If you’re an investor whose goals include earning a decent income from the money you have accumulated, following the Wall Street herd will cost you money: possibly a lot of money.

The investing advice you see, read or are told may not be well aligned with your long-term goals and success. Individual investors who are counting on their portfolios for long term income needs will be best served by learning how to pick a path away from the herd.

There are two themes in play that make it difficult for investors to realize success. The first is the short term focus of the financial news industry. That group focuses on providing entertaining news bites based on data points that change every day. It is a good idea to remember that what you see or read in the financial news is much more about the entertainment part of infotainment than it is about useful information.

The second factor that effects investors are the challenges faced by financial advisors. The typical financial advisor (I know there are exceptions) has a lot on his or her plate besides researching individual investments to discover the very best investments for each individual client. A common practice for full service investment firms is to put client money into portfolios made up of a selection of ETFs that are expected to meet a client’s stated investment goals.

Consider the case of investors who want to draw an income from their portfolio. With this goal, an investor would likely see several popular dividend income ETFs in a portfolio put together by a financial advice firm. Here is a list of those popular income ETFs and their current yields:

- Vanguard REIT Index Fund (NYSE: VNQ) with $35 billion in assets. Current effective yield: 3.86%.

- Utilities SPDR ETF (NYSE: XLU) is the largest utilities ETF with $8 billion in assets. Current yield: 3.07%.

- iShares Select Dividend ETF (NYSE: DVY) is a common stock ETF which as $17 billion in assets. DVY yields 3.1%.

- Vanguard High Dividend Yield ETF (NYSE: VYM) is another stock ETF focused on high-yield common stock shares. VYM has $29 billion in assets. The fund has a current SEC yield of 3.06%.

As you can see, a strategy of using popular income stock ETFs to build a portfolio with produce an average dividend income yield of 3.3%. That means an investor would get just $33,000 per year in income off a $1 million portfolio. I am pretty sure someone living off a million-dollar portfolio would like to receive quite a bit more than $2,750 per month.

The alternate solution for more income is to own a portfolio of individual stocks. There are hundreds of stocks with yields of 6%, 8%, and up into the teens. For my Dividend Hunter service, the primary focus is on the safety of the dividend payments. Yet the current recommended stocks list has an average yield of 8.0%. To illustrate, here is a list of five stocks that are diversified across different financial sectors with very attractive yields:

- Reaves Utility Income Fund (NYSE: UTG) is a utilities sector closed end fund that currently yields 6.1%.

- Hercules Capital Inc (NYSE: HTGC) is a business development company providing capital to growing technology companies. HTGC yields 9.7%.

- Macquarie Infrastructure Corp (NYSE: MIC) owns energy product terminals, power generation facilities and private aviation fixed base operations. This stock yields 7.8%.

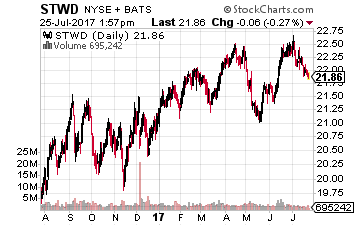

- Starwood Property Trust (NYSE: STWD) is a mortgage lender for commercial properties and yields 8.8%.

- InfraCap REIT Preferred ETF (NYSE: PFFR) is a new to the market ETF that only owns preferred shares of equity (property owning) REITs. The preferred shares have a higher safety level when compared to the bulk of the preferred shares market which are issued by lending institutions. PFFR yields 5.6%.

With just five stocks, you have a decently diversified portfolio and an average yield of 7.5%. That is double the average yield of the income focused ETF list above. I do recommend that investors own about 20 stocks for adequate diversification, but the list above gives you a graphic example of how if you learn about income stocks on your own, you can literally double the dividend income you earn off your investment portfolio.

Individual high yield stocks should be the cornerstone of your income portfolio. And these are the kinds of stocks my Dividend Hunter readers are using to build their own income streams… some of them quite massive. These stocks are part of my new income system called the Monthly Dividend Paycheck Calendar. It’s set up so that by following along you could see extra income of as much as $40,000 or more every year… for the rest of your life.

