We are now rolling into the second quarter of 2018. So far this year the markets have been undeniably jumpy. Just last week global markets posted sharp losses as talk of a trade war continues to spook investors. But for the stocks listed below 2018 hasn’t been so bad at all.

In fact, it’s been something of a blessing. Bearing in mind the recent turbulence, all these stocks have defied the market and posted exceptional first-quarter gains. Here we dive in and take a closer look at the best-performing stock from each sector and what has prompted these out-sized movements.

Some are obvious picks — Netflix, Inc. (NASDAQ:NFLX) for example — while others slide in relatively under the radar; Whiting Petroleum Corporation (NYSE:WLL) anyone? But the crucial question is: Are these stocks capable of recording similar high-growth levels in the coming months?

Using TipRanks we can see both the overall Street take on each stock’s outlook and specific insights from the Street’s top analysts. And if the stock isn’t looking so promising for the next quarter, I suggest a better stock pick to boost your 2018 portfolio. Ready? Let’s take a closer look:

Best Sector Stocks Through Q2: Healthcare: TG Therapeutics (TGTX)

Sector: Biotech

Shares in TG Therapeutics, Inc. (NASDAQ:TGTX) have exploded by a whopping 76% over the last three months. This innovative biotech is focused on developing novel treatments for devastating blood cancers and autoimmune diseases.

“We believe TG is generating a complete B-cell therapy franchise that is unique in the oncology space, which could provide substantial value across various B-cell cancers” cheers B.Riley FBR’s Madhu Kumar. He selects TGTX as an Out the Gate 2018 Pick, due to his “reasonable confidence in success in the Phase III UNITY-CLL trial, with interim data expected in 2Q18.”

For investors looking for some serious upside potential, five-star HC Wainwright analyst Edward White sees the stock spiking to $38 (154% upside potential). He reiterated his buy rating on March 21. White bases his valuation on the potential revenue and success of the company’s two main drugs ublituximab and umbralisib. Combined, he is projecting very promising 2026 revenue for these drugs of $990 million.

Bear in mind that so far White has struck gold with his TGTX recommendations. Across his 20 TGTX ratings he scores an 85% success rate and 38.3% average return.

Overall four analysts have published recent buy ratings on TGTX. No “hold” or “sell” ratings here. And with an average analyst price target of $27.50, on average analysts are predicting huge upside potential of over 80%. Conclusion: for risk-tolerant investors, this top stock still seems like a bargain!

Best Sector Stocks Through Q2: Twilio (TWLO)

Sector: Tech

Cloud communications platform Twilio Inc. (NYSE:TWLO) is no stranger to volatility. After going public in June 2016 at $15/share, prices surged to $71. But a 7-million secondary share offering saw the stock plummet just as fast. And on the shock loss of major customer Uber, shares sunk to just $23.

Now TWLO is on a roll again. In the last three months, prices have climbed almost 61% to $40. So what does all this mean? Will this bumpy ride continue? Well word on the Street is decidedly bullish. Analysts are excited about the recent unveiling of Twilio Flex, a programmable contact center vertical that is poised to become a major new platform for Twilio.

Following Twilio’s strong 4Q17 results, Oppenheimer analyst Ittai Kidron takes a deep dive into the company’s growth metrics. Even though sentiment is improving, the stock’s long-term potential is still underappreciated.

Kidron explains: “We believe that (1) expectations still underestimate Twilio’s growth potential; (2) expansion into traditional enterprise is showing early signs of success and offers a long runway ahead; (3) gross margin is likely to bottom in 1Q18 and has the potential to recover thereafter; and (4) Twilio continues to outperform the competition.”

In total, this ‘Strong Buy’ stock boasts 7 recent buy ratings vs 3 hold ratings. On average these analysts see just 5% upside potential from current levels. However, on the high-end Drexel Hamilton’s $47 price target from Brian White suggests much more appealing upside of almost 18%.

Best Sector Stocks Through Q2: Bofl Holding (BOFI)

Sector: Financials

Internet-based Bofl Holding, Inc. (NASDAQ:BOFI) is proof that banks don’t need physical branches to succeed. Over the last five years, BOFI has posted life-changing returns 344%. Even in the last quarter shares climbed 35% to $39.45 due to better-than-expected earnings results.

