I remember when I first heard about cryptocurrencies. It was in 2013; a Libertarian friend of mine mentioned how he was dabbling in something called “bitcoin.”

“This is the new, new thing,” he said. It would sweep away the need for central banks. The underlying blockchain technology would kill off big paper-shuffling bureaucracies. “People need advice on how to make money from this new digital asset.”

Alas, it was a tough business proposition back then. Ask most people about bitcoin or Ethereum and you got a shrug of the shoulders. But that wouldn’t be the case forever.

So when we created Banyan Hill, we knew we wanted a cryptocurrency expert on the staff. The tough part was finding one with the right experience and credentials for the job.

By that I mean we wanted a pro — someone who “ran money” professionally on Wall Street, someone who didn’t just write about bitcoin but bought and sold it too. And we wanted someone who could explain how to do it to mainstream Americans in simple, clear language.

Quite frankly, that’s a whole other level of expertise. So I’m pleased to announce that, after a long search, we found the right person for the job…

His name is Ian King, Banyan Hill’s new cryptocurrency editor.

Ian believes in the future of cryptocurrencies so much, he broke off from a successful hedge fund career to create his own website teaching people how to buy and sell the likes of bitcoin, Ripple, Litecoin, Monero and other cryptos.

So when we came upon Ian’s work, the team and I here at Banyan Hill all looked at each other and said: “We have to hire this guy.”

Real-Life Crypto Trader

Ian has quite a resume.

He started out as a desk clerk at Salomon Brothers’ famed mortgage bond trading department, then moved on to credit derivatives at Citigroup. From there, he spent a decade as head trader at Peahi Capital, a New York-based hedge fund.

After spotting the opportunity in cryptocurrencies, Ian started his own firm to educate and advise crypto speculators. And that’s where we nabbed him, so he could do the same for Banyan Hill’s subscribers.

That seems like a good point to introduce Ian himself…

Q. First, Ian — welcome to Banyan Hill! We’re all very excited to have you join us as our cryptocurrency trading expert. Tell us a little bit about yourself.

I grew up on the Jersey Shore, where I spent summers as an ocean lifeguard. At 19, I was appointed captain of the busiest beach in Belmar, New Jersey.

It was common to have upward of 50 rescues on days when the ocean was rough.

And, although it may sound odd, this is where I started learning the tools that would lead to my success in trading.

See, lifesaving teaches you how to analyze a situation and react quickly. When charging into the surf to help someone, you need to trust your instincts and think on your feet — skills that have become invaluable in my trading career.

Later, in college, I studied psychology and premed in hopes of becoming a psychiatrist. But in my spare time, I started trading dot-com stocks from my dorm room — and I found that I loved analyzing trends too. So while I received a B.S. in psychology, I decided to grab an internship at Merrill Lynch in the middle of the ‘90s bull market.

Trading fascinates me. It requires a better understanding of oneself — of human psychology — as much as an understanding of the market. After all, markets are comprised of individuals acting in groups. So it all comes down to the same question: Why do we do what we do?

Now I use that question to drive my investigation of the cryptocurrency market from my home in New York City, where I’ve spent the last 20 years.

Q. When did you first get an inkling that cryptocurrencies were going to be the next big thing?

I’ve been thinking about digital money since the end of the financial crisis, when the Fed lowered interest rates to zero.

In 2012, I met with a startup in Silicon Valley that was piloting an e-currency to allow central banks to print and distribute a digital form of money.

To be clear, this was not a cryptocurrency because the value was backed by whatever central bank was issuing it. But the experience sparked my thinking about how digital money can be used to incentivize better citizenry. And how the transfer of value outside the banking system could solve the space and time problem of physical money without the need for a middleman.

There was a need for digital currency here. And the timing was perfect…

Every 10 years, a new technology arrives that changes civilization for the better and creates tremendous wealth for investors.

In the ‘70s, mainframe computing allowed for bulk data processing.

