Tim Plaehn is the lead investment research analyst for income and dividend investing at Investors Alley. He is the editor for The Dividend Hunter, an investment advisory delivering income investments with double digit growth in share price and dividend payments, and 30 Day Dividends, a specialty income service that takes advantage of opportunities for relatively fast, attractive profits around potential dividend payouts. Prior to his work with Investors Alley, Tim was a stock broker, a Certified Financial Planner, and F-16 Fighter pilot and instructor with the United States Air Force. During his time in the service he was stationed at various military locations in the U.S., Europe, and Asia. Tim graduated from the United States Air Force Academy with a degree in mathematics. Learn about Tim's new investment strategy for collecting income from the market each and every month without the use of options, futures, forex, covered calls, or risky trading strategies.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

With my focus on higher yield investments, I often receive questions about various closed-end funds. CEFs are actively managed investment pools with shares that trade on the stock exchanges.

A lot of these funds carry very attractive yields. The danger is that this is an asset class where it is hard to separate the good from the bad from the truly ugly. Here are some danger signs and CEFs that illustrate those dangers.

There are over 500 CEFs trading on the U.S. stock exchanges. A large portion of the funds own municipal bonds and pay dividends that are the pass-through vehicles for the tax-free interest paid by munis.

These funds require different investment criteria and are a topic for another day. Today the focus is on CEFs in the taxable side of the investment universe. The group includes stock funds, bond funds, and hybrid funds.

Evaluating individual closed-end funds can be frustrating. Many fund managers are not very forthcoming about what the own in the portfolios and how they implement investment strategies. Here are some clues with examples that show potential closed-end fund problems.

Share price to NAV premiums. A defining feature of closed-end funds is that once a fund is launched, the management company will not buy back shares. Shares only trade on the stock exchange. That means a CEF will have two share prices, the market price and the net asset value (NAV).

Both deep discounts and high premiums to NAV are danger signals. If you pay a premium for NAV shares, you are paying more than the portfolio assets are worth. Premiums can collapse leading to losses in your fund investments.

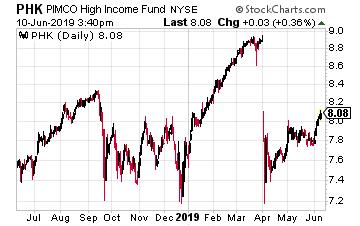

The PIMCO High Income Fund (PHK) currently trades at a 29.0% premium to NAV. This means you pay almost $1,300 for $1,000 worth of bond assets. The chart shows how the share price collapsed in in the Spring even has the NAV was stable to rising.

From the price to NAV premium alone, this is a CEF to sell, not buy. If it was on an investor’s buy list, the best course is to wait until the spread again reaches a low teens percentage, comparable to where it was at the end of 2017.

This closed-end fund is not worth the 10.6% yield.

CEF dividends are not always dividends. Closed-end funds can establish what are called managed distribution schemes. This lets a fund pay level dividends, even if the portfolio income is uneven. What are paid as dividends may be portfolio income, realized capital gains or even return of investor capital –ROC. While some ROC is not destructive to the portfolio value, it is a danger signal and may indicate the fund manager is selling assets to keep paying the dividend. That will erode the NAV over time.

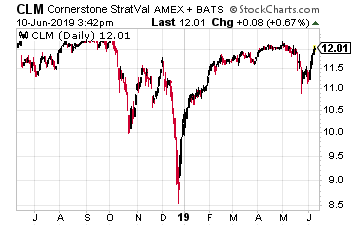

Cornerstone Strategic Value Fund (CLM) is a global equities fund with a 20% yield. CLM is paying a $0.2035 per share monthly dividend. Unfortunately, well over half of the dividend history for the last two years has been ROC.

So far in 2019, 79.7% of the dividends paid have been classified as ROC. That’s 80% of each dividend coming back as a return of the investors’ own money. The paying out of principal instead of earnings will lead to dividend cuts.

To start 2019 this fund slashed the monthly payout by 13%. This fund is an example of a CEF with an eye-popping yield that in reality provides a false sense of investment gains.

CLM is a fund to sell, not own.

Rising interest rates will be bad for bond funds. In the world of taxable CEFs, there are similar numbers of stock funds and bond funds. For bond funds, an increase in interest rates will lead to falling bond prices. The longer the maturity of bonds owned, the steeper the price decline.

