Before the passage of the Tax Cuts and Jobs Act qualified dividends paid by corporations had a perceived tax advantage over fully taxable dividends paid by pass-through businesses like real estate investment trusts (REITs). The new tax law levels the tax playing field for REIT dividends, putting the advantage for investors even more in the camp of the higher yield real estate investment trusts.

Under the old tax rules, REIT investors paid their marginal tax rate on dividends from their REIT shares. For the highest income investors this meant a 39.6% top marginal tax bracket and the 3.8% Medicare surtax. In contrast, qualified dividends paid by regular corporations were subject to a maximum 20% income tax, plus the Medicare surtax. At a glance, REIT investors in the top tax bracket were paying almost twice the tax rate on REIT dividends. What many investors fail to consider is that the net income a corporation generates to pay dividends was taxed at the 35% corporate tax rate, and whatever was left was the money the company had to pay dividends. REITs are pass-through entities for tax purposes, so do not pay corporate income taxes if 90% of net income is passed through to investors as dividends.

Under the new law, the top tax rate for qualified dividends remains at 20%. Corporations did get a tax rate reduction, dropping from 35% down to 21%. I hope that companies take some of those income tax savings and pass them along to investors as higher dividends. It’s too early to tell if that will happen but knowing corporate management teams, I’m not holding my breath.

REIT investors first get new, lower tax brackets. The highest rate has been reduced to 37% from 39.6%. The threshold for the highest bracket has also increased from about $450,000 of income for a married couple to $600,000. Investors in lower tax brackets will also see lower marginal tax rates. In addition –and this is the big news for investors—REIT income gets a 20% deduction before the marginal tax rate is applied. This means a top tax bracket investor has a net 29.6% tax rate on REIT dividends. Married filing joint investors can have income up to $315,000 per year —the top of the 24% tax bracket—and end up with a net REIT dividend tax rate below 20%. Sweet!

If you are new or not highly informed about REITs, it is important to understand that this is not a monolith economic sector. The REIT subsectors cover almost all the different business sectors of the U.S. economy. You can find REITs that focus on properties in sectors such as telecommunications, high-tech data, housing, finance, e-commerce, finance and healthcare, to name a few. You can build a diversified REIT portfolio that will pay a very attractive dividend yield and provide economic diversification. To get you started, here are three REITs from very separate sectors.

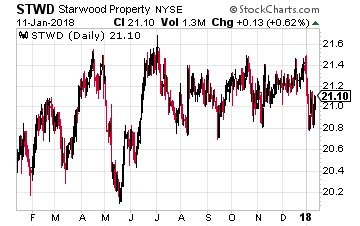

Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT, originates and holds a portfolio of commercial mortgage loans.

Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT, originates and holds a portfolio of commercial mortgage loans.

This is a stock you buy for the high dividend yield, but do not look for a lot of dividend growth.

STWD is one of the largest finance REITs, and from my research, the most conservatively managed, especially regarding protecting the quarterly dividend. This stock currently yields 9.1%.

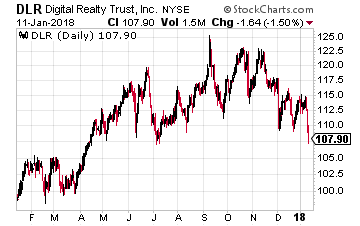

Digital Realty Trust, Inc. (NYSE: DLR) develops owns and operates data center properties. Data storage and management is a huge growth business and many companies prefer to lease space from a data center developer like Digital Realty to house their services and provide the necessary Internet and direct communication links.

Digital Realty Trust, Inc. (NYSE: DLR) develops owns and operates data center properties. Data storage and management is a huge growth business and many companies prefer to lease space from a data center developer like Digital Realty to house their services and provide the necessary Internet and direct communication links.

Investors in DLR can look forward to double digit annual dividend growth for years, if not decades to come. Thus, unlike with STWD above where you’re holding it of the high yield with DLR you’re holding it for the high dividend growth. The shares currently yield 3.5%.

Related: 3 High Growth REITs for Profits in an Amazon World

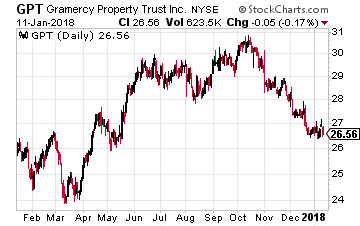

Gramercy Property Trust (NYSE: GPT) is in the process of shifting from a mix of office and industrial properties to focus on the industrial side of their portfolio. Good move! The industrial REIT sector provides necessary support to e-commerce sales, with warehouses and fulfillment centers… sector that grow even if the rest of the country is getting “Amazoned.” For the same amount of sales, the warehouse needs of online retailing are triple the amount of space required by traditional brick and mortar retailers. Industrial real estate profits will grow right along with the growth in e-commerce retail sales. GPT current yields 5.6%.

