Last week I was an invited speaker at the Las Vegas MoneyShow and made several presentations concerning income and dividend stock investing. I like the Q&A portion at the end of each talk. I benefit from learning what income focused investors are most interested in.

One topic that came up several times was my opinion in general about closed-end funds. A lot of these funds sport double digit dividend yields, which are catnip to income focused investors.

Closed-end funds (CEFs) are actively managed investment portfolios, whose shares trade on the stock exchanges. The closed-end part of the name is because these funds raise their initial capital with a one time sale through investment brokers and after that, the fund managers do not issue or redeem shares. The structure of CEFs produce a few interesting effects.

One is that share prices on the stock exchanges can be at significant premiums or discounts to the individual funds’ net asset values (NAV).

Another is that CEF fund managers cannot readily be influenced by share owners. Also, a lot of these funds are opaque concerning holdings and investment strategies.

It is my opinion that Wall Street firms use closed-end funds as a dumping ground for debt securities they manufacture that turn out to be more toxic than beneficial for investors in those securities.

Because of these reasons, I mostly stay away from the entire CEF sector. It would be too much work to analyze the hundreds of funds trading on the market to find the possible handful that are doing a good job. My recommendation to investors that ask me about CEFs is that there are better, safer ways to invest in high-yield securities.

Here are five CEFs with tempting yields where you should avoid that temptation:

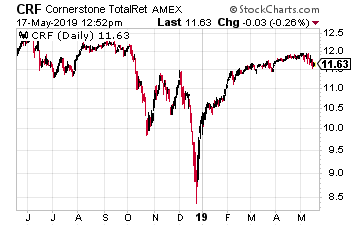

Cornerstone Total Return Fund (CRF) has the stated goal of seeking capital appreciation with current income through investment in common stocks, preferred stocks and convertible stock of large, mid and small cap companies and investment grade U.S. debt securities.

Current yield on the shares is an eye-popping 20.4%. A little digging shows why the yield is so high.

The fund’s policy is to pay out monthly dividends at a rate equal to 21% of the net asset value based on the NAV of the previous year.

The fund’s literature states “The Distribution Percentage is not a function of, nor is it related to, the investment return on a Fund’s portfolio.”

Basically, the big yield on CRF is the fund paying you back your own money. To add insult, CRF trades at a 7% premium to NAV. To buy the shares you pay $1.07 for a dollar’s worth of assets, which are then paid back to you as “dividends”.

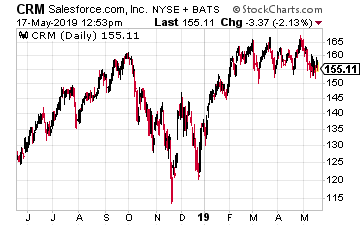

Cornerstone Strategic Value Fund (CRM) seeks long term capital appreciation through investment in global equity securities. Like Cornerstone above, this fund also yields 20% because it has the same dividend policy as its stablemate CRF.

Again the 20% is not a real return, but instead is likely to be the fund paying back your own capital. CRM currently trades at a 6% premium to NAV. These two funds, CRF and CRM are ones that I often get asked about. Looking at the distribution history, the dividends have ranged between 50% and 100% as return of capital.

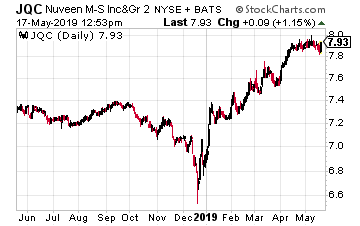

Nuveen Credit Strategies Income Fund (JQC) currently yields 15% and trades at an 8% discount to NAV. The fund invests in corporate debt securities or loans.

At the end of 2018 the fund adopted a capital return plan where now a portion of each dividend is explicitly return of capital. 63% of each monthly dividend is a return of your own money.

I think that is a pretty sneaky way for a fund management company to attract investors with a big stated yield. At least they make it very clear in the fund’s website exactly what they are doing.

But how many investors take the time to dig through a CEF’s website to see where the dividends come from?

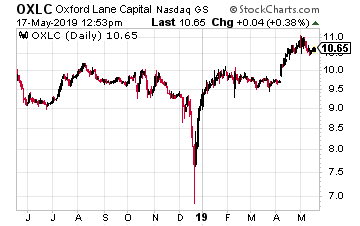

In contrast to the previous funds Oxford Lane Capital (OXLC)reports that 100% of its dividends are earned income. The fund sports a 15% yield.

The danger comes from its investment portfolio of debt and equity tranches of CLO vehicles. CLO means collateralized loan obligations. These are the type of securities manufactured out of pools of loans that caused the 2007-2008 financial crisis.

There is a huge amount of risk in this fund’s portfolio. The management team uses almost 40% leverage on the portfolio to leverage the highly leveraged securities it holds.

Finally, the shares trade at a 40% premium to NAV. Holy cow! What a time bomb.

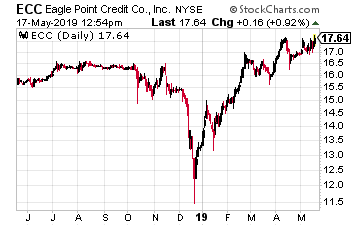

Eagle Point Credit Company LLC (ECC)also invests primarily in equity and junior debt tranches of CLOs. As I noted above, CEFs are a popular home for high risk securities.

For the last seven months 7 cents out of each 20 cent monthly dividend has been classified as return of capital, so the fund is not earning the dividends.

Current yield is 13.8% and the shares are trading at a 22% premium to NAV. That type of premium shows investors are buying shares without any understanding how the fund operates.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

You’re no doubt wondering if there’s anywhere you can invest and still get a decent return—without wincing every time you open your brokerage account.

Good news: there is just such a place. And today I’m going to show it to you—along with three specific “crash-resistant” funds yielding up to 7.1%.

The magical place I’m talking about is an often-ignored corner of the market called closed-end funds (CEFs).

Steady Dividends for Rocky Markets

There’s a weird twist that lets CEFs pay us dividends of 7.1% (and a lot higher) without exposing us to the risk of a surprise payout cut.

It comes down to the fact that several CEFs’ prices (on the open market) trade at a discount to the per-share net asset value (or the liquidation value of their portfolios).

In English?

This means that a CEF’s dividendyield based on NAV—the value that really matters to fund managers—is lower than the yield on market price. That simply makes the dividend easier for management to cover than you might think if you just looked at the “headline” yield.

Aside from a safe yield, these discounts to NAV also give us something else: bargains! Like these three ridiculously cheap, high-yielding and—most important—low-volatility funds:

CEF Pick #1: A Mega-Cap Fund With a Mega 6.8% Dividend

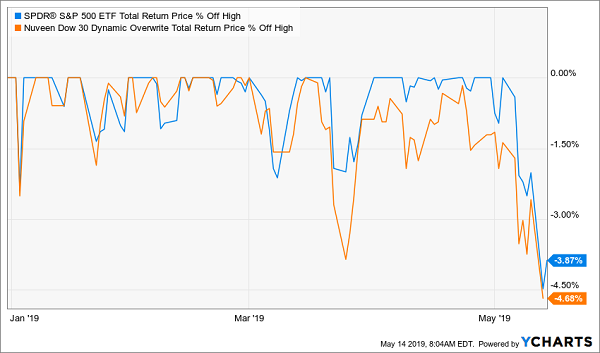

The Nuveen Dow 30 Dynamic Overwrite Fund (DIAX) is a large-cap index fund with a difference: it also sells call options against its portfolio.

Call options are a kind of insurance that essentially protects investors if they’re short the market and think it’s going to go down. DIAX sells those short sellers their insurance, meaning DIAX’s options will go down in value when the market goes up.

That’s one way that DIAX limits its downside. But its downside is already theoretically limited by its mandate: to buy Dow Jones blue-chip stocks. That focus on huge, well-established companies has helped the fund decline a bit less than the S&P 500 itself in this latest selloff:

A Lighter Downside

But that isn’t the best part. DIAX gets cash for selling those call options, and it returns that cash to shareholders. As a result, this fund yields 6.8% based on its market price, a whopping nine times more than the SPDR Dow Jones industrial Average ETF (DIA), which holds the exact same stocks.

