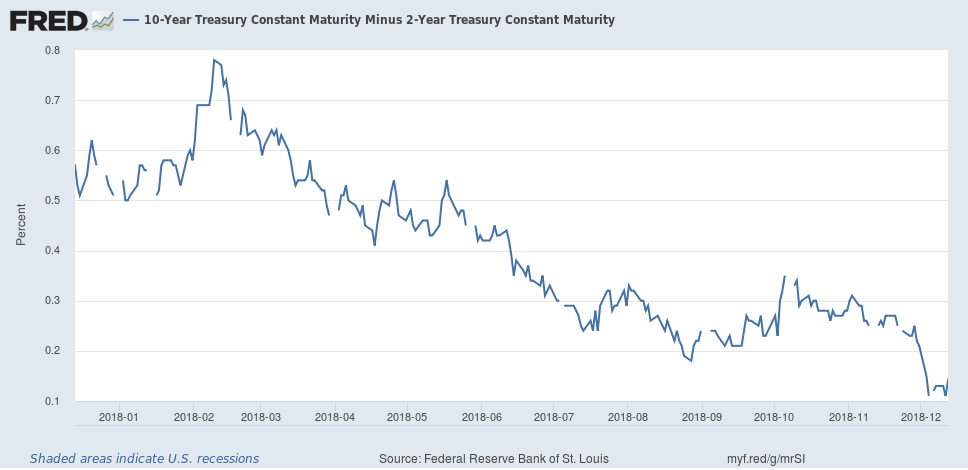

Last week the Federal Reserve Board announced the expected 0.25% increase in the Fed Funds interest rate. Despite doing the expected, the stock market swung from a 1.5% gain for the day to down as much as 2.5%. That’s an 800 point swing by the Dow Jones Industrial Average. Bloomberg noted “…no matter what the Federal Reserve and Chairman Jerome Powell did and said at the final monetary policy meeting of the year, they couldn’t make stock investors happy.”

It appears we have a battle between the stock market traders and investment firm heavyweights against the Fed. The Federal Reserve Board based their decision on forecasts the economy will grow in 2019 at 2% to 3%, inflation will stay below 2%, and employment will continue to improve.

Those who work in the financial industry use the fact that the stock market has gone down as “proof” that what the Fed sees for 2019 is wrong. The financial market pundits believe (or at least publicly say so) that there will be a recession because they believe in one, even though the usual signs a recession is coming are nowhere to be seen.

It seems that the stock market is going down because investors are selling. I am sure that computer trading programs are pushing prices down with short-selling strategies. As of December 20, its safe to say the stock market has fallen into bear market territory. However, it’s a bear without a reason to be one. It is possible that the negativity of the financial markets will spill over to Main Street, leading to an economic slowdown. However, there is not anything in the financial world that will lead to a crisis such as we experienced in 2000-2002 or 2007-2008. This bear market may go for a few months, but it won’t go deep.

Bear markets are not to be feared. They are the times when you get to “buy low”.

It’s a time when disciplined investors take advantage of fear in the markets that always is later shown to be over blown. Income focused investors get to buy in at very attractive yields and benefit from capital gains as the overall market recovers into the next bull market.

In these days of falling stock prices you want to find dividend paying stocks that are built for tougher economic times. Here are three to consider.

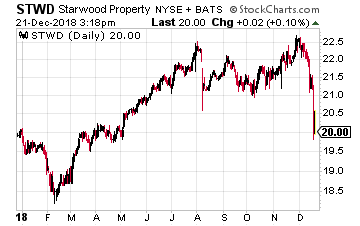

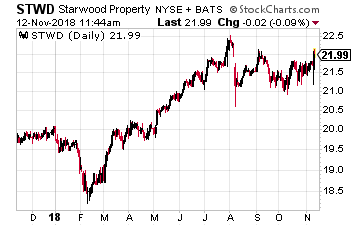

Starwood Property Trust (NYSE: STWD) is a commercial finance REIT. This means it originates mortgage loans for commercial properties, such as office buildings, hotels, and industrial buildings. Starwood has two commercial lending businesses. One is to make large dollar loans to retain in its portfolio.

Starwood Property Trust (NYSE: STWD) is a commercial finance REIT. This means it originates mortgage loans for commercial properties, such as office buildings, hotels, and industrial buildings. Starwood has two commercial lending businesses. One is to make large dollar loans to retain in its portfolio.

