In my focus area of high yield stocks, I am regularly reminded how committed to losing money are many high-yield stock investors. Any whiff of bad news has them running for the exits, which drives down share price, which causes more fear based selling, which further drives down the share price. You get the picture. Investors who buy high yield stocks are often new to owning stocks, or less well informed on how stock prices fluctuate. To avoid being a money-losing, fear-based seller of dividend stocks, an investor needs to understand the difference between real and fake news that moves stock prices.

Real news about publicly traded companies is primarily quarterly earnings results and the associated management comments about business operations. Press releases directly from the individual companies count as real news. You may notice that these items come out just once to a few times per calendar quarter for most stocks. This is the information on which buy and sell decisions should be made.

Related: Separating Real News from Fake News in the Stock Market

However, the financial news media is hungry for items to fill websites and financial news networks’ broadcast time. The information from these news outlets come from Wall Street analysts and financial writers who share their opinions and try to predict the future. They have no deeper insight that what an investor can get from the information released directly by the companies.

Predicting future results are really just estimates or guesses. I refer to these forecasts as “fake news” because they do not add any real information to my knowledge about individual companies. When a “fake news” item results in a steep share price drop, I review the real news I know about a company and often recommend using the price decline as a buying opportunity. Here are two stocks that recently were affected this way.

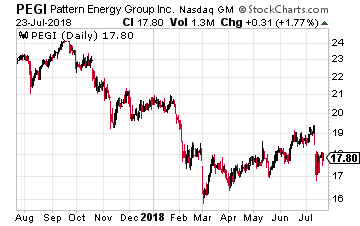

Pattern Energy Group (Nasdaq: PEGI) recently experienced a 12.5% decline when the province of Ontario announced it was cancelling over 750 renewable energy contracts. While Pattern Energy was not singled out, the company has a significant presence with several projects under development in Ontario.

Pattern Energy Group (Nasdaq: PEGI) recently experienced a 12.5% decline when the province of Ontario announced it was cancelling over 750 renewable energy contracts. While Pattern Energy was not singled out, the company has a significant presence with several projects under development in Ontario.

A few days after the big drop, a follow up report noted that none of Pattern Energy’s projects would be affected. However, even though the original cause of the decline has been proven to not affect the company, less than half of the steep drop has been recaptured.

This makes PEGI an attractive purchase now with its stable and growing dividend and 9.6% yield.

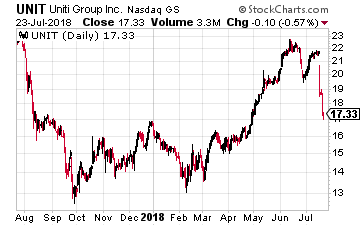

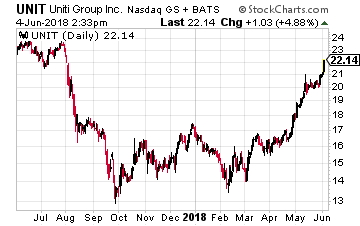

Over the course of just one week, the share price of Uniti Group (Nasdaq: UNIT) declined by 20%. The drop was almost entirely due to a Wall Street analyst putting a sell recommendation on the stock with a $15 price target.

Over the course of just one week, the share price of Uniti Group (Nasdaq: UNIT) declined by 20%. The drop was almost entirely due to a Wall Street analyst putting a sell recommendation on the stock with a $15 price target.

The real facts are that UNIT at $17.40 per share is the same company with the same prospects as it was when the share price was $4 higher. The big dividend is not at risk, and this is a company that is growing and diversifying its business operations. UNIT now yields almost 14%. It is likely that the Q2 earnings release in early August will give a boost to the share price.

Federal Realty Investment Trust (NYSE: FRT) is a $9 billion market cap REIT that owns, operates, and redevelops high quality retail real estate in the country’s best markets. FRT has increased its dividend for 50 consecutive years, the longest growth streak of any REIT.

Federal Realty Investment Trust (NYSE: FRT) is a $9 billion market cap REIT that owns, operates, and redevelops high quality retail real estate in the country’s best markets. FRT has increased its dividend for 50 consecutive years, the longest growth streak of any REIT. Eastgroup Properties Inc (NYSE: EGP) is a $3.3 billion market value REIT that focuses on development, acquisition and operation of industrial properties in major Sunbelt markets throughout the United States with an emphasis on the states of Florida, Texas, Arizona, California and North Carolina. Industrial properties is currently one of the best performing real estate sectors.