CEF Pick #2: A Tax-Free 5.1% Dividend Perfect for the “Tariff Tantrum”

Of course, the best way to avoid stock-market volatility is to avoid stocks altogether. But how do you do that without getting a 0% (and worse, after inflation) return in cash or locking your cash up in Treasuries for 10 years for a crummy (and taxable) 2.4% yield?

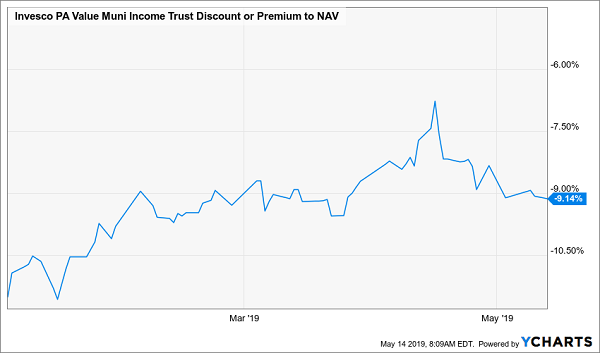

The answer? CEFs that hold municipal bonds, such as the Invesco PA Value Municipal Income Trust (VPV). This fund pays a nice 5.1% yield on its market price (4.7% based on NAV) that in reality is even higher for many folks, as that dividend is tax-free.

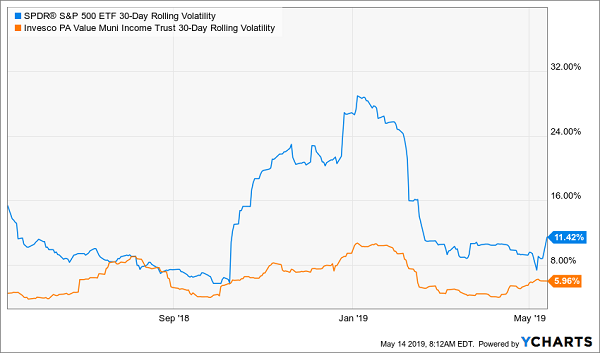

VPV also lacks the volatility of the market, and the best part is that it’s on sale:

A Sale Appears

With a 9.1% discount to NAV, you’re getting $1 of assets for less than a buck. But since the fund recently traded at a smaller discount, you’ll also likely have a chance to sell VPV for a gain if you hold for just a few months. Plus, the stock is much less volatile than the market (blue line below):

A Smoother Ride

With nearly half the volatility of the SPDR S&P 500 ETF (SPY), VPV will not see 20% drops in weeks like stocks do. But it will keep paying its big tax-free income stream, month in and month out.

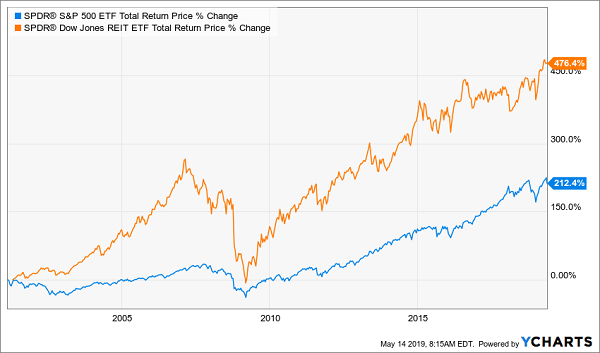

CEF Pick #3: A Bargain Real Estate Buy With a 7.1% Payout

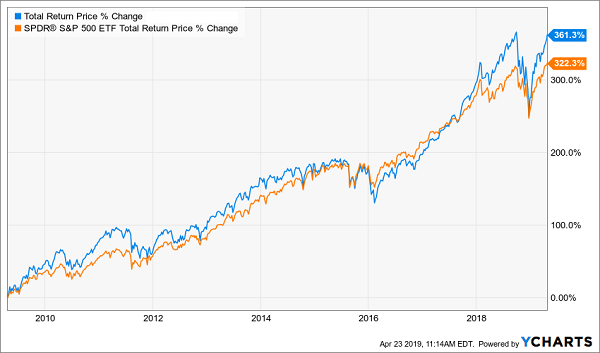

With 2008 being still relatively recent history, it’s easy to think of real estate as risky. But not only is real estate less volatile than equities over the long term, it also beats the market by a pretty big margin.

Real Estate for the Win

The SPDR Dow Jones REIT ETF (RWR) has crushed the S&P 500 over the long haul, with over double the total return. Note that this includes the massive bear market caused by the subprime mortgage crisis, which hit real estate much harder than stocks. Yet RWR is still the big winner.

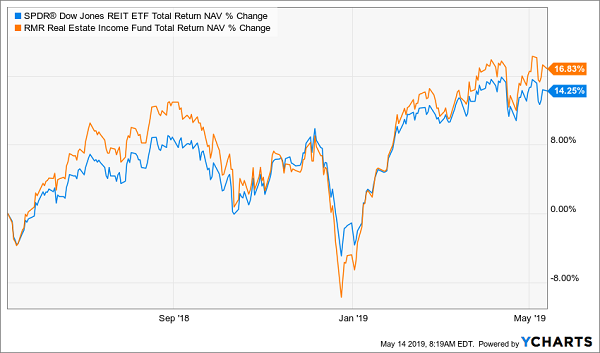

We can do better than RWR’s 2.2% yield, though. The RMR Real Estate Income Fund (RIF) has a 7.1% yield on market price and trades at a huge 20.8% discount (giving it just a 5.6% yield on NAV). There’s a reason for that discount: RIF’s long-term total returns of 4.3% on NAV are far worse than those of the competition. But that’s history. Thanks to some management adjustments, RIF has been doing much better, and has even started to outperform the REIT index fund:

Outperformance—Finally!

When the market realizes RIF isn’t the dud it used to be, expect its 20% discount to disappear—meaning some very nice price upside to go along with the fund’s 7.1% income stream.

NEW: The 4 CEFs You Must Buy Now (8.7% Dividends, Double-Digit Gains Ahead)

The story you just saw with RIF—a fund that has demolishes the market but is still cheap today—is something I see a lot in CEFs.

A situation like that really is the “sweet spot”: the outperformance shows that management has the chops to beat the market, while the yawning discount to NAV sets you up for even more upside!

And you’ll grab a 7%+ cash dividend while you wait for those gains to kick in!

That’s the exact setup you get with one of my four favorite CEFs now, which I’ll show you when you click right here.This bargain-priced fund focuses on high-yield utilities and real estate stocks, and yields an impressive 7.9%.

For good measure, it’s also thoroughly bested the market this year, with a 22% total return:

A Market-Beating Fund

Despite that gain, this fund is still cheap, trading at a ridiculous 13% discount to NAV. That’s why I’m calling for 20% price upside in the next 12 months, to go along with that rich 7.9% payout!

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

If you’re like, well, everybody, you’ve been mulling these three questions lately:

Is this “tariff tantrum” the end of the bull market? Is it time to sell? Or buy more?

I’ll deal with the first question in a second. Meantime, let’s start with the second one: no, it is not time to sell. Because after all, we need to stay invested to keep our dividend checks rolling in.

What about buying?

Yes, it’s still a great time to buy—especially in one corner of the market where 6%+ dividends are everywhere: closed-end funds (CEFs).

In a moment, I’ll reveal a CEF whose yield recently soared to nearly 7%! That makes it more than worth your attention, as buying now lets you “lock in” that payout before the next rebound drives the share price up—and the yield down as the stock climbs.

Before we get to that, though, let’s dive into what this trade melee means, and doesn’t mean, for stocks.

This Economy Is Already “Tariff-Tested”

The market has clearly spoken, and it hates the new 25% tariffs on $540 billion in Chinese imports. After all, tariffs raise prices on consumers and sideswipe growth, right?

Well, it’s not that simple.

Consider the previous round of tariffs: at 10%, they didn’t result in higher prices (inflation has actually slowed in the last three months). They didn’t hurt GDP growth, either: first-quarter GDP was up 3.2%, blowing away expectations of 2%.

And while it may be true that the economy could handle 10% tariffs, and not necessarily these far bigger 25% tariffs, that argument misses the point. The thing to keep in mind here is that this market’s reaction to the new tariffs is just plain silly.

That’s where our opportunity comes in.

