Sometimes identifying the best stocks to buy can be difficult, but you could do a lot worse than checking out the stocks selected by one of the world’s savviest hedge fund managers — Warren Buffett.

Buffett’s stock picks are a popular source for investors, and for good reason. The billionaire Buffett is many things: He’s among the world’s most successful fund managers, a legendary philanthropist and owns more than 60 companies.

Buffett’s formidable stock-picking ability has given him the nickname “the Oracle of Omaha” and a fortune of more than $87 billion. And now we can track the latest trades of his $191 billion Berkshire Hathaway fund.

Just-released SEC forms reveal a valuable glimpse into stocks Buffett likes (and the stocks Buffett doesn’t like). These are the stocks he poured money into in the second quarter.

Here I also include TipRanks’ stock insights from Wall Street’s best-performing analysts. Does the Street sentiment match Buffett’s latest stock picks — or is he going rogue with his investing decisions? Let’s take a closer look at the top Warren Buffett stock picks now:

Editor’s Note: This article was originally published on Aug. 17, 2018. It has been updated to reflect changes in the market.

Apple (AAPL)

Source: Shutterstock

Apple (NASDAQ:AAPL) is now by far and away Buffett’s largest investment. After missing the tech sector rally (Buffett recently admitted that he “blew it” by not investing in Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) earlier), the Oracle of Omaha has been busy plowing money into AAPL.

Following a 5% increase of AAPL shares, Buffett now holds over $55 billion in AAPL stock. This is about 24% of the total portfolio. Interestingly, it also means Buffett now owns almost 5% of Apple stock.

“I clearly like Apple. We buy them to hold,” Buffett told CNBC in May. “We bought about 5 percent of the company. I’d love to own 100 percent of it … We like very much the economics of their activities. We like very much the management and the way they think.”

And the stock also has the Street’s seal of approval. “Despite Apple achieving the $1 trillion milestone last week, we continue to believe Apple remains one of the most underappreciated stocks in the world with a valuation that remains depressed (13.7x our CY:19 EPS estimate, ex-cash)” cheers top Monness analyst Brian White (Profile & Recommendations).

He added: “Now, Apple is heading into the seasonally strongest time of the year with a new iPhone cycle on the horizon.” Indeed, White’s $275 price target indicates big upside potential of 24%.

In total, however, the stock has a “moderate buy” analyst consensus rating. This is with a $214 price target. See what other Top Analysts are saying about AAPL.

US Bancorp (USB)

Source: Shutterstock

Minneapolis based U.S. Bancorp (NYSE:USB) is the fifth largest U.S. bank — and one of the top 10 holdings in the Berkshire portfolio. Following the purchase of almost 10 million USB shares in Q2, Buffett’s USB stake now totals $5.3 billion.

However, Oppenheimer’s Chris Kotowski (Profile & Recommendations) is less convinced. Interestingly, given Buffett’s preference for value stocks, it’s the valuation this top analyst takes issue with. He writes: “USB is one of the “super banks” of the banking industry, and while there is a lot to like about the stock, we think the valuation already embeds it.”

As a result, Kotowski has a “hold” rating on the stock, and tells investors to look elsewhere. “USB is not cheap on either a P/E or price/TBV basis versus peers; given the plethora of cheaper, high-quality franchises trading at a fraction of USB’s TBV multiple, we think there is more upside potential elsewhere in the sector.”

The overall Street perspective also leaves a lot to be desired. In the last three months, the stock has received four hold ratings. This is versus only two more bullish Buy calls. Meanwhile, the average price target stands at $57 (8% upside potential). See what other Top Analysts are saying about USB.

Bank of New York Mellon (BK)

Source: Shutterstock

Buffett has now ramped up his holding of this financial stock by 4% to $3.2 billion. This makes Bank of New York Mellon Corp (NYSE:BK) the tenth-biggest stock in Berkshire’s portfolio. Although Buffett has held BK since 2010, he began to pour money into the stock in 2017 with two 50% increases. Since then, it has been a constant build up.

Analysts, on the other hand, are evenly divided between Hold and Buy. One five-star analyst in the bull camp is Vining Sparks Marty Mosby (Profile & Recommendations). He sees a compelling investment opportunity right now. “BK currently trades at a 13x price-to-earnings multiple, and we believe its expected earnings per share growth could reduce its multiple down to below 12x. We believe this valuation is too low for a bank currently producing 25% return- on-tangible common equity.”

