In my last two articles, I’ve focused on tech sector investments. (Specifically, an industry-leading companywhose critical products are driving several huge tech trends, plus a diversified way to play one of today’s fastest-growing industries).

Over that time, of course, the stock market has also decided that it’s finally time for a good, old-fashioned bout of volatility.

So today – and in the spirit of not panicking – I want to step away from growth-based tech and follow up on Tim Plaehn’s article on Monday by giving you a couple of ways to combat adversity. Investments that will keep passive income rolling in, even when the market takes a dip.

Let’s get to it…

“Complete Morons”

When the S&P 500 closed last Thursday, it officially entered “correction” territory, having dropped by over 10% from its January 26 peak.

In the process, five of the S&P’s 11 sectors also dropped by over 10%, as the index lost $2.5 trillion of its value.

The culprit?

“Complete morons,” according to CNBC’s Jim Cramer.

You’ve heard of the CBOE Volatility Index (VIX) – which measures the level of fear or complacency in the market, based on short-term S&P 500 options activity.

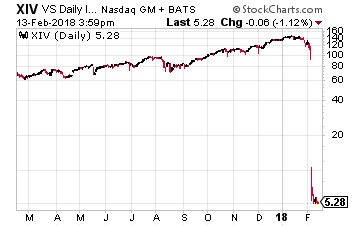

But you may not have heard of the VelocityShares Daily Inverse VIX Short-Term ETN (Nasdaq: XIV). It aims to return the opposite of the VIX – and is one of the investments that Cramer says is responsible for the precipitous drop, due to uninformed speculators betting against volatility through investments they knew little about… and losing big.

But you may not have heard of the VelocityShares Daily Inverse VIX Short-Term ETN (Nasdaq: XIV). It aims to return the opposite of the VIX – and is one of the investments that Cramer says is responsible for the precipitous drop, due to uninformed speculators betting against volatility through investments they knew little about… and losing big.

The fallout was so great that XIV plummeted from a high of $141.39 on January 26 to $5.30 today. As a result, Credit Suisse, which sponsors the fund, announced its liquidation and XIV will cease trading next Tuesday.

When volatility hits, don’t get left holding the bag on these risky investments. There’s a much better way…

Case Closed

A few months ago, I touted the benefits of closed-end funds (CEFs) as hybrid between ETFs and mutual funds. To recap briefly:

- Like ETFs and mutual funds, CEFs invest in a portfolio of underlying stocks. These stocks give a CEF its Net Asset Value (NAV).

- CEFs are actively managed and trade like stocks. There are a limited number of shares available, which are priced intraday – either at a premium or discount to the NAV.

- The “closed-end” part comes from the fact that CEFs are closed to new capital after they’re launched. A fund must subsequently use leverage to raise new money. Because leverage is a percentage of total assets, there’s a risk-reward factor, which affects performance.

But here’s the key point relative to the current climate: They’re less affected by volatility because they don’t create new shares.

They also pay healthy average dividends of around 8%. Check out these ones…

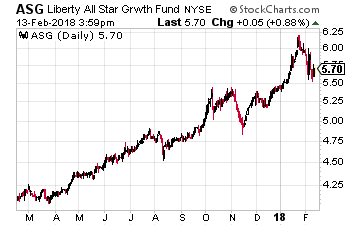

Liberty All-Star Growth Fund (NYSE: ASG): You want diversity? This fund has it – both by industry and asset class. For example, it has strong holdings in tech (28%), consumer cyclicals (18%), industrials (16%), healthcare (15%), as well as financials and real estate.

Liberty All-Star Growth Fund (NYSE: ASG): You want diversity? This fund has it – both by industry and asset class. For example, it has strong holdings in tech (28%), consumer cyclicals (18%), industrials (16%), healthcare (15%), as well as financials and real estate.

It also splits across market caps, with 47% midcaps, 23% small caps, and 17% large caps, with the rest distributed among mega caps and microcaps.

The fund is up 27% over the past 12 months, compared to 12% for the S&P 500. Right now, ASG trades at a very slight premium – just $0.15 above its NAV. But it offers a robust $0.44 per share annual dividend (paid quarterly) – a 7.8% yield.

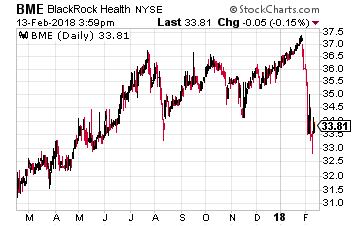

BlackRock Health Sciences (NYSE: BME): From diversity to specificity. This fund focuses exclusively on healthcare, with most of the portfolio dedicated towards large-cap stocks like Pfizer, Merck, Gilead Sciences, Bristol-Myers Squibb, Amgen, Biogen, Celgene, and Johnson & Johnson.

BlackRock Health Sciences (NYSE: BME): From diversity to specificity. This fund focuses exclusively on healthcare, with most of the portfolio dedicated towards large-cap stocks like Pfizer, Merck, Gilead Sciences, Bristol-Myers Squibb, Amgen, Biogen, Celgene, and Johnson & Johnson.

In terms of capital appreciation, the fund has notched gains in eight of the past 10 years, ranging from 5.5% on the low end to 42% at the top end.

And if you like your dividends more often, BME pays them monthly and boasts a 7.1% yield. The fund is also trading at a 4.5% discount to its NAV, with a 1.1% expense fee.