For top B.Riley FBR analyst Steve Moss this is a top-notch stock with multiple positives. We are looking at “a quality franchise with clean credit, solid loan growth, ample capital, and strong profitability.” However, bearing in mind the stock’s sharp gains, he removes BOFI from his Alpha Generator list. He notes a “significant narrowing of its valuation relative to peers.”

Nonetheless, his report ends on a bullish note with a price target ramp from $42 to $45 (14% upside potential). Moss puts the move down to ‘increased confidence’ in estimates following H&R Block‘s (NYSE:HRB) disclosure of $1.07 billion in refund anticipation loans. Indeed this is the first year BofI is the exclusive provider of HRB’s refund anticipation loans giving the company huge cross-selling potential.

In total, this Strong Buy stock has recorded 3 recent buy ratings vs just 1 hold rating. Meanwhile the $43.25 average analyst price target indicates upside potential of just under 10%.

Best Sector Stocks Through Q2: Fossil Group (FOSL)

Sector: Consumer

Is Fossil Group, Inc. (NASDAQ:FOSL) making a comeback? The fashion watch and accessories maker jumped nearly 67% in Q1 on a resound Q4 earnings beat. Specifically, FOSL reported earnings of 64 cents per share, topping analysts’ expectations of 40 cents per share. In addition, revenue came in at $920.8 million, ahead of Wall Street’s estimate of $890 million.

However, don’t bring the champagne out just yet. Top Oppenheimer analyst Anna Andreeva is going into party-pooper mode. She reiterates a Perform rating on FOSL shares as: “On the surface, FOSL appears to be playing better defense” but wearables growth is moderating, and even traditional watches are resetting lower with partners managing inventories down.

She concludes that the: “Stock is heavily shorted and is up big AMC on covering; net/net, in our view, not much has changed fundamentally: sales guided down sharply for 1Q18, profitability improvement aided by financial fixes as underlying trend is still negative.”

If we take a step back, we can see that Wall Street is not rooting for FOSL stock’s success. Based on 4 recent analyst ratings, TipRanks analytics exhibit FOSL as a Hold. However- boosted by the 1 bullish rating- the average analyst price target of $15 indicates 24% upside potential.

A far better investment proposition in the consumer good sector is semiconductor stock Lam Research (NASDAQ:LRCX). As the memory chip industry goes from strength to strength this stock is flourishing right now. With 32% upside potential and 14 recent “buy” ratings this is a stellar company I highly recommend checking out.

Best Sector Stocks Through Q2: Netflix (NFLX)

Sector: Services

Streaming giant Netflix, Inc. (NASDAQ:NFLX) has popped over 56% in Q1 to an all-time-high. Now NLFX is worth approx. 130 billion, just short of Disney’s $150 billion. Of course, at these levels, we need to ask: how sustainable are these gains, and where can the stock price go now? And here the Street is- not surprisingly- divided. Let’s take a look:

On the one hand we have Pivotal analyst Jeffrey Wlodarczak. He is out with a bullish research note on NFLX after conducting thorough country by country research. The analyst’s verdict? “As long as NFLX continues to beat and raise on subscribers we believe the stock will continue to work.” Indeed, his $400 price target suggests big upside potential of 32%.

Long term international subscribers are looking better than ever, with Wlodarczak now angling for 250 million international subscribers by 2024. Netflix is even finally showing traction in Japan with upward trends detected across Asia as a whole. Following Netflix’s fourth quarter print, “the market appeared to effectively give NFLX management carte blanche to spend aggressively to drive healthy subscriber growth” highlights Wlodarczak.

Top Loop Capital Markets analyst Alan Gould is more restrained. Yes Netflix has an “unstoppable lead” in the US streaming TV business but ultimately: “with the stock up 66 percent in the first 11 weeks of the year, we find it hard to justify a bullish rating.” Even so, his Hold rating comes with a $325 price target indicating 8% upside potential.

