So close, and yet so far. That sums up the state of the markets recently, with investors jittery over the sudden chill surrounding U.S.-China relations. In an about-face on the trade dispute, President Trump conceded that tariffs on Chinese goods may remain for a “substantial period of time.” Simultaneously, this hurts the broader markets but it also raises prospects for cheap stocks.

I know what you’re thinking: why should I consider cheap stocks to buy when blue-chip names are also available for deeply discounted prices? Far be it from me to disagree with that logic. Typically, you accrue the biggest profits from striking while others are panicking. But after you’re comfortable with your high-probability bets, penny stocks provide exceptionally robust return potential.

We should also discuss the “under-the-radar” argument. News such as the trade-war dispute disproportionately hurt the blue chips because they’re usually multinational corporations with global vulnerabilities. While penny stocks also suffer the trickle-down effect, they’re more likely to move on sector-specific developments.

With that in mind, let’s take a look at three (very) cheap stocks to buy that are worth every penny:

Entrée Resources (NYSEAMERICAN:EGI) is one of the penny stocks that actually benefits from broader and sector-specific trends. With all eyes focused on the suddenly deteriorating trade-war dispute, investors get nervous. When investors get nervous, they buy gold. Naturally, as a gold miner, EGI has a lot to gain.

Another thing that intrigued me about EGI as a candidate for cheap stocks to buy is its locality. Most speculative miners have projects in extremely unstable countries just begging for nationalization. While Entrée’s main property in Mongolia isn’t the greatest region for stability, it’s also not the worst. Over the last few years, Mongolia improved its standing for ease of doing business.

Additionally, the gold price has also improved, gaining roughly 10% since the first of October. That’s a net positive for EGI stock, especially since it might go higher still. However, keep in mind that gold is extremely volatile, so don’t lever yourself excessively.

Genius Brands International (GNUS)

Source: Shutterstock

The entertainment industry is a tough sector in which to survive, let alone thrive. What works and what doesn’t often seem arbitrary. Moreover, maintaining relevance is a gargantuan task once you’ve accomplished the already difficult task of delivering a hit. But the prospect of finding that hit drives Genius Brands International(NASDAQ:GNUS).

GNUS specializes in creating compelling content and characters. Where it differs compared to other cheap stocks in the entertainment field is the company’s core audience: toddlers to tweens. This is an exceptionally challenging market to crack because you’re dealing with two audiences: the young consumer and their parents/guardians.

At the same time, GNUS has a viable pathway to profound growth. The reason? Brands such as cartoon characters translate very well internationally. If it resonates in America, it will probably resonate everywhere else.

Novavax (NVAX)

Source: Shutterstock

Over the past few years, vaccination captured the public’s attention, and not always in a good way. With President Trump’s election, an increasing number of people became aware of so-called alternative-truth movements. Many of these right-leaning organizations rally fiercely against vaccination, particularly government-imposed protocols.

On the surface, that doesn’t help Novavax (NASDAQ:NVAX), which specializes in the stuff. Nor does the fact that NVAX is one of the riskiest penny stocks to buy. Since Feb. 27, shares have plummeted nearly 71%. Even more concerning is the reason why NVAX fell.

In a clinical trial, the company’s NanoFlu treatment failed to beat placebo. In other words, positive thinking yielded roughly the same efficacy in preventing influenza than the vaccine.

Given that NVAX is a fundamentally poor organization, I’m not surprised that shares fell. However, keep in mind that most Americans support vaccination. Therefore, the broader financial incentive to stay the course until efficacy improves is incredibly high.

With my Dividend Hunter service, I provide a list of high-yield investments that I have deeply researched, and my analysis shows provide an attractive combination of current yield and dividend stability.

As a high-yield stock expert, I often get asked questions about other stocks or investments that are not on my recommendations list. Sometimes a question will show me a new, attractive income investment. Others are learning opportunities on what not to do when picking high-yield investments.

One investment category that generates a lot of questions is closed-end funds (CEFs).

A closed-end fund is an investment pool with shares that trade on the stock exchange. Investors are drawn to CEFs because many have double digit yields and most paid monthly dividends.

Unfortunately, with most closed-end funds there are usually more negatives than positives when evaluating one for investment potential. Here are a few of the problems you could see.

Opaque communications from management on how a CEF is managed. There are not a lot of reporting requirements and any information you find on a fund’s portfolio may be months old. I sometimes refer to the CEF universe as the swamp of managed investment products.

CEF shares can trade at a discount or premium to the net asset value (NAV). Fund sponsors do not redeem shares, so the only place to buy or sell is on the stock exchange. If you buy a fund trading at a premium, you are paying more than a dollar for a dollar’s worth of assets. Not a good deal. A CEF trading at a deep discount can be a danger sign that the management has been making some bad investments.

Dividends classified as return-of-capital (ROC) are a big danger sign. Technically, return-of-capital are dividends/distributions that are not from earned income such as dividends or interest. While there are types and circumstances where ROC is not destructive to a fund’s NAV, unless you know for sure where the ROC comes from, it’s a danger signal to a CEF’s long term viability.

To recap, the problem with many CEFs is that they are hard to analyze with several factors that on their face are dangerous to your long term investment success. With over 700 publicly traded CEF’s, it is too much work to dig a handful of good ones out of the majority of swamp muck. Here are three high yield CEF’s to dump now if you own them.

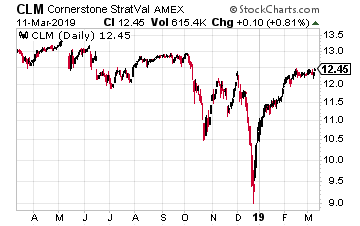

Cornerstone Strategic Value (NYSE: CLM) is a CEF with $570 million in assets that owns a portfolio of global equity (stocks) securities.

CLM currently yields over 20%. There are two big danger signals for this fund. First, it is trading at an 11% premium to NAV. The high yield has caused unwitting investors to bid up the share price to 11% above what they would be worth if the fund is liquidated.

The current monthly dividend is 20.53 cents per share. Out of that just one cent is earned income and two cents are capital gains. The remaining 19.3 cents per share is classified as ROC. Historically, most of the dividends have been ROC, which is reflected in the steadily deteriorating NAV.

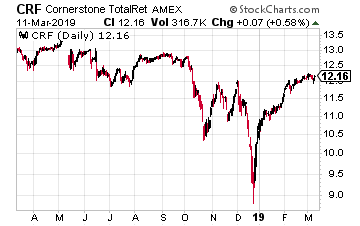

As typically happens, Cornerstone Total Return (NYSE: CRF) is a similar fund managed by the same advisory firm with the same problems.

This fund is trading at a 12.5% premium to NAV. That is very rich pricing in the CEF world.

