Source: Shutterstock

Sometimes identifying the best stocks to buy can be difficult, but you could do a lot worse than checking out the stocks selected by one of the world’s savviest hedge fund managers: Warren Buffett. Warren Buffett stock picks are a popular source for an investors, and for good reason.

Billionaire Buffett is many things: one of the world’s most successful fund managers, legendary philanthropist and owner of over 60 companies. His formidable stock picking ability has given him the nickname ‘the Oracle of Omaha’ and a fortune of over $87 billion. “He beats everybody all the time when it comes to picking stocks” writes Bloomberg’s Nir Kaissar. Indeed, the per-share market value of Berkshire has returned an incredible 20.9% annually from October 1964 through 2017.

And now we can track the latest trades of his $191 billion Berkshire Hathaway fund. Just-released SEC forms reveal a valuable glimpse into which stocks Buffett likes, and which he doesn’t.

Bear in mind that these are the trades the fund made in Q4 rather than the current quarter — so it is possible that the positions have changed since the filing date.

Here I also include TipRanks’ stock insights from Wall Street’s best-performing analysts. Does the Street sentiment match Buffett’s latest stock picks — or is he going rogue with his investing decisions? We can check the overall analyst consensus as well as analysts’ average target price. This is a crucial indicator of how far the Street sees a stock moving over the coming months.

Let’s take a closer look at the top Warren Buffett stock picks now:

Warren Buffett Stock Picks #1: Apple (AAPL)

Apple Inc. (NASDAQ:AAPL) shares spiked higher on the news that this is now Buffett’s largest investment. Following a 23% increase of AAPL shares, Buffett now holds $28 billion in AAPL stock. This is about 14.6% of the total portfolio.

According to Time, Buffett explained that:

“Apple strikes me as having quite a sticky product and an enormously useful product to people that use it, not that I do.”

Indeed, the facts bear this out with Morgan Stanley pegging the iPhone’s retention rate at 92% vs just 77% for Samsung phones.

Guggenheim’s Rob Cihra echoes Buffett’s bullish Apple stance. He has a $215 price target on AAPL (21% upside potential). After dissecting the stats, this top analyst sees ‘Other Products’ revenue hitting $22 billion in 2019.

For Cihra:

“Apple has never been about going after a whole market’s unit share but rather peeling off the high-value tops for max revenue and profit share. It can then compound that by selling MORE into its ‘niche’ installed-base of loyal, high-value customers.”

Overall analysts are cautiously optimistic on AAPL right now. The stock has a Moderate Buy analyst consensus rating with 17 buy ratings and 13 hold ratings. With an average price target of $193, the Street is predicting 8% upside for AAPL from current prices.

Warren Buffett Stock Picks: BNY Mellon (BK)

Buffett has now ramped up his holding of this financial stock by 21% to $3.275 billion. This makes Bank of New York Mellon Corp (NYSE:BK) the 10th biggest stock in Berkshire’s portfolio. Although Buffett has held BK since 2010, he began to pour money into the stock in 2017 with two 50% increases.

From a Street perspective, analysts are divided on BK’s outlook. We can see that BK has a Moderate Buy analyst consensus rating with This includes a recent stock upgrade (from Morgan Stanley) and a downgrade (JP Morgan).

Somewhere in the middle we have one of TipRanks’ Top 10 analysts, Vining Sparks’ Marty Mosby. He maintains his Hold rating on BK with a $60 price target (3.5% upside potential). This is slightly under the average analyst price target of $61.39.

He sees growth ahead but adds a note of caution:

“Looking into 2018E, we believe that BK is still positioned to generate another year of double-digit growth in earnings per share, as its tax rate is reduced and share count continues to be managed lower; however, we believe most of this upcoming benefit is currently priced into BK’s current valuation.”

Warren Buffett Stock Picks: Teva (TEVA)

Buffett surprised the market with a big bet on flailing pharma giant Teva Pharmaceutical Industries Ltd (ADR) (NYSE:TEVA). He snapped up 19 million shares in TEVA, worth about $358 million. This is the only new position initiated by Buffett in Q4. On the news Teva shares climbed over 10%.

But this bump turned out to be short-lived. Shares fell after the Oracle of Omaha revealed that he has no idea why the fund bought Teva. It turns out that one of his investment deputies made the purchase. This isn’t so surprising. Teva is currently one of the most-shorted stocks on the market and has just begun a restructuring program to deal with its massive $35 billion debt burden.

However, given that shares are trading at just $19 vs the 5-year peak of over $70, perhaps this will be a bargain buy. And as Buffett famously says: When others are fearful, be greedy.

Indeed, five-star Mizuho analyst Irina Rivkind Koffler calls the stock a Buy. She sees the stock leaping by more than 10% to $23 in the coming months and says:

“We expect slow but gradual appreciation in TEVA shares. While the 2018 outlook introduced on the 4Q:17 call came in below expectations, we believe there is downside protection, and even longer-term upside to the stock.”

