When the average investor considers an all-cap ETF or mutual fund, it’s usually filled with large-cap stocks to buy with very little consideration for smaller companies despite the fact that small- and mid-cap stocks often deliver periods of excellent performance when large caps aren’t delivering the goods.

The point of an all-cap portfolio, as I see it, is to own a collection of stocks that represent companies of various sizes both large and small. Personally, in my experience, an all-cap portfolio equally weighted with large-, mid-, small- and micro-cap stocks tend to do better like a sports team than one that’s weighted to larger companies whose growth is generally slower.

However, many investors would be hesitant to include such a heavy weighting in stocks of less than $300 million in market cap so most all-cap ETFs and mutual funds tend to be large caps with a small helping of mid-caps.

These are the 10 stocks to buy for the perfect all-cap portfolio.

Large-Cap Stocks to Buy: Apple (AAPL)

Source: Shutterstock

In the past, I’ve mentioned Howard Lindzon in articles I’m discussing because I love the way he thinks about investing. One of his recent newsletter posts discussed how Apple Inc.(NASDAQ:AAPL) isn’t one of the sexiest or most exciting stocks he owns but he’s keeping it for now.

As large-cap stocks go, you can get no bigger. It’s the largest publicly traded company in the world. Apple might not be innovating at the pace it once did, but it’s still delivering great products that do what they’re supposed to.

Except, Lindzon also pointed me to a review of Apple’s AirPods that suggests it still knows a thing or two about designing products customers want.

“Apple’s AirPods design, which I initially ridiculed, is actually the best and most functional one available for truly wireless buds today,” wrote Vlad Savov in The Verge March 19. “Because Apple moved the Bluetooth electronics and batteries to the stem, it was able to use the full cavity of each bud for sound reproduction. That’s how the AirPods reproduce a wider soundstage than most Bluetooth earbuds without being any thicker or protruding from the ear.”

It’s something when you can take a big-time audiophile like Savov is reputed to be and turn his opinion 180 degrees from negative to positive.

So, before you give up on AAPL stock, remember that it has plenty of cash to continue developing products consumers enjoy. You can’t put a price on that.

Large-Cap Stocks to Buy: Berkshire Hathaway (BRK)

Source: Shutterstock

Not quite as big a large cap as Apple, Berkshire Hathaway Inc. (NYSE:BRK.A, NYSE:BRK.B) probably has the best-known CEO of any S&P 500 company.

Who hasn’t heard of Warren Buffett?

Famously honest with his shareholders, I wouldn’t be surprised if ethics professors studied Buffett’s annual letters to shareholders. They’re classic re-tellings of the year that just was — the happenings both good and bad.

I recently highlighted what I thought was the best quote from the 2017 letter.

“In our search for new stand-alone businesses, the key qualities we seek are durable competitive strengths; able and high-grade management; good returns on the net tangible assets required to operate the business; opportunities for internal growth at attractive returns; and, finally, a sensible purchase price,” stated Buffett on page four of the 2017 letter. “That last requirement proved a barrier to virtually all deals we reviewed in 2017, as prices for decent, but far from spectacular, businesses hit an all-time high.”

Buffett’s not perfect.

His stubborn support for Wells Fargo & Co (NYSE:WFC), a bank that faces up to $1 billion in fines from the Consumer Financial Protection Bureau for auto insurance and mortgage lending abuses, is a bit mystifying, but when you have the kind of assets Berkshire Hathaway has, it’s easier to be patient.

Personally, if you only could own two stocks, I’d recommend Apple and Berkshire Hathaway.

Large-Cap Stocks to Buy: JD.Com (JD)

A few months ago, I wrote an article about JD.Com Inc (ADR) (NASDAQ:JD) suggesting that regarding value, JD stock was unquestionably a better buy than Alibaba Group Holding Ltd(NYSE:BABA).

Since that time, both stocks have flatlined. While I like what Jack Ma’s done at Alibaba, I see what JD.com CEO Richard Liu is doing to build a global supply chain and can’t help think that is going to be the difference between success and failure for the company as it expands outside China.