Overall, the stock has a mixed bag of ratings. We can see that the price target average for the last three months indicates downside potential. But crucially the average price target from ratings over just the last month comes out at $348. So now we are looking at 15% upside potential. Not so bad after all for one of the fastest-growing stocks out there!

Best Sector Stocks Through Q2: Whiting Petroleum (WLL)

Sector: Basic Materials

Haven’t heard of Whiting Petroleum Corporation (NYSE:WLL) before? Well now’s your chance. This is a top crude oil producer in North Dakota which also operates substantial assets in northern Colorado. Shares soared over 30% in Q1 after the shale driller reported stronger-than-expected fourth-quarter results and a bullish 2018 outlook.

On the news Seaport Global analyst Mike Kelly upgraded Whiting Petroleum to Buy from Hold. He also increased his price target to $40 from $30 citing confidence in the Bakken development post Q4 results and the experience of new CEO, Brad Holly. He is pushing WLL toward its goal “of becoming a top-tier E&P company as measured by capital efficient growth and free cash flow generation.”

However even though the stock posted stellar gains this quarter, I would recommend not to invest at this point. Top analysts in particular appear unconvinced by WLL’s success story and there are better stocks worth checking out. Instead consider a ‘Strong Buy’ basic materials stock like MasTec, Inc. (NYSE:MTZ).

While MTZ hasn’t posted Q1 gains like WLL, it has big upside potential and has just been named a top mid-cap idea by Canaccord Genuity.

Best Sector Stocks Through Q2: Axon Enterprise (AAXN)

Sector: Industial Goods

Arizona-based Axon Enterprise, Inc. (NASDAQ:AAXN) is best known for its flagship product: electroshock tasers. In fact, the company used to be known as TASER International. However, the company actually develops a wide range of technology and weapons for military, law enforcement and personal defense usage. Right now, it is focusing on developing on-body cameras and digital evidence software.

Over the last few quarters, it is fair to say that AAXN has not been a top performer. However, in Q1 all that changed with an impressive 43% increase in share prices. AAXN finally showed that it is delivering on its promise of better discipline and positive changes. After two quarters of GAAP operating break-even, Axon Enterprises posted the best operating profit in a year. This was on adjusted EBITDA basis the best in three years and a near record.

Top Oppenheimer analyst Andrew Uerkwitz believes that a ‘positive change is occurring.’ Operating expense was still up and there was yet another quirky one-time cash tax expense but “for the first time in several quarters, we are raising our numbers.” However even though he “liked what he heard,” for now Uerkwitz is staying sidelined. “We want to see where the stock settles in the near term and spend time on new growth initiatives such as fleet and RMS” explains Uerkwitz.

For investors looking to invest in the industrial goods sector, I would suggest trying major U.S. defense contractor Raytheon Company (NYSE:RTN) instead. Shares are up 15% in the last three months and with multiple big contract wins the stock has 100% Street support right now.

The 145 Companies Your Stockbroker Will NEVER Tell You About Did you know more than 145 tiny companies have grown to $1 billion-plus valuations since 2012? SpaceX is up 26,309% in value... Dropbox 31,733%... and Pinterest 487,404%. All of these 145 businesses started out as private companies your broker would have NEVER told you about. But now there’s a great way to find the next private companies poised for hyper-growth. Full Details Here.

Source: Investor Place

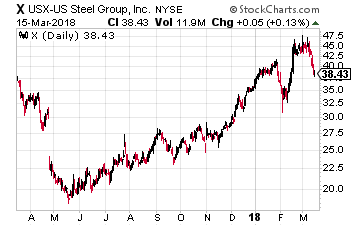

At the top of the list of steel stocks to avoid is U.S. Steel (NYSE: X), which saddens me because my grandfather used to work for the company.

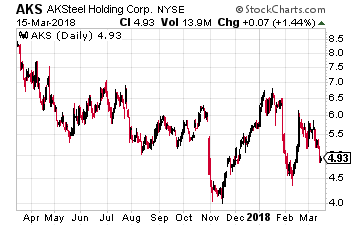

At the top of the list of steel stocks to avoid is U.S. Steel (NYSE: X), which saddens me because my grandfather used to work for the company. The second stock on the no-touch list is AK Steel Holding (NYSE: AKS). Like U.S. Steel, it faces planned maintenance outages in some facilities, affecting production. The company recorded outage costs of $85 million in 2017 and in 2018, it expects expenses associated with planned outages to be about $50 million.