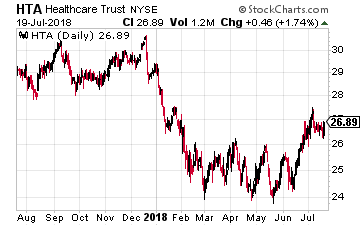

Eastgroup Properties Inc (NYSE: EGP) is a $3.3 billion market value REIT that focuses on development, acquisition and operation of industrial properties in major Sunbelt markets throughout the United States with an emphasis on the states of Florida, Texas, Arizona, California and North Carolina. Industrial properties is currently one of the best performing real estate sectors. Healthcare Trust of America, Inc. (NYSE: HTA) is a $5.4 billion REIT that acquires, owns and operates medical office buildings. The company reduced its dividend in 2012 and 2013, which was followed by small increases in each of the next four years. Last year the dividend was bumped up by 1.7% which is comparable to the increase of the previous year.

Healthcare Trust of America, Inc. (NYSE: HTA) is a $5.4 billion REIT that acquires, owns and operates medical office buildings. The company reduced its dividend in 2012 and 2013, which was followed by small increases in each of the next four years. Last year the dividend was bumped up by 1.7% which is comparable to the increase of the previous year.

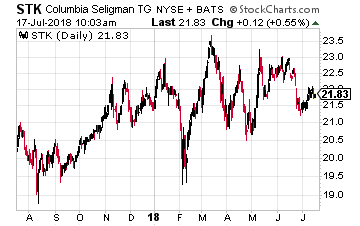

Columbia Seligman Premium Technology Growth Fund (NYSE: STK) seeks capital appreciation through investments in a portfolio of technology related equity securities and current income by employing an option writing strategy.

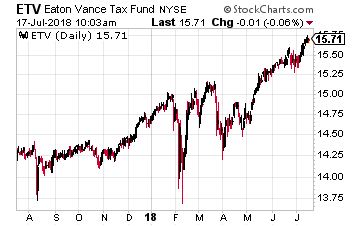

Columbia Seligman Premium Technology Growth Fund (NYSE: STK) seeks capital appreciation through investments in a portfolio of technology related equity securities and current income by employing an option writing strategy. Eaton Vance Tax-Managed Buy-Write Opportunities Fund (NYSE: ETV) invests in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a substantial portion of the value of its common stock portfolio to generate current earnings from the option premium. Buy-Write is another name for covered call writing. Also, as the fund name states, the managers strive to generate the best after tax returns. The fund uses the S&P 500 stock index as its benchmark evaluate returns.

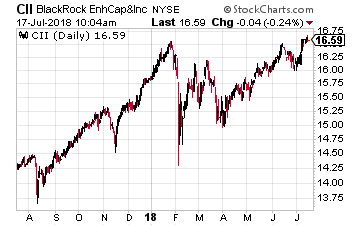

Eaton Vance Tax-Managed Buy-Write Opportunities Fund (NYSE: ETV) invests in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a substantial portion of the value of its common stock portfolio to generate current earnings from the option premium. Buy-Write is another name for covered call writing. Also, as the fund name states, the managers strive to generate the best after tax returns. The fund uses the S&P 500 stock index as its benchmark evaluate returns. BlackRock Enhanced Capital & Income Fund (NYSE: CII) seeks to achieve its investment objective by investing in a portfolio of equity securities of U.S. and foreign issuers. The fund also employs a strategy of selling call and put options.

BlackRock Enhanced Capital & Income Fund (NYSE: CII) seeks to achieve its investment objective by investing in a portfolio of equity securities of U.S. and foreign issuers. The fund also employs a strategy of selling call and put options.

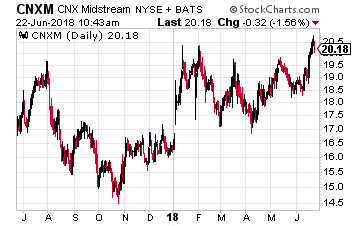

CNX Midstream Partners LP (NYSE: CNXM) is up 23.7% so far this year. CNXM is an MLP that owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. The company operates in the Marcellus and Utica shales, the most prolific natural gas play in the U.S., if not the world. This MLP primarily provides services to CNX Resources Corporation (NYSE: CNX), which has a significant portfolio of midstream assets to be transferred to the MLP. CNXM has provided distribution growth guidance of 15% per year through at least 2022. The CNXM units currently yield 6.7.