Source: Investors Alley

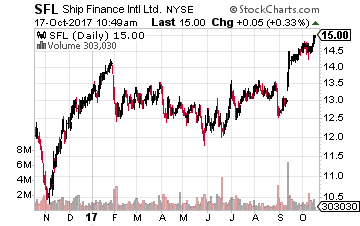

Ship Finance International (NYSE: SFL) owns a diverse fleet of commercial vessels. These ships are leased on long term contracts to shipping operators. Ship Finance gets a significant portion of its revenue from Seadrill Limited (NYSE: SDRL) which is going through a bankruptcy like reorganization. Ship Finance has worked out a new payment scheme with Seadrill, and in late August the SFL dividend was reduced by 22%. Contrary to what you would expect, after the initial price decline following the dividend announcement, the SFL share price has gained over 14%. I think the market is wrong about Ship Finance doing better after the dividend cut. I reviewed the company’s two must recent earnings reports and there are negative headwinds in several of the shipping sectors. I recommend against holding SFL shares through the earnings release in late November.

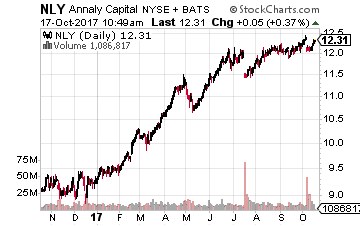

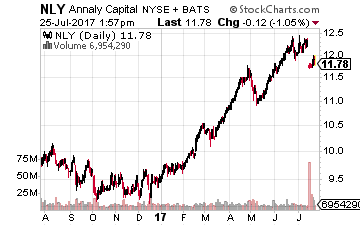

Ship Finance International (NYSE: SFL) owns a diverse fleet of commercial vessels. These ships are leased on long term contracts to shipping operators. Ship Finance gets a significant portion of its revenue from Seadrill Limited (NYSE: SDRL) which is going through a bankruptcy like reorganization. Ship Finance has worked out a new payment scheme with Seadrill, and in late August the SFL dividend was reduced by 22%. Contrary to what you would expect, after the initial price decline following the dividend announcement, the SFL share price has gained over 14%. I think the market is wrong about Ship Finance doing better after the dividend cut. I reviewed the company’s two must recent earnings reports and there are negative headwinds in several of the shipping sectors. I recommend against holding SFL shares through the earnings release in late November. Annaly Capital Management, Inc. (NYSE: NLY) is a high-yield, agency mortgage-backed securities (MBS) owning REIT. In its 2017 first quarter earnings report the company owned $74 billion worth of agency MBS. The company owns $10 billion of other assets, including $5 billion of commercial property mortgages. This large pile of assets is held aloft by a total of $72 billion of debt. In the quarter, Annaly reported an average asset yield of 2.93% and an interest cost of 1.74% leaving a net spread of 1.19%. This spread is down from the second quarter and almost half of the 2.28% spread reported in the first quarter of 2016. Long term rates as indicated by the 10-year Treasury bond remain stubbornly in the 2.25 to 2.3% range. The Fed plans to continue to increase short term rates. Last quarter, NLY just covered the $0.30 per share dividend. If the company does not cover the dividend this quarter, the share price will fall. This company’s profits are being tightly squeezed and the next Fed rate increase is going to significantly tighten the noose.