Preferred shares are bond-like investments that typically do not have maturity dates. In a rising rate environment, preferred stocks share will decline even more than bond prices.

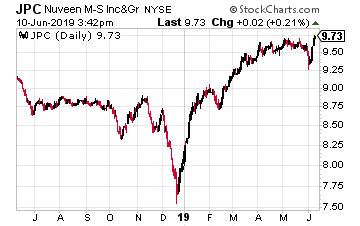

Nuveen Preferred Income Opportunities Fund (JPC) is a closed-end fund that owns a portfolio of debt securities and preferred stock.

79% of the portfolio has time to maturities more than 20 years. This is not the portfolio to own if long term rates start to increase. In additional to the long maturities, the PRF portfolio is 34% leveraged.

In a rising rate environment, the cost of leverage will go up, and that leverage will multiply the bond value drop.

This is a fund to sell if you think interest rates will go up in the next few years and is not worth the 7.5% yield.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

For an investor trying to build wealth, the massive amount of news coming out of the financial media can be contradictory and confusing. Investors often don’t realize that there are two sides to every stock trade.

The seller doesn’t want to own the shares for a range of reasons, and the buyer does so with the belief that the share price will go up. One key to success is to understand which financial news is “real” and which is rumor or opinion, and thus “fake.”

Here are some tips that help you decide whether the stock market information you are hearing, or reading is actual, useful information, or is something we can drop into the “fake news” file.

• Real News: Information provided directly from the company behind the stock. The best of these are the quarterly and annual earnings reports. Income statements and balance sheets give accurate pictures of how a company is operating. Also useful are press releases on other topics and management comments during conference calls and Q and A sessions.

• Fake News: Short term market reactions and financial news comments about an earnings report. Wall Street analysts generate earnings forecasts that are just estimates, and the stock market treats it them as hit or miss targets. Also, in the fake news category are financial writer analysis articles. They can be useful to get an educated opinion, but they are not a substitute for doing your own analysis.

• Real News: Dividend payments. Dividends are a cash return on your investment that cannot be clawed back. Dividends are how a company shares profits with shareholders. If a company can grow profits, it will also grow the dividend payments. Looking at history and monitoring continued dividend payments are a great way to monitor a company’s financial success.

• Fake News: Counting on share price gains as sustainable and predictable profits. It can be surprising how quickly a stock that shows as a profit in your brokerage account can drop and wipe out your gains, and even go to a loss.

The challenge of expecting share appreciation to fuel your expected investment returns is that at some point you need to find another investor willing to buy your shares at a higher price. Trying to pick tops and bottoms in the stock market and share prices is a very difficult, if not impossible, way to build and sustain wealth.

• Real News: To build wealth or sustain a nest egg to last for decades, you need an investment strategy that will work through the stock market cycles. This means being ready to manage and invest during corrections and bear markets as well as when stocks are going up. In my newsletters I discuss strategies focused on building a dividend income stream. Whatever system and strategy selected, you should know how you are going to handle the periods when stock values are falling.

• Fake News: Hot tips and get rich quick offers are designed to separate investors from their money and not to help them actually succeed in reaching their investment goals. Think about this: If someone has a system that will turn a few thousand dollars into millions, why do they need to sell it?

The bottom line to this discussion is that successful investing for the long term will be based on fundamental analysis of the companies behind the shares. Dividend history and payments are a great way to track how well a company is doing, and an attractive yield is a great return in itself.

Here are three stocks currently out of favor with the market with great long term potential.

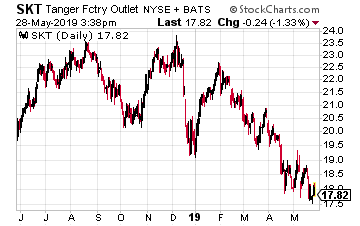

Tanger Factory Outlet Centers, Inc. (SKT) is a pure play owner of outlet style shopping centers. It is the only REIT focused on this type of retail space. Tanger has increased its dividend rate every year since the company’s 1996 IPO.

The recent “fake news” about the end of brick and mortar retail has driven the SKT share price down to around $18, compared to a high over $41 two years ago. The company is financially conservatively managed, and at some point, will resume a growth trajectory. Right now, value oriented investors can pick up shares with a 7.9% yield and annual dividend increases.

History shows that retail trends go through repeating cycles, and when retailers are again opening more stores than closing them, Tanger will be a great stock to own.

