If you’re like many income investors I hear from, you’re probably worried that 2019 is already shaping up to be a repeat of 2008. The media doesn’t help – the talking heads like to conjure up fear because it draws eyeballs to the TV screen and clicks to Internet articles.

But what if they’re right? In a moment we’ll discuss the safest dividends for a serious pullback.

First, let me calm you down and add that a 2008 rerun is not our most likely scenario. As generals tend to fight the last war, investors tend to fear the last bear market. The next bear is likely to have its own unique “charm” – causes and effects – and we’d like to figure out that flavor ahead of time.

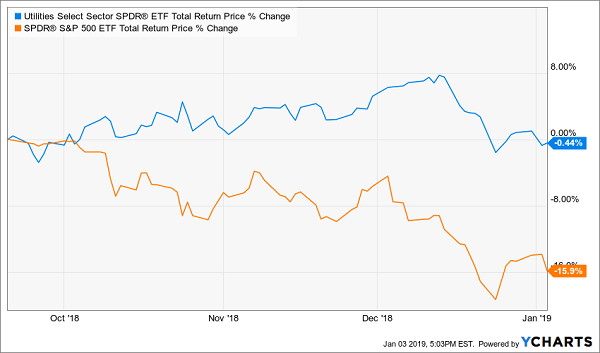

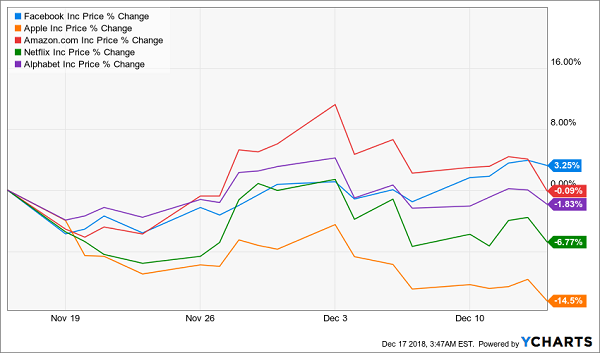

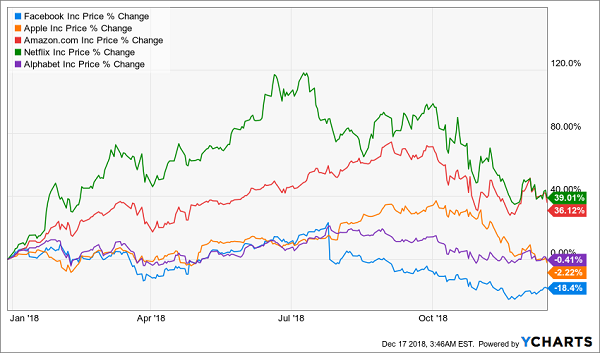

If there’s more to this pullback than we’ve seen, then its affinity for utility stocks is worth noting. The S&P 500 made its recent high on September 20, but don’t tell that to these dividend payers because they’ve shrugged off the broader market’s pullback

This Bear’s Favorite Buy: Utilities?

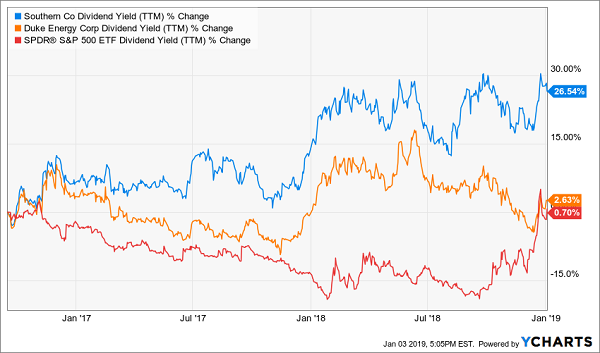

I’ve been down on the utility sector for two years now and have specifically picked on blue chips Duke Energy (DUK)and Southern Company (SO) repeatedly. I don’t have anything against these firms, but I also don’t recommend buying them when their stocks are pricey and their yields are low, as they are today.