In the ‘80s, personal computers allowed corporations and consumers to run these applications.

In the ‘90s, the rise of the internet democratized information.

In the 2000s, we started sharing that information with “friends” on social media.

And now, in the 2010s, crypto assets permit anyone, anywhere in the world, to transfer something of digital value without the need for an intermediary.

Bitcoin is one such form. However, the bigger picture here is the rise of a whole new crypto asset class that investors are just beginning to discover.

This dispersion of capital among new crypto asset ventures is just beginning, as newly minted bitcoin millionaires reinvest their crypto fortunes, and a fresh wave of entrepreneurs look to capitalize on the current rush of capital.

Q. You worked on Wall Street for years, both at Salomon Brothers, then in credit derivatives at Citigroup, and then became head trader at an equities hedge fund. What did you learn on Wall Street that most prepared you for your second career as one of the world’s best cryptocurrency traders?

For one, in trading, you are only as good as your last trade. That always keeps me searching for the best opportunities.

Another thing my experience has taught me: The asset class may have changed, but the investment behavior here is the same as it always is in new markets.

For example, these markets remind me of the dot-com days in the late ‘90s when 22-year-old day traders were making tens of thousands of dollars a day just by being in the right place at the right time.

The crypto markets are in full mania mode right now — and that means anyone who bought within the last six months has witnessed a 500% return.

But there’s much more upside ahead. See, the good news is that with the institutional money still flowing into crypto, we are years away from the end.

That’s what my career on Wall Street has taught me, and that’s why now is the time to get in if you haven’t already.

Despite the fact that everyone has heard about crypto, only a few people actually own it, and even fewer understand it. So you can still get ahead of the pack.

Q. For people who are unfamiliar with cryptocurrencies … what exactly are they?

Cryptocurrencies are a fundamental change in the way people can exchange something of value.

Every transaction is built on trust. Economies thrive in societies where people trust one another.

In a typical economic transaction, I give you something of value (for instance, $10), and you deliver me a good or service in return. (Let’s say it’s a ride somewhere in an Uber.)

Historically, in order for this transaction to happen, there has to be a middleman to oversee the transaction and punish bad actors.

But “smart” digital money that can be programmed is going to change all of that…

For the first time, an internet user can transfer a unique piece of digital property to another internet user in a way that is safe and secure. Everyone knows this transfer occurred, and nobody can oppose it.

This digital property can be exchanged through a decentralized network of trust that gets rid of the need for a bank or middleman to oversee its validity.

No middleman, no fees to pay the middleman! It’s all verifiable without it. This is a huge breakthrough.

When you see just how big it is (something I’ll continue to write about here in Sovereign Investor Daily), you can understand why smart investors are quickly snapping up new crypto assets.

Keep in mind that I’m saying “crypto assets.” Cryptocurrencies were only the first iteration of this new technology, a subclass of crypto assets.

Crypto assets include new projects such as Filecoin, which raised over $200 million this summer and allows consumers to share computer storage over the blockchain.

Or IOTA, which is the platform that will permit the Internet of Things to exchange something of value. Think about your refrigerator ordering groceries for you or your car paying the parking meter.

So you can see why investors are going crazy for this new type of investment…

Q. We’ve read plenty about the price advances in bitcoin and other forms. Is there still money to be made in cryptocurrencies after the big gains we’ve heard about already?

Absolutely. If the dot-com bubble is a roadmap, we are still in the very early innings of the bubble.

As I said before, the good news is that with the institutional money still flowing into crypto, we are years away from the end.

In fact, in my most recent piece for Banyan Hill, which everyone can read Friday in Sovereign Investor Daily, I explain that bitcoin has finally reached a tipping point … but that it just means there are great opportunities in the offing for those who know where to look.

Just keep in mind that this bubble is particularly odd because it’s the first time in history where Wall Street arrived late to the party. That’s why we’re hearing such skepticism about this market.