Gramercy Property Trust (NYSE: GPT) is in the process of shifting from a mix of office and industrial properties to focus on the industrial side of their portfolio. Good move! The industrial REIT sector provides necessary support to e-commerce sales, with warehouses and fulfillment centers… sector that grow even if the rest of the country is getting “Amazoned.” For the same amount of sales, the warehouse needs of online retailing are triple the amount of space required by traditional brick and mortar retailers. Industrial real estate profits will grow right along with the growth in e-commerce retail sales. GPT current yields 5.6%.

Source: Investors Alley

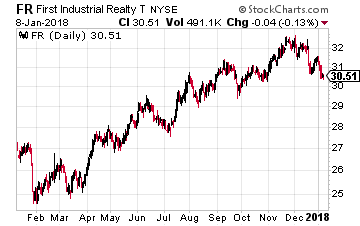

First Industrial Realty Trust, Inc. (NYSE: FR) acquires, owns and leases out industrial properties used by light industrial, warehouse and R&D companies. The company has grown its dividend by over 100% over the last two years, including a 10.5% increase last year. For the first nine months of 2017, FFO per share was up 7.5%. First Industrial pays out about 50% of FFO as dividends. Net income per share growth – which drives the minimum dividend paid – indicates another 10% dividend increase is probable.

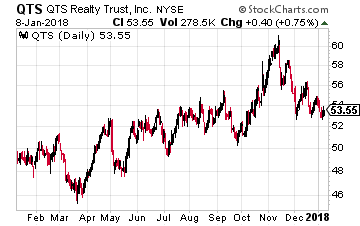

First Industrial Realty Trust, Inc. (NYSE: FR) acquires, owns and leases out industrial properties used by light industrial, warehouse and R&D companies. The company has grown its dividend by over 100% over the last two years, including a 10.5% increase last year. For the first nine months of 2017, FFO per share was up 7.5%. First Industrial pays out about 50% of FFO as dividends. Net income per share growth – which drives the minimum dividend paid – indicates another 10% dividend increase is probable. QTS Realty Trust Inc (NYSE: QTS) is a mid-cap – $2.5 billion value – data center REIT that came to market with an October 2013 IPO. The company is growing rapidly, but FFO per share growth is lagging revenue growth. Reported 2017 adjusted FFO per share was up 5% for the first nine months of last year. In February 2017, the company announced an 8.3% dividend boost.

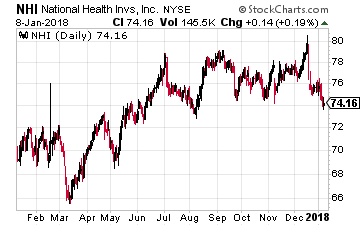

QTS Realty Trust Inc (NYSE: QTS) is a mid-cap – $2.5 billion value – data center REIT that came to market with an October 2013 IPO. The company is growing rapidly, but FFO per share growth is lagging revenue growth. Reported 2017 adjusted FFO per share was up 5% for the first nine months of last year. In February 2017, the company announced an 8.3% dividend boost. National Health Investors Inc. (NYSE: NHI) is engaged in the business of owning and financing healthcare properties. Its portfolio consists of real estate investments in independent living facilities, assisted living facilities, entrance-fee communities, senior living campuses, skilled nursing facilities, specialty hospitals and medical office buildings. Last year the company increased its dividend by 5.6%. Through the 2017 third quarter AFFO per share was up 9.3% compared to the same period in 2016.