The distributions breakdown also is like CLM. The current 19.85 cents month dividend has been paid for since the start of 2019. Each month 18.7 cents of the payout have been classified as return of capital.

Ignore the 20% yield and avoid or sell CRF.

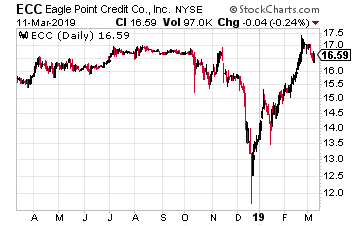

Eagle Point Credit Company LLC (NYSE: ECC)yields 14%. Due to recent large drops in the NAV, the shares trade at an eye-watering 23% premium to NAV.

Out of the 20 cents per share monthly dividends, 7 cents have recently been classified as ROC. Put another way, ECC is earning just 65% of the dividend it’s paying to shareholders.

Here’s the scariest part, the fund’s investment strategy: We seek to achieve our investment objectives by investing primarily in equity and junior debt tranches of CLOs. In plain English, they own the junkiest of the junk in the high-yield debt world.

After a brutal late 2018 selloff, financial markets have been on a healthy and stable recovery path thus far in 2019. Through the first three months of the year, the S&P 500 is up 12%, marking one of its best starts to a calendar year in recent memory.

As broader financial markets have stabilized, growth stocks have come back into favor. Indeed, one could say that they’ve done much more than come back into favor. Many of them have rushed to fresh all-time highs in 2019, and that’s after big corrections in late 2018. That means that a handful of these growth stocks have staged huge rallies over the past three months.

Which stocks fit into this category? And can these big rallies last?

These are questions investors should be asking as we head into what projects to be a more volatile time for financial markets throughout the balance of 2019. As such, let’s take a look at seven growth stocks which have raced to all-time highs in early 2019, and analyze whether or not their big rallies can continue.

iRobot (IRBT)

Why It’s at All-Time Highs: Shares of consumer robotics giant iRobot (NASDAQ:IRBT)have run up to all-time highs prices on the back of a strong double-beat-and-raise fourth-quarter earnings report that emphasized a few positive trends, including continued robust robotic vacuum market expansion, strong margin growth and a mitigated tariff impact.

Where It’s Going Next: The long-term IRBT growth narrative is positive. This company is morphing into a consumer robotics leader with minimal competition, and as such, will be a big revenue and profit grower for a lot longer as the consumer robotics space expands. Such big revenue and profit growth will keep IRBT stock on a long-term winning trajectory. But, in the near term, the valuation seems stretched at nearly 40x forward earnings. This stock needs to trade sideways for the foreseeable future to allow the fundamentals to catch up.

Shopify (SHOP)

Why It’s At All-Time Highs: Shares of e-commerce solutions provider Shopify (NYSE:SHOP) have notched new all-time highs thanks to renewed macroeconomic confidence and a strong Q4 earnings report in which growth hardly slowed and margins continued to move higher.

Where It’s Going Next: In the big picture, Shopify stock is powered by a secular growth narrative that goes something like this: the world is becoming increasingly decentralized thanks to technology democratizing creation and distribution processes. Shopify is enabling and empower this decentralization in the retail world. As this decentralization trend continues to play out over the next several years, Shopify’s merchant base will grow by leaps and bounds. Revenues will roar higher. Profits will, too. So will SHOP stock. As such, the long-term narrative here is very bullish — bullish enough to make this a long-term buy-and-hold stock.

Cronos (CRON)

Why It’s At All-Time Highs: Shares of Canadian cannabis company Cronos (NASDAQ:CRON) have more than doubled in 2019 and run to fresh all-time highs on the back of a multi-billion dollar investment from tobacco giant Altria (NYSE:MO). Investors have interpreted this investment as a major vote of confidence from a well respected global tobacco giant, at a time when global cannabis market fundamentals are improving. Consequently, they have bid up CRON stock to new highs.

Where It’s Going Next: The cannabis market projects to be really, really big one day. With a multi-billion dollar investment from Altria in its back pocket, Cronos has the necessary financial resources, business know-how, and distribution networks to one day turn into a major player in this global market. It’s fair to say that the stock has gone too far, too fast, and needs to cool off. This is likely what will happen. But, after that cooling off period, CRON stock will resume its uptrend, because the long-term fundamentals here of Cronos turning into a global cannabis giant are quite promising.

Wayfair (W)

Why It’s At All-Time Highs: Shares of online home retailer Wayfair (NYSE:W) have surged over the past few weeks to all-time highs thanks to two things. One, confidence in the macroeconomic environments in the U.S. and Europe has dramatically improved. Two, Wayfair’s margins finally stabilized last quarter, and that stabilization coupled with continued robust domestic and international growth served as justification for what had been several quarters of big investment. Investors rallied around those numbers, and bid up W stock to new highs.

Where It’s Going Next: Wayfair is a big growth story. This company has differentiated itself as the leader in a secular growth online home retail market, and this market is very big. Management pegs it at $600 billion in the U.S. and Europe. Revenues were under $7 billion last year, and grew by over 40% year-over-year. Thus, there is lots of runway for Wayfair to remain a big growth company for a lot longer. Having said that, the valuation is a tough pill to swallow here, especially with profit margins still very weak. As such, I wouldn’t chase this rally. But, I would buy any big dips.

The Trade Desk (TTD)

Why It’s At All-Time Highs: Programmatic advertising leader The Trade Desk (NASDAQ:TTD) has exploded to all-time highs over the past few weeks thanks to a robust double-beat-and-raise fourth quarter earnings report which underscored that this company’s growth narrative is still accelerating, and that big growth is here to stay for a lot longer.

Where It’s Going Next: The Trade Desk is a secular growth company powered by still accelerating tailwinds in automation and advertising. Over time, all $1 trillion worth of global ads will be transacted programmatically. That means that Trade Desk, which had under $3 billion in gross spend last year, has a huge opportunity in front of it to grow gross ad spend towards $100 billion-plus. If management successfully executes on that opportunity, TTD stock will head significantly higher in a long term window.

Etsy (ETSY)

Why It’s At All-Time Highs: Shares of Etsy (NASDAQ:ETSY) have surged to all-time highs over the past few weeks thanks to robust holiday numbers which were strong across the board, including robust community, sales, margin, and profit growth. Investors cheered those results, and bid up ETSY stock to fresh highs.

Where It’s Going Next: Etsy is a big growth company with strong growth drivers in e-commerce. But, there’s lots of competition here, from Amazon (NASDAQ:AMZN), eBay (NASDAQ:EBAY), and others. To be sure, Etsy has held off that competition, but that’s because Etsy dominates a niche of the market, meaning that growth won’t remain big forever. Eventually, it will tap out, and so will margins. That may happen sooner than most expect, and at over 60x forward earnings, a slowdown could be catastrophic for ETSY stock.

