Perhaps the most exciting segment of the Singularity for me is the Industrial Internet of Things (IIoT), which will change forever how things are made. It’s the reason some are calling it the Fourth Industrial Revolution.

I’ve written often about two of the main sectors contained in the IIoT. The first is cobots or collaborative robots that will work together with humans in manufacturing. The second is additive manufacturing, which is also known as 3D printing because it involves building objects layer by layer out of substances such as metals or polymers.

But I’ve barely touched upon a third area – digital twins. Let me now fill you on this and point to a few companies heavily involved in the use of digital twins.

What Is a Digital Twin?

A digital twin is a virtual copy of a real machine or system. It is sometimes described as a bridge between the physical and digital worlds. These virtual models are built up based on many gigabytes and terabytes of sensor data. It is an outgrowth today of much cheaper and better sensors, data transmission and data analytics.

In simplest terms, a digital twin works on a simulation platform connected to a predictive analytics platform and which gathers data from a range of sensors from a wide scope of devices/machines and then analyzes the data.

However, a digital twin is not exactly a new concept. NASA developed the concept of a digital twin for its space shuttle program.

Here is a basic example of the usefulness of digital twins: In the past, car companies would build prototypes and then crash them to see whether the cars would hold up to real world situations. Now with digital twins, car companies can use CAD (computer-aided design) data and simulate crashes to see how well their car design will hold up.

Of course, the uses for digital twins extend far beyond cars. It includes oil rigs, jet engines, wind turbines, power plants and pretty much anything worth monitoring.

The value of digital twins to companies is obvious. It offers them numerous advantages throughout the entire lifecycle – from product design, production planning and engineering, to commissioning, operation, servicing and modernization of plant systems and equipment.

Virtual twins allow companies to validate designs earlier and test the configuration of a machine or product or system in the virtual environment. By carrying out checks earlier in the engineering process, the risk of failures and errors in critical phases of the lifecycle, for example during commissioning, is reduced. Eliminating such risks would otherwise only be possible with great effort, cost and time.

Any subsequent modifications can be tested and verified in exactly the same way, accelerating the introduction of a new product. Furthermore, with the help of these virtual models, the operating data can also be used to optimize parameters for production such as energy consumption.

Digital Twin Market Potential

As you can imagine, the potential for virtual twins is vast. According to the German Association for Information Technology, Telecommunications and New Media, every digital twin in the manufacturing industry will have an economic potential of more than 78 billion euros (over $90 billion) by 2025.

A report from TechSci Research says that the digital twin market is expected to grow at a compound annual growth rate (CAGR) of 37% during the forecast period 2017 through 2022. The report points to high demand from the electronics and electrical/machine manufacturing industry as the main driver behind this high growth rate.

Not surprisingly with any rather new technology, the growth geographically is coming from the Asia Pacific region. The firm Research and Markets says that region led the way in 2016 in the overall digital twin market and is expected to continue leading in the 2017 to 2023 period.

This kind of growth rate is what you should look for in an investment and is similar to what I’ve seen in the robotics sector.

Digital Twins Investments

So how can you invest into this exciting new part of the Industrial Internet of Things?

There are a number of very large companies involved in the space including tech giants Microsoft (Nasdaq: MSFT)and Oracle (NYSE: ORCL) as well as industrial powerhouses General Electric (NYSE: GE) and Siemens (OTC: SIEGY).

But instead of these large companies, I prefer the smaller software companies that are involved with CAD design modeling. Here are three companies to consider.

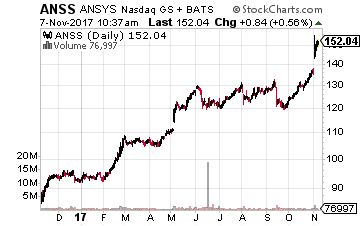

Living in western Pennsylvania, the company at the top of my list is from the area – ANSYS (Nasdaq: ANSS). It is a dominant player in the high-end design simulation software market and is used by most of the well-known manufacturing companies.

Living in western Pennsylvania, the company at the top of my list is from the area – ANSYS (Nasdaq: ANSS). It is a dominant player in the high-end design simulation software market and is used by most of the well-known manufacturing companies.

The company generates revenues in two areas – software licenses (57.5% of 2016 revenues) and maintenance and services (42.5%). Revenues in 2016 were about $988 million. I expect revenues to climb significantly in the years ahead as the company expands its simulation solutions to areas like 5G telecommunications product designs, autonomous vehicles and ADAS systems, as well as the Industrial Internet of Things.