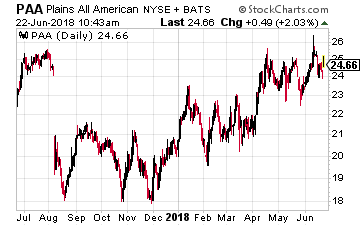

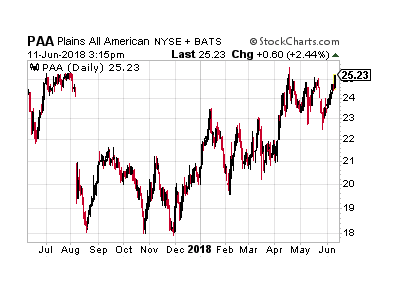

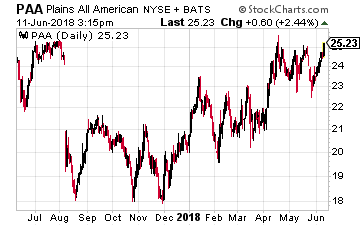

CNX Midstream Partners LP (NYSE: CNXM) is up 23.7% so far this year. CNXM is an MLP that owns, operates, develops and acquires gathering and other midstream energy assets to service natural gas production in the Appalachian Basin in Pennsylvania and West Virginia. The company operates in the Marcellus and Utica shales, the most prolific natural gas play in the U.S., if not the world. This MLP primarily provides services to CNX Resources Corporation (NYSE: CNX), which has a significant portfolio of midstream assets to be transferred to the MLP. CNXM has provided distribution growth guidance of 15% per year through at least 2022. The CNXM units currently yield 6.7. Plains All American Pipeline LP (NYSE: PAA) is up 20.5% year to date. Plains owns and operates the largest independent network of crude oil gather systems, crude oil long distance pipelines, and crude oil storage facilities. The company has the largest gathering presence in the rich Permian energy play. It has one of the best pipeline takeaway capacities and is leading the charge to build new pipelines out of the Permian. This region is the growth engine of U.S. oil production and Plains All American Pipelines is best positioned to benefit from the production growth. The company offers alternative shares in Plains GP Holdings LP (NYSE: PAGP). Both securities pay the same distribution rates (each PAGP share is backed by a PAA unit. The difference is that PAGP is a 1099 reporting company for taxes. Plains should resume distribution growth in 2019. The shares currently yield 5.0%.

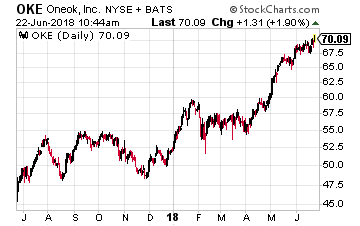

Plains All American Pipeline LP (NYSE: PAA) is up 20.5% year to date. Plains owns and operates the largest independent network of crude oil gather systems, crude oil long distance pipelines, and crude oil storage facilities. The company has the largest gathering presence in the rich Permian energy play. It has one of the best pipeline takeaway capacities and is leading the charge to build new pipelines out of the Permian. This region is the growth engine of U.S. oil production and Plains All American Pipelines is best positioned to benefit from the production growth. The company offers alternative shares in Plains GP Holdings LP (NYSE: PAGP). Both securities pay the same distribution rates (each PAGP share is backed by a PAA unit. The difference is that PAGP is a 1099 reporting company for taxes. Plains should resume distribution growth in 2019. The shares currently yield 5.0%. ONEOK, Inc. (NYSE: OKE) is up 29.8% so far in 2018. ONEOK (pronounced one-oak) is one of the largest energy midstream service providers in the U.S., connecting prolific supply basins with key market centers. It owns and operates one of the nation’s premier natural gas liquids (NGL) systems and is a leader in the gathering, processing, storage and transportation of natural gas. ONEOK’s operations include a 38,000-mile integrated network of NGL and natural gas pipelines, processing plants, fractionators and storage facilities in the Mid-Continent, Williston, Permian and Rocky Mountain regions. In mid-2017 the company merged its controlled MLP into the corporate parent. The share price gains show that the market likes this energy midstream company as a corporation. The OKE dividends increase every quarter and are forecast to grow by 10% per year. The shares currently yield 4.6%.