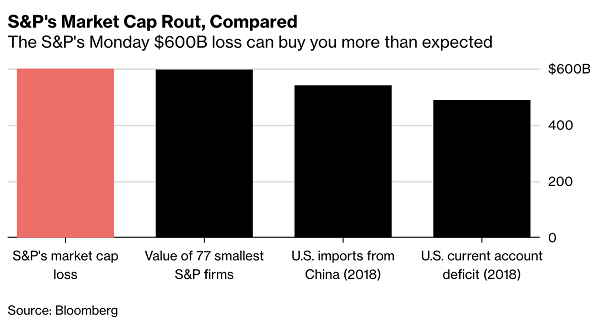

Here’s what I mean: in total, the tariffs will increase the cost of Chinese imports by $80.9 billion. That may sound like a lot, but it’s just 0.4% of America’s GDP—so tiny it’s almost unmeasurable!

Still if the market wants to price in the risk of a shakier economy that’s fine: but how big should that discount be? There’s no right answer to that, but I can tell you the wrong one: the amount that stocks have already lost.

As you can see, the S&P 500’s single-day loss on Monday was more than the total value of all imports from China! What’s more, this number doesn’t include the losses for stocks not in the S&P 500. For instance, the Russell 2000 has lost $273.6 billion, and the entire market has already lost a bit less than $1 trillion, even after Tuesday’s mini-recovery.

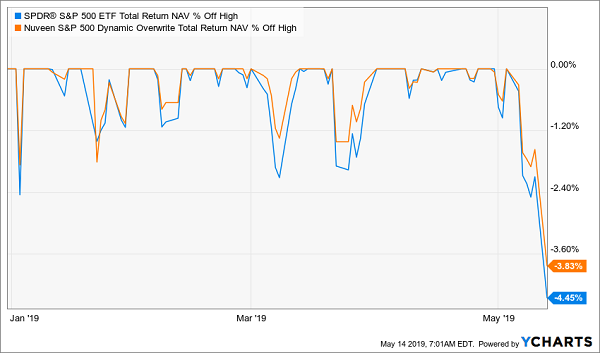

This 6.8% Dividend Is Built for a Correction

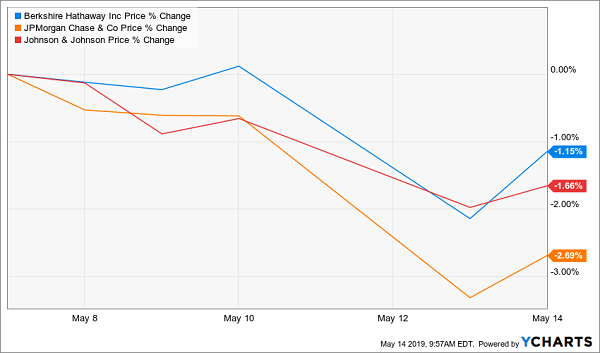

Clearly this market swing doesn’t make any sense. And situations like that make a CEF like the Nuveen S&P 500 Dynamic Overwrite Fund (SPXX) particularly appealing.

SPXX holds top-quality dividend payers (and growers), many of which are have been hammered in the panic—and therefore have plenty of built-in upside. Those include companies without much China exposure, like JPMorgan Chase & Co. (JPM), Johnson & Johnson (JNJ) and Berkshire Hathaway (BRK.A).

SPXX Lets Us Pick Up Strong Stocks and a 6.8% Dividend

There’s more, too, because SPXX also uses covered calls (a type of option that the fund’s managers sell against the shares SPXX holds) to generate extra income, so the fund can deliver that 6.8% dividend to investors.

These options trades also smooth out SPXX’s volatility, meaning it has posted a smaller drop during this latest correction, as its options go up while the market falls:

SPXX Rarely Dives as Far as the Market

Finally, high dividend yields like that of SPXX give you a better shot at living on dividends alone in retirement—and not having to sell your stocks into a downturn like this latest one to generate extra income.

Doing This Would Be a Big Mistake Right Now

In light of the big hit stocks took in late 2018, you might still be hesitant to buy SPXX—or any stock fund—during this latest volatility. That’s understandable, but you’re making a mistake if you let your 2018 fears keep you on the sidelines.

Here’s why.

While the trade war was one reason for the late-2018 downturn, it was really just a sideshow: that collapse had the Federal Reserve’s name written all over it.

With the Fed raising interest rates at a breakneck pace in 2018, an inverted yield curve looked inevitable, and parts of the Treasury-yield curve did briefly invert. Since an inverted yield curve is the most reliable recession indicator in the world, the fear behind the late-year collapse was understandable.

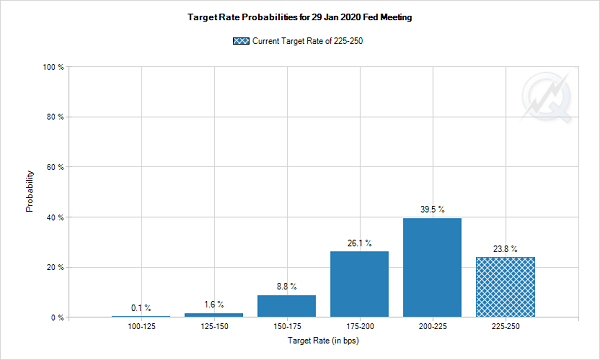

But the Fed isn’t raising rates anymore.

In fact, the Fed has made it clear that it will not raise rates in 2019, and futures markets are betting that rates may actually go down in 2019:

Possible Rate Cut Could Ignite Stocks—and CEFs

Source: CME Group

Let me leave you with this: the Fed is much more important to the economy than politics could ever be. The Fed’s easy monetary policy is a big reason why GDP growth was 3.2% at the start of the year, and it’s also why company sales and profits will stay strong.

It’s only a matter of time before the market realizes this and regains its footing (though we’ll likely see some bumps in the road first).

Revealed: 4 Shocking Selloff Bargains Yielding Up to 10.7%

SPXX isn’t the only terrific opportunity this correction has handed us. It’s far from the highest yielder worth jumping on, either.

For example, consider the ignored CEF my team and I have uncovered: it boasts something most people will tell you is impossible: a 10.7% dividend that’s growing triple digits!

That’s right: this unsung fund yields a mammoth 10.7% as I write, and its payout has exploded 150% in the last decade:

1 Click for a Massive Yield and Soaring Payout Growth

How does this fund do it?

My 10.7%-paying pick is run by a hand-picked investment “all-star team.” These pros have quietly assembled a “no-gimmicks” portfolio of value and growth stocks that are great “buy the dip” opportunities now.

I’m talking about the likes of Visa (V), Microsoft (MSFT), Alphabet (GOOGL) and Abbott Laboratories (ABT).

I know what you’re going to ask next: how has this so-called “all-star team” performed in the past?

See for yourself:

A 10.7%-Paying Market Dominator

Best of all, as this monstrous return includes dividends, a huge slice of it was in cash, thanks to my pick’s massive dividend payout.

Oh, and if you hear “investment all-star team” and think “high fees,” fear not. This fund charges just 1.01% of assets, one of the lowest fees in the CEF universe!

Finally, this fund trades at an unreal 5.1% discount as I write. It’s only a matter of time before that shifts to a massive premium, given this fund’s market dominance, 10.7% yield and 150% dividend growth.

The time to buy is now.

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

The MoneyShow folks have now been asking to come back for five years. Each year it is a great time, and I love to get in front of the investing public.

As the spring show is held in Las Vegas, I thought it would be appropriate to cover some gaming related income stocks.

When it comes to the choice between being a tenant or a landlord, I like being on the landlord side, collecting a rent check every month.

At the end of the day (quarter and year) that is what being an investor in real estate investment trusts (REITs) means. Becoming a commercial property landlord through REIT ownership lets you become a first dollar investor in a wide range business types and industries.

The companies that lease from a REIT have a first dollar commitment to pay those rent checks. Yet often, a REIT will be able to participate in any positive business results produced by the tenant companies.

Gaming companies are a tough group of stocks to own. Profits swing wildly based on economic conditions and the tremendous competition in the areas that allow casino type gaming. Also, most of the gaming companies carry a large amount of debt. It costs a lot of money to build casinos!

It was the debt loads that pushed several publicly traded gaming companies to start to spin-off properties into REIT holding companies. The sponsored REITs gave the gaming companies a way to monetize assets and pay down debt. The gaming REITs are growth focused through the acquisition of additional properties to help support the growth of the sponsor gaming companies.

These three come to mind for your investment consideration.