Chegg (CHGG)

Why It’s At All-Time Highs: Digital education platform Chegg (NASDAQ:CHGG) has roared to all-time highs on the back of a strong Q4 earnings report which included robust subscriber, revenue, and profit growth, as well as a healthy first quarter and fiscal 2019 guide.

Where It’s Going Next: CHGG stock will head higher from here. Why? Because the company is the unchallenged leader in the digital education market, and that market is far bigger than what the company is currently penetrating. At scale, Chegg will transform into a must-have digital education tool for all high school and college students. It is only a fraction of that today. As such, big growth is here stay for a lot longer. Such big growth is also accompanied by big margins. The combination of big growth and big margins will inevitably power CHGG stock higher in the long run.

Big technology companies have been under a lot of political and social pressure recently, mostly because said technology companies have become the be-all, end-all of society. The worry is that these companies are gaining too much power, and that too much power is never a good thing. Big technology companies that provide “free” services by monetizing user data have borne the brunt of it, as such companies are coming under heavy scrutiny for the way they use personal data to make money.

A lot of these concerns haven’t materialized into anything other than talk. But there’s one potential legislation which big tech investors should be aware of, if not concerned about: the data dividend.

The concept is simple: tech companies should pay you for your data. Your data is valuable. It’s being monetized broadly. Since you technically own your own data, when your data does get monetized broadly, you should get a piece of those rewards. That piece is the data dividend, and it would essentially amount to a percent of the company’s data-derived revenues.

The idea isn’t new. The academic world has been discussing the idea for some time. Washington state tried to pass data dividend legislation in 2017. But attempts to implement a data dividend have been too far and few between to mean anything. Until now. California Governor Gavin Newsom recently proposed the idea, and the proposition carries weight both because of when (amid heightened data privacy concerns) and where (California is home to many of the world’s tech giants, and is ahead of the curve when it comes to data protection laws) it was proposed.

As such, while it’s still far from a sure thing, a data dividend is now closer to reality than ever before. That’s bad news for any big tech company which uses consumer data to make money.

Which stocks are most affected by a potential data dividend? Let’s take a deeper look.

Facebook (FB)

Data-Related Revenue (% of Total Revenue): $55 billion (99%)

At the top of this list is a social-media giant which essentially makes all of its money from consumer data, meaning that essentially all of its revenues are theoretically subject to a data dividend.

Facebook (NASDAQ:FB) rakes in over $55 billion (and growing) in ad revenue per year. This money comes from advertisements across its four social media apps — Facebook, Instagram, Messenger and WhatsApp — and is all the byproduct of leveraging user data to incorporate relevant and targeted ads. Facebook is arguably the best in the business at using this data to create effective ad campaigns. They also have more data than pretty much anyone in the world.

But those positives also mean that Facebook could be a big loser if the data dividend idea gains national and global traction. Even if a data dividend amounts to just 2% of revenues, that would equate to over $1 billion per year for Facebook. And, that extra cost would come at a time when costs are dramatically rising for improved data protection.

In the big picture, the data-dividend risk isn’t a reason not to own FB stock. FB stock is a long-term winner supported by the stickiest digital ecosystem in the world. But it is something to be aware of and monitor.

Twitter (TWTR)

Data-Related Revenue (% of Total Revenue): $3 billion (100%)

The second of the possible data dividend stocks is another social media company, which makes essentially all of its money through either leveraging consumer data to create ad campaigns or just straight-up selling that consumer data.

Twitter (NYSE:TWTR) rakes in about $3 billion per year in data-related revenue. Roughly $2.6 billion of that is from ads — Twitter leverages user data to create targeted ad campaigns. The other $400 million-plus comes from Twitter’s data licensing business, which is essentially Twitter just selling user data. Thus, if a data dividend were to be introduced on a global scale, all of Twitter’s revenues would theoretically be subject to that dividend.

That’s not a great thing. But it’s not a deal breaker, either. Much like Facebook, Twitter has created an ultra-sticky digital service. That service is only getting stickier, as Twitter is increasingly becoming a go-to and irreplaceable platform for consumers of all shapes, sizes, and backgrounds to voice their opinion. Thus, while the data-dividend risk should be monitored, it isn’t a reason to sell TWTR stock.

Snap (SNAP)

Data-Related Revenue (% of Total Revenue): $1.2 billion (almost 100%)

Third of the data dividend stocks is yet another social media company that makes essentially of its money through digital advertising, which comprises leveraging user data for targeting purposes: Snap (NYSE:SNAP).

To be sure, Snap does have a hardware business through Spectacles. But that business has struggled to gain traction, and revenue from Spectacles thus far has been immaterial. Thus, of Snap’s $1.2 billion in revenue last year, almost all of it was from digital ads. That means almost all of it would be theoretically subject to a data dividend.

Again, this isn’t a deal breaker for Snap. But it is a bigger concern for Snap than it is for Facebook and Twitter. Why? Because Facebook and Twitter are already profitable, and they can absorb a 2% hit on revenues without materially impacting profitability. Snap cannot. The company is far from profitable, and needs a lot more scale in order to be profitable. Thus, the data dividend risk is much bigger for SNAP stock, than it is for FB or TWTR stock.

Alphabet (GOOGL,GOOG)

Data-Related Revenue (% of Total Revenue): $116 billion (85%)

The first non-social media company on this list also happens to be the world’s largest digital advertiser, and therefore bears substantial exposure to a potential data dividend.

Alphabet (NASDAQ:GOOG,GOOGL) isn’t all digital advertising. The company has hardware, cloud, and AI-related businesses which aren’t built on the back of user data. But Alphabet is mostly digital advertising. Of the company’s near $140 billion in revenue last year, about 85% of it came from digital advertising through Google, YouTube, and other online ad networks and properties. Thus, if a data dividend were to be implemented, Alphabet would have to pay a large sum back to consumers.

This isn’t a big deal for GOOG stock. For starter’s, Google is the backbone of the internet, and YouTube is very sticky in the free, online entertainment world. Neither of those ad businesses will be hit that hard by a data dividend. Also, of all major digital advertising players, Alphabet is the one of the most diversified, with burgeoning businesses in cloud, hardware, and AI.

Overall, then, any negative impact on GOOG stock from a data dividend will be mitigated by growth drivers elsewhere in the business.

Yelp (YELP)

Data-Related Revenue (% of Total Revenue): $907 million (96%)

Another company impacted by a potential data dividend isn’t known as a digital advertising giant, yet still derives a majority of its revenue from digital ads that leverage user data.

