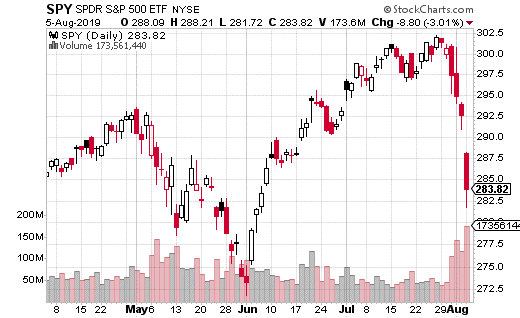

Investors have finally cracked under the pressure of the trade war with China. Stocks, which were at all-time highs just two weeks ago, are now 6% off those highs as of this writing. Although the S&P 500 is still up 13% year-to-date, Monday’s 3% drop set the alert level to red.

Meanwhile, safe-haven investments like gold and bonds are already up big in August. This is the sort of action you tend to see when investors have had enough of stocks. Up until this point, investors were assuming any negative impact from tariffs would be negated by the Fed lowering rates. It appears that’s no longer the case.

The futures market is now pricing in three more rate cuts this year, which places significant pressure on the Fed. The central bank may not want to cut rates further with the job market still hot; theoretically, it could lead to higher inflation. But, if the Fed leaves rates unchanged, there could be substantially more downward pressure on stocks.

There’s no easy answer here. The Fed can go only do so much. Moreover, the U.S, and China aren’t likely to back down from their trade demands, at least in the short-term.

However, let’s not forget the U.S. economy is still in pretty good shape. As I mentioned before, the job market is still smoking hot. We’re not exactly about to plunge into a severe recession.

So, do you buy the dip? Do you stuff your cash in a mattress? While there’s not an obvious solution, looking at the options market can provide some good ideas for how to trade this market.

There were a couple of big trades on Monday in the SPDR S&P 500 ETF (SPY) which caught my eye. Keep in mind, SPY is the most heavily traded ETF in the world and is used actively by retail and institutional traders alike.

Both trades which I’m referring to were covered calls. What? Covered calls during a major selloff? Indeed, covered calls are generally thought of as bullish trades, but they can be instrumental at risk-controlled bullish exposure.

Remember, a covered call is buying shares of a stock/ETF, but also selling calls against those shares. The income provided from selling calls can serve as a cushion to the downside, mainly if those call premiums are rich.

Both covered calls were done with SPY at $284.50. In one case 7,000 October, 292 calls were sold for $5.32 each. In the other trade, 7,000 December 292 calls were sold for $8.28. Combined, these trades brought in about $9.5 million in premiums.

The benefits of using a covered call in this situation are pretty obvious once you break down the strategy. Let’s use the October trade as an example.

Because the calls were sold for $5.32 with the stock at $284.50, the long (owned) shares of SPY are protected down to $279.18. However, the trade can still earn a profit on the upside all the way to $292 where the calls were sold.

Over the next ten weeks, this trade can generate nearly a 2% yield if the SPY hovers at these levels. It also protects against another 2% down move, as I mentioned above. What’s more, the trade can earn up to 4.5% if SPY goes back to $292 or higher by October expiration. The December trade is similar, but just tacks on a couple of months to the position.

While there is hardly a guarantee that the market is going to recover by October or December, it’s more likely we go up than continue plunging. Besides, at worst, these covered call trades are superior to simply buying and holding SPY due to the income/protection from the short calls.

If you’re looking to take a cautious, bullish position on the S&P 500, these types of trades are savvy ways of doing so.

An institution or fund purchased a massive number of put spreads in SPDR S&P 500 ETF (SPY). The put spreads were almost certainly purchased as a hedge against a major market selloff. The trader bought 15,000 put spreads which will pay off if the market drops over 5% in the next two weeks.

That’s why I’m sharing with you today my complete 5 hour, 11 part video training series.

Because after 20 years of trading options…for the first time anywhere…

I’m releasing everything I know about options in one private course.

All the intel I collected on the floor of the CBOE…

All the insider tips picked up as an options Market Maker…

All revealed in seven complete strategies with examples.

In total, to go through everything, I’ve clocked the course at five hours. With this complete course, I believe: In as little as 5 hours, you could master options as well as a seasoned trader.

Plus, have the confidence to trade 7 new strategies right away if you’re new to options or you’re looking to sharpen your skills… the seven strategies I’ll show you right now can help you.

A Strategy for Buying Elite Businesses at Bargain Prices The key is determining whether it’s TRULY a bargain — or deserves to be sold

By Brian Hunt, InvestorPlace CEO

Even elite businesses with juicy dividends suffer share price selloffs from time to time.

Sometimes, these selloffs are caused by short-term, solvable problems within the individual companies.

Sometimes, these selloffs are caused because the overall stock market goes down in value.

These selloffs are almost always opportunities to buy these firms at bargain prices and start collecting steady dividend payments.

When you spend money on any big purchase, like a home or a car, you want to pay a good price. You want to get value for your dollar.

When you buy a car, you want to pay a good price. When you buy a house, you want to pay a good price. You don’t want to overpay. You don’t want to embarrass yourself by getting ripped off.

Yet … when people invest, the idea of paying a good price is often cast aside. They get excited about a story they read in a magazine … or how much their brother-in-law is making in a stock, and they just buy it.

They don’t pay any attention to the price they’re paying … or the value they’re getting for their investment dollar.

Warren Buffett often repeats a valuable quote from investment legend Ben Graham: “Price is what you pay, value is what you get.”

I think that’s a great way to put it.

Like many investment concepts, it’s helpful to think of it in terms of real estate:

Let’s say there’s a great house in your neighborhood. It’s an attractive house with solid, modern construction and new appliances. It could bring in $30,000 per year in rent. This is the “gross” rental income … or the income you have before subtracting expenses.

If you could buy this house for just $120,000, it would be a good deal. Since $30,000 goes into $120,000 four times, you could get back your purchase price in gross rental income in just four years.

In this example, we’d say you’re paying “four times gross rental income.”

Now … let’s say you pay $600,000 for that house.

Since $30,000 goes into $600,000 20 times, you would get back your purchase price in gross rental income in 20 years.

In this example, we’d say you’re paying “20 times gross rental income.”