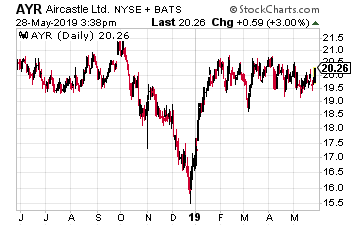

Aircastle Limited (AYR): is an aircraft leasing company that has almost 300 commercial planes leased to airlines around the world.

There are many factors that have “fake” news effects on the Aircastle share price. These include the global economic predictions, forecast travel plans, and the Boeing 737 Max problems. Good news is that Aircastle doesn’t own any 737’s.

Despite all the events that investors believe will affect the company’s results, Aircastle is a very profitable company with steady revenue and free cash flow growth. The dividend will be increased by 6% to 9% per year, generating attractive long term total returns, especially if you add shares on any dips.

Current yield is 6.0%.

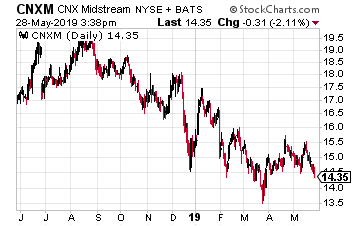

CNX Midstream Partners LP (CNXM) is a is a master limited partnership that owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia.

This MLP is managed and sponsored by CNX Resources Corporation. The share values of both CNX and CNXM are down on lower natural gas prices. However, as a midstream services provider, CNXM operates as a fee based business whose revenues are not dependent on natural gas prices.

The MLP’s management team has stated they are targeting 15% annual distribution growth. Combine that growth with a current 9.7% yield and you have tremendous total return potential.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Last week I was an invited speaker at the Las Vegas MoneyShow and made several presentations concerning income and dividend stock investing. I like the Q&A portion at the end of each talk. I benefit from learning what income focused investors are most interested in.

One topic that came up several times was my opinion in general about closed-end funds. A lot of these funds sport double digit dividend yields, which are catnip to income focused investors.

Closed-end funds (CEFs) are actively managed investment portfolios, whose shares trade on the stock exchanges. The closed-end part of the name is because these funds raise their initial capital with a one time sale through investment brokers and after that, the fund managers do not issue or redeem shares. The structure of CEFs produce a few interesting effects.

One is that share prices on the stock exchanges can be at significant premiums or discounts to the individual funds’ net asset values (NAV).

Another is that CEF fund managers cannot readily be influenced by share owners. Also, a lot of these funds are opaque concerning holdings and investment strategies.

It is my opinion that Wall Street firms use closed-end funds as a dumping ground for debt securities they manufacture that turn out to be more toxic than beneficial for investors in those securities.

Because of these reasons, I mostly stay away from the entire CEF sector. It would be too much work to analyze the hundreds of funds trading on the market to find the possible handful that are doing a good job. My recommendation to investors that ask me about CEFs is that there are better, safer ways to invest in high-yield securities.

Here are five CEFs with tempting yields where you should avoid that temptation:

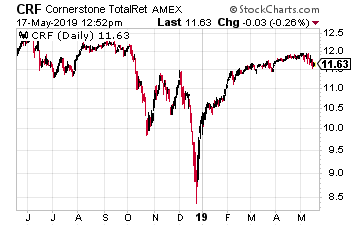

Cornerstone Total Return Fund (CRF) has the stated goal of seeking capital appreciation with current income through investment in common stocks, preferred stocks and convertible stock of large, mid and small cap companies and investment grade U.S. debt securities.

Current yield on the shares is an eye-popping 20.4%. A little digging shows why the yield is so high.

The fund’s policy is to pay out monthly dividends at a rate equal to 21% of the net asset value based on the NAV of the previous year.

The fund’s literature states “The Distribution Percentage is not a function of, nor is it related to, the investment return on a Fund’s portfolio.”

Basically, the big yield on CRF is the fund paying you back your own money. To add insult, CRF trades at a 7% premium to NAV. To buy the shares you pay $1.07 for a dollar’s worth of assets, which are then paid back to you as “dividends”.

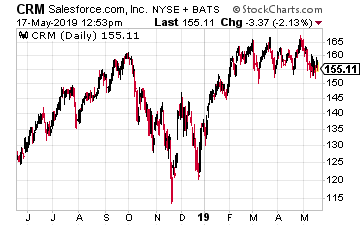

Cornerstone Strategic Value Fund (CRM) seeks long term capital appreciation through investment in global equity securities. Like Cornerstone above, this fund also yields 20% because it has the same dividend policy as its stablemate CRF.