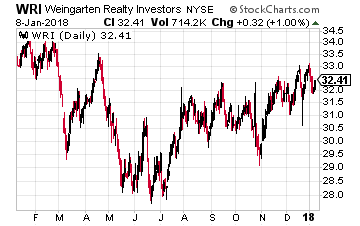

National Health Investors Inc. (NYSE: NHI) is engaged in the business of owning and financing healthcare properties. Its portfolio consists of real estate investments in independent living facilities, assisted living facilities, entrance-fee communities, senior living campuses, skilled nursing facilities, specialty hospitals and medical office buildings. Last year the company increased its dividend by 5.6%. Through the 2017 third quarter AFFO per share was up 9.3% compared to the same period in 2016. Weingarten Realty Investors (NYSE: WRI) is engaged in the business of owning, managing and developing retail shopping centers. Its 230 plus properties consist primarily of neighborhood and community shopping centers. This REIT has increased its dividend every year since 2010. Last year the company increased its quarterly dividend by 5.5% and paid a special $0.75 per share dividend in December. For the first three quarters of 2017, core FFO per share was 5.8% higher than over the same period in 2016. Another 6% dividend increase in 2016 seems probable. The next dividend will be announced in mid-February. Ex-dividend will occur in early March, with a mid-March payment date. WRI currently yields 4.8%.

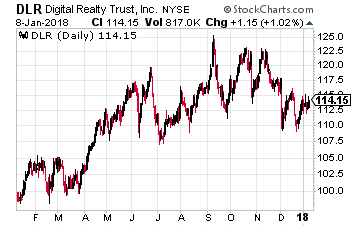

Weingarten Realty Investors (NYSE: WRI) is engaged in the business of owning, managing and developing retail shopping centers. Its 230 plus properties consist primarily of neighborhood and community shopping centers. This REIT has increased its dividend every year since 2010. Last year the company increased its quarterly dividend by 5.5% and paid a special $0.75 per share dividend in December. For the first three quarters of 2017, core FFO per share was 5.8% higher than over the same period in 2016. Another 6% dividend increase in 2016 seems probable. The next dividend will be announced in mid-February. Ex-dividend will occur in early March, with a mid-March payment date. WRI currently yields 4.8%. Digital Realty Trust, Inc. (NYSE: DLR) is a large-cap data center REIT with an 11-year history of above average dividend growth. Last year, the dividend was increased by 5.7%, compared to the 10-year average annual double-digit percentage bump. Growth in 2017 has improved and I expect a 7% to 9% dividend increase for 2018.

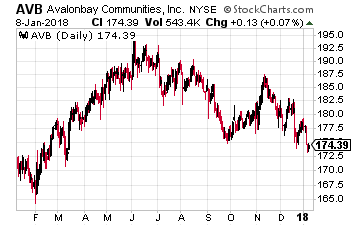

Digital Realty Trust, Inc. (NYSE: DLR) is a large-cap data center REIT with an 11-year history of above average dividend growth. Last year, the dividend was increased by 5.7%, compared to the 10-year average annual double-digit percentage bump. Growth in 2017 has improved and I expect a 7% to 9% dividend increase for 2018. AvalonBay Communities Inc (NYSE: AVB) business is the development, redevelopment, acquisition, ownership and operation of multifamily (apartment) communities primarily in New England, the New York/New Jersey metro area, the Mid-Atlantic, the Pacific Northwest, and Northern and Southern California. The company is focused on the high-end of the apartment spectrum. AVB stopped growing dividends, but did not cut them, from 2008 through 2011. In recent years, the payout has grown by mid-single digits, including a 5.2% increase in 2017. FFO growth in 2017 points to another 5% to 6% increase this year. AvalonBay announces a new dividend rate in early February, with an end of March record date and payment in April. The stock yields 3.3%.

AvalonBay Communities Inc (NYSE: AVB) business is the development, redevelopment, acquisition, ownership and operation of multifamily (apartment) communities primarily in New England, the New York/New Jersey metro area, the Mid-Atlantic, the Pacific Northwest, and Northern and Southern California. The company is focused on the high-end of the apartment spectrum. AVB stopped growing dividends, but did not cut them, from 2008 through 2011. In recent years, the payout has grown by mid-single digits, including a 5.2% increase in 2017. FFO growth in 2017 points to another 5% to 6% increase this year. AvalonBay announces a new dividend rate in early February, with an end of March record date and payment in April. The stock yields 3.3%.

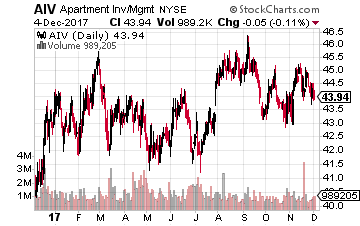

Apartment Investment and Management (NYSE: AIV) is a mid-cap sized REIT that owns and operates about 140 apartment communities. About 40% of the company’s properties are in coastal California, with the balance spread across major U.S. metropolitan areas. Last year, AIV increased its dividend by 9.0%. Cash flow growth has been comparable in 2017, and I forecast an 8% to 10% dividend increase in January. The new dividend rate announcement will come out in late January with a mid-February ex-dividend date and payment at the end of February. AIV yields 3.3%.