The problem with “dividend desperation” – paying too high a price for too low a yield – is that you end up collecting your payout but losing as much or more in price when the stock’s multiple contracts to its usual levels. And that’s exactly what’s played out with DUK and SO. Their price-to-earnings (P/E) ratios have contracted by 5% and 6% respectively as investors pay less for the same dividend. This has resulted in total returns of… not much:

Our Utility Pans Treaded Water

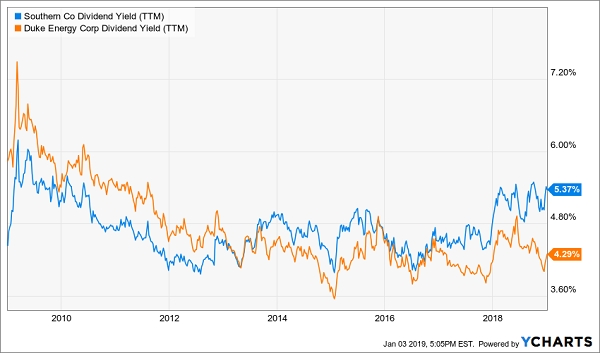

Is this recent “divergence” between these two large utilities and the broader market a significant tell? Perhaps, but neither stock interests me yet because both are still pricey. Their current P/Es, still around 20, are higher than they’ve been over much of the past decade. And their yields, at 4.3% and 5.4% respectively for DUK and SO, aren’t yet high enough to qualify for our 8% No Withdrawal Portfolio.

Fortunately we don’t have to settle for these pedestrian utility yields or their expensive stock prices. We can run these stocks through my Dividend Conversion Machine to double their yields to 8%, 9% and more – without adding any additional risk!

A Dividend Party Like It’s 2009

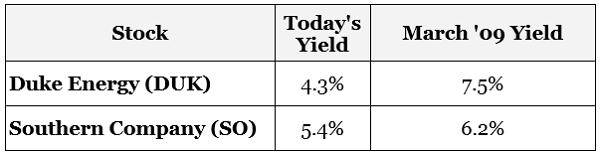

Nobody wants a repeat of 2008, but everyone wants another chance at 2009! Unfortunately most investors were too scared then to take advantage of once-in-a-lifetime yields. Our two utilities, for example, were paying their highest levels in years:

Generous Dividend Yields – For a Moment

More dividends for your dollar. Such were the “good times” that income investors could have enjoyed in 2009:

Why am I living in the past and telling you this now? Isn’t this an opportunity resigned to history forever? Fortunately NO – I’ve actually found a secret way for you to “force” blue chip names just like these to pay you massive, 2009-style dividend yields today.

Just Released: How to “Force” a 7.5% Dividend From Duke Energy

I’ve found 4 mysterious “Dividend Conversion Machines” that let you rewind the clock: buy stocks like Duke, but instead of grabbing today’s 4.4% dividend, you’ll get the same incredible 7.5% CASH payout folks who bought in 2009 bagged instead!

But there’s a vital difference: you won’t have to take a stomach-churning plunge to get it, like you would have back then.

Sure, handy slogans like “Buy when there’s blood in the streets” are easy to say. But actually overcoming fear and hitting the buy button at a time like that is almost impossible for most people.

But with these 4 amazing “Dividend Conversion Machines,” you’ll grab the same massive dividend yields the best blue chips were paying in that fleeting moment back in 2009 right now—TODAY.

And these life-changing payouts are safe, backed by these very same household-name stocks.

Massive Upside and 7.5% to 8%+ Dividends—in 1 Buy

What’s more, you can grab these lofty payouts whenever you’re ready: all at once, on an automatic yearly or monthly schedule … or simply whenever you have new money to invest.

It’s all up to you!

Best of all, each of these 4 incredible investments are about to explode and give us massive price upside, too.

How massive?

I’m talking 20%+ yearly price gains, on top of dividends of 8%, 10% and up—without having to buy in the middle of a meltdown, like our 2009 buyers did.

Editor's Note: The stock market is way up – and that’s terrible news for us dividend investors. Yields haven’t been this low in decades! But there are still plenty of great opportunities to secure meaningful income if you know where to look. Brett Owens' latest report reveals how you can easily (and safely) rake in 8%+ dividends and never worry about drawing down your capital again. Click here for full details!

