There’s been a massive discount building in a pocket of the market where you can get big dividends that are entirely tax-free.

And I’m going to show you three “1-click” ways to tap this income investor’s wonderland today.

I know that tax-free anything these days sounds impossible, but in this case, I assure you it’s not. The key is investing in municipal bonds, which give you a passive income stream that is entirely tax exempt at the federal level. Plus it’s also exempt from state taxes in many situations, too.

That means a 4%-yielding municipal bond, or “muni,” is more like a 5.3%-yielding dividend stock for a family earning $100,000 per year—and that’s before we factor in state taxes.

Plus, there are some funds out there that hold munis that can get you much more than 4%. Below I’ll show you 3 of them with “regular” yields as high as 5.8%. First, let me tell you why now is the perfect time to buy them.

How to Amplify Your Muni Gains (and Dividends)

To get the biggest bang for your buck in munis, buy them through closed-end funds (CEFs). There are nearly 200 muni-bond CEFs out there, and most of them yield over 4%. And since they’re CEFs, several are priced far below their “true” value.

How can you tell?

Because the average municipal-bond CEF’s market price is 8.6% below its net asset value (NAV, or the market value of all the holdings in its portfolio).

That discount to NAV is a key number to watch in any CEF, and with a wide 8.6% average markdown, it’s easy to snap up a great muni-bond CEF cheap, then set yourself up for some nice price upside as that gap narrows to its traditional level.

Muni CEF Pick #1: A 4.9% Yield at a Massive Discount

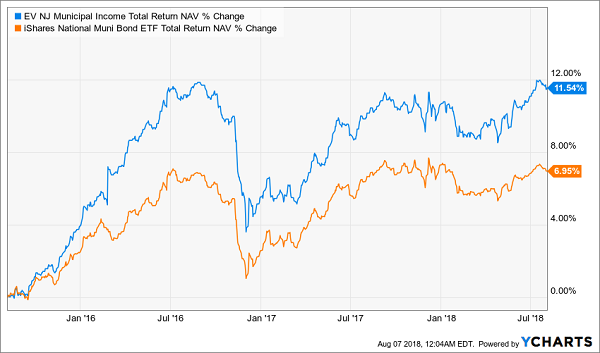

A good example of a great marked-down fund is the Eaton Vance New Jersey Municipal Income Fund (EVJ), which pays a 4.9% dividend and currently trades at a massive 12.3% discount to NAV.

EVJ is no slouch in the performance department, either. On a NAV basis, the fund has earned an 11.5% return over the last 3 years, which is nearly double the gain posted by the muni-bond index fund, the iShares National Muni Bond ETF (MUB).

EVJ Demolishes the Benchmark

On top of that outperformance, EVJ’s yield is about twice that of MUB, making it both a market outperformer and a big yielder.

But should you worry that the fund focuses on just one state? In a word, no.

New Jersey’s average income is $62,554 per capita, the third highest in the union. And while the state’s GDP grew more slowly than that of America as a whole in 2017 (0.9% versus 2.1%), New Jersey is the eighth-wealthiest state in America, which means its growth rate will tend to be lower than those of poorer states.

That wealth has also resulted in fast-growing investment in infrastructure (this spending is budgeted to rise 172% in the next year), which tends to boost economic growth.

But here’s the real key: New Jersey revenues are set to rise 5.7% in 2019 after gaining in 2018. That 2019 estimate is far higher than the 4.2% growth in the state’s spending, so the bottom line here is that New Jersey’s fiscal health is getting better. And that makes EVJ worth considering for income and growth now.

Muni CEF Pick #2: Unbeatable Safety and 4.1% in Tax-Free Cash

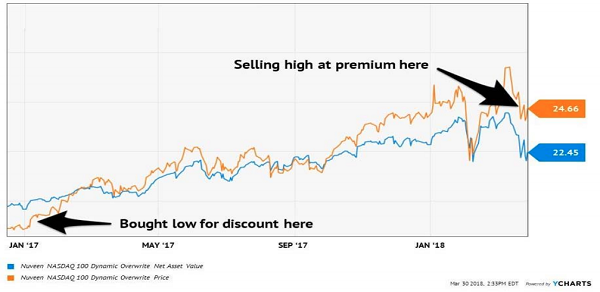

Nonetheless, if you do want to go beyond a fund that focuses on just one state, you’d be smart to snap up the BlackRock Municipal Intermediate Duration Fund (MUI), one of the best-performing muni CEFs over the last decade. Just look at how it’s done compared to MUB:

MUI Quietly Delivers Big Profits

This outperformance isn’t rewarded with a premium price; MUI trades at a 13% discount to NAV, which is double its 6.5% average markdown over the last decade. That also means the fund’s 4.1% dividend yield is extremely sustainable, since MUI’s management only needs to get a 3.6% income stream in the muni-bond markets to keep the payouts coming.