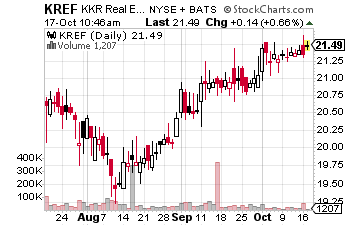

Annaly Capital Management, Inc. (NYSE: NLY) is a high-yield, agency mortgage-backed securities (MBS) owning REIT. In its 2017 first quarter earnings report the company owned $74 billion worth of agency MBS. The company owns $10 billion of other assets, including $5 billion of commercial property mortgages. This large pile of assets is held aloft by a total of $72 billion of debt. In the quarter, Annaly reported an average asset yield of 2.93% and an interest cost of 1.74% leaving a net spread of 1.19%. This spread is down from the second quarter and almost half of the 2.28% spread reported in the first quarter of 2016. Long term rates as indicated by the 10-year Treasury bond remain stubbornly in the 2.25 to 2.3% range. The Fed plans to continue to increase short term rates. Last quarter, NLY just covered the $0.30 per share dividend. If the company does not cover the dividend this quarter, the share price will fall. This company’s profits are being tightly squeezed and the next Fed rate increase is going to significantly tighten the noose. KKR Real Estate Finance Trust Inc. (NYSE: KREF) is a very new commercial mortgage REIT. The company came to market with a May 4 IPO. The shares were priced at $20.50, and now, are trading at $21.35. The company had $838 million dollars of committed capital at the end of 2016. The IPO raised another $200 million, which went into the KREF asset base. The prospectus lists a book value per share of $19.91 following the IPO. The public float after the IPO is 21.5% of the total shares. As of March 31, 2017, the company had originated $1.08 billion dollars of targeted assets. These asset types are senior real estate loans, mezzanine loans, and commercial mortgage backed securities (CMBS) “B pieces”. The third quarter earnings report will be KREF’s releasing of its first full quarter results. The danger with this stock is that it appears to be overpriced with a current 6.9% yield. Other, much larger, more established commercial mortgage REITs yield 7.9 to 8.8%. If KREF does not come out with very spectacular earnings then I expect that the market will start to price this stock like its peers, which means a 14% to 20% share price decline.

KKR Real Estate Finance Trust Inc. (NYSE: KREF) is a very new commercial mortgage REIT. The company came to market with a May 4 IPO. The shares were priced at $20.50, and now, are trading at $21.35. The company had $838 million dollars of committed capital at the end of 2016. The IPO raised another $200 million, which went into the KREF asset base. The prospectus lists a book value per share of $19.91 following the IPO. The public float after the IPO is 21.5% of the total shares. As of March 31, 2017, the company had originated $1.08 billion dollars of targeted assets. These asset types are senior real estate loans, mezzanine loans, and commercial mortgage backed securities (CMBS) “B pieces”. The third quarter earnings report will be KREF’s releasing of its first full quarter results. The danger with this stock is that it appears to be overpriced with a current 6.9% yield. Other, much larger, more established commercial mortgage REITs yield 7.9 to 8.8%. If KREF does not come out with very spectacular earnings then I expect that the market will start to price this stock like its peers, which means a 14% to 20% share price decline.

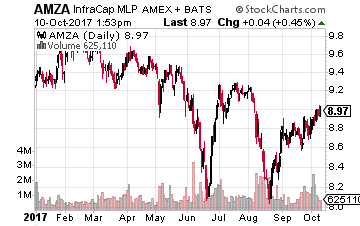

The InfraCap MLP ETF (NYSE: AMZA) sports a hard to believe 23% dividend yield. There is a range of reasons why that yield is so high, but at this point the quarterly dividends are sustainable at the current or close to the current level. If that is the case, AMZA is an investment that you can use to compound income and share count growth by over 5% every quarter.

The InfraCap MLP ETF (NYSE: AMZA) sports a hard to believe 23% dividend yield. There is a range of reasons why that yield is so high, but at this point the quarterly dividends are sustainable at the current or close to the current level. If that is the case, AMZA is an investment that you can use to compound income and share count growth by over 5% every quarter.

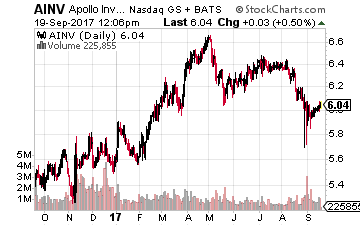

Apollo Investment Corp. (NASDAQ: AINV) is a $1.4 billion market cap BDC. The company reduced its dividend by 25% in 2016. AINV trades at a 10% discount to NAV. The current yield is 10.0% and the company’s net investment income just covered the dividend for the 2017 second quarter.

Apollo Investment Corp. (NASDAQ: AINV) is a $1.4 billion market cap BDC. The company reduced its dividend by 25% in 2016. AINV trades at a 10% discount to NAV. The current yield is 10.0% and the company’s net investment income just covered the dividend for the 2017 second quarter.