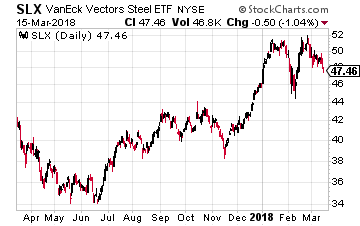

The second stock on the no-touch list is AK Steel Holding (NYSE: AKS). Like U.S. Steel, it faces planned maintenance outages in some facilities, affecting production. The company recorded outage costs of $85 million in 2017 and in 2018, it expects expenses associated with planned outages to be about $50 million. Finally, a broad way to play the chronic overcapacity in the global steel industry is through an exchange traded fund – the VanEck Vectors Steel ETF (NYSE: SLX).

Finally, a broad way to play the chronic overcapacity in the global steel industry is through an exchange traded fund – the VanEck Vectors Steel ETF (NYSE: SLX).

That’s bad news for big, multinational U.S. automakers like Ford Motor Co. (NYSE: F).

That’s bad news for big, multinational U.S. automakers like Ford Motor Co. (NYSE: F).

An ETF owns shares of stock to match the components of a specific stock index. For example, the SPDR S&P 500 ETF (NYSE: SPY) owns the 500 stocks in the same proportion as tracked by the Standard & Poor’s 500 stock index. The financial products industry has gone nuts with the development of new indexes to carve up the market into sectors and ETFs to track them. Currently there are over 2,000 ETFs listed in the U.S. The majority —78% of assets—of ETFs are based on stock market indexes. Those assets total over $2.4 trillion. ETF trading has become a very big part of what goes on in the stock markets.

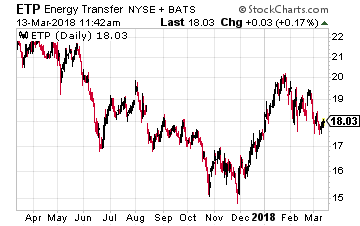

An ETF owns shares of stock to match the components of a specific stock index. For example, the SPDR S&P 500 ETF (NYSE: SPY) owns the 500 stocks in the same proportion as tracked by the Standard & Poor’s 500 stock index. The financial products industry has gone nuts with the development of new indexes to carve up the market into sectors and ETFs to track them. Currently there are over 2,000 ETFs listed in the U.S. The majority —78% of assets—of ETFs are based on stock market indexes. Those assets total over $2.4 trillion. ETF trading has become a very big part of what goes on in the stock markets. There are two ways ETF action can affect the share values of individual stocks. The most obvious and easy to discern is when the weighting of a stock in an index is changed. One high yield example is Energy Transfer Partners LP (NYSE: ETP), a large cap master limited partnership, commonly abbreviated as MLP. In April 2017 ETP completed a merger with Sunoco Logistics Partners LP, another MLP that was a large component of MLP indexes. Because of the merger, ETFs and index funds tracking MLP indexes were forced to sell significant portions of their ETP holdings to bring the size of the positions down to match the index weightings. This merger was the start of a year long decline in the ETP unit value. Later in 2017, Alerian, the provider of the most popular MLP tracking indexes, changed its methodology to cap Alerian MLP Index constituents to a 10% weight. At that time, ETP’s weight was much higher than 10% in the index, so index tracking funds were again forced to sell ETP units, regardless of investment merit. These forced sales of ETP are the source of much of the 25% value decline over the past year. The company’s fundamentals have been steadily improving, but you could not tell by the market price. ETP currently yields 12.5%.