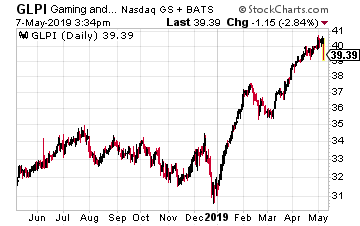

Gaming and Leisure Properties (GLPI) was the first gaming focused REIT when it was spun-out in 2013 by Penn National Gaming.

At that time the new REIT received 21 casino and racetrack properties. The company now owns 44 properties that are leased to and operated by Penn National Gaming, Casino Queen, Eldorado Resorts and Boyd Gaming.

In 2018 the company acquired five casinos from Tropicana Entertainment as the real estate part of the takeover of Tropicana by Eldorado Resorts. Of the three REITs here, GLPI is the most independent, with the ability to put together property and lease deals with a range of gaming companies. The REIT has an $8.7 billion market cap.

The dividend has grown by 5.6% per year over the past three years, and the GLPI shares yield 6.7%.

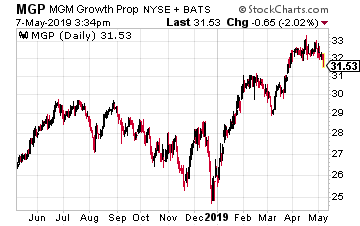

MGM Growth Properties LLC (MGP) was spun out in 2016 by MGM Resorts International. The initial REIT portfolio consisted of 10 MGM run properties, including seven on the Las Vegas strip. MGP now owns 14 properties all leased to MGM.

MGM Growth Properties has a triple-net master lease agreement with MGM Resorts which means all the REIT properties are on a single lease and the gaming company cannot single out one to close or not pay rent.

EBITDA from MGM coverage of the master lease payment is 6.2 times. The lease as a built in 1.8% rent escalator and MGP will also share profit growth at the casinos.

The MGP dividend has grown by 30% since the IPO and the shares yield 5.5%. MGP has a $9.2 billion market cap.

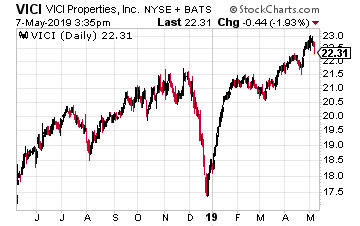

In October 2017 VICI Properties Inc. (VICI) was spun-off by Caesars Entertainment as part of the casino company’s bankruptcy reorganization.

Initially VICI owned 19 Caesars managed properties and that number has grown to 23. VICI has a triple-net master lease arrangement. The REIT has call options or right of first offering on six additional Caesar properties with another seven targeted for likely acquisition. VICI has a lot of growth potential.

VICI’s current market cap is $9.4 billion. Only four full quarter dividends have been paid.

There has been one dividend increase of 9.5%. Current yield is 5.0%.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Did the latest tariff tiff set the stage for the next pullback in stocks? Will this bull market actually die of old age?

The macro picture is dicey and stock valuations are pricey, but we must stay invested. The stock market goes up about two-thirds of the time. Permabears miss out on compounding and it’s not as easy to be a part-time bear as it sounds.

To illustrate this let’s consider a study by Hulbert Financial. The firm looked at the best “peak market timers”–the gurus who correctly forecasted the bursting of the Internet bubble in March 2000 and the Great Recession in October 2007.

These were the clairvoyant advisors who had their clients out of stocks and mostly in cash when the S&P 500 was about to be chopped in half. Surely their clients did great over the long haul, given their capital was largely intact at the market bottoms, right?

Wrong. None of these advisors turned in top performances. The reason? While they were good at timing tops, they were terrible at timing bottoms! The bearish advisors didn’t get their clients back into stocks anywhere near the bottom. They had their capital intact, but they didn’t deploy it–and they largely missed out on the epic bull markets that followed these crashes.

Think about the advisors and investors who sold in late December when the “bear market” became official. They moved to cash at the worst possible moment and have been on the sidelines waiting for a low risk “retest” of the lows. Mr. Market loves to confuse the most amount of people, and he really outdid himself this time!

Barely a Bear Market…

… And Right Back to a Bull!

Now we can be smart about staying in the market. While bull markets may not die of old age per se, this one is ten years old. They don’t run forever, so we should focus on pullback-proof names. Here are five rules to follow for 15% per year returns regardless of what the broader market does.

Recession-Proof Rule #1: Trust Your Dividends

Secure dividend yields are truly the “rubber duckies” of the investing world. Mr. Market can push them underwater for a period of time, but eventually, they rocket back up to the surface.

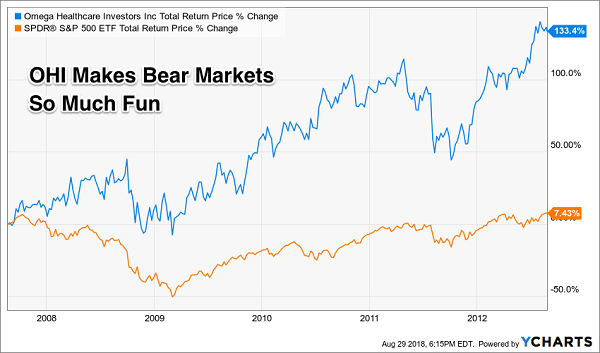

Let’s consider Contrarian Income Report favorite Omega Healthcare Investors (OHI), a big paying landlord in the skilled nursing space. It’s rewarded CIR subscribers with steady 8.1% returns per year, mostly from well-funded quarterly payouts. Anytime OHI rallies I get questions about whether we should book profits. Well, we rarely want to sell a great dividend stock like this–even when our crystal ball forecasts impending doom.

We’ll rewind 11 years to the top of the last extended bull market. If you were savvy enough to time the top in 2007, you would still have been doing yourself a disservice by selling your OHI shares (not least, how would know when to have “gotten back in?”)!

This Dividend Payer Barely Went Below the Water

Five years later, as the S&P 500 barely recovered its crash losses, OHI investors had enjoyed 133% returns (including steady, fat payouts throughout). And while the presence of a dividend does not guarantee protection from losses, examples like this one show that payout-focused investors have a serious edge in the markets because:

Buying stocks for their dividends alone makes day-to-day price action irrelevant.

Of course, you know this already! And you’re probably already wondering how we turn OHI’s 8% returns into 15% per year, so let’s get into rule number two.

Recession-Proof Rule #2: Buy Fast Growing Dividends

Dividends are magnets that pull their share prices along with them. If you’re looking for the stock market’s tail that wags the dog, pay attention to the payouts attached to a given share price.

Regardless of what the stock market does during any given trading session (or month, or whatever), share prices eventually follow their dividends higher. For example, let’s consider Texas Instruments (TXN), which has increased its payout (orange line below) by an amazing 600% over the last decade. Its stock price (blue line) was pulled higher by its dividend:

TXN’s Dividend Magnet

My Hidden Yields subscribers have made 55% in two years from TXN. Two generous dividend raises have provided much of this fuel. And the kicker? We bought when shares were “due” to pop because they had fallen behind their dividend curve.

Recession-Proof Rule #3: Find the Lagging Stock Price

The best time to buy a stock like TXN is nearly anytime. But we can “cherry pick” our entries (and put option sales) by focusing on times when TXN’s price falls behind its payout curve.

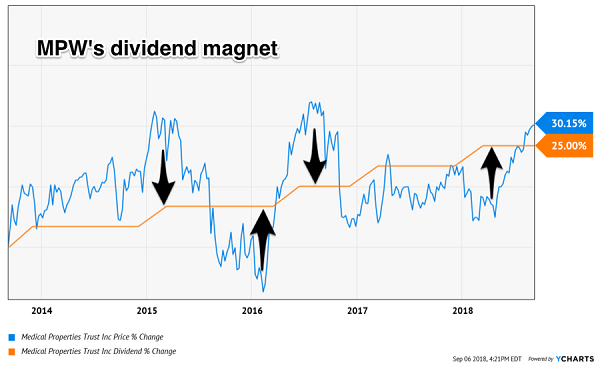

Regular readers will remember Medical Properties Trust (MPW), a hospital landlord we bought and later sold for 105% total returns. MPW’s dividend magnet was part of our secret, and the fact that we bought when the price was lagging dividend growth and sold after it had overtaken it. The “up” arrows below show good times to be a buyer, while the “down” arrows indicate times to hold or sell:

The Cues from a Dividend Magnet

Recession-Proof Rule #4: Buybacks Are a Nice Bonus

Share repurchases can provide fuel for dividend growth. When a firm buys back stock, it saves cash on dividends because it doesn’t have to “dish out” for those retired shares.