I also see it growing faster than Jeff Bezos’s company did at the same time in its corporate history; I consider the risk to reward to be incredibly attractive.

Sure, it’s the riskiest of the large-cap stocks mentioned here, but JD.com also has the most upside.

Large-Cap Stocks to Buy: Royal Caribbean (RCL)

Source: Shutterstock

The other day I happened to read an article about Symphony of the Seas, the world’s largest cruise ship that Royal Caribbean Cruises Ltd (NYSE:RCL) just launched. It’s a fascinating story of how cruise ships became the ultimate in modern hospitality and entertainment.

Since my wife and I got married on Majesty of the Seas in February 2005, one of RCL’s smaller, older ships, I’ve been fascinated by the cruising experience although we’ve never been on one since. I love the idea of visiting some ports without having to pack and unpack several times during a vacation. I suppose that’s why people also love motorhomes.

Anyway, CEO Richard Fain’s been the head of the cruise line since 1988, which is a long time to be in charge of any organization these days, but especially so at one built on the necessity of change.

His tenure is amazing.

Interestingly, millennials are said to like cruising more than boomers or Gen Xers, which means Fain might have to stick around for another 30 years to get the company through the changes bound to come down the pike.

I see smooth sailing ahead for RCL stock.

Mid-Cap Stocks to Buy: Gildan (GIL)

Source: Shutterstock

If you love investing in dividend stocks, Gildan Activewear Inc. (NYSE:GIL) ought to have your attention, because the Montreal-based maker of t-shirts and underwear does a good job growing its annual dividend payment.

On April 4, I identified as a company increasing its annual dividend payment by double digits. It raised its quarterly dividend Feb. 22 by 20% to $0.112-a-share, the sixth consecutive year to raise its annual dividend by 20%.

Seven years ago, it paid an annual dividend of $0.11-a-share. Today, that’s up to $0.45-a-share. In that time, revenues have increased by a billion dollars to $2.8 billion, while operating income has almost doubled from $239 million to $424 million in 2017.

Down more than 8% year-to-date, you’re getting GIL at prices near its 52-week low.

Mid-Cap Stocks to Buy: Axalta Coatings (AXTA)

Source: Shutterstock

I was going to recommend Wabco Holdings Inc. (NYSE:WBC) as one of my three mid-cap stocks because I remember Warren Buffett owning it for the longest time. However, he sold off the last of the company’s shares in the second quarter of 2017.

Instead, I noticed Berkshire Hathaway owns a little more than 23 million shares of Axalta Coating Systems Ltd. (NYSE:AXTA), which the company has owned since it bought most of them in a private deal in 2015 for $28 a share. Now finally making money on his investment, it’s possible that Buffett, as the largest shareholder, could buy the entire company to combine with its Benjamin Moore paint business.

Axalta’s fourth-quarter results were an improvement over the previous quarter providing a ray of hope for the manufacturer of performance coatings for commercial applications including vehicles and building facades to prevent corrosion.

“Axalta’s fourth quarter demonstrated a return to solid growth following our more challenged third quarter result, with net sales and Adjusted EBITDA performance both at or above our revised guidance ranges,” said Charles W. Shaver, Axalta’s Chairman and Chief Executive Officer Feb. 6. “Our stated expectation of improved financial performance beginning in the fourth quarter was met and was supported by the broad-based market strength and sound execution by our business teams.”

If Buffett didn’t own Axalta, I’d be less interested, but he does, and so I am.

Mid-Cap Stocks to Buy: Nordstrom (JWN)

Source: Shutterstock

Investors were disappointed March 20 by news from the special committee advising the Nordstrom, Inc. (NYSE:JWN) board that the Nordstrom family couldn’t pull together a decent deal to acquire the company they founded and still run.

Although it hasn’t been a good time for most department stores in the past three years, Nordstrom’s stock has held up slightly better than its peers over this period, who’ve seen annual losses of close to 13%.