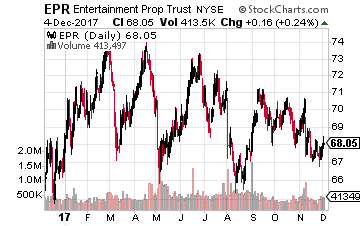

Apartment Investment and Management (NYSE: AIV) is a mid-cap sized REIT that owns and operates about 140 apartment communities. About 40% of the company’s properties are in coastal California, with the balance spread across major U.S. metropolitan areas. Last year, AIV increased its dividend by 9.0%. Cash flow growth has been comparable in 2017, and I forecast an 8% to 10% dividend increase in January. The new dividend rate announcement will come out in late January with a mid-February ex-dividend date and payment at the end of February. AIV yields 3.3%. EPR Properties (NYSE: EPR) focuses its real estate investments in three different business sectors. Primary is the ownership and triple-net leasing of entertainment complexes and multiplex theaters. The second sector is the ownership of golf and ski recreation centers, also triple-net leased. The third sector is the construction, ownership and leasing of private and charter schools. EPR pays monthly dividends, and has grown the dividend rate by an average of 7% per year for the last six years. In 2017 the company was active in both acquisitions and new developments. The new dividend rate is announced in mid-January, with an end of January record date and mid-February payment. EPR currently yields 6.0%.

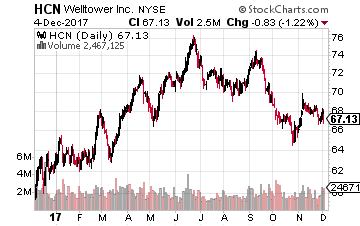

EPR Properties (NYSE: EPR) focuses its real estate investments in three different business sectors. Primary is the ownership and triple-net leasing of entertainment complexes and multiplex theaters. The second sector is the ownership of golf and ski recreation centers, also triple-net leased. The third sector is the construction, ownership and leasing of private and charter schools. EPR pays monthly dividends, and has grown the dividend rate by an average of 7% per year for the last six years. In 2017 the company was active in both acquisitions and new developments. The new dividend rate is announced in mid-January, with an end of January record date and mid-February payment. EPR currently yields 6.0%. Welltower Inc (NYSE: HCN) is a large cap healthcare sector REIT. The company owns interests in properties concentrated in markets in the United States, Canada and the United Kingdom. The portfolio is divided into three segments consisting of: Seniors housing and post-acute communities, and outpatient medical properties. Triple-net properties include independent living facilities, independent supportive living facilities, continuing care retirement communities, assisted living facilities, care homes with and without nursing, Alzheimer’s/dementia care facilities, long-term/post-acute care facilities and hospitals. Outpatient medical properties include outpatient medical buildings. Welltower has increased its dividend every year since 2009, with a modest 1.2% increase to start 2017. I expect a 2.0% to 2.5% increase to be announced in January. The announcement will come out at the end of the month, with an early February record date and payment around February 20. The stock yields 5.1%.

Welltower Inc (NYSE: HCN) is a large cap healthcare sector REIT. The company owns interests in properties concentrated in markets in the United States, Canada and the United Kingdom. The portfolio is divided into three segments consisting of: Seniors housing and post-acute communities, and outpatient medical properties. Triple-net properties include independent living facilities, independent supportive living facilities, continuing care retirement communities, assisted living facilities, care homes with and without nursing, Alzheimer’s/dementia care facilities, long-term/post-acute care facilities and hospitals. Outpatient medical properties include outpatient medical buildings. Welltower has increased its dividend every year since 2009, with a modest 1.2% increase to start 2017. I expect a 2.0% to 2.5% increase to be announced in January. The announcement will come out at the end of the month, with an early February record date and payment around February 20. The stock yields 5.1%.

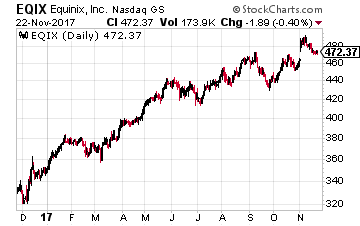

Equinix, Inc. (Nasdaq: EQIX) owns and leases spaces in the datacenter properties it owns. The company has a global footprint with 180 data centers located on every populated continent. Equinix converted to REIT status in late 2014 and started paying dividends for the first quarter of 2015.