Buybacks today are the gifts that keep on giving tomorrow. By reducing the share count, they make every “per share” metric of profit and cash flow look better. Plus, they make it easier to grow the dividends because there are fewer shares to pay them to!

Buybacks work best when the stock itself is cheap. After all, the price you pay for something always matters. Smart management teams take advantage of depressed stock prices to provide their investors with a nice bonus.

Recession-Proof Rule #5: Low Payout Ratios: Where the Party’s At

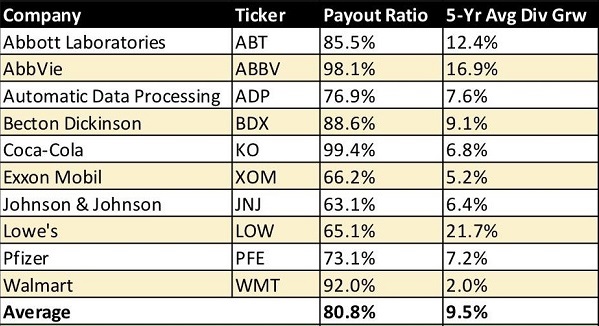

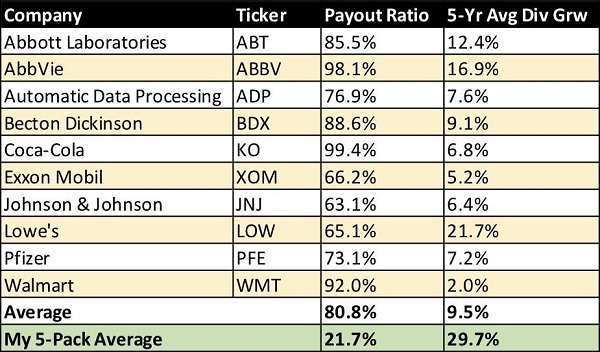

Some dividend-income investors think they are following this strategy by purchasing dividend aristocrats, or stocks that have increased their payouts every year for 25 straight years:

“Brett, I don’t own the S&P 500 index for income. I choose the best companies in the index, the ones whose dividends have gone up and up. The dividend aristocrats.”

Problem is, many of these monarchs have their best years behind them. Check out these payout ratios, or the percentage of profits that these aristocrats are paying out as dividends:

Sky High Payout Ratios

The 9.5% average dividend growth rate above is nice but it’s not sustainable. These firms are already paying 80% of their profits as payouts, when anything more than 50% can spell trouble! This means their upside potential for the next five years is likely limited.

So, let’s look past these paupers for lesser-known bargains that are primed to double their dividends and prices over the next five years. Some will double within three!

How is this possible? These five stocks are only paying 20% of their earnings as dividends, which means they could multiply their payouts by 2X, 3X or even 4X today and still have room to grow without risk of a dividend cut.

They won’t do it overnight, however. These firms will bump their dividends by 15%, 20% and even 25% or more per year. Which means their stock prices will eventually follow, and investors who buy today will double their money with these safe dividends.

7 Dividend Stocks That’ll Double Your Money Every Few Years

Since inception, our Hidden Yields portfolio has exceeded our lofty 15% benchmark, returning 16.4% per year. This means our inaugural subscribers are well on their way to doubling their money with safe dividend stocks. With patience and persistence, you too can enjoy the same types of returns by following our dividend double strategy.

Today, I want to share seven of my recession-proof “Hidden Yield Stocks” with you.

My research indicates each of these investments could easily pay you 15% per year. That’s enough to double your money in under 5 years. Imagine, turning a retirement ‘pot’ of $250,000 into $500,000… or… $500,000 into $1,000,000… and on it goes.

Imagine no more fear of your savings running dry… no more worrying about wild market swings or crashes… no more risky-bets on penny-stocks or cryptos… no more penny-pinching in your golden years.

So, if you’re not quite as wealthy as you hoped you’d be… if you wish you had more money in your retirement account… and… if you’re looking for safe, secure growth over the next 5, 10, 15, even 20 years—as well as predictable income—this could be the most important investment advice you ever read.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

I’ve uncovered two high-yield closed-end funds (CEFs) that are perfect for this “earnings down, stocks up” market.

I’m going to show you both of these bargain-priced, cash-spinning plays—one of which yields an incredible 9.2%, five times more than the typical S&P 500 stock—shortly.

First, we need to talk about where stocks stand now. Because you’re probably wondering how the market can keep ticking up when first-quarter earnings are actually down from a year ago.

You’re right to be concerned, because it makes zero sense—on the surface. But dig deeper and you’ll see that this is a good news story, and a perfect opportunity for contrarians like us to grab big gains (and dividends).

Let’s get into it.

When a Loss Is a Gain

With earnings season half over, profits have fallen 2.3% year over year. That sounds bad, but it’s actually better than the 4% drop analysts predicted before the season started.

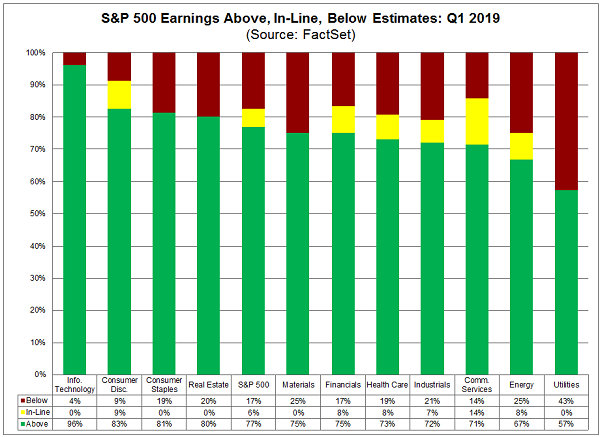

The reason? Surprises. A total of 77% of companies are reporting earnings above estimates, thanks to better-than-expected 5.1% sales growth. Sales are the lifeblood of profits, so this makes it easier to beat profit expectations.

Those earnings beats are also evenly distributed across sectors, with over half of companies in all sectors showing better-than-expected results:

Beating Expectations Across the Board

Again, the common theme is that sales are growing across sectors: people are buying more stuff, and that’s helping earnings across the market.

But Why Are Earnings Down?

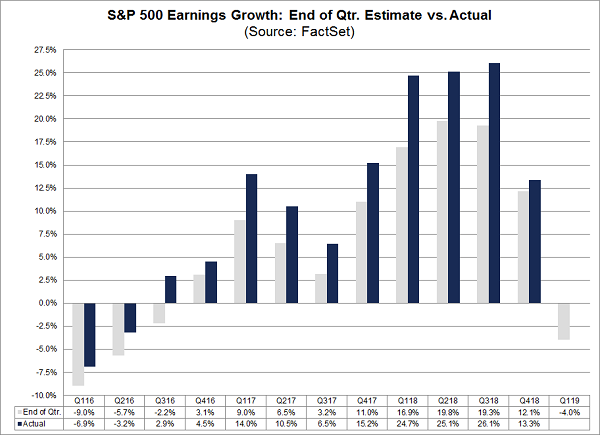

That brings us to the question of why earnings are down at all. If things are so good, why aren’t profits up? There are two answers: the first is that year-ago profits were so strong that they’re tough to build on.

A Big Hill to Climb

In the first quarter of 2018, earnings jumped 24.7% and stayed at that level for the next two quarters. As you can see above, such growth is unusual—and a tough act to follow!

That’s why analysts were modest in their earnings estimates for this quarter. But now earnings are coming close to the mark set a year ago, showing that the economy is still strong, and companies are still in great shape.

The second reason for the lack of earnings growth is that the first quarter tends to be weak. The post-holiday period is no time to load up the credit card, so Q1 expectations are often modest.

In fact, any growth in the first quarter following growth a year earlier is exceptional. That makes 2018’s 24.7% profit jump unusual, since it followed 14% growth a year previous. To expect three straight years of first-quarter growth would be very optimistic indeed.

The takeaway? The economy isn’t getting overheated but isn’t cooling down, either.