In fact, I believe most of Wall Street’s cynicism is simply because it hasn’t yet figured out how to skim its profits off this new financial marketplace. JPMorgan CEO Jamie Dimon has labeled bitcoin as a “fraud,” but he was awfully quiet when his bank was raking in tens of billions by securitizing fraudulent mortgages.

Q. Coming soon, you’ll be launching a cryptocurrency trading service at Banyan Hill. Can you give us some insights into your trading strategy(s) for cryptocurrencies? Are they actually “tradeable”? If so, how?

I’m in the midst of putting this service together, and I’m extremely excited about sharing these opportunities with everyone — because yes, they are tradeable.

See, I look for three big things in a crypto trade before I believe it’s viable:

- Does the crypto asset solve a real-world problem? Is there an immediate use for this new asset? For instance, the insurance company AXA is already using the Ethereum blockchain to run a decentralized flight insurance program. Now when you purchase flight insurance, you will be automatically compensated if the flight doesn’t leave on time. This process is fully autonomous on the blockchain.

- What is the crypto asset’s supply schedule? Is there a limited amount of supply that will give this asset value in the future? Bitcoin has a limited supply of coins, with approximately 80% of the total supply issued. That’s not the case for all cryptocurrencies, where investors risk the chance of future dilution.

- Are the technicals favorable? Is there a strong uptrend in increasing volume? This factor is arguably the most important because strong technicals can be a buy signal to other traders, and higher prices become a self-fulfilling prophecy.

These three factors led me to purchase Litecoin just a few months ago and ride it for 1,000% gains. Many consider this cryptocurrency as “silver” to bitcoin’s “gold,” as it has similar properties … but it’s able to transact four times faster.

Now I’m compiling that type of experience into a service that will help traders — either new to the market or not — experience the gains that Wall Street has said it has missed.

I just want to stress this point — there are plenty of gains still yet to be made in this market. And I want to make sure the everyday investor has clear and easy access to that.

Q: Ian, that seems like a good place to wrap things up. Any last thoughts?

Right now, cryptocurrencies are this new thing. Mainstream Americans are starting to get used to them. The whole thing is sort of a novel experience right now.

So take us into the future. How will we be thinking about cryptocurrencies in five or 10 years from now?

What will our experience or interaction be with these new forms of exchange down the road?

Coming into this year, bitcoin was the only game in town, capturing 87% of the total cryptocoin market cap. That dominant market share has been halved to about 45% (even though bitcoin’s price has quadrupled at the same time).

So it’s clear to me that this thriving market is just getting started, and I’m excited to pinpoint these new trends here.

We are still early in the investment and discovery cycle, and that’s why crypto will end up being much bigger than even the first wave of dot-coms.

If history is any guide, when the first dot-com investment cycle peaked in March 2000, the 280 stocks in the Bloomberg U.S. Internet Index reached a combined market value of $2.94 trillion.

At $600 billion, crypto’s total market cap is still one-fifth of the dot-com peak. However, this is the first bubble in human history where everyone on the planet (at least if you own a mobile phone) can participate.

Kind regards,

Jeff L. Yastine

Editor, Total Wealth Insider

Can a $10 Bill Really Fund Your Retirement? The digital currency markets are delivering profits unlike anything we’ve ever seen. 23 recently doubled in a single week. And some like DubaiCoin have jumped as much as 8,200X in value in 18 months. It’ unprecedented... but you won’t receive any of the rewards unless you put a little money in the game. Find out how $10 could make you rich HERE.

Source:

Banyan Hill

First Data (NYSE: FDC) provides merchant transaction processing; credit, debit and retail card issuing and processing; prepaid services and check verification and other similar services.

First Data (NYSE: FDC) provides merchant transaction processing; credit, debit and retail card issuing and processing; prepaid services and check verification and other similar services. Tenet Healthcare (NYSE: THC) owns and operates hospitals and other healthcare facilities. It is one of the largest investor-owned healthcare delivery systems in the United States.