The company also operates a fee-based CMBS origination business. To further diversify the company as acquired a portfolio of stable returns real estate assets and has added an infrastructure lending arm.

The final piece of the pie is a special servicing division, which will turn very profitable if the commercial real estate sector experiences a downturn.

Investors can expect to earn the dividend, which currently gives the shares a 9.5% yield.

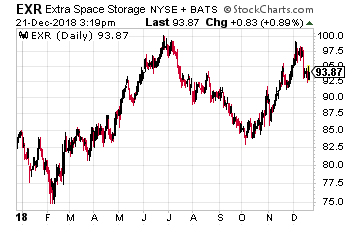

Self-storage REITs are the place to be when the economy gets rough for home ownership. Extra Space Storage (NYSE: EXR) is a large-cap, geographically diversified self-storage REIT.

Self-storage REITs are the place to be when the economy gets rough for home ownership. Extra Space Storage (NYSE: EXR) is a large-cap, geographically diversified self-storage REIT.

The self-storage business is counter-cyclical to the economy. When the economy is booming, developers bring a lot of new inventory into the market. When the economy slows, the inventory growth stops and demand increases.

Extra Space Storage is possibly the best managed REIT in the sector. Investors can expect high single digit annual dividend growth.

Current yield is 3.7%.

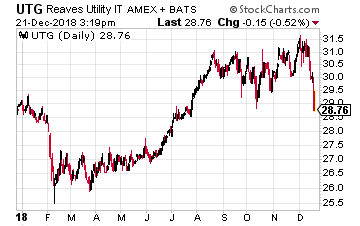

Utilities are supposed to be the safe sector when the stock market goes into a correction. This time utilities are down right along with the rest of the market sectors. Now is a great time to pick up shares of the Reaves Utility Income Fund NYSE: UTG).

Utilities are supposed to be the safe sector when the stock market goes into a correction. This time utilities are down right along with the rest of the market sectors. Now is a great time to pick up shares of the Reaves Utility Income Fund NYSE: UTG).

This is a closed-end fund that owns utility and other infrastructure stocks. UTG has paid a steady and growing monthly dividend since it launched in 2004.

The dividend has never been reduced and the fund has never paid return-of-capital dividends.

Current yield is 6.9%.

Pay Your Bills for LIFE with These Dividend StocksGet your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Click here for complete details to start your plan today.

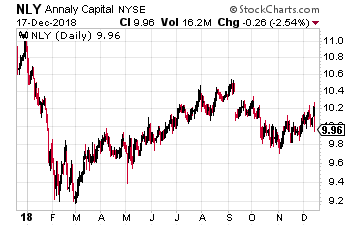

Annaly Capital Management, Inc. (NYSE: NLY) is a high-yield, agency MBS owning REIT. In its 2018 third quarter earnings report the company owned $91 billion worth of agency MBS.

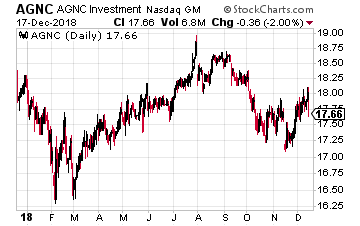

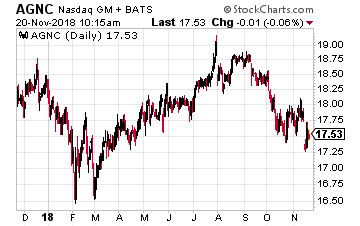

Annaly Capital Management, Inc. (NYSE: NLY) is a high-yield, agency MBS owning REIT. In its 2018 third quarter earnings report the company owned $91 billion worth of agency MBS. AGNC Investment Corp (Nasdaq: AGNC) is another agency MBS REIT. NLY and AGNC are the two largest companies in this REIT sector. As of the third quarter AGNC owned $70.9 billion of agency MBS.

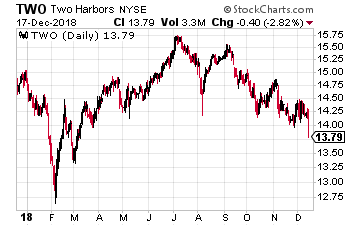

AGNC Investment Corp (Nasdaq: AGNC) is another agency MBS REIT. NLY and AGNC are the two largest companies in this REIT sector. As of the third quarter AGNC owned $70.9 billion of agency MBS. Two Harbors Investment Corp (NYSE: TWO) is a smaller agency MBS REIT that is trying to stay relevant with its recent merger with CYS Investments Inc (CYS).