Paying $600,000 is obviously not as good a deal as paying just $120,000.

Remember, in this example, we’re talking about buying the same house.

We’re talking about the same amount of rental income.

In one case, you’re paying a good price. You’re getting a good deal. You’ll recoup your investment in gross rental income in just four years.

In the other case, you’re paying a lot more. You’re not getting a good deal. It will take you 20 years just to recoup your investment.

And it’s all a factor of the price you pay.

It works the same way when investing in a business …

You want to buy at a good price that allows you to get a good return on your investment. You want to avoid buying at a bloated, expensive price.

This is a vital point.

No matter, how great a business is, it can turn out to be a terrible investment if you pay the wrong price.

If you’re not clear on this point, please read through the home example again. When it comes to buying elite businesses that raise their dividends every year, you can use the company’s dividend yield to help you answer the important question: “Is this business trading for a good price or a bad price?”

Here’s how it works …

When a stock’s price goes down and the annual dividend remains the same, the dividend yield rises.

For example, let’s say a stock is $50 per share and pays a $2 per share annual dividend. This represents a yield of 4% (since 2 is 4% of 50).

If the stock declines to $40 per share and the dividend payment remains $2 per share, the stock will yield 5% (since 2 is 5% of 40).

When a selloff causes an elite dividend-payer to trade near the high end of its historical dividend yield range, it’s a bargain … and it’s a good idea to buy shares.

Remember, these companies pay the world’s most reliable dividends.

Their annual payouts only go one way — UP.

When an elite dividend-payer’s share price suffers a decline of more than 15%, consider it “on sale” and buy it.

For example, in the late 2008/early 2009 stock market decline, shares of elite dividend payer Procter & Gamble (NYSE: PG) fell from $65 to $45 (a decline of 30%).

Procter & Gamble is one of the world’s top consumer product businesses. Every year, it sells billions and billions of dollars’ worth of basic, everyday products like Gillette razors, Pampers diapers, Charmin toilet paper, Crest toothpaste, Bounty paper towels, and Tide laundry detergent. It has raised its dividend every year for more than 60 years.

Investors who stepped in to buy this high-quality business after the market decline could have purchased shares at $50.

In the five years that followed, Procter & Gamble climbed to $80 per share. Its annual dividend grew to $2.57 per share.

This annual dividend represented a 5.1% yield on a purchase price of $50 per share … and that yield will continue rising for many years.

Owning one of the world’s best businesses … earning a 5.1% yield on your shares … collecting a safe income stream that rises every year …

Buying the best at bargain prices is a beautiful thing.

If you have the interest, time and knowhow, you can track these businesses yourself. You can find all the information you need on many free financial websites.

Or, you can simply pay an advisor or research firm to do it for you. I’d be remiss not to invite you to check out Neil George’s picks. Neil can recommend plenty of elite dividend-payers, complete with buy-below prices.

Remember, you can make a bad investment in a great business if you pay a stupid price. View your investment purchases just like you would the purchase of a home, a car, or a computer.

Get good value for your investment dollar. And when an elite dividend-payer sells off for some reason, see it as an opportunity to buy quality at a bargain price.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

Generally, I’m not a big fan of stock screeners. I’ve found that it causes investors to be overly mechanical in their approach.

However, if investors use screeners as a first step in the investing process, then I think it can help them achieve their investment objectives.

With that in mind, I want to share with you what I call “the world’s easiest stock screener.”

You can use the basic screener at www.finviz.com, which is free. I call it the most effortless screen because it only has three steps.

Step #1: Screen for stocks with dividend yields above 3%.

Step #2: Screen for stocks with low levels or long-term debt.

Step #3: Sit by the pool.

Let me take a step back and explain some details. I use dividend yield because it’s a decent (though not perfect) measure of valuation. Of course, there are exceptions. You want to steer clear of stocks that are in a death spiral. They might have high yields because their share is down, and future dividends are in doubt.

Also, companies may list elevated dividend yields because they’re based on a one-time special dividend that can’t be counted on In the future. Think of the dividend yield as a way to avoid too much risk in an investment.

I also like dividends because it’s something tangible. The accounting department can endlessly manipulate earnings and cash flow. Companies also use “adjusted” earnings and share buybacks to make the corporate balance sheet appear the way they want it to. Dividends, by contrast, represent real money that goes to you.

The second screen is too much debt. There are lots of ways to measure this, but a good one is to look for companies whose long-term debt is less than 40% of their equity. Don’t worry about the exact dividing line, but that’s an excellent place to start.

The issue we want to avoid is companies that borrow too much and in effect, use their debt fund their dividends. That’s a big no-no. That’s why these two screens worth together. It’s an efficient way to find companies with organic growth. Too often, companies use their balance sheet to buy growth instead of earning it.

As a very general rule of thumb, a deteriorating balance sheet is often a sign of business trouble. Companies will try to use their finances to mask over difficulties that their products are having. You always have to look behind the numbers.

Their other screens you can use to fine-tune your results. For example, you may only want stocks in the S&P 500. Or stocks above $40 per share. Or stocks based in the United States. There are good arguments for all of these, but don’t lose sight of the basic idea.

Our screener is useful because it focuses on price and quality. As long as you do that, you’re investing correctly.

Now let’s look at three stocks that currently pass our screener:

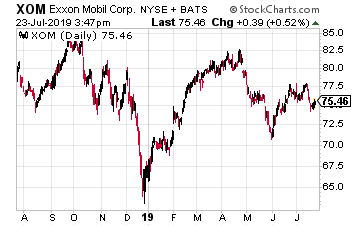

At the top of the list is ExxonMobil (XOM), the largest energy company in the world. Declining energy prices have hurt the stock, but the current yield is 4.6%. That’s excellent protection. Long-term debt currently registers at 21% of equity. That’s not bad. Also, rising geopolitical tensions in the Persian Gulf could be a boost to oil. XOM will report earnings on August 2.