Although the door has closed on the Nordstrom family buying its namesake, the company continues to push on with its future plans. In March, it announced that it had acquired two small tech companies — BevyUp and MessageYes — whose technology allows retail employees to keep in contact with customers when not in the store.

Nordstrom has always been about the customer experience; these two acquisitions will help it maintain its leadership position in this very important part of retailing.

And let’s not forget, Nordstrom generated record revenue of $15.1 billion in fiscal 2017, while also increasing EBIT profits by 15% to almost $1 billion. Department stores might be suffering more than usual but Nordstrom’s not exactly ready for the bargain bin just yet.

Up year-to-date by 2%, I expect the company’s Rack and e-commerce businesses to make up for any softness in the full-line stores.

Small-Cap Stocks to Buy: Callaway Golf (ELY)

Source: Shutterstock

The Masters just finished up for another year delivering an exciting finish that saw Patrick Reed fend off Ricky Fowler by one stroke and the hard-charging Jordan Spieth by two.

Golf is getting exciting again and not just because Tiger Woods is starting to make some competitive noise. Parents are starting to come to the conclusion that violent sports such as football aren’t healthy for their children’s long-term cognitive skills and are pushing them into sports like golf and swimming.

A quick look at a five-year chart of Callaway Golf Co (NYSE:ELY) shows a gradual improvement that’s taken the stock from less than $7 in 2013 to almost $17 today. Up 21% year-to-date through April 6, a lot of that has to do with its improving financials.

In 2017, Callaway grew operating income by 78% to $79 million on revenue of $1.05 billion, itself a 20% increase over last year.

In December, I suggested that Callaway would produce a four straight year of positive returns. Although it’s early, my prediction is looking pretty good.

In my opinion, ELY is a small-cap stock to own beyond 2018.

Small-Cap Stocks to Buy: Restoration Hardware (RH)

Restoration Hardware Holdings, Inc (NYSE:RH) has got to be one of the most mercurial small-cap stocks trading on a U.S. exchange. It’s up and down by major chunks at a time — most recently, it jumped more than 20% after announcing better than expected Q4 2017 earnings — as investors try to figure out whether its move into higher-end furniture and interior design will generate sustainable earnings.

Well, if the fourth quarter is any indication, it will and it can.

The company announced $1.05 a share in Q4 2017 adjusted earnings, 46 cents higher than analysts were expecting. The retailer is doing better as a result of its move to a club membership where customers pay $100 per year to get 25% off everything sold in the store including interior design services.

In its earnings press release, CEO Gary Friedman stated that 95% of its revenue comes from members. Its move from a promotional business model to that of a club has delivered higher profits and free cash flow from lower inventory.

Not only that, but its first three stores with restaurants in Chicago, Toronto and West Palm Beach are all performing well above expectations generating significant traffic for the stores themselves. The West Palm restaurant is expected to generate $7 million in 2018, a huge number.

As InvestorPlace contributor Vince Martin recently suggested, RH shorts got caught in a short-squeeze of epic proportions. Long-term, I think this model makes a lot of sense. I said as much in 2016; nothing has changed in my opinion.

Micro-Cap Stocks to Buy: Red Lion Hotels (RLH)

Source: Shutterstock

Once upon a time, I wrote about micro-cap stocks more frequently; I found them to be a great addition to the typical portfolio filled with large-cap and mid-cap stocks. Today, micro-cap stocks (market cap less than $300 million) seem so foreign to me.

Of the 47 micro-cap stocks I found that had a PEG ratio higher than 1 and trading at less than 20 times operating cash flow, Red Lion Hotels Corporation (NYSE:RLH) appears to be the best bet to fill out my all-cap portfolio.

The Colorado hotel franchiser recently purchased the Knights Inn brand of hotels from Wyndham Worldwide Corporation (NYSE:WYN) for $27 million. The deal gives Red Lion 350 additional properties and brings the total number of hotels it operates to almost 1,500 in the U.S. and Canada.

As a result of the purchase, Red Lion becomes one of the top 10 hotel franchisers in the world. Like many hotel companies these days, it runs an asset-light business model.