Next Leg of Growth About to Kick Off

With first-quarter economic growth ticking along at 3.2%, according to the Commerce Department, it’s no surprise that companies are seeing sales jump 5.1%. That growth also positions them up to expand their operations and set themselves up for higher sales and profits in the future. And companies are doing just that: they spent more on buying, building and upgrading assets in 2018, and that trend is continuing.

But the market hasn’t priced this growth in—not even close. And this is where our opportunity shows up.

A Buying Opportunity in Disguise

Stocks are up less than 10% since before earnings saw three consecutive quarters of 25% growth, which is below the average return stocks deliver in the long term. That means it isn’t too late to get into the market, even if the rebound we’ve seen this year makes it feel that way.

And you’ll be able to buy in even cheaper with the two CEFs I mentioned off the top. Let’s move on to those now.

Two CEFs to Ride the Market Higher (and bag yields up to 9.2%)

Our first high-yield play is the Boulder Growth & Income Fund (BIF), which focuses on bargain-priced large caps. This fund holds much of its portfolio in Warren Buffett’s Berkshire Hathaway (BRK.A, BRK.B), along with other top-quality stocks like JPMorgan (JPM) and American Express (AXP).

So why buy BIF instead of cutting out the middleman and just buying its collection of well-known names on your own?

Simple: as I write, BIF trades at a massive 16.8% discount to net asset value (or NAV, another name for the value of the stocks the fund owns). That means you’re getting these top-quality large caps for 87 cents on the dollar! And while BIF’s 3.7% dividend yield is low for a CEF, it’s still double what the typical S&P 500 name pays.

Finally, you can juice your income stream more with the 9.2%-yielding Cohen & Steers Income Builder (INB), holder of some of the best companies in America, with Microsoft (MSFT), Visa (V), Philip Morris (PM) and Amazon (AMZN) standing out among its top holdings.

Here’s the key point to remember about INB: its NAV has returned 14.2% this year (including dividends and price gains). But investors are giving it very little credit, because the fund still trades at 10.8% below its NAV! That’s one of the widest gaps in the CEF space, and it points to more upside as that discount narrows.

NEW: The 4 CEFs You Must Buy Now (8.7% Dividends, Double-Digit Gains Ahead)

As I just showed you, stocks are still a great buy as investors (slowly) discover there’s still time to get in on this “goldilocks” economy.

And as you saw with BIF and INB, you’ll do better (and grab far higher dividends) if you make your move through a CEF. The best of these funds give you the best of all worlds: huge dividends, market outperformance and bargain prices—often all in one buy.

I know that sounds crazy: a fund that’s still cheap even after a monster gain. But it’s a familiar story with CEFs, thanks to their weird discounts to NAV.

Consider one of my four favorite CEFs now, which I’ll show you when you click right here. This fund focuses on high-yield utilities and real estate stocks, yields an impressive 7.9% and has thoroughly bested the market this year, with a 23% return:

A Market-Beating Fund

Here’s the surprising part: despite that gain, this fund is still cheap! It trades at a 13% discount to NAV, which gives us two advantages you’ll never get buying stocks individually or through an ETF. That’s why I’m forecasting 20% price upside in the next 12 months, to go with that rich 7.9% payout.

Michael Foster has just uncovered 4 funds that tick off ALL his boxes for the perfect investment: a 7.4% average payout, steady dividend growth and 20%+ price upside. — but that won’t last long! Grab a piece of the action now, before the market comes to its senses. CLICK HERE and he’ll tell you all about his top 4 high-yield picks.

We retirees and soon-to-be retirees have a dilemma. The traditional pension is just about gone. Social Security won’t support the lifestyle most of us want. We are left to our own devices.

But even if we do build up a fat balance in a 401(k) or other company retirement plan, how do we make it last? Especially when the bank pays “zero point nothing.” Today, you can’t find anything that pays significant “interest.”

This is becoming a crisis in the US. We are told that stocks provide the best returns over the long term, but retirees need income now. Most retirement investors prefer dividend income to long-term gains, but yields haven’t been this low in decades! The S&P 500 pays a measly 2% or so today. If you have a million-dollar portfolio, that’s a lousy $20,000 per year in income, or $385 a week. That’s no retirement.

Now some dividend-income investors protest, “But I don’t own the S&P 500 index for income. I choose the best companies in the index, the ones whose dividends have gone up and up. The dividend aristocrats.” But are they true monarchs or mere pretenders to the throne.

The problem with growing your dividends for a minimum of 25 consecutive years is that’s a lot of time for your own profit growth to slow down. That means many of your dividend increases are cutting even further into your earnings. You don’t want to break the bank, so your hikes shrink over time–a couple percent here, a couple percent there, just to keep your Aristocrat lapel pin.

I’ll let you in on a secret: Sometimes, the best place to make your dividend-growth play is on the ground floor, in companies that have really only begun to scratch the surface. In fact, two of the picks I’m about to show you have been paying dividends for less than five years.

Let me show you the difference between some of the largest blue-chip Dividend Aristocrats and my plucky group of five turbo-charged dividend growers:

These Blue Chips Are Crawling to the Finish Line

The 9.5% growth rate above is nice but it’s not sustainable. These firms are already paying 80% of their profits as payouts! This stat is great for the last five years, but awful for the next five–and that’s what we care about.

So let’s look past these paupers for lesser-known bargains that are primed to double their over the next five years. Some will double within three!

How is this possible? These five stocks are only paying 20% of their earnings as dividends, which means they could multiply their payouts by 2X, 3X or even 4X today.

They won’t do it overnight however. These firms will bump their dividends by 15%, 20% and even 25% or more per year. Which means their stock prices will probably follow, and investors who buy today will double their money with these safe dividends.

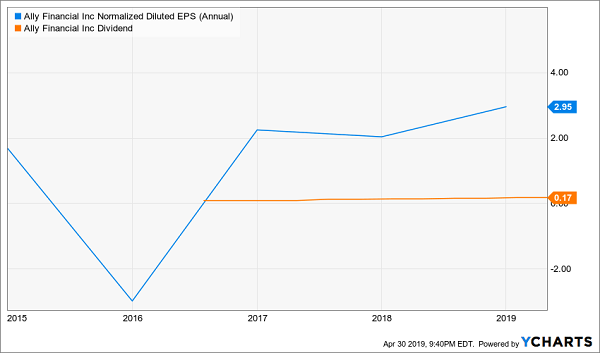

Ally Financial (ALLY) as we currently know it has only been around since 2010, but the company has roots going all the way back to 1919 as General Motors Acceptance Corporation (GMAC) – the financing-providing arm of automaker General Motors (GM).

The company still has extensive automotive operations, providing financing for more than 4 million customers across 18,000 dealerships. But Ally also offers online banking, vehicle insurance and credit cards, among other products. It also re-entered the mortgage business in 2016 via its direct-to-consumer Ally Home, and in mid-April, it announced a partnership with Better.com to launch a digital mortgage platform.

Ally Financial’s top and bottom lines have ebbed and flowed over the past few years, but things are starting to perk up, and the pros are starting to take notice. The company beat Q1 earnings estimates in April, prompting a couple “Buy” calls. That included one from Oppenheimer analyst Dominick Gabriele, who wrote, “We see a long runway for earnings given continued strong management execution that some investors are only just beginning to appreciate.”

The company started dividends relatively recently, at 8 cents per share in 2016, and has already more than doubled it at its current 17 cents per share. That history–as well as optimistic profit-growth estimates of 10% annually through 2024–would almost seem to guarantee breakneck dividend growth going forward … right?

In early April, Ally announced a massive $1.25 billion repurchase program for 2019 that was far more than what most analysts expected. When you factor in that, the financial stock’s total “cash return” payout ratio is actually a hair above 100%. So yes, Ally does indeed have the means to make major dividend increases going forward … but only if it’s less aggressive about buybacks.

Valvoline (VVV) is a global juggernaut in its relatively niche area of the market. It offers automotive services and supplies lubricants to more than 140 countries, including 1,170 quick-lube stores in the U.S. It has roots going all the way back to 1866, though the company is a relative newbie on the public markets, executing its IPO in 2016.

The dividend is just as fresh, so its five-year growth is extrapolated out from its original 4.9-cent dividend to today’s 10.6-cent payout.

That’s a lightning-quick doubler!