Two Harbors Investment Corp (NYSE: TWO) is a smaller agency MBS REIT that is trying to stay relevant with its recent merger with CYS Investments Inc (CYS).

Uniti Group (Nasdaq: UNIT) is a telecommunications REIT focused on fiber optic assets. In recent years the company has focused on acquiring backhaul fiber assets. These are fiber connections between cell towers and the wired Internet.

Uniti Group (Nasdaq: UNIT) is a telecommunications REIT focused on fiber optic assets. In recent years the company has focused on acquiring backhaul fiber assets. These are fiber connections between cell towers and the wired Internet.

Main Street Capital (NYSE: MAIN) is a monthly dividend paying business development company (BDC). The company has also paid semi-annual, supplemental dividends since 2013. The next supplemental payout lands in investor brokerage accounts on December 27 and is equal to 150% of the normal monthly dividend.

Main Street Capital (NYSE: MAIN) is a monthly dividend paying business development company (BDC). The company has also paid semi-annual, supplemental dividends since 2013. The next supplemental payout lands in investor brokerage accounts on December 27 and is equal to 150% of the normal monthly dividend.

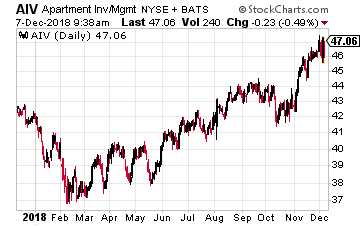

Apartment Investment and Management (NYSE: AIV) is a mid-cap sized REIT that owns and operates about 140 apartment communities.

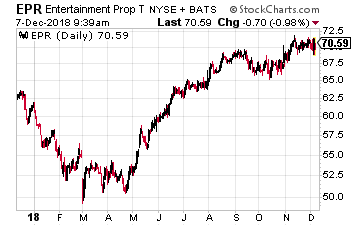

Apartment Investment and Management (NYSE: AIV) is a mid-cap sized REIT that owns and operates about 140 apartment communities. EPR Properties (NYSE: EPR) focuses its real estate investments in three different business sectors. Primary is the ownership and triple-net leasing of entertainment complexes and multiplex theaters. The second sector is the ownership of golf and ski recreation centers, also triple-net leased. The third sector is the construction, ownership and leasing of private and charter schools.

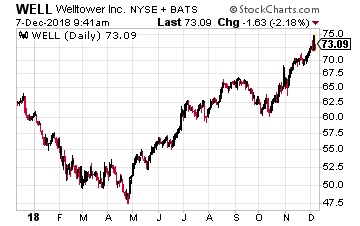

EPR Properties (NYSE: EPR) focuses its real estate investments in three different business sectors. Primary is the ownership and triple-net leasing of entertainment complexes and multiplex theaters. The second sector is the ownership of golf and ski recreation centers, also triple-net leased. The third sector is the construction, ownership and leasing of private and charter schools. Welltower Inc (NYSE: WELL) is a large cap healthcare sector REIT. The company owns properties concentrated in markets in the United States, Canada and the United Kingdom.

Welltower Inc (NYSE: WELL) is a large cap healthcare sector REIT. The company owns properties concentrated in markets in the United States, Canada and the United Kingdom.

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services.

Enterprise Products Partners LP (NYSE: EPD) with a $57 billion market cap is the largest midstream MLP. The company provides the full range of energy infrastructure services. Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines.

Magellan Midstream Partners LP (NYSE: MMP) primarily owns and operates refined products (gasoline, diesel fuel, jet fuel, etc.) pipelines and storage terminals. The company also owns 2,200 miles of interstate crude oil pipelines.

Preferred stock prices will rise in a recession if the Fed reduces interest rates, which it very likely will to stimulate the economy. You need to be aware preferred prices will decline in a rising rate environment. It’s tough to evaluate individual preferred stock issues, so I recommend using a dedicated fund like the iShares U.S. Preferred Stock ETF (NYSE: PFF).

Preferred stock prices will rise in a recession if the Fed reduces interest rates, which it very likely will to stimulate the economy. You need to be aware preferred prices will decline in a rising rate environment. It’s tough to evaluate individual preferred stock issues, so I recommend using a dedicated fund like the iShares U.S. Preferred Stock ETF (NYSE: PFF). Commodity exposure can be a great hedge against rising prices and inflation. Black Stone Minerals, L.P. (NYSE: BSM) is the largest pure-play oil and gas mineral and royalty owner in the United States. The company has rights to over 20 million mineral and royalty acres with interests in 41 states and 64 producing basins.