ONEOK, Inc. (NYSE: OKE) is up 29.8% so far in 2018. ONEOK (pronounced one-oak) is one of the largest energy midstream service providers in the U.S., connecting prolific supply basins with key market centers. It owns and operates one of the nation’s premier natural gas liquids (NGL) systems and is a leader in the gathering, processing, storage and transportation of natural gas. ONEOK’s operations include a 38,000-mile integrated network of NGL and natural gas pipelines, processing plants, fractionators and storage facilities in the Mid-Continent, Williston, Permian and Rocky Mountain regions. In mid-2017 the company merged its controlled MLP into the corporate parent. The share price gains show that the market likes this energy midstream company as a corporation. The OKE dividends increase every quarter and are forecast to grow by 10% per year. The shares currently yield 4.6%.

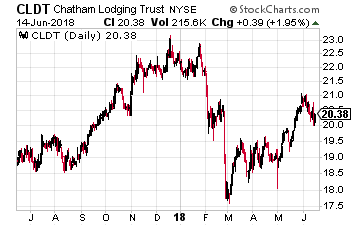

Chatham Lodging Trust (NYSE: CLDT) is a lodging/hotel REIT which owns 40 hotels in 15 states. The portfolio consists of premium branded upscale extended stay and select service hotels. The hotel REIT sector peaked in January 2015 and then went into a steep bear market which bottomed one year later. Over the last two and a half years, share prices have been volatile without a definite up or down trend.

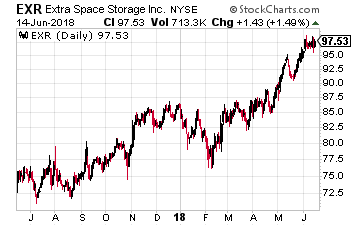

Chatham Lodging Trust (NYSE: CLDT) is a lodging/hotel REIT which owns 40 hotels in 15 states. The portfolio consists of premium branded upscale extended stay and select service hotels. The hotel REIT sector peaked in January 2015 and then went into a steep bear market which bottomed one year later. Over the last two and a half years, share prices have been volatile without a definite up or down trend. Extra Space Storage (NYSE: EXR) is a large-cap, self-storage REIT with a best in class track record. The company owns 851 storage facilities. It has interests in another 216 through joint ventures and provides the management services for an additional 456 properties. The self-storage business provides strong same store revenue growth with low expenses and capital spending requirements.

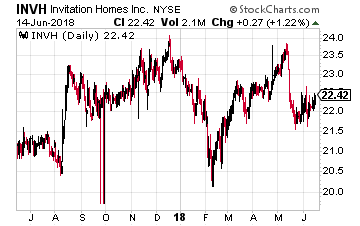

Extra Space Storage (NYSE: EXR) is a large-cap, self-storage REIT with a best in class track record. The company owns 851 storage facilities. It has interests in another 216 through joint ventures and provides the management services for an additional 456 properties. The self-storage business provides strong same store revenue growth with low expenses and capital spending requirements. Invitation Homes (NYSE: INVH) is one of the small number of REITs focused on owning single-family rental homes as opposed to apartment complexes. These REITs are the result of the institutional buying of distressed homes during the housing make crash of 2009-2011.Thousands of homes were bought at low prices, rehabilitated and turned into rental properties.

Invitation Homes (NYSE: INVH) is one of the small number of REITs focused on owning single-family rental homes as opposed to apartment complexes. These REITs are the result of the institutional buying of distressed homes during the housing make crash of 2009-2011.Thousands of homes were bought at low prices, rehabilitated and turned into rental properties.

Plains All American Pipeline LP (NYSE: PAA) is a $30 billion enterprise value MLP focused on crude oil pipelines and terminals. Plains has focused on the Permian and is investing $1.6 billion in growth capital to expand its crude oil gathering and pipeline takeaway capacity in the Basin.

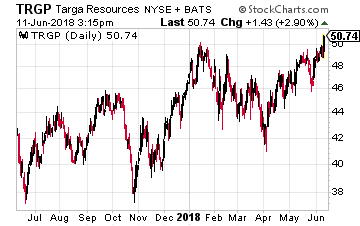

Plains All American Pipeline LP (NYSE: PAA) is a $30 billion enterprise value MLP focused on crude oil pipelines and terminals. Plains has focused on the Permian and is investing $1.6 billion in growth capital to expand its crude oil gathering and pipeline takeaway capacity in the Basin. Targa Resources Corp (NYSE: TRGP) is an $11 billion market cap energy midstream company focused on the gathering, processing, transport and export of natural gas liquids (NGLs). These energy liquids are a big part of the value process of energy production in the Permian, North Texas and Oklahoma.