Source: Contrarian Outlook

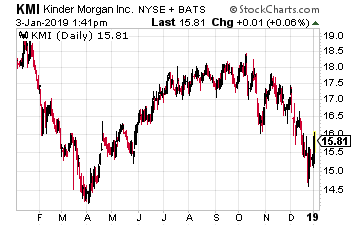

Kinder Morgan Inc. (NYSE: KMI) is one of the largest energy infrastructure companies in North America. The company owns an interest in or operate approximately 84,000 miles of pipelines and 152 terminals. The pipelines transport natural gas, gasoline, crude oil, carbon dioxide (CO2) and more. Terminals store and handle petroleum products, chemicals and other products.

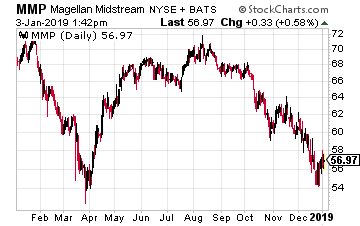

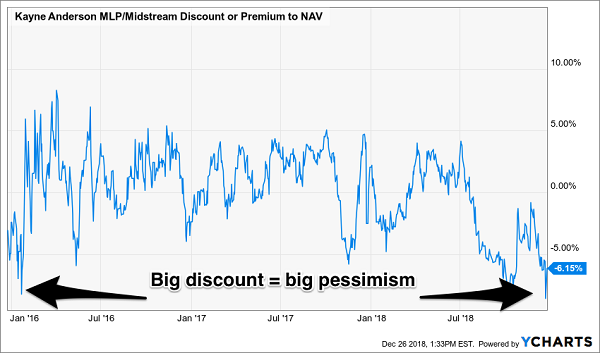

Kinder Morgan Inc. (NYSE: KMI) is one of the largest energy infrastructure companies in North America. The company owns an interest in or operate approximately 84,000 miles of pipelines and 152 terminals. The pipelines transport natural gas, gasoline, crude oil, carbon dioxide (CO2) and more. Terminals store and handle petroleum products, chemicals and other products. Magellan Midstream Partners LP (NYSE: MMP) is a publicly traded oil pipeline, storage and transportation company organized as an MLP. Currently, Magellan has 9,700-mile refined products pipeline system with 53 connected terminals as well as 26 independent terminals not connected to the pipeline system and an 1,100-mile ammonia pipeline system.

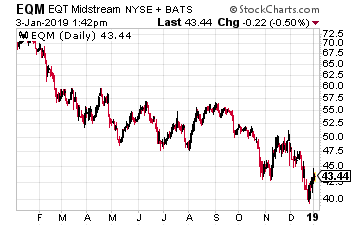

Magellan Midstream Partners LP (NYSE: MMP) is a publicly traded oil pipeline, storage and transportation company organized as an MLP. Currently, Magellan has 9,700-mile refined products pipeline system with 53 connected terminals as well as 26 independent terminals not connected to the pipeline system and an 1,100-mile ammonia pipeline system. EQT Midstream Partners LP (NYSE: EQM) is an MLP that owns and operates a natural gas transmission and storage system serving the Marcellus and Utica basins.

EQT Midstream Partners LP (NYSE: EQM) is an MLP that owns and operates a natural gas transmission and storage system serving the Marcellus and Utica basins.

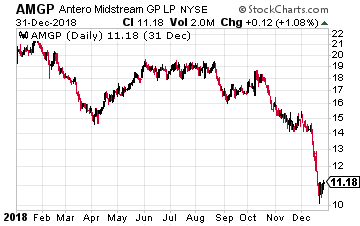

Antero Midstream GP LP (NYSE: AMGP) is an energy midstream services company in transition. The company came to market with a May 2017 IPO. The assets at that time were general partner incentive distribution rights (IDR) ownership interest in high growth, midstream MLP, Antero Midstream Partners (NYSE: AM). The MLP was sponsored and controlled by Marcellus natural gas producer Antero Resources (NYSE: AR).