Yelp (NASDAQ:YELP) reported net revenue of roughly $943 million last year. About $907 million of that, or 96%, was from digital advertising. Thus, although Yelp doesn’t serve consumers ads in the same way that Facebook, Twitter, or Snap do, the company still runs ads based on user data, and those ads are the big driver of the company’s business. Consequently, a data dividend would theoretically be applied to Yelp’s entire business.

A data dividend is just another risk to add to the long list of things not to like about YELP stock, including valuation, competition, slowing growth, lack of scale, and lack of a moat. As such, there’s simply too much not to like here. The data dividend risk is just another reason to stay away from YELP stock.

Amazon (AMZN)

Data-Related Revenue (% of Total Revenue): $10 billion (~4%)

Although the next company on this list also isn’t known as a digital advertising giant, it is quickly building out a giant digital advertising business which is theoretically subject to a data dividend.

Amazon (NASDAQ:AMZN) isn’t known for digital ads. The company is known as an e-commerce and cloud giant. Nonetheless, Amazon is leveraging its huge user-base and reach across Amazon, IMDb, and other digital properties to create a huge and rapidly growing digital ad business. That digital ad business generated $10 billion in revenue last year. To be sure, that’s less than 5% of Amazon’s total revenues. But it’s a much bigger portion of profits (digital ad sales have way higher profit margins than e-commerce sales).

That fact alone is why the data dividend is actually a sizable risk for AMZN stock. Amazon has been counting on ramp in the digital ad business to drive profits higher, while margins in the e-commerce business remain largely weak due to competition. If the digital ad business gets set back due to a data dividend, that would be a set back to the whole Amazon profit growth narrative. As such, while the data dividend risk isn’t a deal-breaker, it is something which AMZN investors should closely monitor.

Microsoft (MSFT)

Data-Related Revenue (% of Total Revenue): More than $12 billion (more than 11%)

Last, but not least, is another big tech company which isn’t known for digital ads, but which nonetheless is one of America’s largest digital advertisers, and consequently has broad exposure to a potential data dividend.

Microsoft (NASDAQ:MSFT) isn’t known for digital advertising or using personal data to generate revenue. Still, the company has a big digital ad business. Microsoft’s search advertising revenues measured $7 billion last year. LinkedIn revenues were around $5.3 billion. The company also makes ad revenue through other segments, but doesn’t break that out. Thus, Microsoft’s total data-related ad revenues measured in excess of $12 billion last year, and likely closer towards $15-20 billion. That would represent about 15% of Microsoft’s total revenues.

Because Microsoft isn’t known for digital advertising, the data dividend risk isn’t a big deal for MSFT stock. The big growth narrative here is cloud, not digital ads. Thus, Microsoft can afford a set back in the digital ad business, so long as the cloud business remains healthy. At the end of the day, as go the cloud businesses, so goes MSFT stock.

As of this writing, Luke Lango was long FB, TWTR, GOOG, and AMZN.

The Big Dance is just around corner. I’m talking about March Madness, of course. The winner-take-all, single-elimination tournament to decide the champion of the 2019 NCAA Men’s Basketball season. Millions of viewers. Sixty eight teams. Dozens of venues. Six rounds. One winner.

Some call it the most exciting times of the year for sports fans. It may be. But the fact that the stock market tends to perform really well during March Madness isn’t up for debate. Stocks often tend to rise during the March Madness tournament, which spans throughout all of March and spills into April. They also tend to rise during that stretch by more than any other stretch during the year.

Maybe it’s just a coincidence. Maybe not. But, there are unarguably a handful of March Madness stocks which do directly benefit in a big way from the Big Dance.

Which stocks fall under that umbrella? Let’s take a look at seven March Madness stocks to track as the Big Dance plays out in March and April.

March Madness Stocks to Watch: Nike (NKE)

Of all March Madness stocks, the one to watch most is Nike (NYSE:NKE).

The athletic apparel giant has its fingertips all over the Big Dance. Nike consistently outfits somewhere north of 40 of the 68 teams that play in March Madness, representing about 60% of the tournament’s participants. That means that six out of every 10 jerseys, shoes, warm-ups and more in March Madness sports a Swoosh or Jumpman logo. So, for the millions of viewers who tune into March Madness every year, the Nike brand is everywhere. It also helps that this year’s top four teams (Gonzaga, Virginia, Duke and Kentucky) are all Nike schools.

Of course, this is huge for Nike basketball mind-share. That’s big for Nike’s entire business. Nike dominates the basketball market, and this dominance is a big driver behind Nike’s nearly $40 billion revenue base. As such, continued dominance in basketball will keep Nike atop the entire the athletic apparel market.

Adidas (ADDYY)

Although Nike is king in the basketball market, Adidas (OTCMKTS:ADDYY) is gradually making moves in this market which are becoming increasingly apparent during March Madness.

In 2015, Adidas outfitted just 11 of the 68 teams in March Madness. In 2017, Adidas outfitted 15 of the teams. This year, that number could very well be higher. Importantly, one of the nation’s top teams — Kansas — is an Adidas school.

As is the case for Nike, basketball is a huge market for Adidas, and a healthy presence in the Big Dance is a net positive for Adidas basketball mind-share. The benefits here are smaller than they are over at Nike, given smaller overall presence. But, if an Adidas team makes some serious noise in the Big Dance (like Kansas), then that could be a huge medium to long term win for ADDYY stock.

Under Armour (UAA)

When it comes March Madness stocks and athletic apparel brands, Nike is king, Adidas is a solid second place and Under Armour (NYSE:UAA) is the dark horse with a lot of potential.

Back in 2015, Under Armour outfitted just six of the 68 teams in the Dance. In 2017, that number doubled to 12. This year, that number could be even bigger. Texas Tech, an Under Armour school, has a fringe-top-10 basketball team this year. Meanwhile, both Maryland and Wisconsin — also Under Armour schools — are top 20 teams, and Cincinnati is a top 25 team. Thus, Under Armour has four teams this year which could make some serious noise in March.

If any of them do, that could be big for UAA stock. Under Armour has struggled in the basketball market ever since early red-hot success with NBA superstar Steph Curry faded. Surprise college basketball success in the 2019 Dance could reinvigorate the now-stalled-out Under Armour basketball growth trajectory. If it does, that could create sizable tailwinds for UAA stock.

CBS (CBS)

Any discussion of March Madness stocks would be incomplete without CBS (NYSE:CBS), the network which hosts a healthy portion of the Dance’s 63 nationally televised games, including the most watched ones.

March Madness coverage averages millions of viewers per game, and most data indicates that those numbers are only going up. A healthy majority of those games air on CBS. Moreover, viewership goes up as the tournament narrows down, and some numbers point to the final games in the Big Dance averaging 15 million-plus viewers. All those final games are televised through CBS.

