinker also has been upgrading its dividend for several years now, and given a payout ratio of just more than half its profits, chances are EAT investors will enjoy another dividend-hike announcement sometime in the middle of August.

Chili’s Parent Brinker International (EAT) Tries to Reach Recovery Road

Federal Realty Investment Trust (FRT)

Dividend Yield: 3.2%

Federal Realty Investment Trust (FRT) is a virtual unicorn – a real estate investment trust (REIT) in the Dividend Aristocrats. In fact, at the moment, it’s the only real estate play in the whole hallowed group.

Despite what the name would imply, Federal Realty isn’t a government-real-estate play – it’s a mixed-use retail REIT that focuses on high-end properties in Washington, D.C.; Boston; San Francisco and Los Angeles. To give you an example, FRT is responsible for Pike & Rose – a commercial/dining/living mixed-use development in North Bethesda, Maryland, that includes tenants such as Pinstripes (a bowling-and-bocce bistro), L.L. Bean, REI Co-Op and four apartment-and-condominium communities.

FRT has grown its dividend every year since 1972, from 7.3 cents to its current payout of $1 per share. The next hike should come in either very early August or the tail end of July.

Healthcare Trust of America (HTA)

Dividend Yield: 4.5%

Healthcare Trust of America (HTA) is one of many “Boomer” plays – this one dubbing itself the “largest dedicated owner & operator of medical office buildings in the country.” Specifically, it owns 432 medical office buildings across 33 states covering just about every region in the U.S. minus “Big Sky” country.

I love niches, I love specialties, and HTA has a fairly interesting one. This REIT has specifically targeted between 20 and 25 “gateway markets” that have top university and medical institutions, which means they’re more likely to be hotbeds of future facility growth. That’s smart.

The downside is, so far, while it has led to excellent growth in funds from operations (FFO), it hasn’t led to riches for shareholders, who are sitting on essentially flat performance since 2015.

Healthcare Trust of America (HTA): What Is Wall Street Waiting For?

But HTA is among a few stocks that have seen recent insider buying – a promising sign of confidence from people who are in the know and have real skin in the game. Maybe that’ll be the kick in the pants the stock needs.

Investors also could use a more robust dividend bump than they’re accustomed to. Healthcare Trust’s income growth has been glacial – just 6.1% total over the past five years. Look to see if management is any more generous sometime during early August or very early July, when the company is likeliest to announce its next dividend top-off.

Verizon (VZ)

Dividend Yield: 4.6%

Telecom titan Verizon (VZ) has been a sleepy disappointment in 2018, off 5% year-to-date against a higher market. You can thank a few things for that – an uber-competitive pricing environment for telcos, an earnings disappointment at the beginning of the year, and sluggishness in its Fios video offerings.

It could be worse. AT&T (T) is off by about 15% as Wall Street voices its skepticism over the Time Warner acquisition.

Verizon remains a stable dividend play, however, delivering a yield well north of 4% on a payout-growth streak of 11 years. No. 12 likely will be announced late in August or in the first couple days of September.

Altria Group (MO)

Dividend Yield: 4.8%

We’ve been told for years that tobacco stocks would be miserable investments thanks to increasingly strict government bans on cigarette use and dwindling consumers as anti-smoking campaigns continue to take root. Yet Marlboro maker Altria Group (MO) mostly managed to swim upstream for many years.

But the stock has seemingly come up against a ceiling, peaking a couple of times in 2017 before succumbing to an eventual downtrend. Altria’s earnings report from April tells a lot of the tale – the company still is squeezing out ever-higher profits, at $1.9 billion versus $1.4 billion in the year-ago period. But sales ticked up just a half a percent, and domestic cigarette shipping volumes actually declined by more than 4%.

A 17% decline in 2018 has juiced Altria’s dividend to nearly 5%, however – but so has a dividend hike announced on March 1. That was actually outside the company’s routine, which is to announce any increases in late August. It’s very possible that the hike was The company typically

Altria actually hiked the dividend once this year, from 66 cents to 70 cents per share, but it did so away from its normal dividend-hike schedule. So Altria is actually a stock to watch here in late August – namely, to see whether the company resumes its routine with a summertime dividend improvement, or simply delivered early.