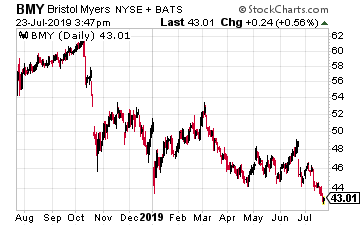

Our next candidate is Bristol-Myers Squibb (BMY). The pharmaceutical company currently yields 3.8%. BMY’s long-term debt is equal to 37% of its equity. The shares have been beaten down this year. BMY is down about 16% in 2019. I like that the shares are currently going for less than ten times next year’s earnings. This could be the time for a turnaround.

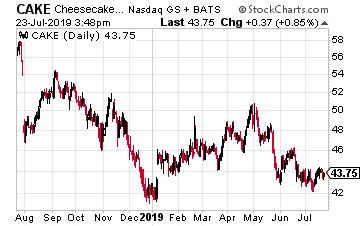

Lastly, we have the Cheesecake Factory (CAKE). The chain restaurant stock has a yield of 3% and their debt position is quite good. CAKE’s long-term debt is just 4% of its total equity. The next earnings report is due out on July 31. Wall Street expects 81 cents per share. Look for an earnings beat. High calories will never go out of business.

To clarify, our stock screener is just a first step in finding good stocks. You still want to make sure you own high-quality shares that are fundamentally sound. The three I’ve just given you fit the bill.

Most importantly, don’t forget the final step this summer. Relax by the pool.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

The stock market has racked up high returns for the first half of 2019. The second-quarter corporate earnings reports so far have not been stellar. So far it’s tough to envision a scenario where the major stock indexes tack on another 10% to 15% in gains for the second half of the year. I think it’s likely that what performs well in the second half of 2019 will be much different from what made investors money in the first half.

While growth stocks have done well so far this year, a lot of high-yield stocks have lagged the major market indexes. High-yield is a different world. The primary investor concern is whether a company can continue to pay those big dividends. High-yield comes with what I call the binary outcome potential. On one side is the company will continue to pay the dividend.

This is the desired outcome, and the significant yield becomes your expected return. The flip side is the dividend cut the market has priced into the shares. A high-yield is the indicator that the market has built in the probability of a dividend reduction. A dividend reduction cuts twice, first your income gets reduced, and second, the reduction usually produces a significant share price drop.

Your goal as an income stock investor is to seek out higher yield stocks where you have conviction the dividend is secure. If you can find stocks with 10% plus yields and the dividends keep coming, you have a good chance to outperform the stock market for the rest of 2019. To find “good” high yield stocks, you need to understand how the individual companies generate cash flow to pay the dividends.

Further, you’ll need to monitor each company every quarter to make sure the dividend is secure. If you like high-yield, but don’t want to become a corporate accountant or Wall Street analyst, consider signing up for my Dividend Hunter service.

To get you started, here are three stocks with yields over 10% where currently the dividend looks secure. They are good ideas for where to begin your research.

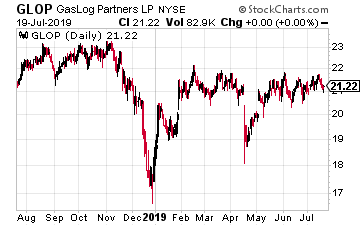

GasLog Partners LP (GLOP) is a publicly-traded partnership that owns a fleet of 15 liquid natural gas (LNG) carrier vessels. Most of the fleet is on long term lease to Royal Dutch Shell plc (RDS.A). The leases provide predictable cash flow, and even with its high yield, GLOP has been growing its dividend by 3% to 5% each year.

The danger is that dividend coverage is very tight, with a first-quarter distributable cash flow of just 1.03 times the dividend. Global LNG trade is a growth business, which is positive for the long-term success of GasLog Partners. The stock currently yields 10.1%.

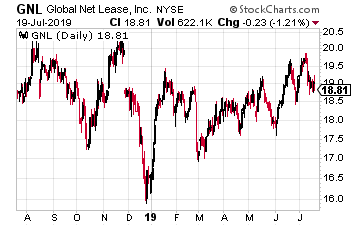

Global Net Lease (GNL) is a $1.6 billion market cap real estate investment trust (REIT). The company focuses on sale/leaseback transactions, where it buys commercial properties and leases them back on triple-net leases to the selling company.

Portfolio properties are evenly split between the U.S. and Europe, with 55% of the portfolio being office buildings. The danger for GNL is after the initial lease period expires if the tenant company doesn’t renew, the expense to retrofit and release will be very high. The shares currently yield 11,2%.

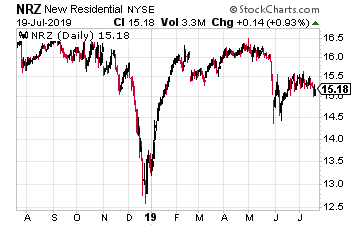

New Residential Investment Company (NRZ) is a finance REIT which has operations in the various phases of the residential mortgage market. Its primary investments are in mortgage servicing rights (MSR). These are fee stream paid on every individual residential mortgage.

The danger to NRZ is that high refinancing activity will deplete the MSR payments stream. To counter this, New Residential has diversified into other sectors of the mortgage business. The shares currently yield 13.1%.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.

If this were any “normal” time, we’d be able to buy safe bonds and collect enough income on our nest egg to fund our retirements. Unfortunately, this is the “new normal” where the Fed is not the friend of us current and hopeful retirees!

Jay Powell is afraid for his job, which means he’s going to cut rates and keep them low for a long time. This means we must look beyond traditional bonds for meaningful income.

What about blue chip dividend-paying stocks? Well, an 11-year stock market rally has ruined that idea. Anyone putting new money in a pricey dividend aristocrat is “buying and hoping” that the stock continues to levitate while the firm dishes its dividend.

And about that dividend. Blue chips don’t pay more than 2% or, at most, 3% today. On a $1 million portfolio that’s less than $30,000 in annual income. Not enough to retire on!

Fortunately, there’s a better way. I’ve developed the Perfect Income Portfolio to safely double, triple, and even quadruple the payouts on your 2% payers. You can turn these misers into 6%, 7% and even 8% yields (for $80,000 on that million bucks) without doing anything risky.

And oh by the way, you can grow your capital base, too! Whether it’s $250,000, a million or $2.5 million (or anywhere lower, higher or in between) you can bank these big yields and enjoy price appreciation to boot.