As such, CBS has a lot to gain through ad revenue and partnerships during March Madness. There’s reason to believe this year will have unusually large March Madness viewership, given the plethora of young talent across college basketball this year, the extreme level of parity among the teams, and the enormous hype surrounding college basketball’s best player, Zion Williamson. If March Madness does score unusually large viewership ratings this year, the biggest winner will be CBS stock.

AT&T (T)

There are 63 nationally televised games in March Madness. CBS doesn’t air all of them. In fact, a majority of the tournament’s early games are aired by Turner Sports, which is owned by AT&T(NYSE:T).

Through TBS, TNT and truTV, Turner Sports actually airs a majority of March Madness games in the first and second rounds, as well as half the games in the Sweet 16 and Elite 8. To be sure, those games average less viewers than the Final Four and Championship Game. Nonetheless, they still average millions of viewers per game, and represent a sizable ad revenue opportunity for AT&T.

As stated earlier, this year’s Dance could have unusually large viewership due to various factors, one of which is an unusually large amount of parity among this year’s field of teams. Higher parity usually lends itself to closer early round games, and also more upsets. That usually lends itself to higher viewership in the earlier rounds. As such, AT&T could actually be a big March Madness winner this year.

Coca-Cola (KO)

One company that consistently has its finger tips all over March Madness is Coca-Cola(NYSE:KO).

The beverage giant is one of the Dance’s official NCAA Corporate Champions, and that means that Coca-Cola TV ads and in-arena ads will be all over the place during March Madness. That’s a win for mind-share. It’s also worth noting that Coca-Cola owns Powerade, the sports drink brand which is typically front-and-center during the entire March Madness tournament.

This year is especially important for Coca-Cola. The company is under intense pressure regarding the health of some of its core drinks, including the staple Coca-Cola carbonated beverage. Thus, it has an opportunity this year to reduce that pressure via effective March Madness marketing. If they do, sales in North America could get a nice lift, and that could power gains in KO stock for the rest of the year.

Calendar 2018 was a big year for initial public offerings, or IPOs. The number of IPOs in 2018 rose more than 20% year-over-year to nearly 230, the highest mark since 2014 and the third highest mark over the past ten years.

Yet, there’s reason to believe that 2018 was just the beginning of a multi-year IPO boom. Here’s the thing about the IPO market: it runs in cycles. Multiple consecutive years of low IPO volume are followed by multiple consecutive years of high IPO volume. From 2015 to 2017, we had three years of below-average IPO volume. Calendar 2018 broke that trend with 200-plus IPOs. History tells us that 2019 and 2020 should be more of the same.

Indeed, calendar 2019 should be one for the record books in the IPO market. The list of potential 2019 IPOs is long, diverse, and includes some of the biggest and fastest growing private companies. Those companies promise to make an unforgettable splash when they go public later this year.

More than that, I think many of these IPOs will be extremely successful. The batch of companies going public this year include the batch of companies that were birthed out of the Financial Crisis a decade ago. They are disruptive and innovative, and cut from a different cloth than current public companies. Most importantly, most of these companies are employing coordinated economic principles to give power back to the people, and in so doing, are aligned with the biggest trend of the century.

As such, not only does the 2019 IPO market project to be one for the record books, but it should also yield some big winners. With that in mind, let’s take a look at a list of seven IPOs that investors should be excited for in 2019.

Uber

At the head of this list is Uber, the ride-sharing company which has already entirely disrupted the transportation industry.

Investors should be excited about the Uber IPO because this company has truly optimized transportation services, and in so doing, has established a massive driver base which will be hard for anyone else to replicate, and from which multiple valuable business opportunities can be created. In a nutshell, Uber is the quintessential coordinator. Before Uber, transportation services were performed by the few (namely, taxis). Uber democratized the supply of transportation services, and said anyone with a car can now perform this service, creating a surge in supply. Uber coordinated that supply, so that it would satisfy demand-side expectations. Net result? Supply caught up to robust demand, price points fell, and convenience went up. Uber won.

Now, Uber has a driver base that numbers several million globally. Uber can use that unparalleled driver base to optimize price and convenience in other transportation-related industries, such as delivery and last-mile logistics. The sum potential of all these industries numbers in the hundreds of billions of dollars, and potentially even in the trillion dollar range if Uber wins the race to self-driving. As such, while Uber’s rumored $120 billion IPO valuation may drop some jaws, it’s worth it.

Lyft

Uber isn’t the only ride-sharing company going public in 2019. In fact, before Uber ever hits public markets, its competitor Lyft should have already spent a few months on Wall Street.

Lyft is planning to launch its IPO roadshow in mid-March. That means that by the summer of 2019, Lyft should be a publicly traded company. That’s exciting news. Much like Uber, Lyft is a quintessential coordinator who has helped democratize and coordinate supply in the transportation industry to meet robust demand. In so doing, Lyft has huge opportunities in front it to not only become a solid second player in the ride-sharing market, but also the number one or number two company in a plethora of other transportation-related markets.

The attractive thing about the Lyft IPO is that the valuation is rumored to be under $25 billion. That is just a fraction of Uber’s valuation. To be sure, Uber is much bigger than Lyft in terms of total revenues and rides. But, Lyft is supposedly growing much more quickly than Uber, and the company has largely avoided negative press (much unlike Uber). Consequently, investors should be excited about the upcoming Lyft IPO, given its discounted valuation relative to Uber and that the company is apparently gaining share in ride-sharing.

Airbnb

The coordinated economy hasn’t just hit the transportation industry. It has also hit the accommodations industry, thanks to Airbnb, who also projects to go public in 2019.

Much like Uber, Airbnb has become a quintessential coordinator. Before, accommodation services were provided by the few (namely, hotels). Airbnb democratized supply in that market, and said that anyone who has an extra room or living space can rent it out for accommodation purposes. Supply surged. Airbnb coordinated that supply to satisfy demand-side expectations. Consequently, supply caught up to demand, prices fell, and convenience rose.

Much unlike Uber, however, Airbnb doesn’t have any big second competitor that is also set to IPO in 2019. Thus, the competition landscape for Airbnb is quite attractive for the foreseeable future. Also, Airbnb is in an optimal position to jump into other accommodation-related industries, like the travel and car rental industries, meaning the long term opportunity here is quite large.

Postmates

Following in the footsteps of Uber, Postmates took those same coordinated economy principles and applied them specifically to the delivery process.

While you may be inclined to compare Postmates to food-delivery services including UberEatsand GrubHub (NYSE:GRUB), that’s not entirely accurate. Postmates will also deliver items from local stores such as groceries, alcohol, and other items–making for a nice moat. (Though for these other items, they may eventually have to compete with the likes of Amazon(NASDAQ:AMZN), which is no joke for any company, but for now, same-day delivery isn’t widespread and it isn’t under an hour or so wait time.) But the (prepared) food-delivery market will be really big one day (like $100 billion-plus big), and Postmates is maintaining steady double-digit market share. Plus, the current valuation on Postmates is reasonable ($1.85 billion).