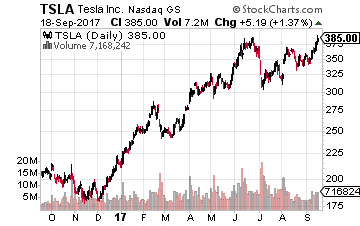

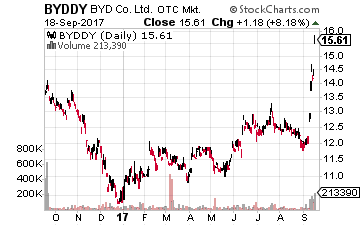

So let’s ‘imagine’ a bit… I’m going to reveal to you the best ways to play this milestone for the electric vehicle industry. And it does not involve buying Elon Musk’s Tesla Motors (Nasdaq: TSLA).

So let’s ‘imagine’ a bit… I’m going to reveal to you the best ways to play this milestone for the electric vehicle industry. And it does not involve buying Elon Musk’s Tesla Motors (Nasdaq: TSLA). Leading the race already in China is BYD (OTC: BYDDY), of which Warren Buffet owns 8.25%. It is currently the world’s largest electric car maker and produced nearly 47,000 electric and hybrid vehicles in the first seven months of 2017.

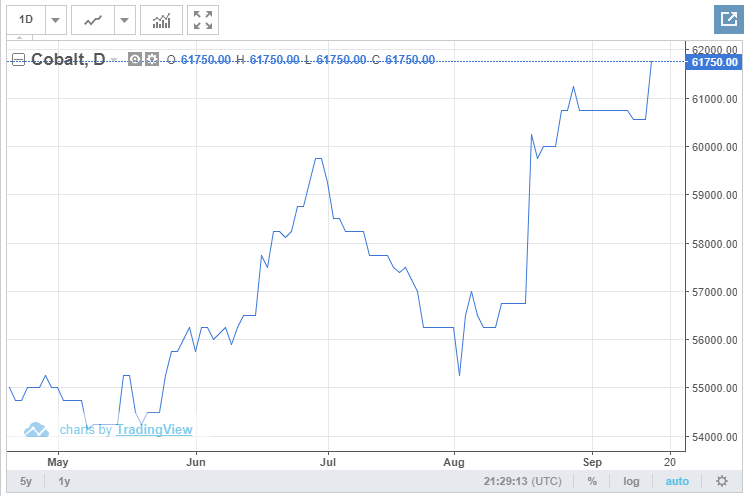

Leading the race already in China is BYD (OTC: BYDDY), of which Warren Buffet owns 8.25%. It is currently the world’s largest electric car maker and produced nearly 47,000 electric and hybrid vehicles in the first seven months of 2017. That hottest of all commodities sector centers on the key elements needed in lithium-ion batteries – lithium and cobalt (needed for the cathodes). These commodities account for roughly 60% of the cost of a lithium-ion battery, so says Simon Moores of the specialized consultancy, Benchmark Mineral Intelligence.

That hottest of all commodities sector centers on the key elements needed in lithium-ion batteries – lithium and cobalt (needed for the cathodes). These commodities account for roughly 60% of the cost of a lithium-ion battery, so says Simon Moores of the specialized consultancy, Benchmark Mineral Intelligence. Investors almost got it right this past week when they poured money into the Global X Lithium & Battery Tech ETF (NYSE: LIT). Investors sent the price of this ETF up by 10.25% last week, pushing this year’s gain to 55.25%.

Investors almost got it right this past week when they poured money into the Global X Lithium & Battery Tech ETF (NYSE: LIT). Investors sent the price of this ETF up by 10.25% last week, pushing this year’s gain to 55.25%.

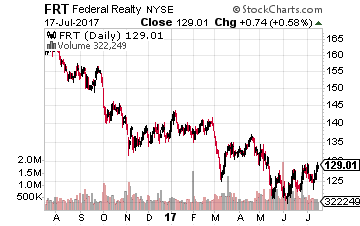

Federal Realty Investment Trust (NYSE:FRT) is a $9 billion market cap REIT that owns, operates, and redevelops high quality retail real estate in the country’s best markets. FRT has increased its dividend for 49 consecutive years, the longest growth streak of any REIT. Over the last 10 years, the average annual dividend increase has been about 5%. Last year the dividend was increased by 4.3%. Based on management guidance, an increase close to the 5% annual average is in the cards for this year. The company announces its new dividend rate in early August. The ex-dividend date will be in mid-September with payment about a week later. The FRT share price is down by 22% over the last year. This is a very high-quality REIT currently on sale. The stock yields 3.1%.