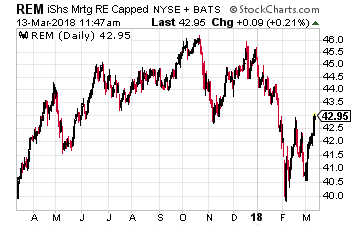

There are two ways ETF action can affect the share values of individual stocks. The most obvious and easy to discern is when the weighting of a stock in an index is changed. One high yield example is Energy Transfer Partners LP (NYSE: ETP), a large cap master limited partnership, commonly abbreviated as MLP. In April 2017 ETP completed a merger with Sunoco Logistics Partners LP, another MLP that was a large component of MLP indexes. Because of the merger, ETFs and index funds tracking MLP indexes were forced to sell significant portions of their ETP holdings to bring the size of the positions down to match the index weightings. This merger was the start of a year long decline in the ETP unit value. Later in 2017, Alerian, the provider of the most popular MLP tracking indexes, changed its methodology to cap Alerian MLP Index constituents to a 10% weight. At that time, ETP’s weight was much higher than 10% in the index, so index tracking funds were again forced to sell ETP units, regardless of investment merit. These forced sales of ETP are the source of much of the 25% value decline over the past year. The company’s fundamentals have been steadily improving, but you could not tell by the market price. ETP currently yields 12.5%. A subtler effect of the ETF boom is that trading of these funds leads to lack of discrimination between the financial results and business prospects. Stocks get lumped together into the ETFs that track specific market sectors. It is tough to figure out whether stock share prices and ETF trading are a chicken and egg dilemma, but it is becoming clearer that increases in ETF trading are tightening correlations, or the tendency for individual stocks and sectors to move up or down in lock step, regardless of a company’s fundamentals. While ETFs account for about 8% of the U.S. stock market value, ETFs are the source of more than 25% of the trading volume. Market observation clearly shows that share prices are greatly affected by short term sector switching by traders. The iShares Mortgage Real Estate ETF (NYSE: REM) provides a couple of examples. Most of the 30 or so stocks in this ETF own leveraged portfolios of residential mortgage backed securities, MBS in industry parlance. This business model is a dangerous game of lending long and borrowing short. This is a group of companies whose finances can be destroyed by a quick change in the yield curve. I recommend against owning any residential MBS focused REITs.

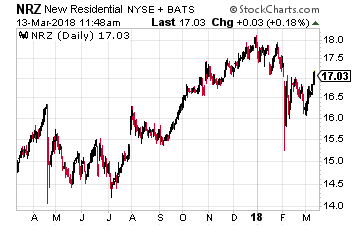

A subtler effect of the ETF boom is that trading of these funds leads to lack of discrimination between the financial results and business prospects. Stocks get lumped together into the ETFs that track specific market sectors. It is tough to figure out whether stock share prices and ETF trading are a chicken and egg dilemma, but it is becoming clearer that increases in ETF trading are tightening correlations, or the tendency for individual stocks and sectors to move up or down in lock step, regardless of a company’s fundamentals. While ETFs account for about 8% of the U.S. stock market value, ETFs are the source of more than 25% of the trading volume. Market observation clearly shows that share prices are greatly affected by short term sector switching by traders. The iShares Mortgage Real Estate ETF (NYSE: REM) provides a couple of examples. Most of the 30 or so stocks in this ETF own leveraged portfolios of residential mortgage backed securities, MBS in industry parlance. This business model is a dangerous game of lending long and borrowing short. This is a group of companies whose finances can be destroyed by a quick change in the yield curve. I recommend against owning any residential MBS focused REITs. In contrast, the third and fourth heavily weighted stocks in REM are solid companies with business operations that are sustainable through market cycles. In contrast to the rest of the REM portfolio stocks, these two will do even better when short term rates rise. Starwood Property Trust, Inc. (NYSE: STWD) and New Residential Investment Corp (NYSE: NRZ) are very attractive stocks with share prices that have trouble escaping from the trading in REM. STWD currently yields 9% and NRZ is over 11%.

In contrast, the third and fourth heavily weighted stocks in REM are solid companies with business operations that are sustainable through market cycles. In contrast to the rest of the REM portfolio stocks, these two will do even better when short term rates rise. Starwood Property Trust, Inc. (NYSE: STWD) and New Residential Investment Corp (NYSE: NRZ) are very attractive stocks with share prices that have trouble escaping from the trading in REM. STWD currently yields 9% and NRZ is over 11%.{kind=link}