He concludes, “As a result of earnings growth, multiple expansion, and a 2.1% dividend yield, we are targeting over 15% total shareholder return over the next 12 months.” See what other Top Analysts are saying about BK.

Delta Airlines (DAL)

At the end of 2016, Buffett shocked the market with huge investments in four key airline stocks. Only a few years ago, Buffett called the sector a “death trap for investors.” However, with the industry fast consolidating, he decided to change his tune.

Buffett’s partner, Charlie Munger, explains “It (the railroad industry) was a terrible business for 80 years … but they finally got down to four big railroads, and it was a better business. And something similar is happening in the airline business.”

And one of the four stocks to buy that he particularly likes is Delta Air Lines (NYSE:DAL). A further $559 million investment in Q2 means Buffett now holds over 63 million DAL shares. This equates to a whopping $3.15 billion investment.

Luckily, Imperial Capital’s Michael Derchin (Profile & Recommendations) expects pricing power in key domestic hubs, improving business yields, and strong international results to boost earnings this year and next. His $68 price target indicates 25% upside potential.

But Stifel Nicolaus’ Joseph DeNardi (Profile & Recommendations) is by far the stock’s biggest supporter. With a $95 price target, DeNardi sees prices spiking a whopping 72%. This top analyst has just calculated that DAL made at least $800 million from frequent flyer programs just in 1H18.

Overall, DAL, a “strong buy” stock, has received eight buy ratings versus just a single “hold” rating. See what other Top Analysts are saying about DAL.

Southwest Airlines (LUV)

Texas-based Southwest Airlines (NYSE:LUV) is the world’s largest low-cost airline carrier. After initiating his $2.1 billion position in LUV, Buffett continued to up the stock in 2017. In Q1, Buffett ramped up the position by 10% with the purchase of 4.45 million more shares. Now the fund has a huge $3.3 billion LUV stake.

LUV shares are currently rebounding after a tricky second quarter. Shares plunged in April following a fatal accident caused by an exploding engine. The accident — the first in the company’s 47-year-old history — cost LUV over $100 million in revenue.

However: “We have recovered at this point,” CEO Gary Kelly told Bloomberg recently. “We have been enjoying very strong close-in demand and close-in revenue for a number of weeks.”

This chimes with Cowen & Co’s Helane Becker (Profile & Recommendations) analysis. “Southwest will have a lingering impact from the discounting and a sub-optimal schedule, but the third quarter appears to be the inflection point as management does not anticipate continued issues into the fourth quarter.”

She keeps her “buy” rating on this “strong buy” stock with a $66 price target (11% upside potential). See what other Top Analysts are saying about LUV.

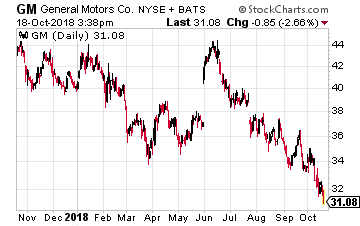

General Motors (GM)

Source: Shutterstock

Buffett is also a long-standing supporter of top dividend stock General Motors (NYSE:GM). After upping Berkshire’s GM position by 2% in Q2, the fund now holds 51 million GM shares valued at $1.6 billion.

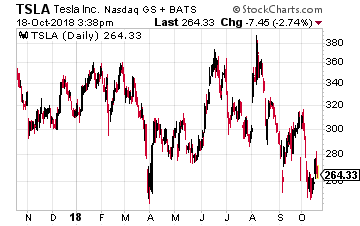

While Tesla (NASDAQ:TSLA) has been hogging most of the self-driving spotlight, GM is busy making its own mark in this fast-growing space. SoftBank Vision fund recently announced a huge $2.25 billion stake in GM’s self-driving Cruise unit.

Top RBC Capital analyst Joseph Spak (Profile & Recommendations) sees a promising long-term opportunity. This is even though GM has now lowered its 2018 outlook.

He writes “It remains to be seen whether GM can win on the robo-taxi opportunity, but it has a seat at the table. And it’s early enough in the story that we still see a lot of potential for that narrative to take hold and for growth/tech investors to look to GM, increasing demand for the shares and potentially the multiple.”