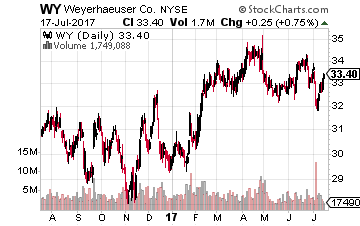

Federal Realty Investment Trust (NYSE:FRT) is a $9 billion market cap REIT that owns, operates, and redevelops high quality retail real estate in the country’s best markets. FRT has increased its dividend for 49 consecutive years, the longest growth streak of any REIT. Over the last 10 years, the average annual dividend increase has been about 5%. Last year the dividend was increased by 4.3%. Based on management guidance, an increase close to the 5% annual average is in the cards for this year. The company announces its new dividend rate in early August. The ex-dividend date will be in mid-September with payment about a week later. The FRT share price is down by 22% over the last year. This is a very high-quality REIT currently on sale. The stock yields 3.1%. Timberlands owner and wood products producer Weyerhaeuser Co (NYSE:WY) converted to REIT status in 2010. Since then the company has more than doubled its quarterly dividend rate. However, last year, the company did not increase the dividend. Weyerhaeuser completed a merger with Plum Creek Timber in February 2016, so it’s likely that the consolidation costs kept the company from announcing a higher dividend. Business results are off to a very strong start in 2017 compared to 2016. This points to a resumption of dividend growth this year. Historically, Weyerhaeuser announces a new dividend rate in the second half of August, with payment dates in September or November. The next dividend declaration date is August 24th with the next payment dates on September 22nd and December 15th. WY yields 3.7%.

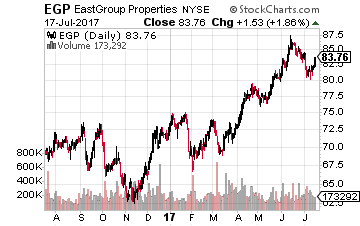

Timberlands owner and wood products producer Weyerhaeuser Co (NYSE:WY) converted to REIT status in 2010. Since then the company has more than doubled its quarterly dividend rate. However, last year, the company did not increase the dividend. Weyerhaeuser completed a merger with Plum Creek Timber in February 2016, so it’s likely that the consolidation costs kept the company from announcing a higher dividend. Business results are off to a very strong start in 2017 compared to 2016. This points to a resumption of dividend growth this year. Historically, Weyerhaeuser announces a new dividend rate in the second half of August, with payment dates in September or November. The next dividend declaration date is August 24th with the next payment dates on September 22nd and December 15th. WY yields 3.7%. Eastgroup Properties Inc (NYSE:EGP) is a $2.8 billion market value REIT that focuses on development, acquisition and operation of industrial properties in major Sunbelt markets throughout the United States with an emphasis on the states of Florida, Texas, Arizona, California and North Carolina. The industrial properties segment is currently one of the best performing real estate sectors. The company has increased its dividend for 21 of the last 24 years, including the last five in a row. Last year the payout was increased by 3.3%. This year my forecast is for a 5% to 7% increase. The new dividend rate should be announced in late August or early September, with a mid-September ex-dividend date and end of the month payment date. EGP yields 3.0%.

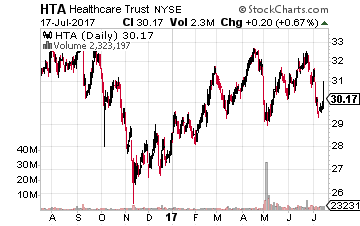

Eastgroup Properties Inc (NYSE:EGP) is a $2.8 billion market value REIT that focuses on development, acquisition and operation of industrial properties in major Sunbelt markets throughout the United States with an emphasis on the states of Florida, Texas, Arizona, California and North Carolina. The industrial properties segment is currently one of the best performing real estate sectors. The company has increased its dividend for 21 of the last 24 years, including the last five in a row. Last year the payout was increased by 3.3%. This year my forecast is for a 5% to 7% increase. The new dividend rate should be announced in late August or early September, with a mid-September ex-dividend date and end of the month payment date. EGP yields 3.0%. Healthcare Trust of America, Inc. (NYSE: HTA) is a $5.8 billion REIT that acquires, owns and operates medical office buildings. The company reduced its dividend in 2012 and 2013, which was followed by small increases in each of the next three years. Last year the dividend was bumped up by 1.7%, double the increase of the previous year. In 2016, the funds available for distribution per share increased by 12%, and for the 2016 first quarter, FAD per share was up 8.8% compared to a year earlier. Management has been very conservative with the dividend growth, but this year’s dividend increase may be significantly greater than the change of the past two years. Last year the new dividend rate was announced in early August, with an end of September ex-dividend date and early October payment date.