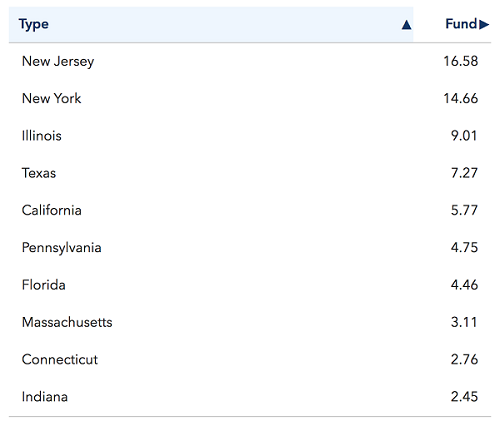

Then there’s the diversification. Here’s a chart from BlackRock breaking down the fund’s exposure by state—you can see that it focuses on the biggest states with the healthiest budgets:

A Diverse Fund

Plus, MUI is exposed to the northeast, southwest and every area in between—the fund actually holds municipal bonds from 44 states in total!

If you’re looking for a sleep-well-at-night, high-yielding, tax-free income stream, MUI is a great option.

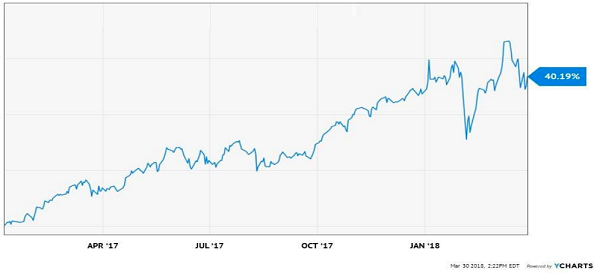

Muni CEF Pick #3: Crushing the Index for Over 2 Decades

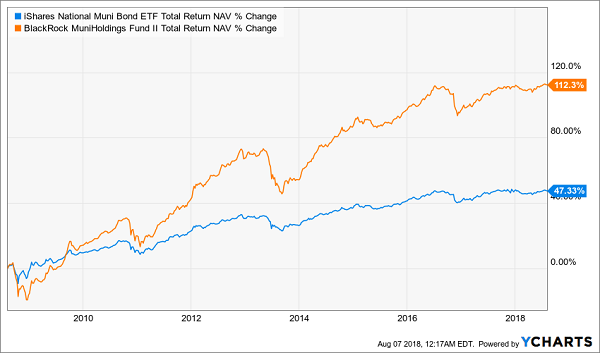

The last fund I want to show you is another BlackRock fund, the BlackRock MuniHoldings Fund II (MUH), which is one of the best-performing muni CEFs of all time. Over the last decade, it’s returned 7.5% annualized. Just look at what it’s done compared to MUB!

Another Long-Term Winner

What’s the secret to this fund’s success?

Two things. First, it invests in municipal bonds that are income tax free but not alternative minimum tax (AMT) free. That limits the appeal of these bonds to some investors, making the market for them less efficient. That, in turn, lets the geniuses at BlackRock easily spot bargains that will boost your returns (as management has for the last decade).

Another big reason for MUH’s healthy gains is the fund’s use of derivatives. By using a mixture of futures, options and interest-rate swaps, MUH can boost your total return by actively playing the bond market as it relates to the Federal Reserve’s changing monetary policy. This approach has worked well over the fund’s history, going back to the 1990s.