In 2017, RLH generated $172 million in revenue and operating income of $1.1 million, a significant improvement from 2016. The acquisition of the Knights Inn brand will continue to improve the top- and bottom-line.

Red Lion Hotels flies under the radar of most investors. You might want to check this hotel stock out a little closer.

Get up to 14 dividend paychecks per month from safe, reliable stocks with The Monthly Dividend Paycheck Calendar, an easy-to-use system that shows you which dividend stocks to pick, when to buy them, when you get paid your dividends, and how much. All you have to do is buy the stocks you like and tell them where to send your dividend payments.

For more information Click Here.Source:

Investor Place

So how can you invest in water? The broadest way is through an exchange traded fund. There are five such ETFs that are available to you. The one I like the most is the former Guggenheim S&P Global Water Index ETF, which is now controlled by Invesco and is called the PowerShares S&P Global Water Index Portfolio (NYSE: CGW).

So how can you invest in water? The broadest way is through an exchange traded fund. There are five such ETFs that are available to you. The one I like the most is the former Guggenheim S&P Global Water Index ETF, which is now controlled by Invesco and is called the PowerShares S&P Global Water Index Portfolio (NYSE: CGW).

The oil companies that seem to have begun the process of adapting to a lower carbon economy are located across the pond in Europe. These include Royal Dutch Shell PLC (NYSE: RDS.A and NYSE: RDS.B), Total SA (NYSE: TOT) as well as the aforementioned BP. Both Shell and Total, for example, have invested heavily into natural gas as a cleaner alternative to coal for power generation.

The oil companies that seem to have begun the process of adapting to a lower carbon economy are located across the pond in Europe. These include Royal Dutch Shell PLC (NYSE: RDS.A and NYSE: RDS.B), Total SA (NYSE: TOT) as well as the aforementioned BP. Both Shell and Total, for example, have invested heavily into natural gas as a cleaner alternative to coal for power generation.

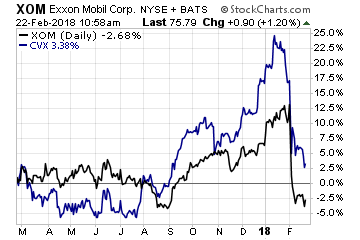

Yet the two U.S. giants – ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) – have largely not followed their European peers into other forms of energy besides oil. They seem content being dinosaurs drawing jeers from climate activists.

Yet the two U.S. giants – ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) – have largely not followed their European peers into other forms of energy besides oil. They seem content being dinosaurs drawing jeers from climate activists.

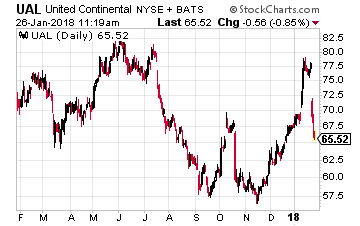

Based on the recent earnings call from United Continental Holdings (NYSE: UAL), it looks like another airfare price war is just around the corner.

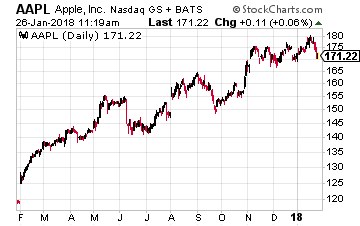

Based on the recent earnings call from United Continental Holdings (NYSE: UAL), it looks like another airfare price war is just around the corner. Apple (Nasdaq: AAPL) garnered a lot of headlines recently when it said it would make a one-off $38 billion tax payment on the repatriation of some of its overseas profits. That led to speculation by the Trump Administration and others about how other technology companies would follow Apple’s lead.