Again the 20% is not a real return, but instead is likely to be the fund paying back your own capital. CRM currently trades at a 6% premium to NAV. These two funds, CRF and CRM are ones that I often get asked about. Looking at the distribution history, the dividends have ranged between 50% and 100% as return of capital.

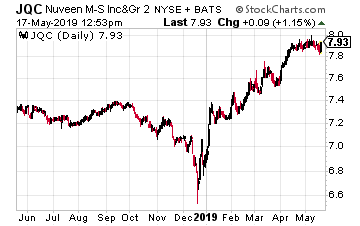

Nuveen Credit Strategies Income Fund (JQC) currently yields 15% and trades at an 8% discount to NAV. The fund invests in corporate debt securities or loans.

At the end of 2018 the fund adopted a capital return plan where now a portion of each dividend is explicitly return of capital. 63% of each monthly dividend is a return of your own money.

I think that is a pretty sneaky way for a fund management company to attract investors with a big stated yield. At least they make it very clear in the fund’s website exactly what they are doing.

But how many investors take the time to dig through a CEF’s website to see where the dividends come from?

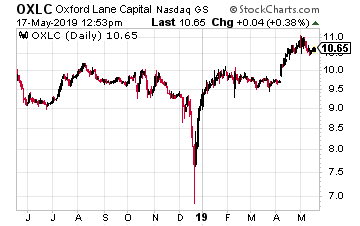

In contrast to the previous funds Oxford Lane Capital (OXLC)reports that 100% of its dividends are earned income. The fund sports a 15% yield.

The danger comes from its investment portfolio of debt and equity tranches of CLO vehicles. CLO means collateralized loan obligations. These are the type of securities manufactured out of pools of loans that caused the 2007-2008 financial crisis.

There is a huge amount of risk in this fund’s portfolio. The management team uses almost 40% leverage on the portfolio to leverage the highly leveraged securities it holds.

Finally, the shares trade at a 40% premium to NAV. Holy cow! What a time bomb.

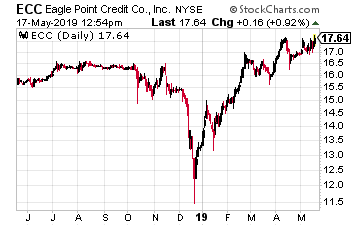

Eagle Point Credit Company LLC (ECC)also invests primarily in equity and junior debt tranches of CLOs. As I noted above, CEFs are a popular home for high risk securities.

For the last seven months 7 cents out of each 20 cent monthly dividend has been classified as return of capital, so the fund is not earning the dividends.

Current yield is 13.8% and the shares are trading at a 22% premium to NAV. That type of premium shows investors are buying shares without any understanding how the fund operates.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

The Las Vegas MoneyShow kicked off on Monday with a 600 point drop in the Dow Jones Industrial Average. Not a good stock market start for a conference focused on investment strategies and idea.

My first presentation was one of the earliest on the schedule for Monday morning. The groups I talked to were very interested in learning about dividend-centric strategies that don’t rely on share price appreciation.

Over the last five years, my presentations have evolved to spend more time on developing individual portfolio strategies. I now like to talk with investors about developing individual strategies.

The fact is that without an investment plan, most investors are doomed to the greed and fear cycle of buying high and selling low. Whatever strategy you develop should be designed to take the emotion of your investment decisions.

Here is a good anecdote from this year’s MoneyShow so far. I know the reps and portfolio managers from Reaves Asset Management well.

They have done exclusive online conference calls with my subscribers. I ran into one of the Reaves guys in the hall, said hi, and he was happy to let me know that utilities were the one stock market sector having a up day.

The folks at Reaves Asset Management run private money and a pair of publicly traded utility focused funds. The Reaves Utility ETF (UTES) is the only actively managed utility stocks focused ETF.

The fund has consistently out performed (by a small amount) the utilities index since its 2015 launch. Through April 30, over the last year, UTES has returned 18.2%. To compare, for the same period the SPDR S&P 500 ETF (SPY) returned 13.3%.

UTES is a nice ETF to hold in turbulent times for the stock market.

My presentations are mostly about strategies and techniques individual investors can use to build their own portfolios. However, I know the attendees love to hear stock ideas, and one from my first presentation was also one of the few stocks going up while the market went steeply down.