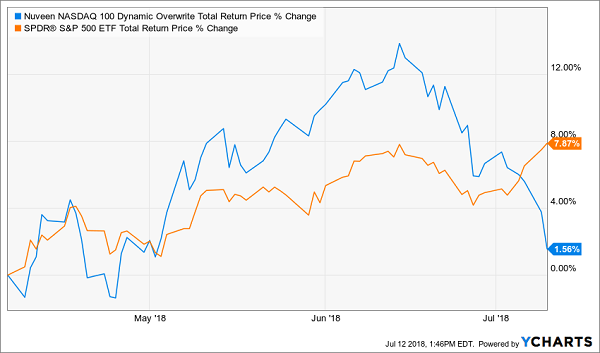

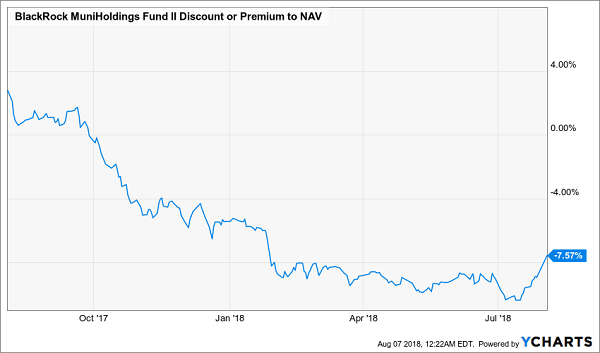

Finally, MUH trades at a 7.6% discount to NAV, far higher than the 3.4% markdown it’s averaged over the last decade. That discount has gotten unusually big in the last year—but it’s also starting to recover:

Sale Ending Soon

That makes a good time to consider moving into MUH. You’ll collect a nice 5.8% income stream while you wait for its discount to close.

Beyond Munis: 4 Buys for 7.8% CASH Payouts and 20%+ Upside

As I mentioned earlier, a CEF’s discount to NAV is an incredibly reliable indicator that it’s poised to deliver serious price upside.

That’s true of the 3 funds I just showed you … and it goes double for the 4 other CEFs I want to show you now. Each one trades at an even more absurd discount to NAV than our 3 muni funds … so these 4 unsung funds are spring-loaded to catapult us to price gains of 20%+ in the next 12 months.

When you combine these 4 buys with our muni-fund CEFs, you get an “instant” portfolio that lets you dip a toe in some of the best income investments in the world: munis, high-yield REITs, preferred stocks, corporate bonds and dividend stocks, to name a few.

PLUS, these 4 amazing income plays also pay dividends 3 or 4 TIMES higher than your typical stock—up to 8.0%! So you’re getting paid very handsomely while you wait for these funds’ discount windows to slam shut.

Here’s a quick look at each of them:

- The real estate mogul: This fund has DOUBLED the market’s return since inception—including during the financial crisis—by investing in real estate, the very thing that caused the meltdown in the first place! It pays you 7.8% in cash today, and its silly discount points to a shockingly big price rise ahead.

- The bond play with a fat 7.2% payout: This one trades at a totally unusual 14.9% discount to NAV. And it has something I love in a CEF: management with skin in the game. The team at the top includes a Wall Street vet with $250,000 of his own cash in the fund, so you can bet he’ll be working for you.

- The perfect buy for rising rates: This one holds floating-rate loans, whose rates adjust higher with interest rates. If you want to hedge your portfolio against the Fed’s next move (and collect 6.4% in cash while you do) this fund is for you.

- The preferred-stock player: Preferred stocks trade around a par value, like a bond, but pay outsized dividends, fueling this fund’s amazing 6.9% payout. Better yet, preferreds have gone on sale in the last few months, driving this fund to a rare discount—and giving us our in.

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

Source: Contrarian Outlook

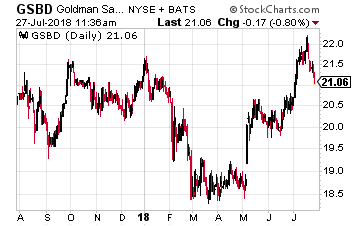

Goldman Sachs BDC, Inc. (NYSE: GSBD) is a newer BDC managed by the famed investment bank. The company launched with a March 2015 IPO. The dividend has been level at $0.45 per share since the IPO.