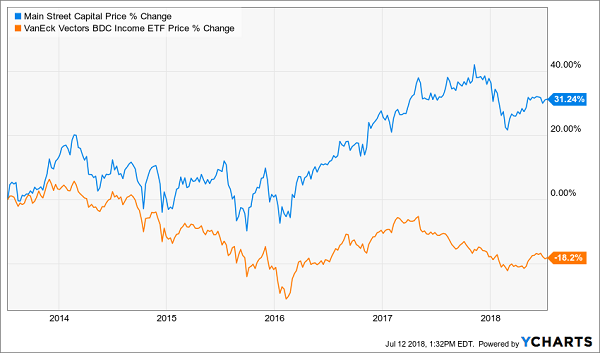

Main Street Capital (MAIN)

Dividend Yield: 5.9%

I have a love-hate relationship with Main Street Capital (MAIN): I love this business development company’s ability to execute, but I hate how expensive the stock typically is! Few BDCs are run as well as Main Street Capital, but you really have to pick your spots.

As a reminder: BDCs help finance small- and midsize businesses. In Main Street’s case, they provide capital for lower and middle-market companies. Their target company has revenues between $10 million and $150 million, and EBITDA between $3 million and $20 million, and Main Street typically will invest anywhere between $5 million and $75 million.

Main Street is one of a few good actors in the space, and its long-term performance reflects that. In fact, MAIN has nearly quadrupled the broader VanEck Vectors BDC Income ETF (BIZD) in total returns over the past five years.

Main Street Capital (MAIN) Is Among the Best in This Brutal Biz

While many BDCs have stagnant dividends, Main Street Capital’s payout keeps ticking higher, even if it’s just by a little bit year after year. The company should announce its next set of monthly payouts at the very beginning of August or the end of July – and there should be a slightly higher number attached to them.

Buckeye Partners LP (BPL)

Distribution Yield: 14.7%

Buckeye Partners LP (BPL) might have the highest yield of any company on this list, but it’s not a product of a hyper-aggressive dividend-growth problem. BPL is earning its yield the wrong way: hemorrhaging shares. The stock is off nearly 60% since mid-2014, in fact, not rebounding with much of the rest of the energy space.

Buckeye Partners is mostly split into two parts – about half of its profits comes from domestic pipelines and terminals, while most of the rest comes from global marine terminals. Despite this diversified business, BPL keeps running into hurdles, such as losing a large storage customer in 2017.

The company has gone so far as to abandon its practice of increasing dividends every quarter, thanks to extremely tight dividend coverage. That having been said, the company still has a 22-year streak of annual dividend increases it probably wants to extend, so it’s entirely possible that Buckeye Partners will offer up a token hike in the first week of August – roughly a year since its last dividend increase.

Lock In 100%+ Dividend Growth Returns

If you want a healthy retirement portfolio, it’s absolutely vital that you stuff it with dividend growth stocks. High-yield stocks with stagnant payouts will actually lose value over time, and your regular income checks won’t stretch as far as they used to thanks to inflation drag. But dividend growth stocks will not only keep you ahead of inflation – they’ll help grow your nest egg, too!

Because, like I showed you with A.O. Smith, the very best dividend stocks will rise in line with their increasing payments.

Most people never realize this. But those of us who DO stand to profit handsomely and almost automatically!

It’s a simple three-step process:

Step 1. You invest a set amount of money into one of these “hidden yield” stocks and immediately start getting regular returns on the order of 3%, 4%, or maybe more.

That alone is better than you can get from just about any other conservative investment right now.

Step 2. Over time, your dividend payments go up so you’re eventually earning 8%, 9%, or 10% a year on your original investment.

That should not only keep pace with inflation or rising interest rates, it should stay ahead of them.

Step 3. As your income is rising, other investors are also bidding up the price of your shares to keep pace with the increasing yields.

This combination of rising dividends and capital appreciation is what gives you the potential to earn 12% or more on average with almost no effort or active investing at all.

I’ve scoured thousands of stocks out there right now, looking for the very best companies that have both rising dividends and strong buyback programs in place … the kind of stocks that could easily spin off annual total returns of 12%, 17%, even 25% or more … doubling your money in very short order.

Right now, at this very moment, there are 7 in particular that I think you should consider buying.

They stand to do well no matter what the broad market does … regardless of what happens in Washington … and irrespective of interest rate trends.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again.

Click here for full details!