Healthcare Trust of America, Inc. (NYSE: HTA) is a $5.8 billion REIT that acquires, owns and operates medical office buildings. The company reduced its dividend in 2012 and 2013, which was followed by small increases in each of the next three years. Last year the dividend was bumped up by 1.7%, double the increase of the previous year. In 2016, the funds available for distribution per share increased by 12%, and for the 2016 first quarter, FAD per share was up 8.8% compared to a year earlier. Management has been very conservative with the dividend growth, but this year’s dividend increase may be significantly greater than the change of the past two years. Last year the new dividend rate was announced in early August, with an end of September ex-dividend date and early October payment date.

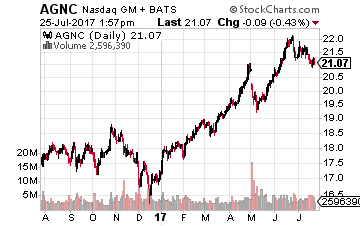

Investors familiar with the high yield residential MBS REITs may be surprised to learn that Starwood Property Trust is the third largest company by market cap in the sector. Only Annaly Capital Management, Inc. (NYSE: NLY) and AGNC Investment Corp (NASDAQ: AGNC) are valued higher than the STWD $5.7 billion market capitalization.

Investors familiar with the high yield residential MBS REITs may be surprised to learn that Starwood Property Trust is the third largest company by market cap in the sector. Only Annaly Capital Management, Inc. (NYSE: NLY) and AGNC Investment Corp (NASDAQ: AGNC) are valued higher than the STWD $5.7 billion market capitalization. Trust is that the company is a safe and steady cash flow generator. There are no risks in the Starwood balance sheet or income statement that would give a financial writer something interesting to dig into for an article. Safe and conservative doesn’t sell in the financial news world. It sounds pretty good for an individual investment portfolio.

Trust is that the company is a safe and steady cash flow generator. There are no risks in the Starwood balance sheet or income statement that would give a financial writer something interesting to dig into for an article. Safe and conservative doesn’t sell in the financial news world. It sounds pretty good for an individual investment portfolio.

ents start to hit my e-mail inbox. I look forward to reading about how much of a pay raise my income stocks are giving me every quarter.

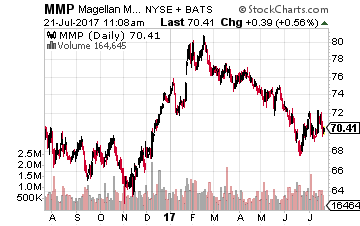

ents start to hit my e-mail inbox. I look forward to reading about how much of a pay raise my income stocks are giving me every quarter. Magellan Midstream Partners, L.P. (NYSE: MMP)primarily provides refined energy products pipeline and terminal services. Magellan has now increased its distribution for 61 consecutive quarters. The new distribution is 2% higher than last quarter’s payout and up 9% compared to one year ago. MMP yields 4.95%.

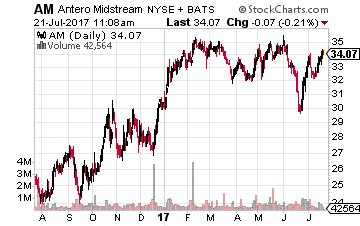

Magellan Midstream Partners, L.P. (NYSE: MMP)primarily provides refined energy products pipeline and terminal services. Magellan has now increased its distribution for 61 consecutive quarters. The new distribution is 2% higher than last quarter’s payout and up 9% compared to one year ago. MMP yields 4.95%. and has been increased by 21.8% over the last year. The units yield 4.5%.

and has been increased by 21.8% over the last year. The units yield 4.5%. The AM distribution was just increased by 6.7% and is up 28% year-over-year. The units yield 3.7%

The AM distribution was just increased by 6.7% and is up 28% year-over-year. The units yield 3.7%