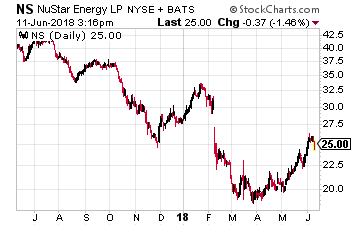

Targa Resources Corp (NYSE: TRGP) is an $11 billion market cap energy midstream company focused on the gathering, processing, transport and export of natural gas liquids (NGLs). These energy liquids are a big part of the value process of energy production in the Permian, North Texas and Oklahoma. NuStar Energy LP (NYSE: NS) is an MLP whose business operations are a balance of pipelines and storage facilities for both crude oil and refined energy projects. In May 2017 the company acquired an integrated crude oil and transport system in the heart of the Permian Basin.

NuStar Energy LP (NYSE: NS) is an MLP whose business operations are a balance of pipelines and storage facilities for both crude oil and refined energy projects. In May 2017 the company acquired an integrated crude oil and transport system in the heart of the Permian Basin.

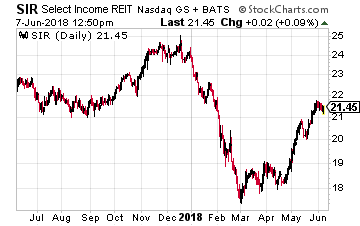

Select Income REIT (Nasdaq: SIR) owns 100 buildings, containing 17 million square feet that are 88.7% leased. In January the company spun off its 266 industrial properties into a new REIT, Industrial Logistics Properties Trust (NYSE: ILPT). SIR retained 69% ownership in the new REIT and consolidates the industrial company results to its income statement. Revenue growth is generated by built in rent escalators and the development of raw land industrial properties at ILPT.

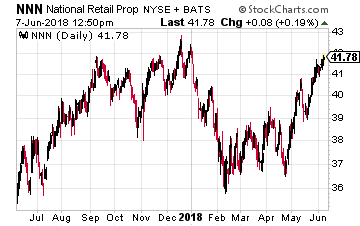

Select Income REIT (Nasdaq: SIR) owns 100 buildings, containing 17 million square feet that are 88.7% leased. In January the company spun off its 266 industrial properties into a new REIT, Industrial Logistics Properties Trust (NYSE: ILPT). SIR retained 69% ownership in the new REIT and consolidates the industrial company results to its income statement. Revenue growth is generated by built in rent escalators and the development of raw land industrial properties at ILPT. National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. The top types of businesses are convenience stores, casual and fast food restaurants, auto service shops, fitness outlets, movie theaters and auto parts stores. When acquiring new properties NNN focuses on buying stores with great locations over high quality tenants. The good locations mean that the tenants will be successful and be able to pay the rents. Also, if a tenant does leave, it will be easier to re-lease a property in a great location.

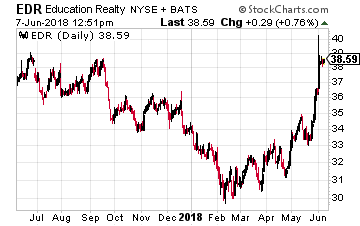

National Retail Properties, Inc. (NYSE: NNN) is a traditional triple-net lease REIT. The company owns over 2,800 (up by 300 in the last year) free-standing, single tenant retail properties. most of the REIT’s tenants are in business that cannot be hurt or replaced by online sellers. The top types of businesses are convenience stores, casual and fast food restaurants, auto service shops, fitness outlets, movie theaters and auto parts stores. When acquiring new properties NNN focuses on buying stores with great locations over high quality tenants. The good locations mean that the tenants will be successful and be able to pay the rents. Also, if a tenant does leave, it will be easier to re-lease a property in a great location. EdR, Inc. (NYSE: EDR) develops, acquires, owns and manages collegiate housing communities located near university campuses. Currently the company owns 79 (up 13 in the last year) communities in 50 different university communities. These communities are located 1/10th to 1/3rd of a mile from the campuses. The college housing business model has produced stable revenue growth, averaging 3.7% per year same store gains. Development and acquisitions boost that core growth rate.