The stock hasn’t been nearly so spry, however. VVV has bounced back and forth since it came public, and shares sit about 16% lower than their IPO price. Particularly troubling was its fiscal first-quarter report in February. Not only did Valvoline miss the mark on both earnings and revenues, but it announced a restructuring to “reduce costs, simplify processes and ensure that the organization’s structure and resource allocation are focused on key growth initiatives.” The initiative should save the company about $40 million to $50 million pretax each year starting with fiscal 2020.

Valvoline surely has the room to keep the pedal down on its dividend, though the company’s focus now appears to be reinvigorating growth. I would wait to see green shoots from its restructuring efforts before even considering a move into VVV.

Income investors should know that earnings payout ratios for dividends don’t always tell the whole story. Net income can be manipulated, after all. So I also like to look at free cash flow payout ratios. (You can calculate free cash flow simply by subtracting capital expenditures from operating cash flow.)

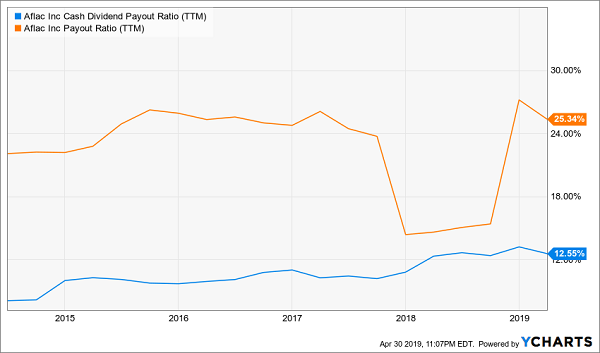

Aflac (AFL) is, and has long been, a reliable dividend stock on that and several other fronts.

Aflac, which we all know from its ubiquitous duck commercials, is a leading provider of supplemental insurance – things such as dental and vision plans, short-term disability insurance and life insurance – serving more than 50 million customers.

The company has been slowly but steadily growing for years, though 2017 earnings spiked thanks to a considerable tax benefit. Analysts see more of the same going forward, with low-single-digit profit-growth estimates for the next couple of years. That’s fine. Aflac is an insurer, not a chipmaker.

That reliable growth has translated into a higher dividend each and every year since 2000. And given payout levels like these, shareholders can count on Aflac continuing to plump up the dividend.

Chemours (CC) is one of the byproducts of years of wheeling and dealing by DuPont … which, following a merger with Dow is now DowDuPont (DWDP) … which recently spun off Dow Inc. (DOW).

That confusing bit of history aside, Chemours–the “performance chemicals” division of DuPont that was spun off in 2015–is pretty straightforward, and really fascinating. For instance, it’s the world’s largest producer of high-quality titanium dioxide, which goes into coatings in automobiles, marine craft and airplanes. It also makes fluor0products such as Teflon, and chemical solutions that cover a wide range of applications, such as acids for semiconductor manufacturing and sodium cyanide production for gold and silver miners.

Chemours’ “performance” isn’t limited to its products. While CC shares had a nasty start in their first year of trading, they’ve exploded by more than 525% off their July 2016 lows, versus 48% returns for the S&P 500 in that time.

The dividend didn’t start to get off the ground until a couple years after the spinoff. What started as a mere 3-cent payout finally took off with a massive jump to 17 cents in 2018, then to 25 cents that same year, where the payout stands today.

Pricing weakness in some of its products have hobbled its performance, and the stock, over the past year, and analysts see earnings weakening this year before returning to 2018 levels in 2020. That’s a lot of sideways movement, which means Chemours would have to inflate its payout ratio to keep up with its red-hot income growth. But considering it distributes just 15% of its net income as dividends … that’s no biggie.

Baconator slinger Wendy’s (WEN) has really come into its own over the past three years.

The House That Dave Thomas Built was only the eighth-biggest fast food chain as of QSR magazine’s August roundup–behind both McDonald’s (MCD) and Restaurant Brands International’s (QSR) Burger King. But it has the happiest shareholders.

While its actual financial results have been up and down for years, they’re generally trending upward, and analysts expect that to continue this year and next. One of the catalysts for 2019 is a less value-focused environment in the fast-food arena, which is tailor-made for Wendy’s more premium positioning compared to the likes of McDonald’s and Yum! Brands’ (YUM) Taco Bell.

Wendy’s also has managed to double its dividend since 2014 to its current dime per share without stretching the purse strings. The company has a lean sub-20% payout ratio and could double the payout again overnight without dropping a bead of sweat.

I obviously don’t expect that, but I do expect the next few Februaries – when Wendy’s announces its payout increases – to be full of fireworks.

7 More Dividend Stocks That’ll Double Your Money Every Few Years

Since inception, my Hidden Yields portfolio has returned 16.3% per year. This means our inaugural subscribers are well on their way to doubling their money with safe dividend stocks! With patience and persistence, you can enjoy the same types of returns by following our dividend double strategy.

Today, I want to share seven of my recession-proof ‘Hidden Yield Stocks’ with you.

My research indicates each of these investments could easily pay you 15% per year. That’s enough to double your money in under 5 years. Imagine, turning a retirement ‘pot’ of $250,000 into $500,000… or… $500,000 into $1,000,000… and on it goes.

Imagine no more fear of your savings running dry… no more worrying about wild market swings or crashes… no more risky-bets on penny-stocks or cryptos… no more penny-pinching in your golden years.

So, if you’re not quite as wealthy as you hoped you’d be… if you wish you had more money in your retirement account… and… if you’re looking for safe, secure growth over the next 5, 10, 15, even 20 years—as well as predictable income—this could be the most important investment advice you ever read.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Much of the income stock universe will report 2019 first quarter results starting on April 28 and running through May 8. Last week there was a 4% to 5% sell-off of many income stocks.

The drop was fueled by some negative Wall Street analyst comments that don’t seem to be well grounded in reality. For many stocks, the quarterly earnings reports are most of the real news upon which long term investors can hang their hats.

I expect that earnings from quality dividend paying companies will positively surprise the market and lead to a reverse of last week’s share price declines.

For long-term, income focused investors, earnings season is a mixed bag. The actual earnings and management comments provide an accurate snapshot of a company’s business and how well they are operating in relation to expectations.

For the stocks I follow, I have a good idea on where the important numbers such as cash flow and dividends should trend. Whether a company remains on or misses the forecast trend determines my recommendation concerning the stock.

The downside to earnings are the games played between Wall Street analyst estimates and the actual earnings result. An earnings “miss” can produce significant share price volatility.

Since the Wall Street crowd changes there expectations frequently, the estimates are of little use for real investment planning. The share price moves you see around the earnings dates are just a game between Wall Street and short term traders.

If you are a longer term investor, sharp share price drops in quality dividend stocks should be viewed as attractive times to buy.

Here are three stocks that have dropped in the weeks before they release earnings and have good potential to exceed market expectation when results are actually announced.

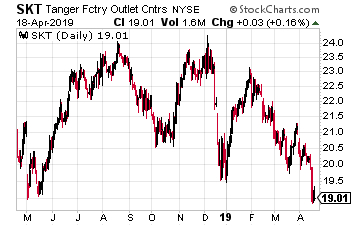

Tanger Factory Outlet Centers (SKT) is real estate investment trust –REIT—that is the only pure play outlet mall company in the larger shopping center REIT sector. The SKT share price has lost 10% of its value over the last few weeks.

Over the last two years, Tanger has struggled with tenant retailers declaring bankruptcy, returning space in the REIT’s malls. Management has been able to keep occupancy high at the cost of not getting historical rental rate growth.

Cash flow per share has been flat and dividend increases in the 1.5% per year range. On the positive side, Tanger has a very conservative balance sheet and a 25 year history of successful business management and dividend growth.

A positive quarterly result could give this stock a solid share price increase. SKT currently yields 7.5%.

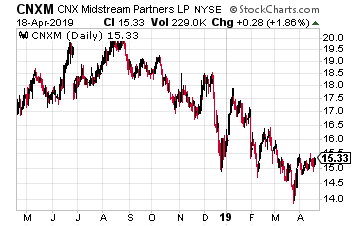

CNX Midstream Partners LP (CNXM) is a growth-oriented master limited partnership –MLP– that owns, operates, and develops gathering and other midstream energy assets to service natural gas production in the Marcellus Shale in Pennsylvania and West Virginia.