How do I know? Because we’ve done it. In the four years I’ve been managing our Perfect Income Portfolio, our investors have enjoyed 11.4% returns per year since inception. This means they’ve collected their 6%, 7% and 8%+ cash yields while enjoying additional price appreciation on their investments.

Our “secret” has been three safe yet lesser-known income vehicles. Their obscurity creates opportunity for us contrarian income seekers. I’ll explain by showing you how we buy bonds for less than their face value.

Perfect Income Vehicle #1: Buy $1 in Bonds for Less

Many investors believe bond ETFs are a convenient way to add a basket of bonds to their portfolio. Problem is, they’re not getting any deals buying them.

ETFs never trade at discounts. Their sponsors simply issue more shares to capitalize on any increased demand, which means anyone who buys one of these popular vehicles always pays list price.

But we don’t have to pay full price for a bond. Ever. Which is why we should look past ETFs and consider underappreciated closed-end funds (CEFs) instead.

The “closed” in CEF means that the fund’s pool of shares is fixed. Which is why these vehicles can have wild price swings above and below the values of their actual assets. (Good for us contrarian income seekers – we can buy below fair value to maximize our yields and upside.)

They are also “closed” in their actual communications with the financial world. Fund information is often limited (sometimes to one-page fact sheets) and it’s difficult to get management to talk to you.

(Also good for us, because it makes bargains more prevalent in this “mysterious” corner of the income world. Especially for us persistent types).

Plus, we can hire the best bond managers on the planet to handpick our bond buys for free!

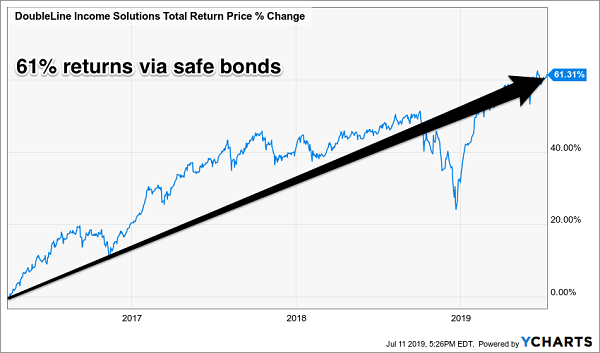

Take the DoubleLine Income Solutions Fund (DSL), the vehicle run by the “bond god” Jeffrey Gundlach himself. Its holdings pay plenty, boasting coupons of 7%, 8% and even 9% and higher!

Granted, DSL’s bond holdings are a bit obscure (63% foreign corporate bonds, for example). But there are deals to be had and that’s exactly why we hired Gundlach to search the globe for us for big fixed income payments. He’s the man in Bondland and often gets the first phone call on new juicy deals. You and I can’t buy these bonds as individual investors, but the bond god can buy them for us.

My income subscribers have indeed enjoyed 61% total returns (including dividends) courtesy of Gundlach’s DSL.

When We Were Bond Gods

And they make CEFs in more traditional bond flavors, too. Some provide you with ways to trade in your mere “common” shares for preferred stock that pays more.

Perfect Income Vehicle #2: One-Click to Double Your Yields

Not familiar with preferred shares? You’re not alone—most investors only consider common shares of stock when they look for income. But you can double your yields or better and actually reduce your risk by trading in your common shares for preferreds.

A company will issue preferred shares to raise capital, just as it offers bonds. In return it will pay regular dividends on these shares and, as the name suggests, preferred shareholders receive their payouts before common shares.

They typically get paid more and even have a priority claim over common stock on the company’s earnings and assets in case something bad happens, like bankruptcy. They are “preferred” over common stock and come after secured debt in the bankruptcy pecking order.

So far, so good. The tradeoff? Less upside. But in today’s expensive stock market that may not be a bad substitution to make. Let’s walk through a sample common-for-preferred exchange that would nearly double your current dividends with a simple trade-in.

As I write, the common shares from JPMorgan (JPM) pay 2.8%. But the firm recently issued Series DD preferreds paying 5.75%. JPMorgan shareholders looking for more income may be happy to make this tradeoff.

Meanwhile, Bank of America (BAC) common pays 2% today. But B of A just issued some preferreds that pay a fat 5.88%. That’s a 194% potential income raise for shareholders who want to trade in their garden-variety shares. But how exactly do we buy these as individual investors? Which series are we looking for again?

A big problem with preferred shares is that they are complicated to purchase without the help of a human broker. So, many investors attempt to streamline their online buys and simply purchase ETFs (exchange-traded funds) that specialize in preferreds, such as the PowerShares Preferred Portfolio (PGX) and the iShares S&P Preferred Stock Index Fund (PFF).

After all, these funds pay up to 5.9% and, in theory, they diversify your credit risk. Unfortunately, many ETF buyers have little understanding of preferred shares, let alone how a particular fund invests in them. Should we entrust the selection of preferred shares to a mere formula baked into an ETF?

Again, no! Another problem with the ETF model is that it doesn’t account for credit risk as accurately as an expert human can. Which means a better idea is — you guessed it! — to find an active manager to handpick your preferred portfolio. Buying a discounted closed-end fund (CEF) is the best way to do this.

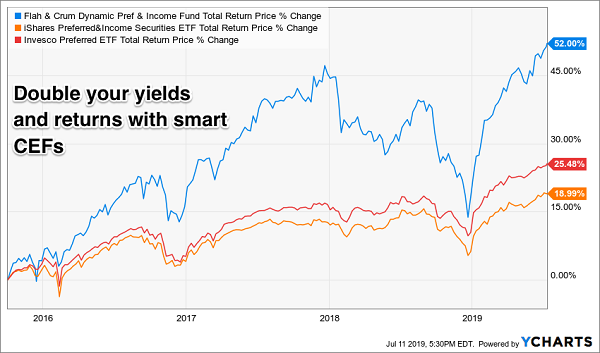

Here’s a Perfect Income Portfolio favorite outperforming its more popular ETF cousins since we bought the CEF in late 2015:

Why We Prefer CEFs

When we’re shopping in the preferred aisle, it’s a “no brainer” to go with the CEF concierge service. They yield more, they appreciate in price more, and again, the money manager is free when we buy at a discount.