Commodity exposure can be a great hedge against rising prices and inflation. Black Stone Minerals, L.P. (NYSE: BSM) is the largest pure-play oil and gas mineral and royalty owner in the United States. The company has rights to over 20 million mineral and royalty acres with interests in 41 states and 64 producing basins.

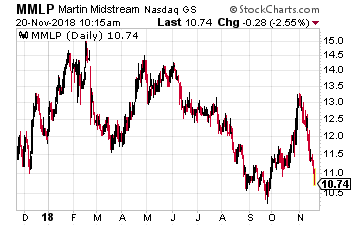

Martin Midstream Partners L.P. (Nasdaq: MMLP) is a high-yield master limited partnership. The shares currently yield over 17%. After a decade of dividend growth, the music stopped and in November 2016 the company slashed its payout by 38%.

Martin Midstream Partners L.P. (Nasdaq: MMLP) is a high-yield master limited partnership. The shares currently yield over 17%. After a decade of dividend growth, the music stopped and in November 2016 the company slashed its payout by 38%. AGNC Investment Corp (Nasdaq: AGNC) is the largest of a group of finance real estate investment trusts (REITs) that own portfolios of government agency backed mortgage backed securities, often called MBS. You will see these referred to as Freddie Mac, Fannie Mae and Ginnie May mortgage backed bonds.

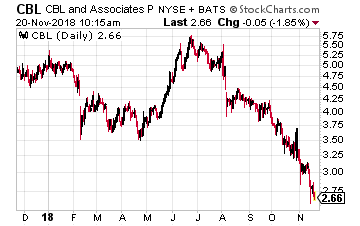

AGNC Investment Corp (Nasdaq: AGNC) is the largest of a group of finance real estate investment trusts (REITs) that own portfolios of government agency backed mortgage backed securities, often called MBS. You will see these referred to as Freddie Mac, Fannie Mae and Ginnie May mortgage backed bonds. CBL & Associates Properties, Inc. (NYSE: CBL) is a shopping mall REIT on the wrong side of the shopping center great divide. At one end are the successful REITs that own Class A malls which are 95% plus occupied with successful retailers. At the other end are the REITs that own malls with fading demographics anchored by declining retailers like Sears and JC Penny.

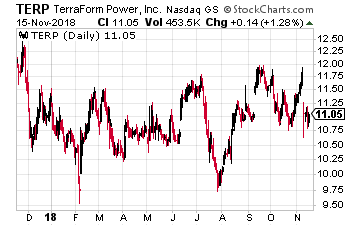

CBL & Associates Properties, Inc. (NYSE: CBL) is a shopping mall REIT on the wrong side of the shopping center great divide. At one end are the successful REITs that own Class A malls which are 95% plus occupied with successful retailers. At the other end are the REITs that own malls with fading demographics anchored by declining retailers like Sears and JC Penny. TerraForm Power (Nasdaq: TERP) is a $2.3 billion market cap which owns wind and solar power production assets. The company has gone through significant transformation over the last year. In October 2017 Brookfield Asset Management took over sponsorship of TERP and became a 51% shareholder in the Yieldco.

TerraForm Power (Nasdaq: TERP) is a $2.3 billion market cap which owns wind and solar power production assets. The company has gone through significant transformation over the last year. In October 2017 Brookfield Asset Management took over sponsorship of TERP and became a 51% shareholder in the Yieldco. Brookfield Renewable Partners (NYSE: BEP) was operating like a Yieldco long before the term was invented. The company owns 260 hydro power plants, which account for 76% of production. 35% of production is done outside of North America. Also, 90% of power production is purchased on long-term contracts.

Brookfield Renewable Partners (NYSE: BEP) was operating like a Yieldco long before the term was invented. The company owns 260 hydro power plants, which account for 76% of production. 35% of production is done outside of North America. Also, 90% of power production is purchased on long-term contracts. Clearway Energy (NYSE: CWEN) is another Yieldco that recently went through a change of sponsorship. Clearway was started by utility company NRG Energy (NYSE: NRG).

Clearway Energy (NYSE: CWEN) is another Yieldco that recently went through a change of sponsorship. Clearway was started by utility company NRG Energy (NYSE: NRG).