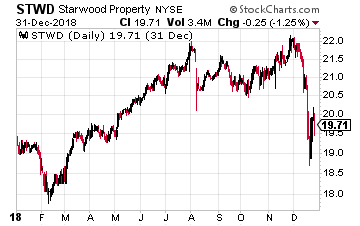

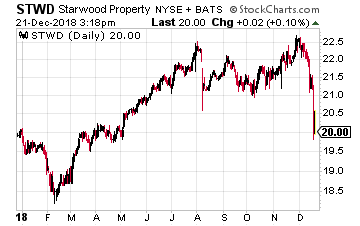

Antero Midstream GP LP (NYSE: AMGP) is an energy midstream services company in transition. The company came to market with a May 2017 IPO. The assets at that time were general partner incentive distribution rights (IDR) ownership interest in high growth, midstream MLP, Antero Midstream Partners (NYSE: AM). The MLP was sponsored and controlled by Marcellus natural gas producer Antero Resources (NYSE: AR). Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT whose primary business is the origination of commercial property mortgages. As one of the largest players in the field, Starwood Property trust focuses on making large loans with specialized terms. This gives them a competitive advantage over banks and smaller commercial finance REITs.

Starwood Property Trust, Inc. (NYSE: STWD) is a finance REIT whose primary business is the origination of commercial property mortgages. As one of the largest players in the field, Starwood Property trust focuses on making large loans with specialized terms. This gives them a competitive advantage over banks and smaller commercial finance REITs.

Starwood Property Trust (NYSE: STWD) is a commercial finance REIT. This means it originates mortgage loans for commercial properties, such as office buildings, hotels, and industrial buildings. Starwood has two commercial lending businesses. One is to make large dollar loans to retain in its portfolio.

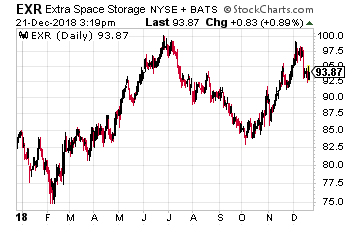

Starwood Property Trust (NYSE: STWD) is a commercial finance REIT. This means it originates mortgage loans for commercial properties, such as office buildings, hotels, and industrial buildings. Starwood has two commercial lending businesses. One is to make large dollar loans to retain in its portfolio. Self-storage REITs are the place to be when the economy gets rough for home ownership. Extra Space Storage (NYSE: EXR) is a large-cap, geographically diversified self-storage REIT.

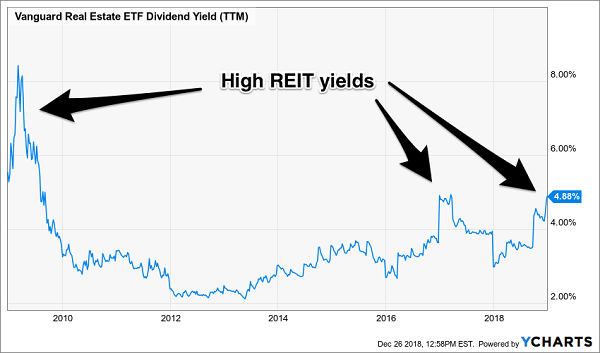

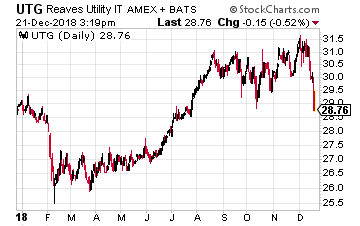

Self-storage REITs are the place to be when the economy gets rough for home ownership. Extra Space Storage (NYSE: EXR) is a large-cap, geographically diversified self-storage REIT. Utilities are supposed to be the safe sector when the stock market goes into a correction. This time utilities are down right along with the rest of the market sectors. Now is a great time to pick up shares of the Reaves Utility Income Fund NYSE: UTG).

Utilities are supposed to be the safe sector when the stock market goes into a correction. This time utilities are down right along with the rest of the market sectors. Now is a great time to pick up shares of the Reaves Utility Income Fund NYSE: UTG).