Perfect Income Vehicle #3: Doubling Your Money with Dividends

We’re going to switch gears and jump into stocks. But don’t worry, these aren’t overpriced, underpaying blue chips that the Wall Street fanboys push. No, these are hidden gems that get no coverage from the (lame) mainstream financial media.

We can thank the giant firms that manage most of the investment money in the US for these bargains being available. Think Wells Fargo, Morgan Stanley, Merrill Lynch, your neighborhood Edward Jones, and even Fidelity, Schwab and Vanguard.

These firms serve hundreds of thousands of clients, with millions and millions of dollars, around the country and the world. They offer the same approaches for people of similar situations, which means they can only buy stocks which there are “enough of” (have enough liquidity) for everyone.

That means one simple thing. The familiar names can’t recommend our high-income producers to you. Instead, they stick you in pretty much what everyone has.

Apple has a market value of more than $900 billion. And shares yield just 1.5%. Convenience, familiarity, and liquidity come at the expense of the stock’s current payout.

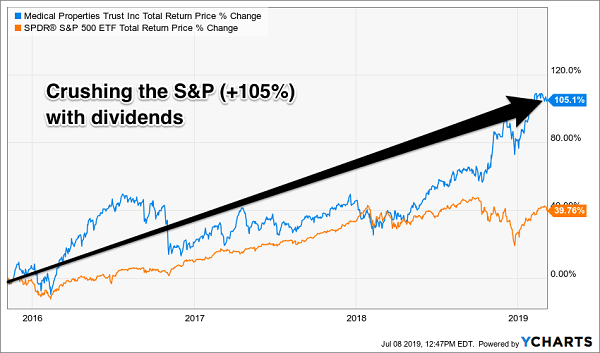

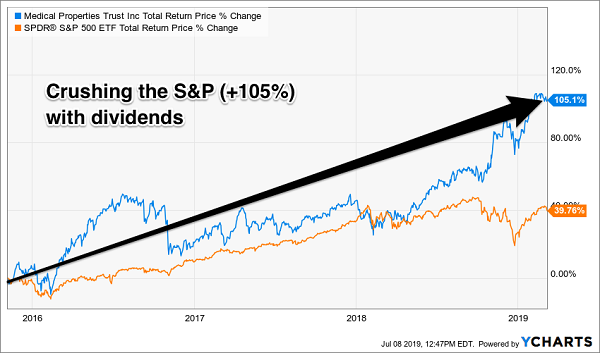

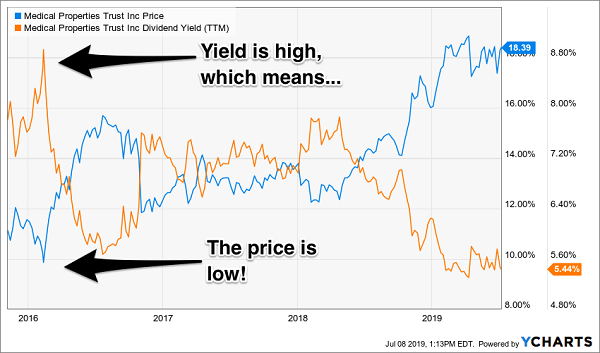

Let’s contrast Apple with hospital landlord Medical Properties Trust (MPW). The firm pays a generous 5.4% on the capital you invest today, 3.5X as much as Apple! And its focus, the hospital, is arguably even more indispensable than the iPhone (which does have competition from Samsung and others).

But MPW the stock isn’t large enough for the big pension funds to buy or for the brand-name money managers to pile into. With a modest market cap of $7 billion, MPW is plenty liquid for you and me—and exclusive enough to provide us with this generous yield premium!

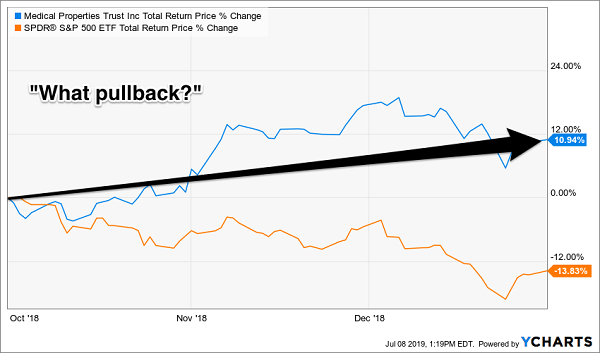

Plus, just like Apple, it raises its dividend every year. And dividend growth is, over the long haul, the main driver of higher stock prices. We added MPW to our Perfect Income Portfolio stock in November 2015 and received three dividend raises over the ensuing three-and-a-half years. The result? We enjoyed 105% total returns and really crushed the broader S&P 500:

Perfect Income Vehicle #3: Dividends with 100%+ Upside

The Perfect Income Portfolio also adds years to our lives. We don’t need stock prices to stay high to retire! Most investors who sell shares for income spend their days staring at every tick of the markets.

You can live better than this, generate more income and even enjoy more upside by employing our contrarian approach to the yield markets. We live off dividends alone. And we buy issues when they are out-of-favor (like right now) so that our payouts and upside are both maximized.

Plus 8% Dividends, Paid Monthly, Make Retirement Even Easier

And by the way, you can even use my “no withdrawal” strategy to make sure you’re:

Banking 8% annual dividends,

Enjoying additional price upside, and

Getting paid monthly to boot!

If this interests you, I’d recommend starting with my all-star retirement portfolio. It contains 8 of the absolute best-preferred stocks, REITs and CEFs out there.

If you’re scratching your head at these terms, you’re not alone. These are investments that you won’t hear about on CNBC or read about in the Wall Street Journal. Which is why we have these fantastic opportunities available in this “no yield” world.

I’ll explain more about them in a minute. I’ll also show you why my 8% eight-pack is well diversified across all types of investments and sectors, and the cash flows funding these dividends will do well no matter what happens in the broader economy or stock market.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Successful dividend investing is simple, though not necessarily easy. There are nuances which trip up many investors (including most professionals!) These twists and turns create “yield alpha” opportunities for contrarian-minded income investors like us.

If everyone else in the market were perfectly grounded and calculated, there would be no chance for us to make above-average returns. After all, the 11.3% and 17.5% annualized returns that my Contrarian Income Report and Hidden Yields readers are earning would be snapped up in a perfectly efficient market.