EdR, Inc. (NYSE: EDR) develops, acquires, owns and manages collegiate housing communities located near university campuses. Currently the company owns 79 (up 13 in the last year) communities in 50 different university communities. These communities are located 1/10th to 1/3rd of a mile from the campuses. The college housing business model has produced stable revenue growth, averaging 3.7% per year same store gains. Development and acquisitions boost that core growth rate.

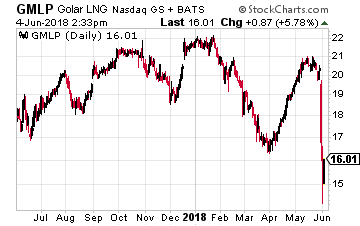

On May 31, Golar LNG Partners LP (Nasdaq: GMLP) reported the company’s 2018 first quarter results. Cash flow for the quarter was just 32% of the dividend rate. Management noted that the Board of Directors would review future dividend payments. The GMLP share price dropped by 29% over the next two trading days. Many investors who contacted me were convinced that a dividend cut was imminent. After reviewing the earnings report, management comments and any other facts I could find, my analysis is that the current GMLP situation is similar to what occurred with Uniti Group (Nasdaq: UNIT) in July and August 2017.

On May 31, Golar LNG Partners LP (Nasdaq: GMLP) reported the company’s 2018 first quarter results. Cash flow for the quarter was just 32% of the dividend rate. Management noted that the Board of Directors would review future dividend payments. The GMLP share price dropped by 29% over the next two trading days. Many investors who contacted me were convinced that a dividend cut was imminent. After reviewing the earnings report, management comments and any other facts I could find, my analysis is that the current GMLP situation is similar to what occurred with Uniti Group (Nasdaq: UNIT) in July and August 2017. Last year the UNIT share price crashed from over $26 to a low of $13.81. The near 50% decline was due to the belief that UNIT’s primary customer

Last year the UNIT share price crashed from over $26 to a low of $13.81. The near 50% decline was due to the belief that UNIT’s primary customer

PowerShares S&P 500 BuyWrite ETF (NYSE: PBP) is the largest buy-write ETF by assets under management. As an ETF, the fund tracks a specific index, in this case the CBOE S&P 500 BuyWrite Index.

PowerShares S&P 500 BuyWrite ETF (NYSE: PBP) is the largest buy-write ETF by assets under management. As an ETF, the fund tracks a specific index, in this case the CBOE S&P 500 BuyWrite Index. Nuveen S&P 500 Buy-Write Income Fund (NYSE: BXMX) is a closed-end fund that seeks to substantially replicate the price movements of the S&P 500 Index and by selling index call options covering approximately 100% of the Fund’s equity portfolio value with a goal of enhancing the portfolio’s risk-adjusted returns.

Nuveen S&P 500 Buy-Write Income Fund (NYSE: BXMX) is a closed-end fund that seeks to substantially replicate the price movements of the S&P 500 Index and by selling index call options covering approximately 100% of the Fund’s equity portfolio value with a goal of enhancing the portfolio’s risk-adjusted returns. Horizons NASDAQ 100 Covered Call ETF (Nasdaq: QYLD) is an ETF that tracks the CBOE NASDAQ-100® BuyWrite Index. As a result, this ETF will be more focused on the large technology stocks that make up a large part of the Nasdaq 100 stock index.

Horizons NASDAQ 100 Covered Call ETF (Nasdaq: QYLD) is an ETF that tracks the CBOE NASDAQ-100® BuyWrite Index. As a result, this ETF will be more focused on the large technology stocks that make up a large part of the Nasdaq 100 stock index. Nuveen Nasdaq 100 Dynamic Overwrite Fund (Nasdaq: QQQX) is a closed-end fund using the Nasdaq 100 Stock Index as its basis for covered call writing.

Nuveen Nasdaq 100 Dynamic Overwrite Fund (Nasdaq: QQQX) is a closed-end fund using the Nasdaq 100 Stock Index as its basis for covered call writing. First Trust Enhanced Equity Income Fund (NYSE: FFA) is a closed-end fund where the managers actively manage the stock portfolio and enhance income by selling call options.

First Trust Enhanced Equity Income Fund (NYSE: FFA) is a closed-end fund where the managers actively manage the stock portfolio and enhance income by selling call options.