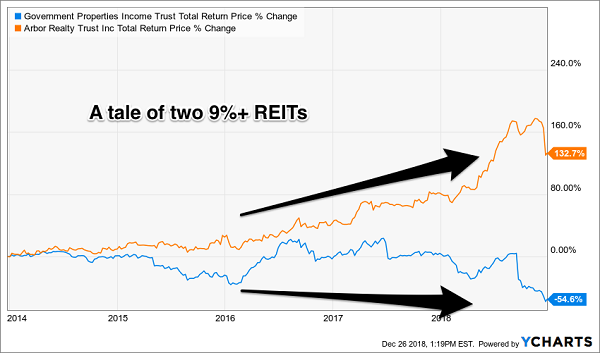

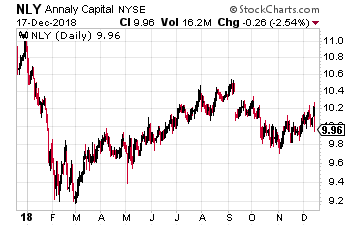

Annaly Capital Management, Inc. (NYSE: NLY) is a high-yield, agency MBS owning REIT. In its 2018 third quarter earnings report the company owned $91 billion worth of agency MBS.

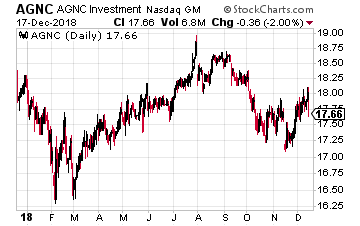

Annaly Capital Management, Inc. (NYSE: NLY) is a high-yield, agency MBS owning REIT. In its 2018 third quarter earnings report the company owned $91 billion worth of agency MBS. AGNC Investment Corp (Nasdaq: AGNC) is another agency MBS REIT. NLY and AGNC are the two largest companies in this REIT sector. As of the third quarter AGNC owned $70.9 billion of agency MBS.

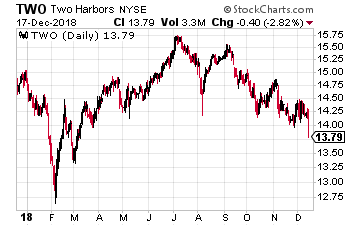

AGNC Investment Corp (Nasdaq: AGNC) is another agency MBS REIT. NLY and AGNC are the two largest companies in this REIT sector. As of the third quarter AGNC owned $70.9 billion of agency MBS. Two Harbors Investment Corp (NYSE: TWO) is a smaller agency MBS REIT that is trying to stay relevant with its recent merger with CYS Investments Inc (CYS).

Two Harbors Investment Corp (NYSE: TWO) is a smaller agency MBS REIT that is trying to stay relevant with its recent merger with CYS Investments Inc (CYS).

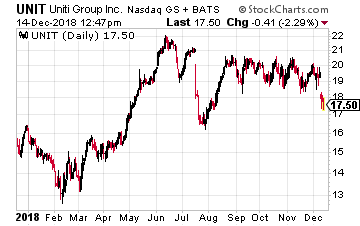

Uniti Group (Nasdaq: UNIT) is a telecommunications REIT focused on fiber optic assets. In recent years the company has focused on acquiring backhaul fiber assets. These are fiber connections between cell towers and the wired Internet.

Uniti Group (Nasdaq: UNIT) is a telecommunications REIT focused on fiber optic assets. In recent years the company has focused on acquiring backhaul fiber assets. These are fiber connections between cell towers and the wired Internet.

Main Street Capital (NYSE: MAIN) is a monthly dividend paying business development company (BDC). The company has also paid semi-annual, supplemental dividends since 2013. The next supplemental payout lands in investor brokerage accounts on December 27 and is equal to 150% of the normal monthly dividend.

Main Street Capital (NYSE: MAIN) is a monthly dividend paying business development company (BDC). The company has also paid semi-annual, supplemental dividends since 2013. The next supplemental payout lands in investor brokerage accounts on December 27 and is equal to 150% of the normal monthly dividend.