Thus, in the big picture, Postmates is a solid growth company in a big growth industry. There’s some competition, but the valuation reflects those competitive risks, and is actually quite attractive considering the market growth potential. As such, the Postmates IPO is one to watch for later this year.

Pinterest

The last big social media app to IPO was Snap (NYSE:SNAP). That didn’t go too well. But, there’s reason to believe that the next big social media app to IPO, Pinterest, will have a different outcome.

Snap struggled for three reasons. The user base fell flat, engagement proved difficult to monetize, and margins were weak. Pinterest won’t have those problems. The platform has about 250 million monthly active users, and is growing that base at a fairly consistent 50 million new users per year. Also, given Pinterest’s curation focus, data indicates that engagement on the platform can be very easily monetized, as consumers are already using Pins to influence purchasing behavior. Perhaps most importantly, Pintrest’s gross margins are north of 45%.

All in all, Pinterest looks positioned for big success on Wall Street. User growth is healthy. Engagement is easily monetized. Margins are high. There’s a lot to like here, meaning that Pinterest stock will likely have a much better start on Wall Street than Snap stock.

Pinterest filed for IPO at the end of last week, seeking a valuation of at least $12 billion.

Slack

If you thought social networking was exclusive to the personal level, think again. Enterprise social networking, or ESN, is a rapidly expanding industry, and at the heart of all that growth is Slack, yet another company set to IPO in 2019.

One aspect of the cloud tech boom is the growing demand for enterprise cloud solutions tailored to addressing intra-business communication and workflow needs. ESN is the market which addresses those needs, as it includes a portfolio of platforms which allow for seamless intra-business communication and workflow sharing. The most popular of those platforms is Slack, which has gone from 365,000 daily active users to 10 million daily active users in just four years. Indeed, some say Slack is the fastest growing software-as-a-service (SaaS) company ever.

Going forward, there are two important things to note here. One, demand in the ESN space will only continue to grow. Two, Slack has beaten out competition from Facebook (NASDAQ:FB) in this space. As such, Slack has a proven ability to beat top-quality competition in a big growth market. That positions the company for robust growth for a lot longer, which roughly translates into Slack stock doing well on Wall Street.

Palantir

Peter Thiel is an important and impressive guy. He co-founded PayPal (NASDAQ:PYPL), and was the first major outside investor at Facebook. Now, his latest venture, Palantir (which Thiel founded in 2003), is set to go public in 2019.

At its core, Palantir provides solutions which enable companies of all sizes to make sense of big data. This is a very important service. Big data is of increasing importance when it comes to enterprise decision making. But, the quality of insights device from big data relies on the quality of analysis done on that big data. That’s where Palantir excels — providing the best of the best analysis on such data.

The long-term outlook for Palantir looks good. So long as data becomes increasingly important, Palantir’s services will have growing demand. The only big concern is competition. But, this market projects to be so big one day that it will support multiple players at scale. Consequently, the Palantir IPO should be successful.

As of this writing, Luke Lango was long GRUB, FB, and PYPL.

[Editor’s note: This story was originally published in August 2018. It has since been updated and republished.]

The stock market’s volatility in recent months has not made me less bullish on the five cheap stocks profiled in this article. Among these stocks, market movements can cause some noise. But the investment thesis on cheap stocks is predicated on huge moves higher in the long-term. Thus, in the near-term, macro-driven movements amount to nothing more than a sideshow.

From this perspective, now might be a good time to pile into some stocks under $5. These stocks are a high-risk bunch. But they do have high-reward potential, too.

With that in mind, here is a list of five cheap stocks, which I think have big upside potential.

Source: Shutterstock

Pier 1 (PIR)

PIR Stock Price: 88 cents

Furniture retailer Pier 1 Imports (NYSE:PIR) has had a tough time getting its act together for several years.

Peer Restoration Hardware (NYSE:RH) has seen its stock rise 30% over the past year thanks to a red-hot housing market and robust demand for home furnishings. PIR stock, however, has collapsed during that same stretch. These problems aren’t new. Over the past five years, this stock has lost more than 90% of its value.

Having said that, there is visibility for a turnaround in PIR stock in the near future.

At its core, Pier 1 has been killed by rising e-commerce threats creating huge pricing and traffic headwinds. Pier 1, which stands somewhat square in the middle of price and quality, doesn’t really have anything special about the business to protect against these headwinds. Consequently, sales and margins have dropped in a big way.

But, the company has a three-year strategic plan to turn the business around. The plan includes bigger investments in omni-channel commerce capabilities and marketing.

No one knows whether this plan will actually work. But home furnishings is a market with enduring demand, so that helps.

Meanwhile, PIR stock is dirt cheap. This company used to have earnings power of $1 per share. Even half of that earnings power (50 cents) would be huge for a stock trading under $1. At 50 cents per share in earnings power, it wouldn’t be unreasonable to see this stock hit $8 (a market-average 16x multiple).

Source: Shutterstock

Groupon (GRPN)

GRPN Stock Price: $3.50

Much like Pier 1, savings-king Groupon (NASDAQ:GRPN) feels like one of those companies that were loved yesterday but will be forgotten tomorrow. But I don’t think that’s true. I get that the savings and deals market is commoditized now. I also understand that Groupon really isn’t a household name for coupons like it used to be.

But I’m a numbers guy. And Groupon’s numbers are pretty good. Its margins are improving thanks to management’s focus on higher-margin businesses. Operating expenses are also being removed from the system, so the company’s overall profitability profile is improving.

Aside from the numbers, Groupon launched an aggressive advertising campaign last year with hyper-relevant Tiffany Haddish that scored just shy of 100 million views. I think this campaign will have a long-term positive effect on usage, which could drive the stock higher.

Put it all together, and it looks like GRPN stock could have a big-time rally in 2019.

Note: ZNGA stock rose over $5 since this article was originally published.

I’m not a huge fan of the mobile gaming sector. It’s a tough space plagued with competition and low margins. Plus, competition is only building thanks to social media apps becoming increasingly multi-purpose.

But mobile gaming company Zynga (NASDAQ:ZNGA) seems to have found the key to success in the mobile gaming world.

Zynga used to be a mega-popular browser game company with tons of users. But then the company overreached by branching into games that had heavy overlap with the traditional video game market, like sports titles. They couldn’t compete in that market. Eventually, the over-extension sparked user churn, and ZNGA stock spiraled downward.

That forced Zynga to re-invent itself into something much more relevant and defensible. They did just that. Zynga has transitioned its business model from web-focused to mobile-first while narrowing its gaming title focus. This pivot has streamlined operations, re-invigorated top-line growth, cut costs and improved profitability.