While much of the energy infrastructure sector has gone through a painful round of financial restructuring, CNXM has steadily grown its revenues and distributions to investors. The MLP’s small cap status has kept it off the radar of investors.

With a 9% yield and 15% distribution growth, this MLP has a good chance for a nice value pop when earnings come out.

New Residential Investment Corp (NRZ) is a finance REIT whose complicated investment portfolio leaves investors confused concerning the company’s prospects. Thus the 12% yield. Over the last six months New Residential has raised over $1 billion from common stock secondary offerings.

Management has not yet revealed how that capital will be invested. A big investment or merger announcement with earnings could boost the NRZ share price.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments. For more information Click Here.

“Jenny, I can imagine. My wife makes fun of me when I ice my knees after basketball games,” I confided to my friend and favorite bartender.

Her husband, no “young chicken” anymore either she joked, was sore from his own martial arts contest. She bought him a CBD “bath bomb” to help with the aches of being active and middle-aged.

Always the sucker for natural remedies and bartender wisdom, I teed up an Amazon selection for pain and inflammation. Just 26 hours later, I was massaging hemp, turmeric and MSM into my patella tendon (about an hour before tipoff):

BO’s Anti-Inflammatory Pick

“You’re a terrible scientist,” my wife reprimanded me after I bragged about my patella’s comeback in my postgame recap. “You’re supposed to change one variable at a time. You changed everything.”

She was right, of course. I had new basketball shoes and wore a knee brace for the first time in years. I’d changed three variables, had no idea which was the miracle cure. I was left with no choice but to keep my three member “knee team” together! (Who knows how it’s working, as long as it is working, right?)

Hemp has been a popular free agent addition for many aging athletes since its increasing legalization. As you know the crop has other popular uses, too. Mine is more mundane, yet probably fitting for a dividend analyst!

The plant was used in China nearly 5,000 years ago and is enjoying a good old-fashioned American boom thanks to state governments. I live just a few blocks from our neighborhood dispensary yet I wouldn’t have thought to get a doctor’s note for the salve. Put it in on Amazon Prime, though, and it’s in my cart in minutes.

Now what about weed dividends? We’ve had plenty of readers write in asking and, with “pot holiday” April 20 just days away, I thought it’d be fitting for us to review the current crop of dividends.

The Horizons Marijuana Life Sciences Index ETF (HMMJ) just paid its seventh quarterly dividend last Wednesday. Its $0.3811 per share payout is good for a generous 5.1% trailing yield. Plus investors have been as high as a kite since inception, enjoying 160% total returns versus 22% for the S&P 500:

An ETF Contact High

But where exactly do these dividends come from? Most of the stocks the fund holds are not profitable. And the lone dividend payer Scotts Miracle-Gro (SMG) in the fund is only 7.2% of assets.

HMMJ actually makes its money by lending its shares to short sellers. Remember, when you sell a stock “short,” you are actually borrowing shares so that you can sell them at their current market price. Later, you must buy back these shares to “cover” your short position.

Normally it doesn’t cost that much money to short a stock. But the mostly-unprofitable shares that HMMJ holds are in high demand by short sellers today, and the ETF itself holds much of the supply. So, the fund’s “side hustle” of renting out its holdings is booming.

But there is no actual cash flow backing up its distribution. Nor is there any guarantee that its “short lending” business will remain as robust in future quarters. To paraphrase Prince, this distribution is just a party and parties weren’t meant to last.

How about Scotts, which does manufacture actual products? It’s more of a “pick and shovel” play on weed. The company doesn’t peddle the crop directly but sells growing equipment. Scotts stock pays 2.7% today and, while the firm raises its dividend regularly to the tune of about 5% per year.

As much hype as there is around weed, the power of the “dividend magnet”—the gravity exerted by a payout on its stock price—is even stronger. While Scotts has hiked its dividend by 17% over the last three years, its stock price has risen by the exact same amount:

The All-Powerful Dividend Magnet

The firm’s subsidiary for cannabis growers has, troublingly, not been growing organically. It’s been more hype than hemp to date for this baked maker of lawn and garden products.

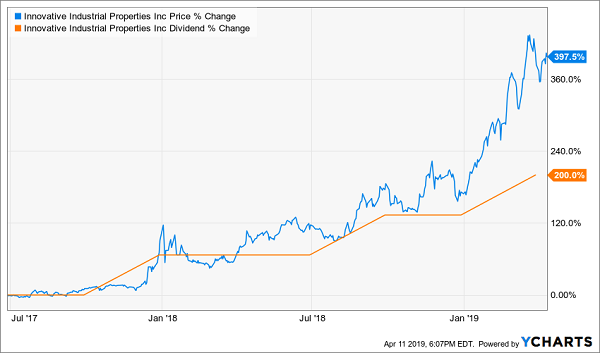

A better backdoor play on the sector is landlord Innovative Industrial Properties (IIPR). Remember, while many states have legalized pot, it remains illegal under federal law. Financing is challenging for weed peddlers, so many sell their properties to IIPR to get cash in the door for their operations. The firms then rent their former buildings back from IIPR.

Why IIPR? It’s the only real estate investment trust (REIT) that works with weed growers. As a publicly traded company, it gets to borrow money at much lower rates than it collects from its cannabis clients. As a REIT, IIPR is obligated to dish most of its profits back to its shareholders as dividends. The result is a good old-fashioned payout boom, a 200% increase in less than two years:

The Landlord’s High

The only “problem” with the chart above is that, if you don’t yet own IIRP, it is now quite expensive to do so. Its price line has run away from its payout line, which is a sign that shares are dangerously overvalued. The stock now pays just 2.1% and trades for an extremely rich 31-times its annual cash flow.

Sure, you may be able to buy IIRP “high” and sell it higher. But that’s a different dividend drug altogether.

Forget dividends you say? Let’s not forget the example that money-losing, no-dividend firm India Globalization Capital (IGC) set for us. IGC found the magic investor formula when they put two investing buzzwords side-by-side:

Cannabis, and

Blockchain.

The savvy marketers at IGC then introduced an energy drink infused with hemp, and wow, what a rush!

We level-headed contrarians should stay away from this circus. In fact, you need to be honest with yourself about the latest weed craze. If you’re tempted at all to buy this junk, it’s better if you change the channel.

Many marketers know that you and your peers are fixating on these parabolic charts. It’s going to end in tears, but they don’t care. They know they can get your attention now with a weed-fueled promise of 100% to 1,000%+ gains and get out while the getting is good.

The epilogue on IGC? Tears would be putting it mildly:

IPC’s Fast Rise and Fall

One of the smartest investors I know is a sweet grandma. She’d never fall for this speculative stuff! Grandma has a modest $387,000 nest egg that is on pace to last forever. No joke.

Recently I was chatting with a reader of mine who manages money for a select group of clients. He’s using my 8% Monthly Payer Portfolio to make a client’s modest savings – a nice grandmother with $387,000 – last longer than she ever dreamed:

“She brought me $387,000,” he said. “And wants to take out $3,000 per month for ten years.”

“Well she’s already withdrawn money for eight months (at $3,000 per month) and her balance has actually grown to $397,000. If the portfolio continues yielding 7% per year plus 2% per year in capital gains, and she withdraws $3,000 per month, it will pay my fees and still last her 27 years!”

Now many retirement experts pitch real estate as the best way to bank monthly income. But this grandma isn’t hustling to collect rent checks, or fix broken light bulbs. She’s simply collecting her “dividend pension” every month, which is 100% funded by her stocks and funds.

Actually her monthly salary is more than 100% financed – which is why her portfolio has grown by $10,000 as she’s withdrawn $3,000 per month.

I’m ready to give you everything you need to know about this life-changing portfolio now. Let’s talk about Grandma’s secret – her 8% monthly dividend superstars (which even have 10% price upside to boot!)

Grandma focuses on the 12 monthly payers in my “8% Monthly Payer Portfolio.” If you’ve got a bit more than she does–say $500,000 invested–it’ll hand you a rock-solid $40,000-a-year income stream. That’s an 8% dividend yield … and it’s easily enough for most folks to retire on.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it! Of the 19 income studs in this unique portfolio, 12 pay dividends monthly, so you can look forward to the steady stream of $3,333 in income, month in and month out—give or take a couple hundred bucks – on every $500K in capital you’re able to invest.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!