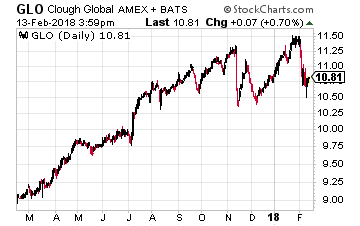

Clough Global Opportunities Fund (NYSE: GLO): As the name suggests, this fund offers a more global outlook, with around 22% of the portfolio containing non-U.S. stocks. This includes the likes of Samsung, Alibaba, Broadcom, and the Swiss-based CRISPR Therapeutics.

Clough Global Opportunities Fund (NYSE: GLO): As the name suggests, this fund offers a more global outlook, with around 22% of the portfolio containing non-U.S. stocks. This includes the likes of Samsung, Alibaba, Broadcom, and the Swiss-based CRISPR Therapeutics.

Technology, healthcare, and financials make up the bulk of the sector denomination and it’s weighted towards bigger companies, with around 55% of the portfolio comprising large-cap stocks.

The fund enjoyed an impressive 2017, notching a 35% return.

Dividends are paid monthly and GLO currently spits back a beefy 11.7% yield. Even better… it’s trading at a 9.3% discount to its NAV. However, its management fee is a little more expensive than the other two funds, with an expense ratio of 2.2%.

Ultimately, diversified closed-end funds like these offer a much better way to shelter your portfolio from volatility, versus the riskier, more direct ways that we’ve seen investors try to play the market recently.

And remember… even if the stocks fall with the market, you’ve still got an all-important income stream coming in.

Source: Investors Alley

XPO Logistics is a top ten global logistics firm with operations in both logistics and transportation in 32 countries. Customers trust XPO with an average of 160,000 shipments and over seven billion inventory units every day.

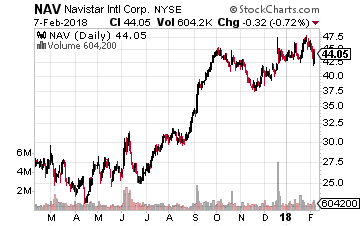

XPO Logistics is a top ten global logistics firm with operations in both logistics and transportation in 32 countries. Customers trust XPO with an average of 160,000 shipments and over seven billion inventory units every day. Navistar International manufactures International brand commercial and military trucks, school and commercial buses as well as diesel engines. Trucks make up most of its revenues, generating 67.8% of the total in 2017. The company has issued positive guidance for 2018 saying it expects revenues to be in the range of $9 to $9.5 billion versus $8.6 billion in fiscal 2017.

Navistar International manufactures International brand commercial and military trucks, school and commercial buses as well as diesel engines. Trucks make up most of its revenues, generating 67.8% of the total in 2017. The company has issued positive guidance for 2018 saying it expects revenues to be in the range of $9 to $9.5 billion versus $8.6 billion in fiscal 2017.

So what could the investment implications be for you? They’re pretty obvious.

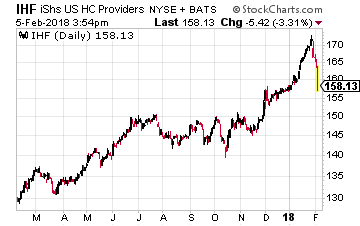

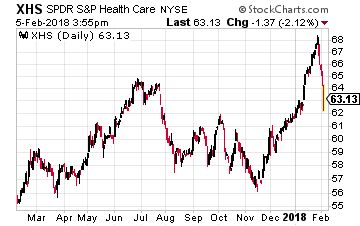

So what could the investment implications be for you? They’re pretty obvious. I would even go as far as, if you have a high risk tolerance, to look at shorting these two ETFs that are loaded with middlemen stocks, the iShares U.S. Healthcare Providers ETF (NYSE: IHF) and the SPDR S&P Health Care Services ETF (NYSE: XHS).

I would even go as far as, if you have a high risk tolerance, to look at shorting these two ETFs that are loaded with middlemen stocks, the iShares U.S. Healthcare Providers ETF (NYSE: IHF) and the SPDR S&P Health Care Services ETF (NYSE: XHS).

Tied for second on the list are Mastercard (NYSE: MA) and International Business Machines (NYSE: IBM). The latter was one of the very first big companies to see the promise of blockchain, contributing code to an open-source effort and encouraging start-ups to try the technology on its cloud for free. What really caught my eye regarding IBM’s blockchain efforts was a recent announcement.

Tied for second on the list are Mastercard (NYSE: MA) and International Business Machines (NYSE: IBM). The latter was one of the very first big companies to see the promise of blockchain, contributing code to an open-source effort and encouraging start-ups to try the technology on its cloud for free. What really caught my eye regarding IBM’s blockchain efforts was a recent announcement. The words supply chain bring me to what I consider to be a major announcement last week from IBM and the world’s largest shipping company, AP Moller Maersk A/S (OTC: AMKBY). The two firms are setting up a joint venture to use blockchain technology in order to help make the companies’ supply chains more efficient.

The words supply chain bring me to what I consider to be a major announcement last week from IBM and the world’s largest shipping company, AP Moller Maersk A/S (OTC: AMKBY). The two firms are setting up a joint venture to use blockchain technology in order to help make the companies’ supply chains more efficient.