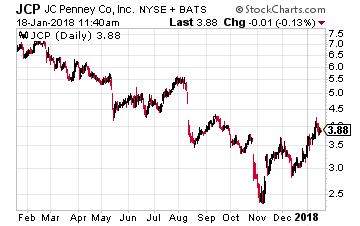

Tenet Healthcare (NYSE: THC) owns and operates hospitals and other healthcare facilities. It is one of the largest investor-owned healthcare delivery systems in the United States. JC Penney (NYSE: JCP) is a well-known department store chain with still 875 stores across the U.S. It is almost a poster child for being Amazoned. Adding to all the woes it faces on the competitive front is its heavy debt burden in excess of $4 billion.

JC Penney (NYSE: JCP) is a well-known department store chain with still 875 stores across the U.S. It is almost a poster child for being Amazoned. Adding to all the woes it faces on the competitive front is its heavy debt burden in excess of $4 billion.

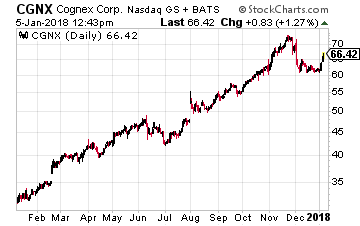

Foremost in this sector is Cognex (Nasdaq: CGNX), which is the leader globally in providing vision systems, vision software, vision sensors and industrial ID readers. It sells its vision systems to most of the big players in the industrial robotics industry including ABB, Yaskawa Electric and Germany’s Kuka AG. The only exception is Fanuc, which makes its own vision systems. This translates to Cognex having a 30% share of the vision systems market.

Foremost in this sector is Cognex (Nasdaq: CGNX), which is the leader globally in providing vision systems, vision software, vision sensors and industrial ID readers. It sells its vision systems to most of the big players in the industrial robotics industry including ABB, Yaskawa Electric and Germany’s Kuka AG. The only exception is Fanuc, which makes its own vision systems. This translates to Cognex having a 30% share of the vision systems market.

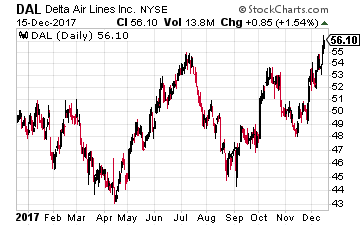

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually.

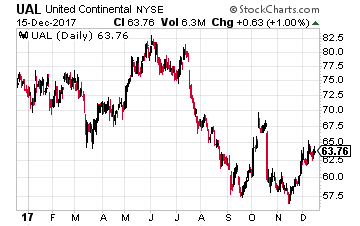

Delta operates a fleet of over 700 aircraft and serves more than 170 million customers annually. United is the world’s largest airline, operating about 5,000 flights a day. Unlike Delta, it is not showing growth in its passenger revenue per available seat mile. But it is showing improvement – the company’s latest estimate is for it to be flat to down 2% year-over-year. That compares to the previous estimate of down 1% to 3%.

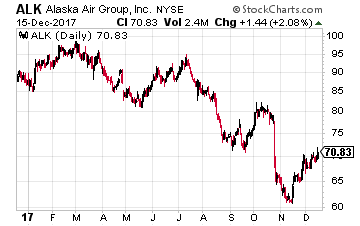

United is the world’s largest airline, operating about 5,000 flights a day. Unlike Delta, it is not showing growth in its passenger revenue per available seat mile. But it is showing improvement – the company’s latest estimate is for it to be flat to down 2% year-over-year. That compares to the previous estimate of down 1% to 3%. Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like its purchase of Virgin America this year, despite the rise in the amount of debt it now has. The company also owns Horizon Air.

Alaska Air operations cover the western U.S., Canada and Mexico as well as, of course, Alaska. I like its purchase of Virgin America this year, despite the rise in the amount of debt it now has. The company also owns Horizon Air.