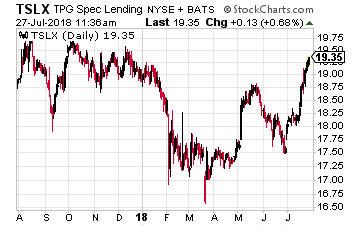

Goldman Sachs BDC, Inc. (NYSE: GSBD) is a newer BDC managed by the famed investment bank. The company launched with a March 2015 IPO. The dividend has been level at $0.45 per share since the IPO. TPG Specialty Lending (NYSE: TSLX) has been a publicly traded since March 2014. The BDC is managed by private asset manager TGP, which has $80 billion under management. The management team has demonstrated excellent discipline in its approach to making portfolio loans. As a result, the company has shown slow but steady NAV appreciation.

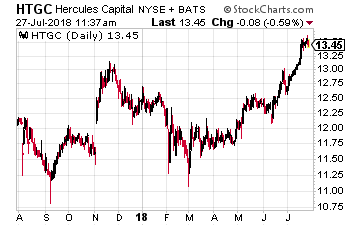

TPG Specialty Lending (NYSE: TSLX) has been a publicly traded since March 2014. The BDC is managed by private asset manager TGP, which has $80 billion under management. The management team has demonstrated excellent discipline in its approach to making portfolio loans. As a result, the company has shown slow but steady NAV appreciation. Hercules Capital (Nasdaq: HTGC) is an internally managed BDC exclusively focused on making loans and equity investments in the venture capital space.

Hercules Capital (Nasdaq: HTGC) is an internally managed BDC exclusively focused on making loans and equity investments in the venture capital space.

Pattern Energy Group (Nasdaq: PEGI) recently experienced a 12.5% decline when the province of Ontario announced it was cancelling over 750 renewable energy contracts. While Pattern Energy was not singled out, the company has a significant presence with several projects under development in Ontario.

Pattern Energy Group (Nasdaq: PEGI) recently experienced a 12.5% decline when the province of Ontario announced it was cancelling over 750 renewable energy contracts. While Pattern Energy was not singled out, the company has a significant presence with several projects under development in Ontario. Over the course of just one week, the share price of Uniti Group (Nasdaq: UNIT) declined by 20%. The drop was almost entirely due to a Wall Street analyst putting a sell recommendation on the stock with a $15 price target.

Over the course of just one week, the share price of Uniti Group (Nasdaq: UNIT) declined by 20%. The drop was almost entirely due to a Wall Street analyst putting a sell recommendation on the stock with a $15 price target.

The first is an old-fashioned, but effective, way. You can buy a mutual fund from a company whose sole focus is Asia – the Mathew Asia Dividend Fund (MUTF: MATIX). Its top holdings include well-known blue chips such as Taiwan Semiconductor and HSBC.

The first is an old-fashioned, but effective, way. You can buy a mutual fund from a company whose sole focus is Asia – the Mathew Asia Dividend Fund (MUTF: MATIX). Its top holdings include well-known blue chips such as Taiwan Semiconductor and HSBC.

Columbia Seligman Premium Technology Growth Fund (NYSE: STK) seeks capital appreciation through investments in a portfolio of technology related equity securities and current income by employing an option writing strategy.

Columbia Seligman Premium Technology Growth Fund (NYSE: STK) seeks capital appreciation through investments in a portfolio of technology related equity securities and current income by employing an option writing strategy. Eaton Vance Tax-Managed Buy-Write Opportunities Fund (NYSE: ETV) invests in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a substantial portion of the value of its common stock portfolio to generate current earnings from the option premium. Buy-Write is another name for covered call writing. Also, as the fund name states, the managers strive to generate the best after tax returns. The fund uses the S&P 500 stock index as its benchmark evaluate returns.

Eaton Vance Tax-Managed Buy-Write Opportunities Fund (NYSE: ETV) invests in a diversified portfolio of common stocks and writes call options on one or more U.S. indices on a substantial portion of the value of its common stock portfolio to generate current earnings from the option premium. Buy-Write is another name for covered call writing. Also, as the fund name states, the managers strive to generate the best after tax returns. The fund uses the S&P 500 stock index as its benchmark evaluate returns. BlackRock Enhanced Capital & Income Fund (NYSE: CII) seeks to achieve its investment objective by investing in a portfolio of equity securities of U.S. and foreign issuers. The fund also employs a strategy of selling call and put options.

BlackRock Enhanced Capital & Income Fund (NYSE: CII) seeks to achieve its investment objective by investing in a portfolio of equity securities of U.S. and foreign issuers. The fund also employs a strategy of selling call and put options.