Consequently, the numbers supporting Zynga are pretty good. In Q4, its revenue rose 7% year-over-year and its bookings jumped 19% YoY. Finally, its operating cash flow soared 241%.

From where I sit, this pivot appears to be in its early stages. Mobile is a secular growth narrative, and ZNGA has developed a gaming portfolio that is focused and tailored to that growth narrative. Thus, so long as mobile engagement heads higher, Zynga’s numbers should get better. Better numbers will inevitably lead to a higher stock price.

There is no hiding the fact that the defense sector has been hot under President Trump.

Trump came into office, upped the ante on defense and military spending, and in response, the whole world is spending more on defense and military.

Defense contractors win when this happens. That is why mega-cap defense contractors like Lockheed Martin (NYSE:LMT) and Boeing (NYSE:BA) have been on fire for the past several quarters.

But one micro-cap defense contractor that has missed out on this rally is Arotech (NASDAQ:ARTX). Over the past several years, the financials at Arotech haven’t gained any ground. Five years ago, its revenues were $103.5 million and its net income was $3.5 million. In 2017, its revenues were $98.7 million and its net income was $3.8 million.

In other words, its profits haven’t risen much in five years. When profits don’t go up, the stock tends not to go up. It is a simple relationship.

But its profits are stabilizing. When profits go from declining to stabilizing, they usually go to growth next.

And, when profits go up, stocks tend to go up.

As such, it looks like Arotech is finally joining the tide when it comes to big boosts in defense and military spending. This tide will inevitably lift Arotech’s earnings power substantially, and ARTX will rally as a result.

Source: Shutterstock

Blink Charging (BLNK)

BLNK Stock Price: $3.05

When it comes to cheap stocks, there are few as volatile as Blink Charging (NASDAQ:BLNK).

Over the past two years, BLNK stock has gone from $10 to $3, and popped from $4.50 to $8 … it now sits at a paltry $3.04. This volatility won’t give up any time soon. Thus, if you want to avoid volatility, I’d say avoid BLNK stock.

That being said, if this company’s secular growth narrative surrounding building a network of electric vehicle charging stations globally materializes within the next five years, this stock could be a 5-to-10 bagger.

It is a big risk. But, eventually, global infrastructure will need to match demand. At that point in time, there will be some huge contracts awarded to electric vehicle charging station companies.

Will Blink be one of them? Perhaps. Tough to tell. But if they do land some big contracts, this stock could have another huge pop in a short amount of time.

As of this writing, Luke Lango was long FB, PIR, GRPN and ARTX.

On April 7, 2017, Tesla (NASDAQ:TSLA) stock cleared $300 for the first time. Tesla stock would close that day at $302.54. Yesterday, TSLA stock closed at $302.56.

Source: Shutterstock

Over the last 22+ months, TSLA stock has risen… 0.07%. Given the intensity of the debate over TSLA — without a doubt the biggest battleground stock in the market — the lack of movement is beyond ironic.

Where does Tesla stock go from here? There are cases on both sides. I’ve long leaned toward the bearish case: I argued in December that TSLA would decline in 2019. That prediction has been right so far, with the stock down 9%. But Tesla has managed to confound the doubters so far, and there are still reasons to believe it will do so again.

The Case for Tesla Stock

At this point, the bull case for TSLA has both short-term and long-term aspects. The long-term case is the same as it’s been for years now: Tesla has the opportunity to revolutionize worldwide energy usage. The company isn’t just about the Model 3 — or even just about automobiles. The solar division, Powerwall, and other future initiatives all offer additional profit opportunities.

A $52 billion market capitalization hardly suggests Tesla stock is cheap, but it’s puny compared to what the valuation could be if Tesla achieves even some of its goals across the energy space. ARK Invest famously has put a $4,000 per share bull case price target on TSLA stock — which would suggest a valuation over $500 billion. Given that Exxon Mobil (NYSE:XOM) is worth about $375 billion, including debt, that figure perhaps isn’t as ludicrous as it sounds.

In the short term, meanwhile, Tesla stock is getting to a point where it doesn’t look that expensive. 2020 analyst EPS estimates are over $9 per share, suggesting a 33x forward P/E multiple. That’s a big number as far as auto stocks go — General Motors (NYSE:GM) and Ford Motor Company (NYSE:F) both trade in the single digits — but it’s a valuation that Tesla at least can grow into. As the company expands into Europe and China, its earnings should grow, and that multiple should come down.

The Case Against TSLA Stock

The case against Tesla stock is starting to build, however, and it comes down to one simple problem: trust. For all the arguments over convertible debt maturities and 25% gross margins and weekly production levels, the broad argument is rather simple.

If Tesla can build cars more effectively and more efficiently than existing manufacturers, TSLA stock probably rises. It will make more money per car than anyone else — and enough to fund its moves into semi trucks, energy storage, and other areas.

If it doesn’t, TSLA stock falls. Auto companies aren’t valued at 30x earnings — or even 20x. Earnings expectations come down, multiples compress, and the Tesla stock price comes down significantly. And so far, we’re simply not seeing much evidence that Tesla is that much better than anyone else at production.

Tesla hasn’t released a $35K Model 3 yet, as promised. It built vehicles in a tent. Target after target has been missed. For all the hype about the 5,000 per week production target (sort of) reached in late June, Tesla hasn’t been able to get back to that level on a consistent basis.

There’s a lot of big talk and big promises out of Tesla. The results — thin profitability and missed goals — haven’t been good enough yet.

The Trust Problem

And with each passing month, it becomes harder to trust Tesla and CEO Elon Musk. Musk clearly violated his settlement with the SEC with Tweets this week initially guiding for production of 500,000 cars this week.

The CEO did correct the tweet four hours later, admittedly. But for those bulls chalking the Tweet up to a simple mistake, it’s worth noting that Musk did the exact same thing on the Q4 conference call last month. He projected 350,000 to 500,000 Model 3s in 2019 — after the shareholder letter issued the same day only guided for 360,000 to 400,000.

At this point, investors perhaps don’t care. Soon after the tweet, Tesla’s general counsel resigned after two months on the job, the latest in a series of executive departures. TSLA stock dropped just 1%.

Investors should care, however. Given the goals here, execution needs to be close to perfect at worst. It hasn’t been. A CEO who continually overpromises doesn’t help on that front. Nor does the revolving door of executives.

The biggest reason to see upside in Tesla stock is the big promises — and the big hopes. The biggest risk to TSLA stock is that the company won’t deliver. For 22 months, the market hasn’t made up its mind as to which is more likely. At some point, it will. Right now, it still seems far too difficult to trust this company — and this CEO — to deliver the rewards they promise.

As of this writing, Vince Martin has no positions in any securities mentioned.

