The domestic stock market averages started April on a positive note and on Thursday, the S&P 500 index achieved its longest winning streak in over a year.

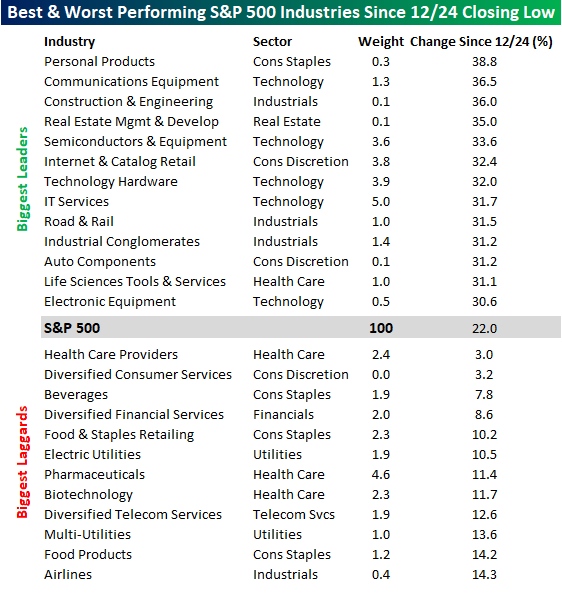

Taking a bit further look back, Bespoke Investment Group noted this week that it’s now been 100 days since the major U.S. indexes bottomed in late December. Highlighted in the following table, Industrial and Technology names have led the average 22% gain in the S&P 500 since then, while healthcare stocks have lagged.

Source: Bespoke Investment Group

Full Slate of Economic News

In overseas news this week, Theresa May suffered yet another defeat in Parliament, regarding the Brexit process. As a result, May finally proposed conceding to a strategy that could result in the UK pursuing a “softer” exit from the European Union.

Elsewhere, President Trump met with China’s Vice Premier Liu in Washington on Thursday. Earlier in the week, two separate reports of China’s manufacturing purchasing managers’ index confirmed that the economy returned to a state of expansion in March.

Back in the U.S., the March jobs report came in slightly ahead of expectations on Friday. The economy added 196,000 non-farm payrolls last month and numbers from the past two months were also revised higher by 14,000 jobs.

Looking ahead to next week, we’ll get a look at inflation measures for both consumer and producer prices in the U.S. In addition, the minutes from the latest FOMC meeting will be released on April 10.

Q1 Earnings Could Decline

Walgreens Boots Alliance (WBA) was a big earnings-related loser this week, falling 12% a day after disappointing investors with forward guidance.

Once again, earnings season is just around the corner, with activity set to pick up the week of April 22. In the meantime, the companies below are scheduled to headline the reporting calendar next week:

| Date | Company | Exp. EPS |

| 4/10 | Delta Air Lines (DAL) | $0.91 |

| 4/12 | JP Morgan Chase (JPM) | $2.36 |

| 4/12 | Wells Fargo (WFC) | $1.11 |

According to Factset, S&P 500 earnings are expected to decline 3.9% in the first quarter of 2019, down from expectations for 2.9% growth at the beginning of the year. Even though actual profits have historically exceeded expectations, the final result will likely be a far cry from the double-digit growth posted in each of the four quarters of 2018.

Stocks are up 22% over the past 100 days, but we’re staring at a potential earnings recession in the first quarter of 2019.

At times like this, a key question we usually hear is: “what’s still worth buying now?”

It’s important for investors to remember that whether stocks are up or down, the market always places a premium on growth.

A stable dividend of 5% or more is nice, but what investors really need to build wealth over time, is a dividend that management continues to raise year in and year out.

It may sound too good to be true, because growth investors and income investors don’t usually see eye to eye.

Income seekers want the security of 5%-plus annual dividend yields, while growth hounds think that cash should be reinvested back into the business– because a solid earnings report can send a stock up that much in one day.

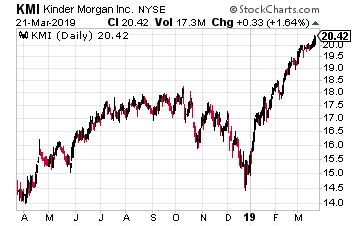

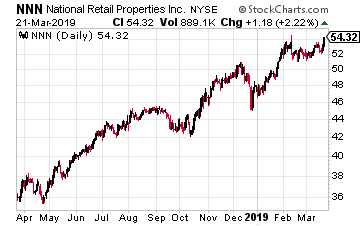

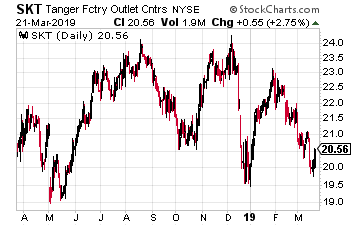

We’re here to tell you it’s possible to have the best of both investing worlds, and my colleague Brett Owens can show you how, with his simple (and safe) way to earn 12% a year from stocks with “hidden yields”.

At that rate, your money will double every six years, plus you can triple the retirement income that most dividend aristocrats or “safe” fixed income investments currently offer.

How do we accomplish this? Brett has discovered a key relationship between dividends and price gains that allow investors to find both growth and income in “hidden yields”.

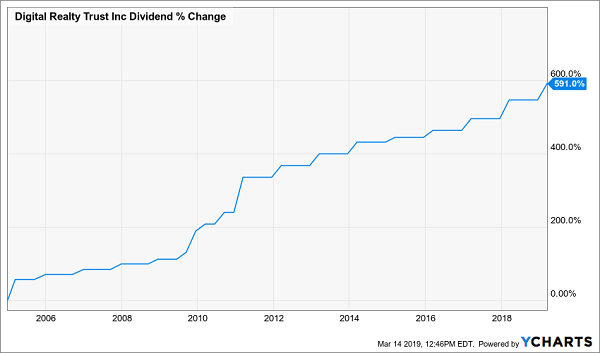

Companies that consistently grow their dividends over time tend to outperform. The trick is the best dividend stocks almost never show high yields, because stock gains tends to track the size of dividend increases. If a company increases its dividend by 10% and the higher yield brings new buyers in, it often will send the price up and the yield back down toward where it started.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Source: Contrarian Outlook