Its stock spiked 10% last week on the back of a great earnings report. It also recently closed a three-year contract worth over $45 million, which was the largest in the company’s history. The stock is now up 60% year-to-date and 77% over the past 12 months.

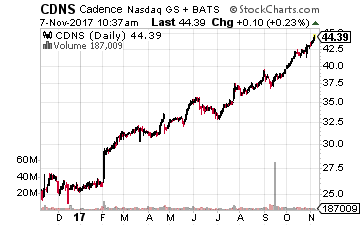

The second company is Cadence Design Systems (Nasdaq: CDNS). Over 90% of its revenue is recurring, which is outstanding.

The second company is Cadence Design Systems (Nasdaq: CDNS). Over 90% of its revenue is recurring, which is outstanding.

In addition to IIoT, it is also involved other fast-growing sectors such as aerospace, autonomous vehicles and augmented and virtual reality (AR/VR). It has won orders from Infineon and MobilEye who are developing advanced driver assistance systems (ADAS) technologies. However, its core currently remains the semiconductor market and the design of integrated circuits.

The stock’s performance has been stellar with a gain of 75% year-to-date and 77% over the past year.

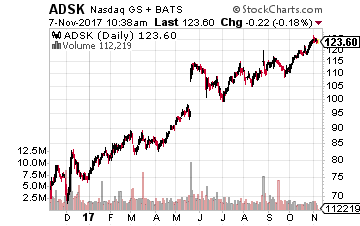

The final company is Autodesk (Nasdaq: ADSK), which generated over $2 billion in revenues in fiscal 2017. It serves customers in architecture, engineering and construction, manufacturing, and digital media and entertainment.

The final company is Autodesk (Nasdaq: ADSK), which generated over $2 billion in revenues in fiscal 2017. It serves customers in architecture, engineering and construction, manufacturing, and digital media and entertainment.

The company’s business transition from licenses to cloud-based services should benefit it over the long-term through higher subscriptions and deferred revenues. Its management forecasts long-term CAGR of 20% from subscriptions that will lead to 24% CAGR in recurring revenues.

That forecast along with its results have propelled the stock 68% higher year-to-date and nearly 80% over the past year. One caution though – on a non-GAAP basis, it is still losing money.

I do expect though all three of these companies’ stocks to continue outperforming the general market.

Buffett just went all-in on THIS new asset. Will you?Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

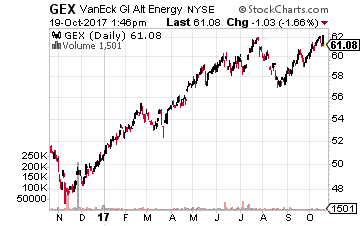

But that doesn’t mean you can’t make money with some U.S.-listed investments. For very broad exposure to the sector, there is the VanEck Vectors Global Alternative Energy ETF (NYSE: GEX). It is up a very nice 21% year-to-date and over 17% the past year.

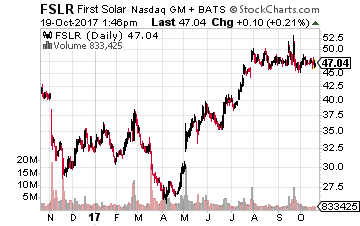

But that doesn’t mean you can’t make money with some U.S.-listed investments. For very broad exposure to the sector, there is the VanEck Vectors Global Alternative Energy ETF (NYSE: GEX). It is up a very nice 21% year-to-date and over 17% the past year. For single stock exposure to solar power, a good choice is First Solar (Nasdaq: FSLR), which is also in GEX’s portfolio. The stock has gained nearly 48% year-to-date. The company is the leading global provider of solar energy solutions with more than 10 gigawatts of installed capacity.

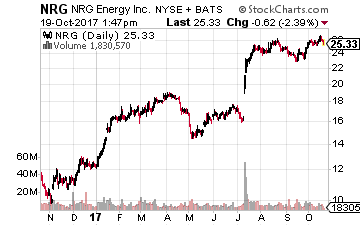

For single stock exposure to solar power, a good choice is First Solar (Nasdaq: FSLR), which is also in GEX’s portfolio. The stock has gained nearly 48% year-to-date. The company is the leading global provider of solar energy solutions with more than 10 gigawatts of installed capacity. Another possible way to play the rush to renewable energy is through a utility that is involved in the sector. One such example is NRG Energy (NYSE: NRG), which is the second-largest U.S. power producer and is expanding its renewable energy operations. Its stock has soared 113% year-to-date and is up 123% over the past 12 months. So even more than the double digits promised in the headline.