That stock is NextEra Energy Partners (NEP). This company is in the “Yieldco” category, similar to sponsored oil and gas infrastructure asset stocks.

NEP owns interests in wind and solar projects in the U.S., as well as natural gas infrastructure assets in Texas. The shares yield around 4% and the dividend grows every quarter.

My morning presentation was one of three in what the MoneyShow calls a Master Class. There were three dividend investing experts speaking. One of the others very much likes a stock that has done very well for my newsletter subscribers.

The company is Arbor Realty Trust (ABR), a commercial finance REIT. This stock has had a great run over the last two years, and its nice to see another well respected analyst express a very positive opinion about the stock’s future. ABR yields 7.9% and has been growing the dividend.

Final note on Las Vegas hotels. I can’t stop turning the wrong way every time I come off the elevator. I know I do it so second guess my first choice and it still turns out to be opposite of the direction I wanted to go.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

The MoneyShow folks have now been asking to come back for five years. Each year it is a great time, and I love to get in front of the investing public.

As the spring show is held in Las Vegas, I thought it would be appropriate to cover some gaming related income stocks.

When it comes to the choice between being a tenant or a landlord, I like being on the landlord side, collecting a rent check every month.

At the end of the day (quarter and year) that is what being an investor in real estate investment trusts (REITs) means. Becoming a commercial property landlord through REIT ownership lets you become a first dollar investor in a wide range business types and industries.

The companies that lease from a REIT have a first dollar commitment to pay those rent checks. Yet often, a REIT will be able to participate in any positive business results produced by the tenant companies.

Gaming companies are a tough group of stocks to own. Profits swing wildly based on economic conditions and the tremendous competition in the areas that allow casino type gaming. Also, most of the gaming companies carry a large amount of debt. It costs a lot of money to build casinos!

It was the debt loads that pushed several publicly traded gaming companies to start to spin-off properties into REIT holding companies. The sponsored REITs gave the gaming companies a way to monetize assets and pay down debt. The gaming REITs are growth focused through the acquisition of additional properties to help support the growth of the sponsor gaming companies.

These three come to mind for your investment consideration.

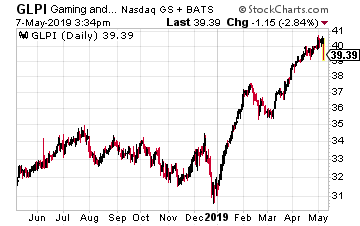

Gaming and Leisure Properties (GLPI) was the first gaming focused REIT when it was spun-out in 2013 by Penn National Gaming.

At that time the new REIT received 21 casino and racetrack properties. The company now owns 44 properties that are leased to and operated by Penn National Gaming, Casino Queen, Eldorado Resorts and Boyd Gaming.

In 2018 the company acquired five casinos from Tropicana Entertainment as the real estate part of the takeover of Tropicana by Eldorado Resorts. Of the three REITs here, GLPI is the most independent, with the ability to put together property and lease deals with a range of gaming companies. The REIT has an $8.7 billion market cap.

The dividend has grown by 5.6% per year over the past three years, and the GLPI shares yield 6.7%.

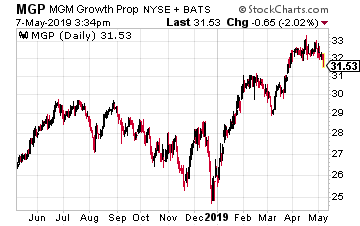

MGM Growth Properties LLC (MGP) was spun out in 2016 by MGM Resorts International. The initial REIT portfolio consisted of 10 MGM run properties, including seven on the Las Vegas strip. MGP now owns 14 properties all leased to MGM.

MGM Growth Properties has a triple-net master lease agreement with MGM Resorts which means all the REIT properties are on a single lease and the gaming company cannot single out one to close or not pay rent.

EBITDA from MGM coverage of the master lease payment is 6.2 times. The lease as a built in 1.8% rent escalator and MGP will also share profit growth at the casinos.

The MGP dividend has grown by 30% since the IPO and the shares yield 5.5%. MGP has a $9.2 billion market cap.

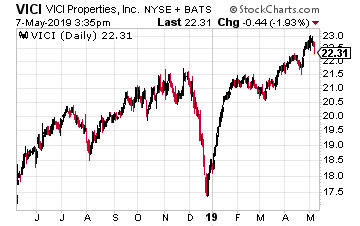

In October 2017 VICI Properties Inc. (VICI) was spun-off by Caesars Entertainment as part of the casino company’s bankruptcy reorganization.