So far this year, the average tax refund amount is down about 8.4% to $1,865. As should be no surprise, this has stirred up quite a bit of disappointment. A tax refund is often an important part of people’s spending.

Well, this is true. However, even though the withholding levels were lowered, they did not account for some of the key changes in the tax code. The result is that for many Americans there was not enough money withheld from their paychecks.

So what to do to boost your tax return? Unfortunately, the tax law has also cut back on many tax breaks. Here are just some examples:

Personal exemptions have been eliminated

Moving expenses can no longer be deducted

Miscellaneous itemized deductions have been eliminated

State and local tax deductions have been limited to $10,000

Despite all this, there are still benefits available and strategies to pursue. So let’s take a look:

Tax Refund Strategy: IRA and HSA Contributions

One of the best tax breaks is the IRA (Individual Retirement Account). It not only provides a lucrative deduction (whether you take the standard deduction or itemize) but is also a great vehicle for savings. The presumption is that when you reach retirement your withdrawals from the account will be at a lower tax rate.

Something else to consider: You can make a contribution by April 15th of this year. This can then be included on your 2018 tax return.

The maximum contribution amount for an IRA is $5,500 per person and this must be based on earned income. But if you are 50 or older, this goes up to $6,500.

Yet there are some wrinkles. If you are eligible for a company retirement plan, then the deduction may be limited or disallowed. This is based on your income.

OK then, what about a Roth IRA? Can this boost your refund? The answer is no. While a Roth IRA has nice tax benefits (withdrawals are not taxed) you do not get deductions for the contributions.

Finally, you can setup a Health Savings Account or HSA, which allows for tax benefits when paying for medical bills. Like an IRA, the deadline for contributions is April 15th.

Tax Refund Strategy: Filing Status

What you indicate as your filing status on your tax return can make a big difference. Keep in mind that the new tax law made some significant changes with the standard deduction levels, which now include the following:

Single: $12,000

Head of Household: $18,000

Qualified Widow(er) $12,000

Married Filing Jointly $24,000

Married Filing Separate $12,000

The rules for filing status can get complicated, especially with the Head of Household designation. You will need to understand the costs of maintaining the household and what types of dependents qualify (which may include parents who do not live with you). But it is worth evaluating.

Another strategy is to compute your tax return using different filing statuses. And yes, may be surprised by the results. Consider that filing separate could mean bigger tax savings if you or your spouse has substantial medical expenses.

If anything, all this is a good reason to get some advice from a tax professional, say by setting up an appointment at H&R Block (NYSE:HRB) or seeking out a local CPA or Enrolled Agent. The tax benefits could easily exceed the fee.

Tax Refund Strategy: Credits

A tax credit is can go a long way to boosting your refund. The reason is that you get a dollar-for-dollar reduction of your tax liability. A deduction, on the other hand, is subtracted from your income, which is then subject to a potential tax.

There are a variety of credits available, such as for education (American Opportunity Credit) and lower income households (Earned Income Tax Credit). But they do require some research and record keeping.

The new tax law also has improved the Child Tax Credit, so as to help make up for the elimination of the personal exemption. It has been increased by $1,000 to $2,000 for a qualifying child who is under 17.

There is also a personal credit of $500 for the taxpayer, spouse and other dependents that are not eligible for the Child Tax Credit. These credits phase out at $400,000 in income for joint filers and $200,000 for all other taxpayers.

Tom Taulli is an Enrolled Agent and also operates PathwayTax.com, which is a tax advisory and preparation firm. Follow him on Twitter at @ttaulli. As of this writing, he did not hold a position in any of the aforementioned securities.

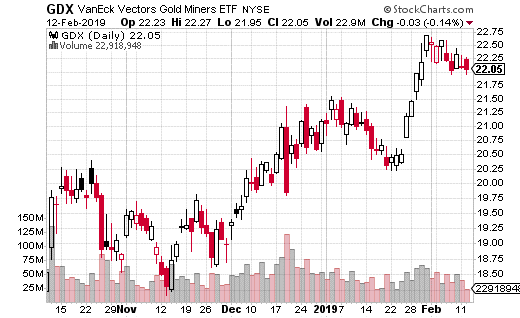

One of the unsung stories of the last few months is the resurgence in gold prices. An ounce of gold has climbed from a low of about $1,200 in mid-November to over $1,300 as of this writing. That’s a pretty sizable jump in a relatively short amount of time.

There are a few reasons why gold may be on the move higher. At least part of it could be due to the amount of overall uncertainty we’ve seen this year – with plenty of unresolved issues remaining at the macro level. But perhaps more importantly, the Fed’s commitment to keeping interest rates low could lead investors to believe that inflation is going to surface anytime now.

Since gold is considered a decent hedge against inflation, it may be a big part of why the rally has occurred. (Gold is actually a better hedge against deflation than inflation, but generally speaking, uncertainty over future currency levels leads to more demand for gold).

Along with gold itself, gold miners have also benefited from the renewed interest in precious metals.

VanEck Vectors Gold Miners ETF(NYSE: GDX) is a widely popular method for investing in gold miners. The ETF invests in the biggest gold miners that trade in the US and Canada. About 60% of the fund’s holdings are invested in the top 10 names in the industry.

GDX trades nearly 50 million shares a day on average – making it one of the most heavily traded ETFs. It also averages about 85,000 option contracts per day. Very few other ETFs or stocks can beat that average.

Gold miners have the advantage of tracking gold but also producing an income stream. That makes them a bit more palatable to many investors in comparison to the commodity itself. Not to mention, GDX even offers a dividend, something gold bullion can’t ever do.

A fund or well-capitalized trader just rolled out 10,000 GDX calls to May, suggesting gold miners could be in for a big rally over the next 3 months. The trade itself was the purchase of the GDX May 17th 22 calls for $1.22 with the stock trading at $22.15 per share.

At 10,000 contracts, it means the trader spent $1.2 million in premium, which is obviously a strong commitment to GDX’s upside. That’s because the premium is the max loss potential on the trade, so if GDX is under $22 at May expiration, the calls will be worth zero.

That sort of confidence in GDX’s upside also suggests that gold and gold miners are going to maintain the gains they’ve seen over the last month or so. Of course, the call buyer is looking for more than just sideways movement. For every dollar above the breakeven point of $23.22, the trade pulls in $1.2 million in profits.

If you’re bullish on gold miners, you could make this same trade. Or, if you want to save some money and do a similar trade, you could turn the trade into a call spread instead. With GDX trading at around $22, the 22-24 May call spread is trading for about $0.70.

That lowers the breakeven point to $22.70 and your max loss is down to $0.70 per spread. You max gain is capped at $24 or above in the stock, which is $1.30 after accounting for the cost of the spread. Still, that’s 186% potential gains for a relatively inexpensive trade that covers the next three months.