Right now Spak has a $49 price target on the stock (54% upside). Overall analysts have a “strong buy” consensus on GM. The average analyst price target of $52 suggests shares can climb 63% from current levels. See what other Top Analysts are saying about GM.

Teva (TEVA)

Buffett surprised the market with a big bet on flailing pharma giant Teva Pharmaceutical (NYSE:TEVA) back in Q417. He gobbled up 19 million shares in TEVA, worth about $358 million. Since then, Buffett hasn’t stopped buying.

He picked up a further 21.6 million shares in Q1. And now for Q2 we see another 6% boost to his position (with 61 million shares). This takes his total bet on TEVA to a staggering $1.05 billion.

There’s no doubt this is a risky move. Out of 14 recent analyst ratings, only three are buys. This is versus 10 buy ratings and one sell rating. Oppenheimer analyst Christopher Liu (Profile & Recommendations) is sitting this one out. He has a “hold” rating on the stock due to “base business headwinds.”

Liu explains, “We no longer see a clear path for TEVA to return to growth in a timely manner, and continued pricing pressure in US generics makes us less optimistic its US generic business will meet/ exceed Street expectations in FY2018.”

He is worried that the growth story will be hampered by an ongoing focus on cost cutting/divestments. This is required to ensure it meets its massive $28 billion debt obligations. However, there’s no doubt that Buffett sees the cut-priced pharma as a longer-term rebound stock. See what other Top Analysts are saying about TEVA.

Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

Source: Investor Place

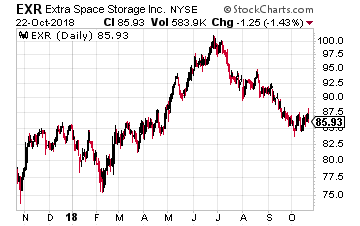

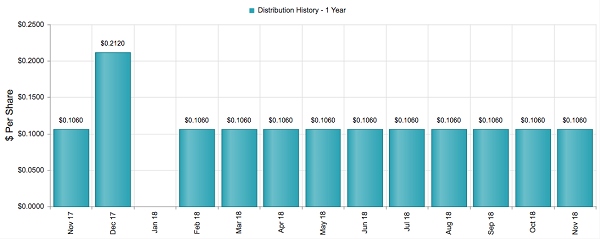

Extra Space Storage (NYSE: EXR) owns or manages almost 1,600 self-storage properties with 115 million rentable square feet. EXR is a real estate investment trust, which means it must pay out the majority of net income as dividends to investors.

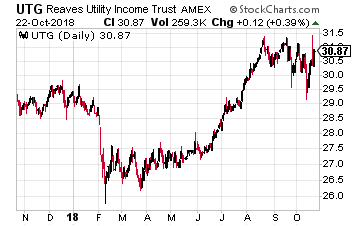

Extra Space Storage (NYSE: EXR) owns or manages almost 1,600 self-storage properties with 115 million rentable square feet. EXR is a real estate investment trust, which means it must pay out the majority of net income as dividends to investors. For this market sector I like the Reaves Utility Income Fund (NYSE: UTG). This is a closed-end fund that owns a diversified portfolio of utility and related stocks. Reaves Asset Management focuses only on utility and infrastructure stock investments.

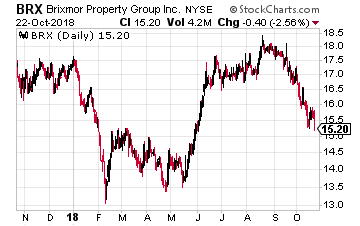

For this market sector I like the Reaves Utility Income Fund (NYSE: UTG). This is a closed-end fund that owns a diversified portfolio of utility and related stocks. Reaves Asset Management focuses only on utility and infrastructure stock investments. Brixmor Property Group (NYSE: BRX) owns 471 open air shopping centers. The company focuses on centers that are the center of their communities. Anchor tenants are the main revenue drivers for Brixmor, and over half of those tenants are grocery stores.

Brixmor Property Group (NYSE: BRX) owns 471 open air shopping centers. The company focuses on centers that are the center of their communities. Anchor tenants are the main revenue drivers for Brixmor, and over half of those tenants are grocery stores.