The finance REIT side of the REIT universe typically carries much higher dividend yields, which are very attractive to income-focused investors. For comparison, REM currently yields 10% while the largest equity REIT ETF, the Vanguard REIT Index Fund (NYSE: VNQ), yields 4.8%.

The finance REIT side of the REIT universe typically carries much higher dividend yields, which are very attractive to income-focused investors. For comparison, REM currently yields 10% while the largest equity REIT ETF, the Vanguard REIT Index Fund (NYSE: VNQ), yields 4.8%. For example, consider the case of one of the larger and more popular agency MBS REITs, American Capital Agency Corp. (NASDAQ: AGNC), which yields an attractive 12%. Digging deeper shows the current dividend rate at just 43% the size of the dividend AGNC investors were earning in 2012. Put another way, the AGNC dividend has been cut by more than half over the last 6 years. With the Treasury yield curve continuing to flatten, I would not be surprised by another dividend cut soon.

For example, consider the case of one of the larger and more popular agency MBS REITs, American Capital Agency Corp. (NASDAQ: AGNC), which yields an attractive 12%. Digging deeper shows the current dividend rate at just 43% the size of the dividend AGNC investors were earning in 2012. Put another way, the AGNC dividend has been cut by more than half over the last 6 years. With the Treasury yield curve continuing to flatten, I would not be surprised by another dividend cut soon. Starwood Property Trust, Inc. (NYSE: STWD) is a commercial mortgage lender. Starwood has a diverse business which includes a portfolio of commercial mortgages, an energy infrastructure loan business and holdings, a commercial mortgage servicing company and some commercial property investments.

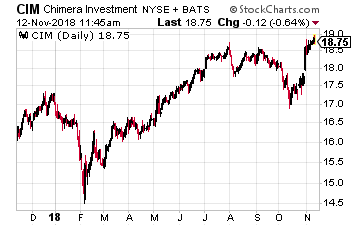

Starwood Property Trust, Inc. (NYSE: STWD) is a commercial mortgage lender. Starwood has a diverse business which includes a portfolio of commercial mortgages, an energy infrastructure loan business and holdings, a commercial mortgage servicing company and some commercial property investments. Chimera Investment Corporation (NYSE: CIM) aims to provide attractive risk-adjusted returns by investing in a diversified investment portfolio of residential mortgage securities, residential mortgage loans, real estate-related securities and various other asset classes.

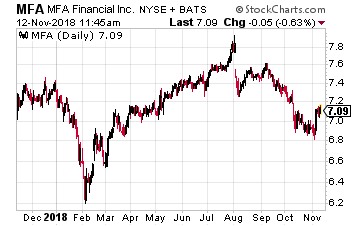

Chimera Investment Corporation (NYSE: CIM) aims to provide attractive risk-adjusted returns by investing in a diversified investment portfolio of residential mortgage securities, residential mortgage loans, real estate-related securities and various other asset classes. MFA Financial, Inc. (NYSE: MFA) owns a diversified portfolio of mortgage securities. This is the most traditional agency MBS owning REIT on this list. However, it has avoided the rising interest rate challenges that has resulted in deep dividend cuts from its peer REITs.

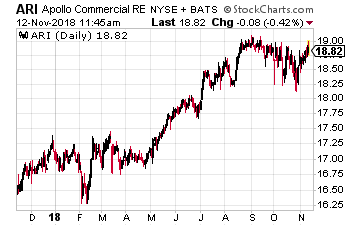

MFA Financial, Inc. (NYSE: MFA) owns a diversified portfolio of mortgage securities. This is the most traditional agency MBS owning REIT on this list. However, it has avoided the rising interest rate challenges that has resulted in deep dividend cuts from its peer REITs. Apollo Commercial Real Est. Finance Inc. (NYSE: ARI) is a real estate investment trust that primarily originates and invests in senior mortgages and mezzanine loans collateralized by commercial real estate throughout the United States and Europe.

Apollo Commercial Real Est. Finance Inc. (NYSE: ARI) is a real estate investment trust that primarily originates and invests in senior mortgages and mezzanine loans collateralized by commercial real estate throughout the United States and Europe. Blackstone Mortgage Trust (NYSE: BXMT) is a pure play originator of commercial real estate mortgages. The company focuses on larger loans, where competition for the business is less fierce.

Blackstone Mortgage Trust (NYSE: BXMT) is a pure play originator of commercial real estate mortgages. The company focuses on larger loans, where competition for the business is less fierce.