Another possible way to play the rush to renewable energy is through a utility that is involved in the sector. One such example is NRG Energy (NYSE: NRG), which is the second-largest U.S. power producer and is expanding its renewable energy operations. Its stock has soared 113% year-to-date and is up 123% over the past 12 months. So even more than the double digits promised in the headline.

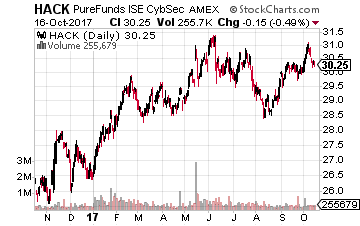

So at the top of my Internet of Things list to buy is something related to cybersecurity. A good, broad-based choice is the ETFMG Prime Cyber Security ETF (NYSE: HACK).The fund’s portfolio consists of 35 stocks and an expense ratio of only 0.60%. The ETF is up nearly 15% year-to-date.

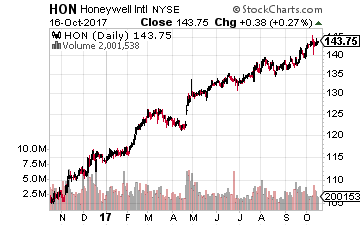

So at the top of my Internet of Things list to buy is something related to cybersecurity. A good, broad-based choice is the ETFMG Prime Cyber Security ETF (NYSE: HACK).The fund’s portfolio consists of 35 stocks and an expense ratio of only 0.60%. The ETF is up nearly 15% year-to-date. Next on my list is an industrial company that is hitting on all cylinders and a major player in the Industrial Internet of Things – Honeywell International (NYSE: HON). Its stock has climbed about 24% so far in 2017. While Honeywell recently announced the spinoff of its home heating and security business as well as its turbocharger unit, the company currently is divided into four divisions:

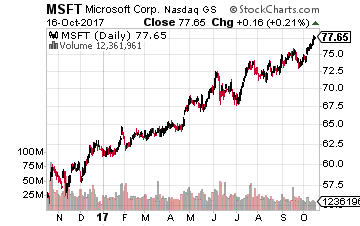

Next on my list is an industrial company that is hitting on all cylinders and a major player in the Industrial Internet of Things – Honeywell International (NYSE: HON). Its stock has climbed about 24% so far in 2017. While Honeywell recently announced the spinoff of its home heating and security business as well as its turbocharger unit, the company currently is divided into four divisions: On the technology side, I’d feel comfortable owning another company hitting on all cylinders, Microsoft. Its stock has jumped 25% so far in 2017.

On the technology side, I’d feel comfortable owning another company hitting on all cylinders, Microsoft. Its stock has jumped 25% so far in 2017.

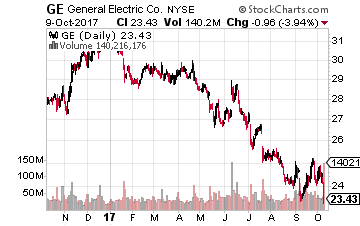

One company that is a believer in additive manufacturing is General Electric (NYSE: GE). In 2016, it introduced additively manufactured metal parts into an aircraft engine – the inside of fuel nozzles. The company says one-third of its new turboprop engine will also be produced using 3D printing, with 12 major 3D-printed parts for the engine section instead of 855 parts. Needless to say, that is a great way to gain control of your supply chain.

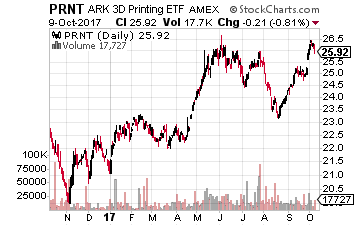

One company that is a believer in additive manufacturing is General Electric (NYSE: GE). In 2016, it introduced additively manufactured metal parts into an aircraft engine – the inside of fuel nozzles. The company says one-third of its new turboprop engine will also be produced using 3D printing, with 12 major 3D-printed parts for the engine section instead of 855 parts. Needless to say, that is a great way to gain control of your supply chain. Normally, I do like to tell you to consider buying a broad-based ETF. And indeed, there is the Ark Invest 3D Printing ETF (BATS: PRNT), which is up 23% year-to-date and 14% over the past 52 weeks.