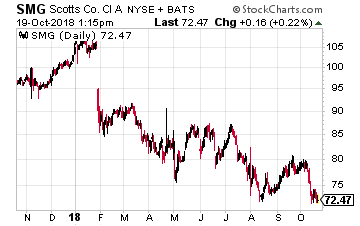

It is very possible that you are familiar with The Scotts Miracle-Gro Company (NYSE: SMG). Scotts is the world’s largest marketer of branded consumer lawn and garden products. In the case of the pot market, the company offers the necessary solutions to enhance the abilities of a marijuana business to produce product.

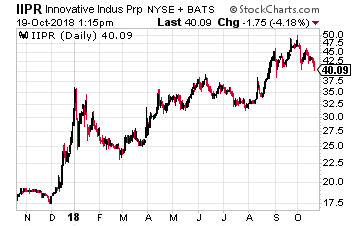

It is very possible that you are familiar with The Scotts Miracle-Gro Company (NYSE: SMG). Scotts is the world’s largest marketer of branded consumer lawn and garden products. In the case of the pot market, the company offers the necessary solutions to enhance the abilities of a marijuana business to produce product. Innovative Industries Properties (NYSE: IIPR) is a REIT that calls itself “The Leading Provider of Real Estate Capital for the Medical-Use Cannabis Industry.”

Innovative Industries Properties (NYSE: IIPR) is a REIT that calls itself “The Leading Provider of Real Estate Capital for the Medical-Use Cannabis Industry.”

Or as GM president Dan Ammann said recently to the Financial Times, “We see this as the race to the starting line.” In other words, the real race hasn’t even started.

Or as GM president Dan Ammann said recently to the Financial Times, “We see this as the race to the starting line.” In other words, the real race hasn’t even started. General Motors (NYSE: GM) seems to have bolstered its claim to be the leading carmaker developing self-driving systems after Hondainvested $750 million into its Cruise division, with the promise of a total of $2.75 billion over 12 years.

General Motors (NYSE: GM) seems to have bolstered its claim to be the leading carmaker developing self-driving systems after Hondainvested $750 million into its Cruise division, with the promise of a total of $2.75 billion over 12 years.

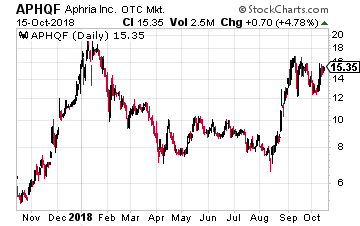

Finally, we have Big Tobacco moving into the marijuana space also. The biggest U.S. cigarette company, Altria Group (NYSE: MO) is reportedly in talks to buy a stake in Aphria (OTC: APHQF).

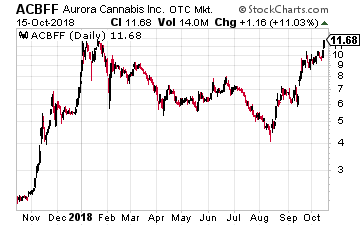

Finally, we have Big Tobacco moving into the marijuana space also. The biggest U.S. cigarette company, Altria Group (NYSE: MO) is reportedly in talks to buy a stake in Aphria (OTC: APHQF). A better choice is Canada’s second-biggest marijuana company, Aurora Cannabis (OTC: ACBFF), which is the company Coke is believed to talking to about a deal. Its $2 billion deal to take over rival MedReLeaf in May was the largest deal in the sector at the time.

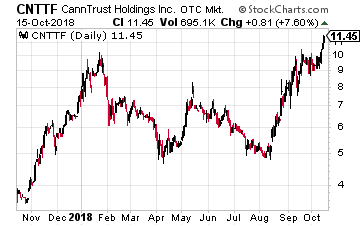

A better choice is Canada’s second-biggest marijuana company, Aurora Cannabis (OTC: ACBFF), which is the company Coke is believed to talking to about a deal. Its $2 billion deal to take over rival MedReLeaf in May was the largest deal in the sector at the time. Another company I would consider is CannTrust Holdings (OTC: CNTTF), which will be listing soon also on a major U.S. stock exchange. It is in active discussions with a number of firms in the beverage, food and cosmetics industries and expects to announce a deal within the next two months.

Another company I would consider is CannTrust Holdings (OTC: CNTTF), which will be listing soon also on a major U.S. stock exchange. It is in active discussions with a number of firms in the beverage, food and cosmetics industries and expects to announce a deal within the next two months.