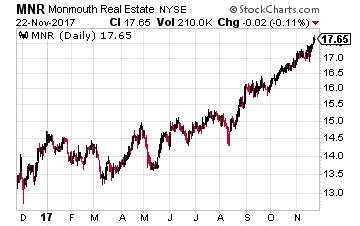

Equinix, Inc. (Nasdaq: EQIX) owns and leases spaces in the datacenter properties it owns. The company has a global footprint with 180 data centers located on every populated continent. Equinix converted to REIT status in late 2014 and started paying dividends for the first quarter of 2015. Monmouth Real Estate Investment Corp (NYSE: MNR) is an industrial property REIT that owns 108 warehouse and logistics properties. Monmouth is unique in that 54.5% of its revenue comes from lease contracts with leases from FedEx Ground, FedEx Express, and FedEx Supply Chain Services. To be blunter, Monmouth Real Estate is a significant landlord for FedEx. FedEx has evolved into a dominant logistics company including delivery of online sales purchases. Monmouth’s industrial properties are “mission critical” for the processing and delivery of online retail sales. The company recently boosted its quarterly dividend by 6.25%. The stock yields 3.9%.

Monmouth Real Estate Investment Corp (NYSE: MNR) is an industrial property REIT that owns 108 warehouse and logistics properties. Monmouth is unique in that 54.5% of its revenue comes from lease contracts with leases from FedEx Ground, FedEx Express, and FedEx Supply Chain Services. To be blunter, Monmouth Real Estate is a significant landlord for FedEx. FedEx has evolved into a dominant logistics company including delivery of online sales purchases. Monmouth’s industrial properties are “mission critical” for the processing and delivery of online retail sales. The company recently boosted its quarterly dividend by 6.25%. The stock yields 3.9%. With a $35 billion market cap, Prologis Inc (NYSE: PLD) is the largest industrial REIT. The company is the world’s leading owner, operator and developer of logistics real estate. It is likely that almost every product sold by online retailers passes once or more through a Prologis owned property.

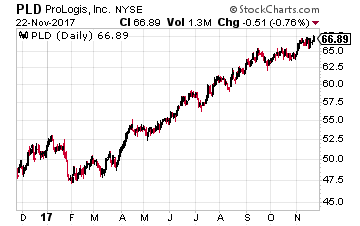

With a $35 billion market cap, Prologis Inc (NYSE: PLD) is the largest industrial REIT. The company is the world’s leading owner, operator and developer of logistics real estate. It is likely that almost every product sold by online retailers passes once or more through a Prologis owned property.

Targa Resources Corp (NYSE: TRGP) engages in the following energy midstream services:

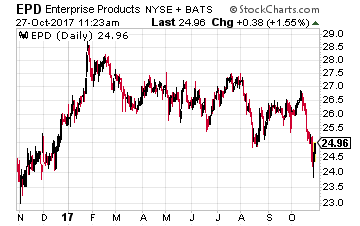

Targa Resources Corp (NYSE: TRGP) engages in the following energy midstream services: Enterprise Products Partners LP (NYSE: EPD) has a market cap more than $50 billion and is the largest MLP by enterprise value. The company’s business segments include:

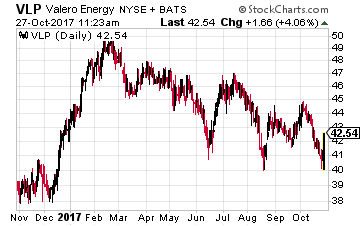

Enterprise Products Partners LP (NYSE: EPD) has a market cap more than $50 billion and is the largest MLP by enterprise value. The company’s business segments include: Valero Energy Partners LP (NYSE: VLP) is controlled by and provides pipeline, storage and terminal services to its sponsor, Valero Energy Corporation (NYSE: VLO). Through asset drops from Valero, the cash flow and distribution growth at VLP is very predictable. The VLP payments to investors will grow 25% in 2017 and at least by 20% in 2018, with high probability for 20% growth in future years. Now at $41, VLP could easily surpass its 52-week high of $51. The units currently yield 4.7%.

Valero Energy Partners LP (NYSE: VLP) is controlled by and provides pipeline, storage and terminal services to its sponsor, Valero Energy Corporation (NYSE: VLO). Through asset drops from Valero, the cash flow and distribution growth at VLP is very predictable. The VLP payments to investors will grow 25% in 2017 and at least by 20% in 2018, with high probability for 20% growth in future years. Now at $41, VLP could easily surpass its 52-week high of $51. The units currently yield 4.7%.