Thanks to these inefficiencies, we are able to bank big yields and price returns in Dividend Land. Ready to retire on dividends? Follow these seven steps and we’ll do it together. Let’s start with an obvious yet underappreciated rule for income investors.

Step 1: Count Your Dividends

Since we focus on high yield, most of our returns come from the “yield” component of stocks. So let’s not forget about them when figuring out our returns!

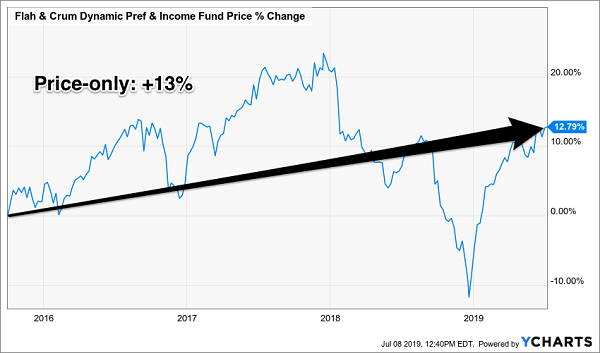

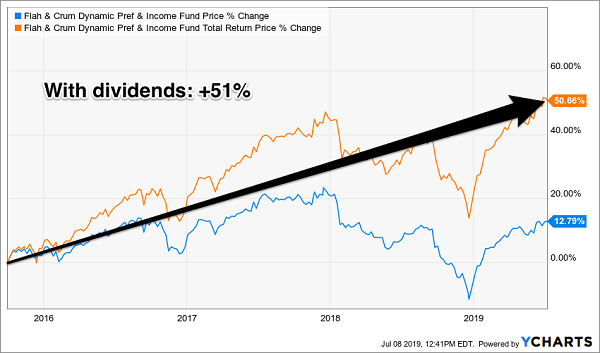

For example, we added this preferred stock fund to our portfolio in October 2015 and its price-only returns look quite pedestrian:

Don’t Fixate on Price Alone…

We’ve gained 51%, while the price is up only 13%. The majority of our fat 51% gains have been delivered via cash dividends. So let’s make sure we add in the orange (top) line below to reflect the big driver of our profits!

… Remember to Add Those Dividends!

Step 2: Find Price Upside, Too

While we could build a portfolio that’s 100% invested in these types of safe bonds and do just fine, we’re better off putting 50% or so of our cash in stocks. The upside is too good to ignore.

Dividend growth is, over the long haul, the main driver of higher stock prices. We added this stock in November 2015 and received three dividend raises over the ensuing three-and-a-half years. The result? We enjoyed 105% total returns and really crushed the broader S&P 500:

Why We Buy Dividend Stocks, Too

Step 3: Monitor Dividend Coverage

A dividend hike is the ultimate sign of dividend safety, so I prefer stocks that consistently raise their payouts. The likelihood that a company is going to raise its dividend (or cut it) is directly related to its payout ratio or the percentage of its profits (or cash flows) that it is dishing out to shareholders as dividends.

As a rule of thumb, a payout ratio below 50% is a sign of dividend safety. Some capital efficient firms can pay more and real estate investment trusts (REITs) can pay up to 90% of their cash flows as dividends.

It depends on the company (and if you don’t feel like following the payouts and cash flows of 20 stocks and funds yourself, I’ll gladly do it for you as part of your subscription!)

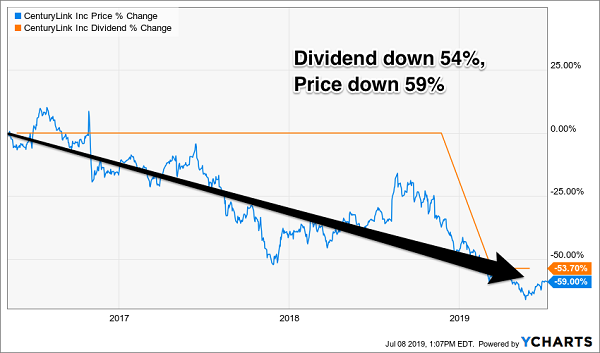

Dividend cuts are no fun. Not only are they a monthly pay cut for us, but (worse) they destroy capital. Take the case of CenturyLink (CTL), which has been writing its investors dividend checks that it couldn’t cash since I called out this “paper telecom tiger” in May 2016 (and many times since!)

At the time, CTL was paying out 135% of its earnings as dividends. The company wasn’t growing profits, either, so the payout eventually had to go. Mr. Market eventually sniffed this out and CTL’s management team finally made the inevitable cut earlier this year:

Stocks Rise and Fall with Their Dividends

Remember the rising dividend that drove our gains in step two? The opposite happened to unfortunate CTL investors here, as their stock’s price dropped 59% while they received a 54% pay cut!

Step 4: Don’t Fight the Fed

“Don’t Fight the Fed” was chapter four in investing wizard Martin Zweig’s legendary book Winning on Wall Street. Here’s why we’ll make it step four here.

Zweig devoted 40 thoughtful pages to teach readers why they should “go with the flow” with respect to the Fed’s trend at any given moment.

Is the Fed raising rates? Then we should favor floating-rate bonds because their coupons (and values) tend to tick higher as rates climb.

Has the cycle topped? When the Fed is prioritizing “easy money,” we should trade in our floaters for fixed-rate bonds, which gain in value as rates fall.

Step 5: Favor Out-of-Favor

What did our winners in step one and two have in common? Two things:

They were well run, and (most importantly)

We bought them when each was out-of-favor.

Contrarian investing should be uncomfortable. We want to buy stocks when their yields are high with respect to their norms. To put it plainly, we want to buy this stock when our “dividend per dollar” (as reflected by the orange line) is high. It means the price is low!

High Historical Yield Meant Low Price

And likewise, we want to purchase closed-end funds (CEFs) when they are trading at discounts to the value of the assets on their books. This is a unique feature of CEFs because they trade like stocks, with fixed pools of shares. They can and will trade at premiums and discounts to their portfolios, which means we can sit back and wait for bargains.

Step 6: Get (and Stay) Fully Invested

The stock market goes up about two-thirds of the time. Permabears miss out on compounding and it’s not as easy to be a part-time bear as it sounds.