Overall, TipRanks shows TEVA has a Hold consensus rating from top analysts. These analysts have an average price target on Teva of $21- 8% upside from the current share price.

Warren Buffett Stock Picks: US Bancorp (USB)

Minneapolis based U.S. Bancorp (NYSE:USB) is the fifth largest US bank — and one of the top 10 holdings in the Berkshire portfolio. Following the purchase of almost 2 million USB shares in Q4, Buffett’s USB stake now totals $4.66 billion.

The bank has just announced a fine of $613 million for ‘willful’ anti-money laundering (AML) shortcomings from 2009-2014. “We regret and have accepted responsibility for the past deficiencies in our AML program,” said CEO Andy Cecere on Feb. 15. “Our culture of ethics and integrity demands that we do better.”

For five-star RBC Capital analyst Gerard Cassidy this $613 million resolution is ‘good news’. He says:

“USB has made significant investments to improve its risk controls in the intervening years, and we believe that today’s resolution will allow USB to move past this issue…[Ultimately] US Bancorp has demonstrated, through the compound annual growth rate of shareholders’ return over the last 10 to 20 years, to be consistently one of the best-performing banks in the US.”

He has a buy rating and $61 price target on USB (10% upside potential). Note that this analyst is currently the no.1 analyst on TipRanks for his precise stock picking ability.

In contrast, the Street is taking a backseat on USB right now. The stock has a Hold consensus rating while its average analyst price target of $59.95 indicates just over 7% upside potential.

Warren Buffett Stock Picks: Monsanto (MON)

Last but not least we have biotech giant Monsanto Company (NYSE:MON) — one of the world’s top suppliers of farm pesticides and seeds. Throughout 2017, Buffett made a number of bullish MON trades. Starting in Q4 2016 he initiated a position — which he then increased in both Q3 and Q4. Now the fund holds 11,708,747 MON shares worth close to $1.37 billion.

German drugs and pesticide group Bayer AG (ADR) (OTCMKTS:BAYRY) is planning a massive $66 billion takeover of Monsanto. The deal was supposed to go through in 2017, but it has been delayed by an antitrust review from the European Commission (EC). The EC will now deliver their verdict on or before April 5.

Bayer CEO Werner Baumann said on Feb 28:

“We see ourselves on a good path for the regulatory approvals that are still outstanding, In Europe, as far as the process goes, we are further along than in the USA, but in the USA we will certainly also make progress in the coming weeks.’’

Baumann also revealed that the company is planning to sell its entire veg-seed business to secure regulatory approval.

However, the Street is staying on the sidelines right now. With a “Hold” analyst consensus rating, analysts are predicting just 4.3% upside from the current share price.

Buffett just went all-in on THIS new asset. Will you?

Buffett could see this new asset run 2,524% in 2018. And he's not the only one... Mark Cuban says "it's the most exciting thing I've ever seen." Mark Zuckerberg threw down $19 billion to get a piece... Bill Gates wagered $26 billion trying to control it...

What is it?

It's not gold, crypto or any mainstream investment. But these mega-billionaires have bet the farm it's about to be the most valuable asset on Earth. Wall Street and the financial media have no clue what's about to happen...And if you act fast, you could earn as much as 2,524% before the year is up.

Click here to find out what it is.

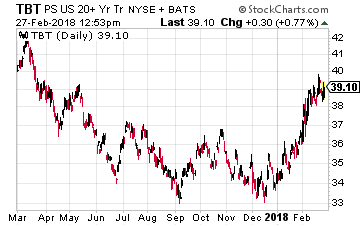

Source: Investor Place

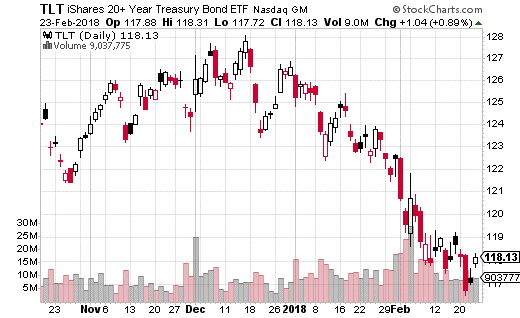

Then putting money into the ProShares UltraShort 20+Year Treasury ETF (NYSE: TBT) would make a lot of sense. This ETF uses futures and swaps to correspond to twice the inverse of the ICE U.S. Treasury 20+Year Bond Index. It is up 15% year-to-date thanks to the recent bond market scare, but is little changed over the past year.

Then putting money into the ProShares UltraShort 20+Year Treasury ETF (NYSE: TBT) would make a lot of sense. This ETF uses futures and swaps to correspond to twice the inverse of the ICE U.S. Treasury 20+Year Bond Index. It is up 15% year-to-date thanks to the recent bond market scare, but is little changed over the past year.