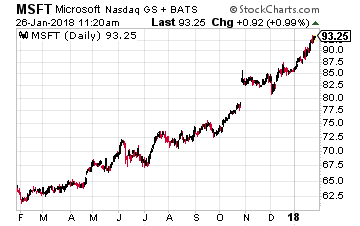

Apple (Nasdaq: AAPL) garnered a lot of headlines recently when it said it would make a one-off $38 billion tax payment on the repatriation of some of its overseas profits. That led to speculation by the Trump Administration and others about how other technology companies would follow Apple’s lead. One prime example is Microsoft (Nasdaq: MSFT). In early December, its stock was down to $81 over worries about the tax bill. Now it is over $92 a share and still climbing. There are lots of reasons why, but I’m sure Wall Street has by now realized the new tax law won’t hurt Microsoft. Again, never make an investment decision solely on something like taxes.

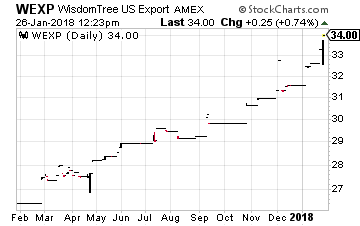

One prime example is Microsoft (Nasdaq: MSFT). In early December, its stock was down to $81 over worries about the tax bill. Now it is over $92 a share and still climbing. There are lots of reasons why, but I’m sure Wall Street has by now realized the new tax law won’t hurt Microsoft. Again, never make an investment decision solely on something like taxes. One other investment for you to consider is the WisdomTree U.S. Export and Multinational Fund (NYSE: WEXP). It is filled with blue-chip U.S. multinationals such as Microsoft, Boeing, Johnson & Johnson, Apple and Alphabet.

One other investment for you to consider is the WisdomTree U.S. Export and Multinational Fund (NYSE: WEXP). It is filled with blue-chip U.S. multinationals such as Microsoft, Boeing, Johnson & Johnson, Apple and Alphabet.

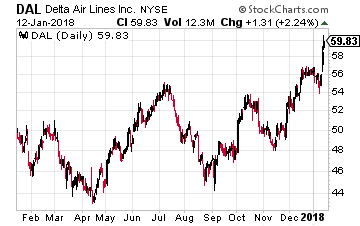

Take Delta Air Lines (NYSE: DAL), for example. Just last week it said that the tax cut will boost its earnings by about $800 million a year. That translates to about $1 per share in increased earnings for 2018. Delta management raised their earnings per share guidance for 2018 to a range of $6.35 to $6.70, up 20% to 30% from the year earlier level.

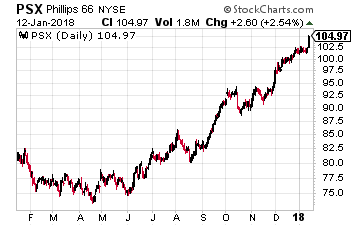

Take Delta Air Lines (NYSE: DAL), for example. Just last week it said that the tax cut will boost its earnings by about $800 million a year. That translates to about $1 per share in increased earnings for 2018. Delta management raised their earnings per share guidance for 2018 to a range of $6.35 to $6.70, up 20% to 30% from the year earlier level. And it’s not just the big oil firms to benefit. The oil refining segment should really get a major boost. The largest company in the segment, by market capitalization, Phillips 66 (NYSE: PSX), will receive a 16% boost to 2018 earnings according to an estimate from Piper Jaffray’s Simmons & Company energy investment bank unit.

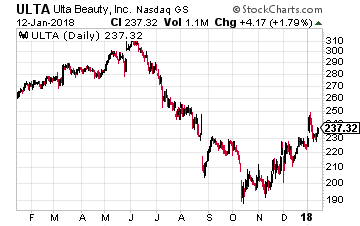

And it’s not just the big oil firms to benefit. The oil refining segment should really get a major boost. The largest company in the segment, by market capitalization, Phillips 66 (NYSE: PSX), will receive a 16% boost to 2018 earnings according to an estimate from Piper Jaffray’s Simmons & Company energy investment bank unit. One of my favorites in the sector is Ulta Beauty (Nasdaq: ULTA), which operates 1,058 stores and generated $4.8 billion in revenues in 2016. It should get a double boost – not only from the tax cut itself, but from consumers with a little extra in their pocket spending on simple luxuries like makeup, lip gloss, etc. Perhaps that’s why the stock is already up over 6% year-to-date.