To illustrate this let’s consider a study by Hulbert Financial. The firm looked at the best “peak market timers”–the gurus who correctly forecasted the bursting of the Internet bubble in March 2000 and the Great Recession in October 2007.

These were the clairvoyant advisors who had their clients out of stocks and mostly in cash when the S&P 500 was about to be chopped in half. Surely their clients did great over the long haul, given their capital was largely intact at the market bottoms, right?

Wrong. None of these advisors turned in top performances. The reason? While they were good at timing tops, they were terrible at timing bottoms! The bearish advisors didn’t get their clients back into stocks anywhere near the bottom. They had their capital intact, but they didn’t deploy it–and they largely missed out on the epic bull markets that followed these crashes.

Think about the advisors and investors who sold in late December when the “bear market” became official. They moved to cash at the worst possible moment and have been on the sidelines waiting for a low risk “retest” of the lows. Mr. Market loves to confuse the most amount of people, and he really outdid himself this time!

Barely a Bear Market…

… And Right Back to a Bull!

We can be smart about staying in the market by focusing on “pullback-proof” names.

Step 7: Prepare for Pullbacks

Where’s the market going from here? Well, if you own pullback-proof dividend payers, you probably don’t care.

My readers are often asking for safe income ideas. For stocks that pay dividends and never drop in price. It’s a very difficult task, but not quite impossible.

For most long-term investors who want big dividends–I’m talking 6%, 7% and even 8%+ current yields–I recommend holding safe dividend-paying bonds and funds through any market turbulence.

Big dividends are the rubber duckies of the investing world. Wall Street hysteria may push their prices underwater for days or weeks at a time, but as the months and years pass these stocks bounce back to the surface. Let’s revisit our dividend machine from steps two and five. Did its investors even realize we had a market collapse in the fourth quarter of 2018? No.

Q4 2018’s Dividend Rubber Duckie

There’s nothing quite like a pullback-proof dividend machine! And if it’s “2008-proof” then even better. After all, we’re 11 years older now and few of us can afford a 50% drawdown.

If you need big income without the drawdowns, I do love the short and long-term prospects for five 2008-proof dividend payers yielding an average of 7.5%. If you’re worried about a repeat of 2008 (and again let’s be honest, who isn’t), here are five solid payouts you can purchase today without worrying about an overdue pullback (or worse, an all-out crash).

Introducing the “2008-Proof” Income Portfolio Paying 7.5%

The “cash or bear market” no-win quandary inspired me to put together my 5-stock “2008-Proof” portfolio, which I’m going to GIVE you today.

These 5 income wonders deliver 2 things most “blue-chip pretenders” don’t, such as:

Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure a safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a SAFE 8.5%.

Think about that for a second: buy this incredible stock now and every single year, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is. These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “2008-proof” plays might have wondered what all the fuss was about!

These five “2008-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out (every year), with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

You can’t deny that the technology sector is fast-paced. It’s ever-changing as new fads, trends, devices, and applications come and go. Today, it’s cloud computing. A few years ago, it was wearable devices. And who can forget the hype surrounding B2B stocks during the dotcom days?

But as these trends shifted, so too have the various tech stocks. The sector is littered with former leaders that have now turned into losers.

Not all former high-flying tech stocks are worthy of the dust bin, though.

In fact, there are plenty of decidedly old-school technology firms that are still making plenty of profits, cash flows and even dividends for their shareholders.

For investors, these now-forgotten tech stocks could be huge potential values in the making. Sure, they require some patience and a little luck, but the potential rewards are great. All in all, making some room in a portfolio for a few forgotten tech stocks could make a ton of sense.

But which ones actually have the goods to outperform over the long haul? Here are three former high-flying tech stocks that could be big bargains.

eBay (EBAY)

While Amazon (NASDAQ:AMZN) and even Walmart (NYSE:WMT) capture most of investor’s e-commerce love, old school tech stock eBay (NASDAQ:EBAY) continues to rack up sales and profit growth.

The firm is still one of the largest online retailers in the world — with more than 179 million active users and an average of over 1.9 billion listings on its site at any one time. Meanwhile, as a third-party listing service, EBAY features some pretty high margins and cash flows when it comes to people actually making a purchase on the site.

And it turns out, the firm has some tricks up its sleeve to get its former mojo going.

After eBay jettisoned PayPal (NASDAQ:PYPL), growth at the firm slowed to a trickle. In order to get that growth back, the firm is starting to copy a playbook that has helped both AMZN and WMT: sponsored ads and promoted listings.

EBAY charges sellers a fee in order to boost the prevalence of their products and quicken the pace of a sale. The beauty is that EBAY will still get the standard commission fees when the item does sell.

These promoted ads are starting to work wonders. During the first quarter, eBay managed to generate more than $65 million in extra revenues from them. Better still, this only improves the firm’s margins. Adding in moves to refresh and simplify the buying experience, eBay is back on track to post some significant gains this year.

Despite the potential, new dividend, and increased estimates, EBAY stock trades at a forward P/E of 13. When it comes to tech stocks, eBay should not be forgotten.

Groupon (GRPN)

Source: Shutterstock

A strange thing recently happened at a summer kick-off barbecue I attended. Multiple people were talking deals that they had scored on Groupon (NASDAQ:GRPN).

About a decade ago, the deal-making site became a huge fad as it promoted its voucher system for local restaurants, goods, and various services. You could pay a low cost to save as much as 80% on dinner, a movie, and even dog grooming services. These days, GRPN is moving away from that system and into a potentially more lucrative one for consumers and its bottom line.

Groupon now offers what’s called card-linked deals. Instead of buying a voucher for a service later on, consumers are able to link a credit card to the account and then get cash back after they buy a good or service advertised on the platform. The benefit is that customers don’t pay until the point of service and can use deals an unlimited number of times.

At the same time, it has revamped its voucher-based products by adding appointments for certain services and experience segments. These two moves are designed to create a more seamless interaction between customers and businesses. Moreover, it’s designed to make using GRPN a habit. The tech stock just sits back and collects the fees.

And while it’s easy to write GRPN off as a former fad, the firm continues to be free cash flow positive, have a huge $1 billion in cash on its balance sheet, and see improving results. In the end, Groupon may be a former high-flyer, but today, investors are getting a huge sale on the discount provider.