Initially VICI owned 19 Caesars managed properties and that number has grown to 23. VICI has a triple-net master lease arrangement. The REIT has call options or right of first offering on six additional Caesar properties with another seven targeted for likely acquisition. VICI has a lot of growth potential.

VICI’s current market cap is $9.4 billion. Only four full quarter dividends have been paid.

There has been one dividend increase of 9.5%. Current yield is 5.0%.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

The need for an ever-increasing amount of data storage is a growth story that appears to have a very long runway. Experts estimate that the “digital universe” will double every two years (that’s a 50-fold increase in a decade).

Enterprise IT, cloud computing and services, the Internet of Things, and autonomous vehicles all require larger and larger amounts of data storage capacity. Data center owning real estate investment trusts (REITs) are a conservative way to play this trend, with potential for high teens, up to 20% annual total returns.

There is a small handful of REITs that specialize in developing and leasing data centers. All these companies are in growth mode and are either acquiring and/or developing new facilities to lease out to a wide range of customers.

The investing public often forgets that this REIT sector is an integral part of the technology industry. Often, they are treated like any other class of REIT. This dichotomy of market focus allows the attentive investor to pick up data center REIT shares on sale when the larger REIT sector goes into a decline.

Multi-year investment returns from the data center companies will be driven by cash flow and dividend growth rates.

Here are three REITs that can put high-teens annual compounding total returns into your portfolio.

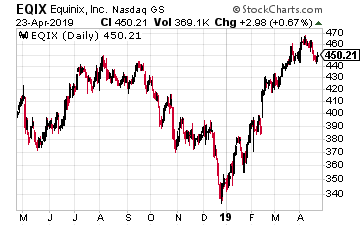

Equinix, Inc. (EQIX) is the $37 billion market cap, 800 lb. gorilla of the data center industry. The company converted from corporate tax payer to REIT status at the start of 2015. The company is a colocation and interconnection service provider.

Colocation is a data center facility in which a business can rent space for servers and other computing hardware. Typically, a colocation facility provides the building, cooling, power, bandwidth and physical security while the customer provides servers and storage.

The company’s services currently give 9,800 customers 333,000 interconnects between data centers and world’s digital exchanges. According to the current Investor Overview presentation, Equinix owns 200 data centers in 24 countries, on five continents. This is truly an international company.

Equinix has produced 64 consecutive quarters of revenue growth – the longest growth track record in the S&P500. This results in mid-teen per share cash flow growth.

For 2018 the company forecasts 8% to 11% FFO per share and dividend increases.

The shares currently yield 2.2%.

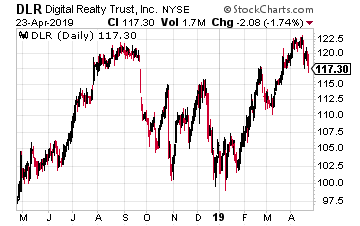

Digital Realty Trust, Inc. (DLR) is a $26 billion market cap REIT that owns 214 data centers in 13 countries. Digital Realty has 2,300 customers.

Like Equinix, Digital Realty is also a colocation and interconnection services provider. This REIT’s customer list includes some of the largest technology and telecommunications companies. In the top 10 are IBM, Facebook, Oracle, Verizon, LinkedIn, and even Equinix.

According to the current investor presentation, Digital Realty has increased its dividend per share for 14 straight years. Over that period cash flow to pay dividends has grown by a compounding 11.4% per year.

The DLR dividend has grown by 10% plus per year for the last 14 years.

The shares currently yield 4.0%.

CoreSite Realty Corp (COR) is a $4.0 billion market cap REIT that owns 22 data centers in eight strategic U.S. cities. The company’s focus is to provide colocation services to enterprise, network, and cloud services companies.

CoreSite is the high growth, higher risk company out of the three covered here. From 2011 through 2017, FFO per share grew by 23% compounded and the dividend by more than 30% per year.

Future results will cycle from relatively flat to high growth years. The company is currently in a flat growth stretch with management forecasting 4% FFO growth for 2019. That could easily increase back to historic levels with a few new data center investments.

An investment in COR will not be as stable as with the large cap data center REITs. The flip side is the potential for large dividend increases and corresponding share price gains.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.