One of my favorites in the sector is Ulta Beauty (Nasdaq: ULTA), which operates 1,058 stores and generated $4.8 billion in revenues in 2016. It should get a double boost – not only from the tax cut itself, but from consumers with a little extra in their pocket spending on simple luxuries like makeup, lip gloss, etc. Perhaps that’s why the stock is already up over 6% year-to-date.

Let me start by talking about a company that was unavoidable at this year’s CES – Nvidia (Nasdaq: NVDA). Their graphics processing units (GPUs) are at the core of many machine learning and artificial intelligence solutions, including for automobiles.

Let me start by talking about a company that was unavoidable at this year’s CES – Nvidia (Nasdaq: NVDA). Their graphics processing units (GPUs) are at the core of many machine learning and artificial intelligence solutions, including for automobiles. A company to consider is Visteon (NYSE: VC), which designs and manufactures electronics products for automakers. Visteon provides everything from standard gauges to high resolution, reconfigurable digital 2D and 3D displays to infotainment and audio systems.

A company to consider is Visteon (NYSE: VC), which designs and manufactures electronics products for automakers. Visteon provides everything from standard gauges to high resolution, reconfigurable digital 2D and 3D displays to infotainment and audio systems.

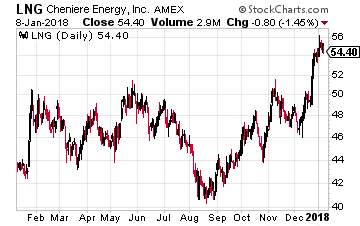

Primary among U.S. LNG exporters is Cheniere Energy (NYSE: LNG), which is the owner of the first LNG export terminal in the U.S. that has been operating since early 2016. It is exporting at its Sabine Pass facility with three trains and a capacity of about two billion cubic feet of gas per day. Its total capacity is expected to be about five billion cubic feet per day once all five trains are completed (the fourth train was recently completed). An LNG train is a liquified natural gas plant’s liquefaction and purification facility.

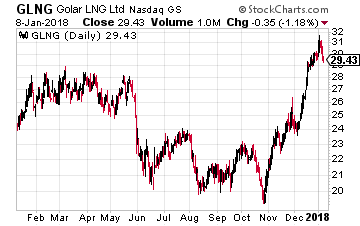

Primary among U.S. LNG exporters is Cheniere Energy (NYSE: LNG), which is the owner of the first LNG export terminal in the U.S. that has been operating since early 2016. It is exporting at its Sabine Pass facility with three trains and a capacity of about two billion cubic feet of gas per day. Its total capacity is expected to be about five billion cubic feet per day once all five trains are completed (the fourth train was recently completed). An LNG train is a liquified natural gas plant’s liquefaction and purification facility. Golar LNG (Nasdaq: GLNG) – its stock is up nearly 20% over the past year. The company is one of the world’s largest independent owners and operators of marine-based LNG midstream infrastructure and is involved in the liquefaction, transportation and regasification of natural gas.

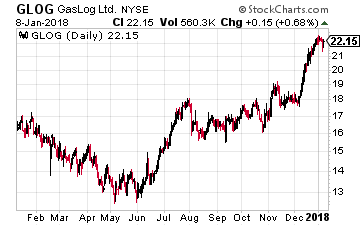

Golar LNG (Nasdaq: GLNG) – its stock is up nearly 20% over the past year. The company is one of the world’s largest independent owners and operators of marine-based LNG midstream infrastructure and is involved in the liquefaction, transportation and regasification of natural gas. If you are looking at more of a pure-play LNG shipper, there is Gaslog Ltd. (NYSE: GLOG), whose stock is up nearly 30% over the last year, with most that gain occurring in the last three months.

If you are looking at more of a pure-play LNG shipper, there is Gaslog Ltd. (NYSE: GLOG), whose stock is up nearly 30% over the last year, with most that gain occurring in the last three months.{kind=link}