Dell Technologies (DELL)

Dude, you’re getting a Dell … again. However, these days Dell Technologies (NASDAQ:DELL) is a far better and perhaps more important tech stock than it was during the go-go dotcom days.

The story of how DELL got here is perhaps a bit convoluted. The PC maker was public throughout the internet boom and was taken private by founder Michael Dell and Silver Lake Partners. During that time, the firm made a big splash when it bought enterprise software specialist EMC Corporation, which also included a stake in VMware(NASDAQ:VMW). This led to a tracking stock covering Dell’s VMW holding.

Which brings us to today. Dell decided to roll-up that tracking stock and once again IPO as its former ticker DELL.

And while it may have fallen out of the public eye in the five or so years it wasn’t openly traded, DELL has become a monster of an integrated tech stock. The PC and server business is still there — which is booming thanks to rising data center demand. Meanwhile, the firm is a leader in cloud computing and virtualization software, cybersecurity via RSA as well as various infrastructure-as-a-service (IaaS) products. Today’s DELL is looking like a real contender among leading tech stocks. That fact has shown up in its first-quarter results. First quarter revenue clocked in at $21.9 billion — an increase of 3%.

In the end, Dell may be a blast from the past. But this is one forgotten tech stock ready to rewrite its future.

At the time of writing, Aaron Levitt held a long position in AMZN.

July marks the start of the 2019 third quarter, and in a few weeks, earnings season starts, with a flood of quarterly earnings reports. With income stocks, quarterly earnings often are closely led or followed by dividend announcements.

Common stock dividends are note sure things until they are announced. It’s even better when a dividend announcement comes with a payout rate increase.

If you expect a dividend increase is coming soon, you can put the stock on your watch list to pick up shares during any price dip in the weeks leading up to the announcement date. Today I am giving you lead time warning on some projected dividend increases for next month.

Real estate investment trusts (REITs) pay attractive current yields and regularly increase their dividend rates. I maintain a database of about 140 REITs, out of which about 100 have histories of dividend growth.

Most of these companies increase the quarterly dividend once a year, and then pay the new rate for the next four quarters. Even though individual REITs increase their dividends just once a year, those announcements are spread across almost every month of the year.

To capture those share price gains, you want to buy shares a few weeks to a month before the next dividend increase announcement is published. Now in early July, it is a great time to look at those REITs that should increase dividends in August.

Here are a few REITs from my database that historically have boosted their payouts in August.

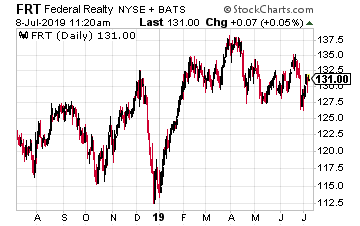

Federal Realty Investment Trust (FRT) is a $10 billion market cap REIT that owns, operates, and redevelops high quality retail real estate in the country’s best markets.

FRT has increased its dividend for over 50 consecutive years, the longest growth streak of any REIT. Over the last 5 years, the average annual dividend increase has been 6%. Last year the dividend was increased by 2.0%. Based on management guidance, an increase close to the 5% annual average is in the cards for this year.

The company announces its new dividend rate in early August. The ex-dividend date will be in mid-September with payment about a week later.

This is a very high-quality REIT. The stock yields 3.1%.

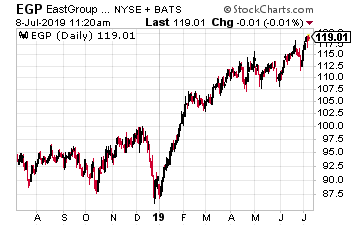

Eastgroup Properties Inc. (EGP) is a $4.3 billion market value REIT that focuses on development, acquisition and operation of industrial properties in major Sunbelt markets throughout the United States with an emphasis on the states of Florida, Texas, Arizona, California and North Carolina.

The industrial properties sector is currently one of the best performing real estate sectors.

The company has increased its dividend for 23 of the last 26 years, including the last seven in a row. Last year the payout was increased by 12%. This year my forecast is for a 5% to 7% increase.

The new dividend rate should be announced in late August or early September, with a mid-September ex-dividend date and end of the month payment date.

EGP yields 2.5%.

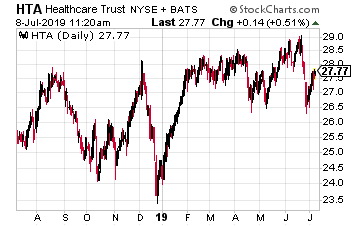

Healthcare Trust of America, Inc. (HTA) is a $5.7 billion REIT that acquires, owns and operates medical office buildings. The company reduced its dividend in 2012 and 2013, which was followed by small increases in each of the next four years.

Last year the dividend was bumped up by 1.7%; comparable to the increase of the previous year. In 2018, the funds available for distribution per share increased by 1.2%, and for the 2019 first quarter, FAD per share was flat compared to a year earlier.

Management has been very conservative with the dividend growth and I expect a small increase comparable to the last couple of years. Last year the new dividend rate was announced in early August, with an end of September ex-dividend date and early October payment date.

The stock currently yields 4.5%.

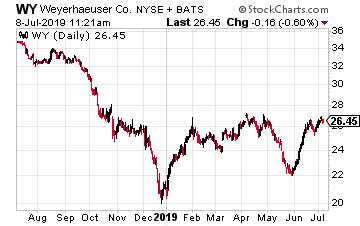

Bonus Recommendation:

Weyerhaeuser Company (WY) is a $20 billion market cap company that converted to REIT status in 2010. The company owns forest land and generates revenue by harvesting trees and processing the trees into lumber and pulpwood products.

Since the REIT conversion, the dividend has steadily increased, but not on a regular schedule. The current rate has been paid for four quarters, so an increase is due with the next announcement.

Last year the WY dividend increased by 6.3%. The next dividend announcement will be in late August with mid-September record date and end of September payment.

Get your hands on my most comprehensive, step-by-step dividend plan yet. In just a few minutes, you will have a 36-month road map that could generate $4,804 (or more!) per month for life. It's the perfect supplement to Social Security and works even if the stock market tanks. Over 6,500 retirement investors have already followed the recommendations I've laid out.