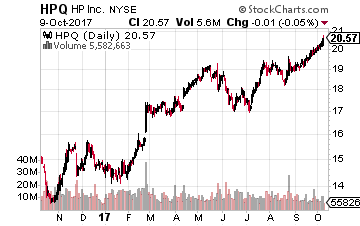

Normally, I do like to tell you to consider buying a broad-based ETF. And indeed, there is the Ark Invest 3D Printing ETF (BATS: PRNT), which is up 23% year-to-date and 14% over the past 52 weeks. No discussion of printing technology would be complete without mentioning the ‘gorilla’ in the space, HP Inc. (NYSE: HPQ), although only 38% of its business is from printers and related businesses. The rest is from PCs, notebooks, etc.

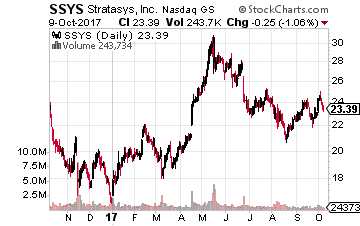

No discussion of printing technology would be complete without mentioning the ‘gorilla’ in the space, HP Inc. (NYSE: HPQ), although only 38% of its business is from printers and related businesses. The rest is from PCs, notebooks, etc. The aforementioned 3D printer used by the McLaren racing team was made by the world’s largest manufacturer of 3D printers, Stratasys (Nasdaq: SSYS). I consider it to be the leader in the sector.

The aforementioned 3D printer used by the McLaren racing team was made by the world’s largest manufacturer of 3D printers, Stratasys (Nasdaq: SSYS). I consider it to be the leader in the sector.

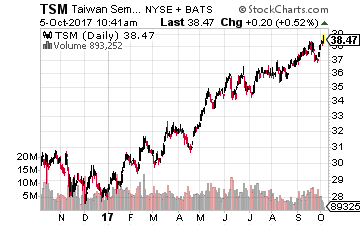

That is simply due to the exorbitant cost of building a new plant to make semiconductors, which are called foundries or fabs. Even back in 2010, a new foundry set Taiwan Semiconductor (NYSE: TSM) back $9.7 billion. Today, that cost is likely doubled.

That is simply due to the exorbitant cost of building a new plant to make semiconductors, which are called foundries or fabs. Even back in 2010, a new foundry set Taiwan Semiconductor (NYSE: TSM) back $9.7 billion. Today, that cost is likely doubled.

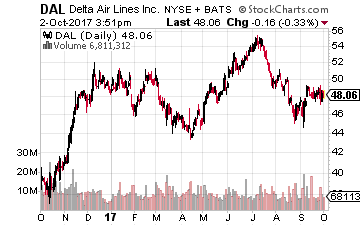

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually. Its revenues fell 3% in 2016 to $39.64 billion, giving its efforts to reduce its debt levels more urgency. Its management is also maintaining capacity discipline while simultaneously trying to modernize its fleet and expand its operations.

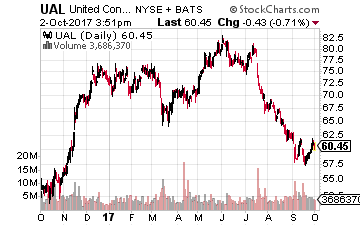

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually. Its revenues fell 3% in 2016 to $39.64 billion, giving its efforts to reduce its debt levels more urgency. Its management is also maintaining capacity discipline while simultaneously trying to modernize its fleet and expand its operations. United is the world’s largest airline, operating about 5,000 flights a day. However, the merger of UAL with Continental has left the merged company with a significant debt load. Its significant exposure to Houston also means it was greatly affected by Hurricane Harvey.

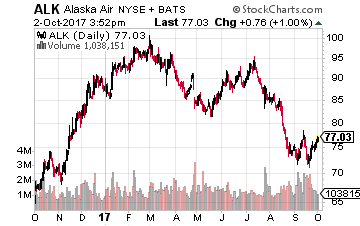

United is the world’s largest airline, operating about 5,000 flights a day. However, the merger of UAL with Continental has left the merged company with a significant debt load. Its significant exposure to Houston also means it was greatly affected by Hurricane Harvey. Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like the purchase of Virgin America, despite the rise in the amount of debt it now has. The company’s August traffic report showed that its load factor (percentage of seats filled by passengers) increased to 86.2% from 85.8% in the year ago period as traffic growth exceeded capacity expansion.

Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like the purchase of Virgin America, despite the rise in the amount of debt it now has. The company’s August traffic report showed that its load factor (percentage of seats filled by passengers) increased to 86.2% from 85.8% in the year ago period as traffic growth exceeded capacity expansion.

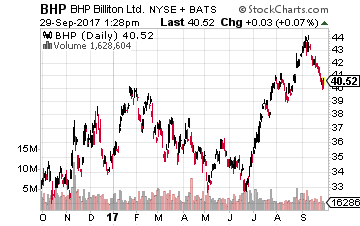

One company worth consideration to buy is the aforementioned diversified miner BHP Billiton (NYSE: BHP). It was the world’s fourth largest producer of copper in 2016 at 1,113 kilotons. A kiloton is equal to about 1,120 of our U.S. tons. BHP’s stock has risen 12% year-to-date and 17.6% over the last 12 months.

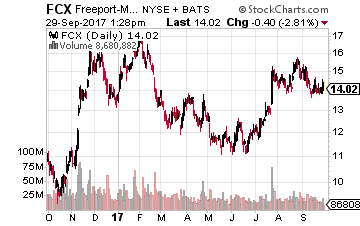

One company worth consideration to buy is the aforementioned diversified miner BHP Billiton (NYSE: BHP). It was the world’s fourth largest producer of copper in 2016 at 1,113 kilotons. A kiloton is equal to about 1,120 of our U.S. tons. BHP’s stock has risen 12% year-to-date and 17.6% over the last 12 months. Next on the list is the world’s largest publicly-traded (Chile’s Codelco is government-owned) copper producer, Freeport-McMoran (NYSE: FCX), which trailed only Codelco in copper production last year (1,696 kilotons). Its stock is up 5.5% year-to-date and 27.5% over the past year.

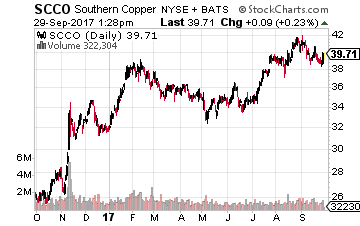

Next on the list is the world’s largest publicly-traded (Chile’s Codelco is government-owned) copper producer, Freeport-McMoran (NYSE: FCX), which trailed only Codelco in copper production last year (1,696 kilotons). Its stock is up 5.5% year-to-date and 27.5% over the past year. Another possibility is the fifth-biggest producer of copper in 2016, Southern Copper (NYSE: SCCO), which indirectly is part of Grupo Mexico and has operations in Peru and Mexico. Its stock rose 22% so far in 2017 and is up more than 46% over the past 52 weeks.

Another possibility is the fifth-biggest producer of copper in 2016, Southern Copper (NYSE: SCCO), which indirectly is part of Grupo Mexico and has operations in Peru and Mexico. Its stock rose 22% so far in 2017 and is up more than 46% over the past 52 weeks.

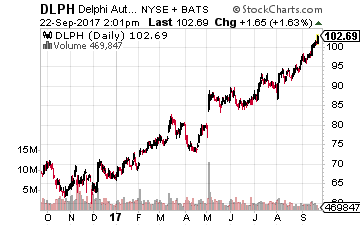

At the top of the list is a company that was once part of General Motors (NYSE: GM), Delphi Automotive PLC (NYSE: DLPH). The spinoff was completed in 1999, as sadly, GM management listened to Wall Street advice about streamlining operations by getting rid of a business “going nowhere.”

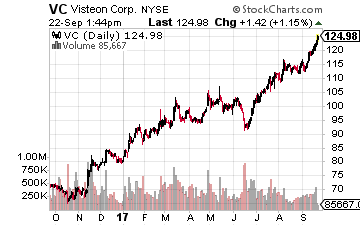

At the top of the list is a company that was once part of General Motors (NYSE: GM), Delphi Automotive PLC (NYSE: DLPH). The spinoff was completed in 1999, as sadly, GM management listened to Wall Street advice about streamlining operations by getting rid of a business “going nowhere.”  The next company to consider was also a spinoff – this time from Ford in 2000 – Visteon (NYSE: VC). The reasons were similar to those of General Motors.

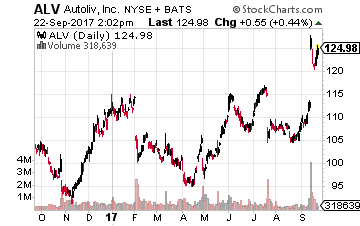

The next company to consider was also a spinoff – this time from Ford in 2000 – Visteon (NYSE: VC). The reasons were similar to those of General Motors. The third company has been a relative laggard, with its stock only up about 8.5% so far in 2017, the Swedish auto parts giant Autoliv (NYSE: ALV). Most of that upward movement in the stock price happened after a recent announcement.

The third company has been a relative laggard, with its stock only up about 8.5% so far in 2017, the Swedish auto parts giant Autoliv (NYSE: ALV). Most of that upward movement in the stock price happened after a recent announcement.

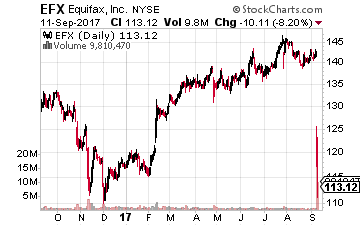

But first, more on this nasty underside of life in the 21stcentury coming to the fore again as the credit-reporting agency Equifax (NYSE: EFX) revealed a massive breach of its cyber defenses.

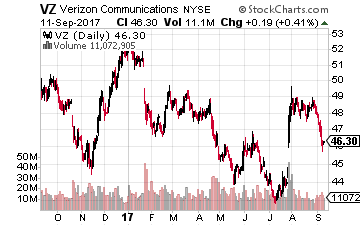

But first, more on this nasty underside of life in the 21stcentury coming to the fore again as the credit-reporting agency Equifax (NYSE: EFX) revealed a massive breach of its cyber defenses. Of course, massive data breaches aren’t confined to just this industry. Last December, Yahoo (now part of Verizon (NYSE: VZ) revealed that attacks between 2013 and 2016 had compromised the personal information of more than a billion users. The data stolen included names, phone numbers, birth dates and passwords.

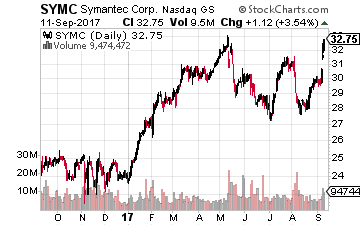

Of course, massive data breaches aren’t confined to just this industry. Last December, Yahoo (now part of Verizon (NYSE: VZ) revealed that attacks between 2013 and 2016 had compromised the personal information of more than a billion users. The data stolen included names, phone numbers, birth dates and passwords. According to a report from cyber security company Symantec (Nasdaq: SYMC), hackers have breached the operational systems of utility companies in the U.S. Symantec says they are lying in wait with the ability to switch off the power and sabotage computer networks.

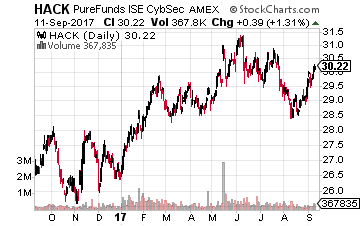

According to a report from cyber security company Symantec (Nasdaq: SYMC), hackers have breached the operational systems of utility companies in the U.S. Symantec says they are lying in wait with the ability to switch off the power and sabotage computer networks. For the broadest possible exposure to the sector, I like the ETFMG Prime Cyber Security ETF (NYSE: HACK). It is up nearly 13% year-to-date and just 10% over the 52 weeks.

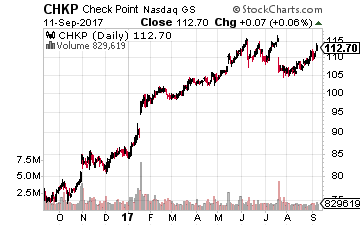

For the broadest possible exposure to the sector, I like the ETFMG Prime Cyber Security ETF (NYSE: HACK). It is up nearly 13% year-to-date and just 10% over the 52 weeks. Palo Alto Networks offers network security solutions, such as next-generation firewall products, to businesses, service providers and governments. As of the end of 2016, the company was third in the security appliance segment (in terms of revenues) trailing only Cisco Systems and Check Point Software Technologies (Nasdaq: CHKP).

Palo Alto Networks offers network security solutions, such as next-generation firewall products, to businesses, service providers and governments. As of the end of 2016, the company was third in the security appliance segment (in terms of revenues) trailing only Cisco Systems and Check Point Software Technologies (Nasdaq: CHKP).